Aluminum Caps And Closures Market Size and Growth

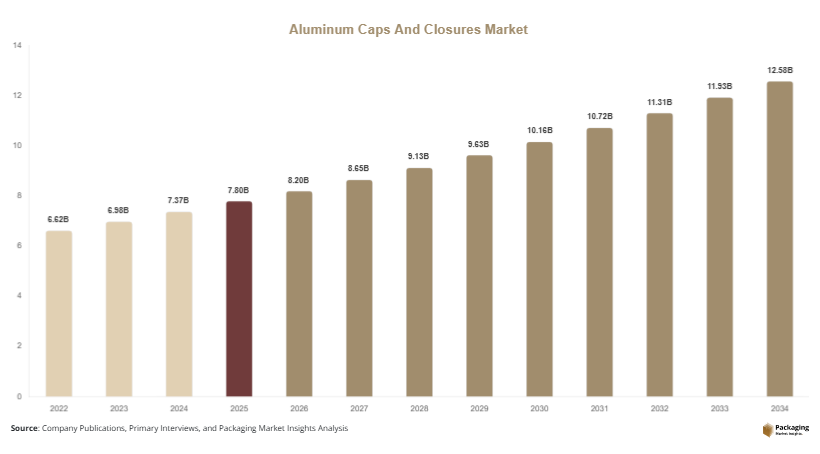

The global aluminum caps and closures market size was valued at approximately USD 7.8 billion in 2025 and is projected to reach USD 8.2 billion in 2026. With increasing adoption of recyclable and sustainable packaging materials, the market is forecasted to grow to USD 12.6 billion by 2034, registering a CAGR of 5.5% during the period from 2025 to 2034. This growth reflects a balanced combination of industrial demand, regulatory influence, and consumer preference for eco-conscious solutions. The aluminum caps and closures market is experiencing steady expansion, supported by rising demand from beverage, pharmaceutical, and personal care industries.

One of the primary growth factors is the expansion of the global beverage sector, particularly bottled water, carbonated drinks, and alcoholic beverages. Aluminum closures provide durability, resistance to corrosion, and reliable sealing, making them suitable for maintaining product quality. In addition, the pharmaceutical sector is contributing to demand growth due to the need for tamper-proof and contamination-resistant packaging. Aluminum closures ensure product safety and compliance with strict industry standards.

Key Market Insight

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Screw caps led the type segment with a 31.5% share, while roll-on pilfer-proof closures are expected to grow at a CAGR of 6.1%.

- Beverage packaging dominated with a 54.8% share, while pharmaceutical applications are forecasted to grow at a CAGR of 6.0%.

- Food & beverage end-use led the segment with 46.7% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 1.9 billion in 2025 and USD 2.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Preference for Sustainable and Recyclable Packaging

Sustainability has become a defining factor influencing the aluminum caps and closures market. Manufacturers and brand owners are actively shifting toward recyclable materials to reduce environmental impact and comply with evolving regulations. Aluminum closures offer a strong advantage as they can be recycled multiple times without degrading quality. This characteristic aligns well with circular economy initiatives adopted across several regions. Beverage companies are increasingly incorporating aluminum closures into their packaging strategies to meet sustainability targets and enhance brand perception. In addition, consumers are showing a growing preference for products packaged in eco-friendly materials, which is encouraging companies to invest in aluminum-based solutions.

Advancements in Manufacturing and Closure Design

Continuous improvements in manufacturing technologies are driving innovation in the aluminum caps and closures market. Companies are adopting automated production systems and advanced forming techniques to produce high-quality closures with reduced material usage. Lightweight aluminum closures are gaining traction as they lower transportation costs and improve operational efficiency. Enhanced sealing technologies are also being developed to ensure better product protection and extended shelf life. These innovations are particularly important for premium products, where packaging quality plays a key role in brand positioning. Customization capabilities are expanding as well, allowing manufacturers to offer visually appealing designs that meet specific client requirements.

Market Drivers

Expansion of the Global Beverage Industry

The growth of the global beverage industry continues to play a significant role in driving the aluminum caps and closures market. Increasing consumption of bottled beverages, including water, soft drinks, and alcoholic products, is creating strong demand for reliable closure solutions. Aluminum closures are widely used due to their ability to maintain product freshness and prevent leakage. Premiumization trends in the beverage sector are also contributing to demand, as manufacturers seek high-quality packaging that enhances product appeal. Wine and spirits producers are increasingly adopting aluminum screw caps for their convenience and performance advantages. This consistent growth in beverage consumption is expected to support long-term market expansion.

Rising Demand for Secure Pharmaceutical Packaging

The pharmaceutical sector is a major contributor to the demand for aluminum caps and closures. The need for safe, tamper-evident, and contamination-resistant packaging is increasing as global healthcare requirements expand. Aluminum closures provide strong barrier properties that help maintain the integrity of medicines and healthcare products. Regulatory standards in pharmaceutical packaging are becoming more stringent, encouraging the adoption of reliable materials such as aluminum. In addition, the growth of pharmaceutical manufacturing in emerging markets is creating new opportunities for closure manufacturers. The increasing focus on patient safety and product quality continues to drive demand in this segment.

Market Restraint

Fluctuations in Raw Material Prices and Supply Chain Challenges

The aluminum caps and closures market faces challenges related to volatility in raw material prices. Aluminum prices are influenced by factors such as energy costs, mining output, and global trade conditions. Sudden price fluctuations can increase production costs and impact profit margins for manufacturers. This situation creates uncertainty, particularly for smaller companies that have limited ability to absorb cost changes. Supply chain disruptions also pose a challenge, as delays in raw material availability can affect production schedules. For instance, disruptions in bauxite mining or refining processes can lead to shortages, impacting the overall supply of aluminum. These factors can slow market growth and create operational difficulties for industry participants.

Market Opportunities

Growth Potential in Emerging Economies

Emerging economies present strong growth opportunities for the aluminum caps and closures market. Rapid urbanization and rising disposable incomes are increasing the demand for packaged goods, particularly in Asia Pacific, Latin America, and parts of Africa. The expansion of retail networks and e-commerce platforms is further supporting the consumption of packaged food and beverages. As companies in these regions look for durable and sustainable packaging solutions, aluminum closures are gaining popularity. Government initiatives promoting industrial development and foreign investment are also creating a favorable environment for market expansion.

Development of Lightweight and Cost-Efficient Solutions

Innovation in lightweight aluminum closures is opening new avenues for market growth. Manufacturers are focusing on reducing material usage while maintaining performance and durability. Lightweight closures not only lower production costs but also reduce transportation expenses and environmental impact. These benefits make them attractive for large-scale beverage producers seeking efficiency improvements. Research and development efforts are enabling the creation of advanced designs that offer enhanced functionality without increasing costs. This focus on cost efficiency is particularly important in competitive markets where pricing plays a key role in purchasing decisions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Size in 2026 | USD 8.2 Billion |

| Market Size in 2034 | USD 12.6 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The screw caps segment held the largest share of the aluminum caps and closures market in 2024, accounting for approximately 31.5% of total revenue. These closures are widely used in beverage applications due to their ease of use, reusability, and strong sealing capabilities. They are particularly common in wine and spirits packaging, where maintaining product quality is essential. The growing demand for convenient packaging solutions continues to support the dominance of screw caps. Technological improvements in design and production are further enhancing their performance and visual appeal.

The roll-on pilfer-proof closures segment is projected to grow at the fastest CAGR of 6.1% during the forecast period. These closures provide enhanced security features, making them suitable for pharmaceutical and beverage applications. The increasing focus on product safety and regulatory compliance is driving demand for this segment. Manufacturers are developing advanced designs to improve efficiency and reduce material usage, supporting continued growth.

By Application

Beverage packaging accounted for the largest share of 54.8% in 2024, driven by the global demand for bottled drinks. Aluminum closures are preferred in this segment due to their durability and ability to preserve product quality. The expansion of the beverage industry, combined with increasing demand for premium products, is supporting growth.

Pharmaceutical packaging is expected to grow at a CAGR of 6.0% during the forecast period. The need for secure and contamination-free packaging is driving demand in this segment. Aluminum closures offer excellent barrier properties, ensuring product integrity. The growth of the pharmaceutical industry and strict regulatory standards are key factors supporting this trend.

By End-Use

The food & beverage segment dominated the market in 2024, accounting for 46.7% of total share. The high consumption of packaged food and drinks is driving demand for reliable closure solutions. Aluminum closures are widely used due to their ability to maintain freshness and prevent contamination.

The healthcare segment is projected to grow at a CAGR of 6.3%. Increasing demand for pharmaceutical products and secure packaging solutions is driving this growth. Aluminum closures provide strong protection against external factors, making them suitable for healthcare applications.

Aluminum Caps And Closures Market Segmentations

By Type

- Screw Caps

- Roll-On Pilfer-Proof Closures

- Crown Caps

- Others

By Application

- Beverage Packaging

- Pharmaceutical Packaging

- Personal Care

- Others

By End-Use

- Food & Beverage

- Healthcare

- Cosmetics

- Industrial

Regional Analysis

North America

North America accounted for approximately 22.5% of the aluminum caps and closures market share in 2025 and is projected to grow at a CAGR of 4.8% during the forecast period. The region benefits from a mature packaging industry and strong demand from beverage and pharmaceutical sectors. Increasing focus on sustainable materials is encouraging the adoption of aluminum closures across various applications, supported by regulatory initiatives promoting recycling.

The United States remains the dominant country in this region, driven by its large beverage production capacity and advanced manufacturing capabilities. A key growth factor is the rising demand for premium alcoholic beverages, which require high-quality closures. Continuous innovation in packaging technologies also supports market expansion.

Europe

Europe held a market share of 20.3% in 2025 and is expected to grow at a CAGR of 4.9%. The region is characterized by strict environmental regulations and a strong commitment to sustainability. Aluminum closures are gaining traction as companies seek alternatives to plastic packaging. The presence of established beverage industries further supports steady demand.

Germany leads the European market due to its strong industrial base and focus on eco-friendly solutions. A unique growth factor is the widespread use of aluminum closures in the wine industry, where they offer improved preservation and convenience. This trend continues to support market growth across the region.

Asia Pacific

Asia Pacific dominated the aluminum caps and closures market with a 38.2% share in 2025 and is projected to grow at a CAGR of 6.0%. Rapid urbanization and increasing population are driving demand for packaged products. The region’s expanding middle-class population is also contributing to higher consumption of beverages and pharmaceuticals.

China is the leading country in the region, supported by its large-scale manufacturing capabilities. A key growth factor is the rapid expansion of the beverage industry, particularly bottled water and carbonated drinks. Government initiatives promoting sustainable packaging further encourage the adoption of aluminum closures.

Middle East & Africa

The Middle East & Africa region accounted for 8.6% of the market share in 2025 and is expected to grow at a CAGR of 5.7%. Increasing demand for packaged beverages and pharmaceutical products is supporting market growth. Investments in manufacturing infrastructure are also contributing to regional development.

Saudi Arabia dominates the market in this region, driven by its expanding food and beverage sector. A unique growth factor is the high demand for bottled water due to climatic conditions. This creates consistent demand for durable and reliable aluminum closures.

Latin America

Latin America held a 10.4% share in 2025 and is projected to grow at a CAGR of 6.4%. The region is witnessing increasing consumption of packaged goods, supported by urbanization and changing lifestyles. The beverage industry remains a key driver of demand.

Brazil leads the regional market due to its strong beverage sector and large population. A unique growth factor is the growing awareness of sustainable packaging solutions. Regulatory initiatives and increasing consumer preference for eco-friendly materials are supporting market expansion.

Competitive Landscape

The aluminum caps and closures market is moderately competitive, with several global players focusing on innovation and sustainability. Amcor plc is a leading company due to its strong global presence and diverse product portfolio. The company has introduced lightweight aluminum closures to improve efficiency and reduce environmental impact.

Other companies are investing in research and development to enhance product quality and expand their market reach. Strategic partnerships and capacity expansions are common approaches used by key players to strengthen their positions.

Key Players List

- Amcor plc

- Crown Holdings Inc.

- Guala Closures Group

- Silgan Holdings Inc.

- Ball Corporation

- Berry Global Inc.

- Alcoa Corporation

- Tecnocap Group

- Closure Systems International

- Nippon Closures Co. Ltd.

- Herti JSC

- Mala Closure Systems

- Federfin Tech S.R.L.

- Cap & Seal Pvt. Ltd.

- Manaksia Ltd.