Caps And Closure Market Size and Growth

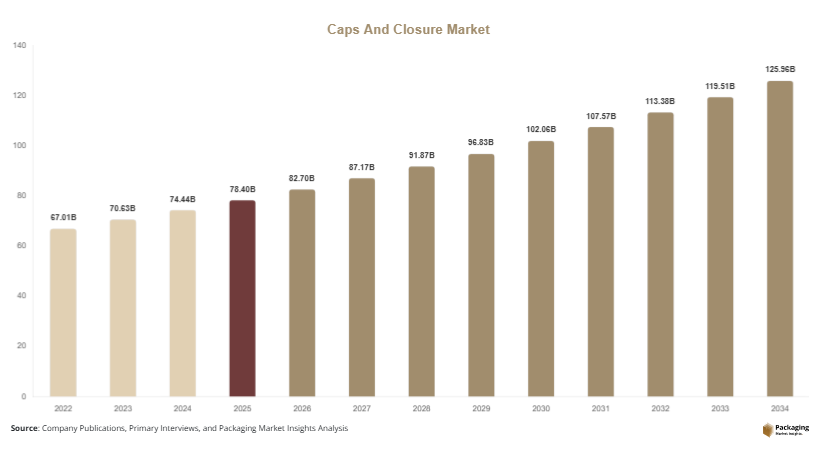

The global caps and closure market size is estimated at USD 78.4 billion in 2025 and is projected to reach USD 82.7 billion in 2026. By 2034, the market is forecast to reach USD 132.6 billion, registering a CAGR of 5.4% during 2025–2034. The caps and closure market continues to play a central role in the global packaging industry, supported by rising packaged product consumption, growing demand for convenience packaging, and increasing innovation in sustainable closure systems. Caps and closures are critical packaging components used across beverages, food products, pharmaceuticals, personal care, home care, and industrial packaging applications to ensure product safety, sealing integrity, contamination prevention, and consumer convenience.

One of the primary growth factors driving the market is the sustained expansion of packaged beverage demand. Carbonated drinks, bottled water, juices, dairy beverages, alcoholic beverages, and functional wellness drinks all require high-performance closure systems that offer tamper evidence, leak prevention, resealability, and shelf-life protection. Lightweight threaded caps, sports closures, tethered caps, and premium dispensing closures are seeing wider adoption as beverage packaging evolves toward convenience and regulatory compliance.

Key Highlights:

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.1%.

- Screw caps led the type segment with a 36.4% share.

- Plastic-based closures dominated with 67.2% share.

- Food & beverage applications led the segment with 49.3% share.

- The US remained the dominant country with a market size of USD 14.1 billion in 2025 and USD 14.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Tethered Closures

Sustainability is reshaping product development across the caps and closure market, particularly with growing adoption of tethered closures, lightweight resin caps, and recyclable mono-material closure systems. Regulatory shifts in packaging waste management are encouraging beverage companies and packaged goods manufacturers to redesign closure formats that remain attached to containers after opening, improving recycling capture rates and reducing litter generation. Large bottled beverage producers are increasingly transitioning to tethered cap systems for water, soft drinks, and dairy beverages. At the same time, resin optimization is reducing cap weight without compromising torque strength or sealing performance. Future market growth will increasingly be supported by closures designed for recyclability, lower material intensity, and compatibility with circular packaging systems.

Growth in Functional and Premium Dispensing Closures

Consumer demand for convenience packaging is accelerating adoption of advanced dispensing closures in food, beauty, healthcare, and household applications. Flip-top caps, trigger spray closures, dosage-control dispensers, precision pumps, and dual-dispensing systems are increasingly used to improve consumer usability and product differentiation. Personal care brands are adopting premium tactile closures with controlled dispensing for skincare, haircare, and wellness packaging, while condiment manufacturers increasingly use easy-flow dispensing caps that improve pouring control and reduce waste. In healthcare packaging, accurate dosage dispensing closures are becoming more common in liquid medicines and nutraceutical products. Over time, smart closure functionality, ergonomic design, and premium convenience features will continue driving value-added innovation across the market.

Market Drivers

Expansion of Packaged Beverage Consumption

The growing global consumption of packaged beverages remains a major demand driver for the caps and closure market. Bottled water, carbonated soft drinks, ready-to-drink tea, coffee beverages, dairy drinks, energy drinks, and sports beverages all require closure systems that provide leak prevention, tamper evidence, carbonation retention, and resealability. Beverage producers increasingly prioritize lightweight caps that reduce packaging material use while supporting high-speed filling operations. Sports caps and easy-open closures are also gaining wider adoption in convenience beverage formats. For example, premium hydration brands increasingly use ergonomic closures with improved grip design and controlled flow functionality. As packaged beverage consumption expands in urban markets worldwide, demand for innovative caps and closure systems is expected to remain strong.

Growth of Pharmaceutical and Healthcare Packaging

Healthcare packaging is becoming an increasingly important growth engine for the caps and closure market, driven by rising pharmaceutical production, growing home-based healthcare consumption, and increasing demand for tamper-resistant packaging systems. Prescription medicines, nutraceutical supplements, liquid formulations, diagnostic kits, and wellness packaging all rely on advanced closure systems that ensure safety, contamination control, and dosing precision. Child-resistant closures are increasingly used in over-the-counter medicines, while tamper-evident seals are becoming standard across pharmaceutical bottle packaging. Liquid medicine packaging increasingly requires dosage-control closures for accurate dispensing. Growth in online pharmacy distribution and consumer wellness packaging is further strengthening closure demand in healthcare channels globally.

Market Restraint

Volatility in Resin Prices and Material Supply Chains

Raw material price volatility remains a notable restraint for the caps and closure market, particularly for manufacturers dependent on polymer-based closure production. Polypropylene, polyethylene, specialty resins, and engineered polymers are widely used in cap and closure manufacturing, making producers sensitive to feedstock cost fluctuations, energy price shifts, and supply chain disruptions. Rising resin prices can compress manufacturer margins and increase pricing pressure across packaging supply chains. For example, beverage bottling companies operating at large scale often negotiate aggressively on closure pricing due to high-volume procurement, limiting supplier pricing flexibility during raw material inflation periods. Material shortages can also disrupt delivery schedules for packaging converters and consumer brands. Continued volatility may increase operational complexity and encourage material diversification strategies.

Market Opportunities

Expansion of Smart Closure Technologies

Smart packaging is creating strong opportunity in the caps and closure market, especially through connected closures integrated with authentication systems, freshness monitoring, dosage tracking, and consumer engagement tools. QR-enabled closures, NFC-integrated caps, anti-counterfeit sealing systems, and temperature-sensitive indicators are increasingly being explored across premium beverages, pharmaceuticals, and high-value packaged products. For example, premium spirits brands are adopting smart closures that enable digital authentication and traceable supply chain verification. In pharmaceuticals, connected closures can support dosage monitoring for consumer compliance packaging. As digital packaging ecosystems expand, intelligent closures are expected to become a commercially attractive high-value segment within the broader market.

Growth in Bio-Based and Compostable Closure Materials

The shift toward renewable packaging inputs is creating meaningful long-term opportunity for bio-based and compostable closures. Manufacturers are investing in plant-derived polymers, compostable resin blends, and renewable feedstock materials that reduce dependence on conventional fossil-based plastics. Foodservice beverage packaging, personal care refill packaging, and specialty organic products are early adopters of bio-based closure systems because sustainability positioning is closely linked to brand value. Improved material science is enhancing heat resistance, sealing performance, and structural integrity in bio-derived closures. As commercial scalability improves and regulatory support strengthens, bio-based closure materials are expected to create new growth opportunities across packaging markets globally.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.4 Billion |

| Market Size in 2026 | USD 82.7 Billion |

| Market Size in 2034 | USD 132.6 Billion |

| CAGR | 5.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Screw caps represented the dominant subsegment in the caps and closure market, accounting for 36.8% market share in 2024. Their leadership position is supported by wide usage across bottled water, carbonated beverages, dairy drinks, edible oils, sauces, pharmaceuticals, and household chemicals. Screw caps provide reliable sealing, strong leak resistance, easy resealability, and compatibility with automated high-speed bottling lines, making them highly preferred across mass-market packaging applications. Plastic threaded closures remain especially dominant due to lightweight performance and cost efficiency. Premium beverage producers are also introducing ergonomic threaded caps with improved grip texture and controlled opening torque. In pharmaceutical packaging, screw closures remain essential because they can be integrated with tamper-evident bands, child-resistant systems, and induction sealing liners. Their broad application range and manufacturing scalability continue supporting segment leadership.

Dispensing closures are projected to register the fastest growth, expanding at a CAGR of 6.5% during 2025–2034. Growth is being driven by rising consumer demand for convenience packaging, precise dispensing, reduced product waste, and improved user experience. Flip-top caps, trigger closures, squeeze-dispensing nozzles, pump dispensers, and dosage-control systems are increasingly used in condiments, skincare products, liquid medicines, household cleaners, and personal hygiene packaging. Brands are investing in premium dispensing functionality to differentiate products in crowded retail environments. Packaging innovation is also improving closure precision, leak prevention, and ergonomic usability. Sustainability-focused mono-material dispensing caps are further accelerating adoption because they improve recyclability while maintaining functional performance. As packaging becomes more user-centric, dispensing closures are expected to become a high-value growth category.

By Material

Plastic remained the dominant material segment, capturing 68.1% share in 2024 across the global caps and closure market. Polypropylene and polyethylene are the most widely used materials because they offer excellent molding flexibility, lightweight performance, chemical resistance, durability, and cost competitiveness. Plastic closures are used extensively in beverage bottles, dairy packaging, edible oils, pharmaceuticals, detergents, and cosmetic packaging. Their compatibility with precision molding technologies enables complex designs such as tamper-evident bands, flip-top mechanisms, child-resistant systems, and dispensing valves. Lightweighting initiatives have also improved resin efficiency without sacrificing sealing integrity. Recyclable mono-material cap systems are increasingly replacing mixed-material closure formats in packaged consumer goods. High-volume beverage bottlers continue prioritizing plastic closure systems because they combine low production cost with consistent functional performance across automated filling environments.

Bio-based closure materials are expected to witness the fastest growth, registering a CAGR of 6.8% through 2034. Increasing regulatory focus on sustainable packaging, corporate emission reduction goals, and consumer preference for renewable packaging solutions are driving this segment forward. Plant-derived polymers, compostable resin blends, and renewable feedstock plastics are emerging as commercially attractive closure alternatives in niche and premium packaging categories. Organic beverages, wellness products, natural cosmetics, and environmentally positioned household brands are early adopters of bio-based closure systems. Improvements in material engineering are enhancing heat tolerance, sealing strength, structural stability, and commercial scalability. As manufacturing costs decline and processing compatibility improves, bio-based closure materials are expected to expand into larger beverage and food packaging applications over the forecast period.

By End-Use

Food & beverage dominated the caps and closure market, accounting for 49.6% share in 2024. This dominance is supported by large-scale global consumption of bottled water, carbonated drinks, dairy beverages, juices, alcoholic beverages, sauces, edible oils, condiments, and packaged food products requiring reliable sealing systems. Caps and closures in this segment must maintain freshness, protect product quality, prevent contamination, and offer convenience features such as resealability and easy opening. Beverage producers increasingly use lightweight threaded closures, tethered caps, and premium sports caps to improve sustainability and functionality. Sauce and condiment manufacturers are adopting precision dispensing caps that improve flow control and reduce product waste. Food packaging innovation is also driving adoption of freshness-lock closures and tamper-evident sealing systems. The sheer scale of packaged food and beverage consumption continues to secure segment dominance.

Pharmaceutical applications are forecast to grow at the fastest CAGR of 6.2% during 2025–2034, driven by rising medicine production, growth in nutraceutical packaging, and increasing demand for safety-focused packaging formats. Child-resistant closures, tamper-evident caps, sterile dispensing systems, and dosage-control closures are becoming standard across prescription medicines, OTC formulations, liquid drugs, supplements, and wellness packaging. Home healthcare expansion is increasing packaging demand for accurate dispensing closures used in liquid medication bottles and therapeutic nutrition packaging. Anti-counterfeit closure technologies integrated with authentication features are also gaining commercial interest. Pharmaceutical packaging regulations are increasingly emphasizing closure integrity, contamination prevention, and consumer safety. As healthcare packaging volume rises globally, pharmaceutical closure demand is expected to deliver steady long-term market expansion.

Caps And Closure Market Segmentations

By Type

- Screw Caps

- Dispensing Closures

- Flip-Top Closures

- Snap-On Caps

- Cork Closures

- Child-Resistant Closures

- Tamper-Evident Closures

- Specialty Closures

By Material

- Plastic

- Metal

- Bio-Based Materials

- Composite Materials

- Rubber & Specialty Polymers

By End-Use

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Household Chemicals

- Industrial Packaging

- Automotive Fluids

- Agriculture Packaging

Regional Analysis

North America

North America accounted for 24.8% of the global caps and closure market share in 2025 and is projected to grow at a CAGR of 4.9% through 2034. Regional growth is supported by strong packaged beverage demand, a mature pharmaceutical industry, and broad adoption of premium dispensing closures across food, home care, and personal care packaging. Beverage companies are actively transitioning toward lightweight and tethered closure systems aligned with sustainability targets, while healthcare packaging demand continues supporting growth in tamper-evident and child-resistant closure formats. Increasing automation in bottling and packaging facilities is also strengthening demand for precision-engineered closures compatible with high-speed production lines.

The United States dominates the regional market. A unique growth driver is the rapid expansion of premium functional beverages, including protein drinks, hydration products, kombucha, and nutraceutical beverages, which increasingly use specialized dispensing and resealable cap systems. Many premium beverage brands now prioritize ergonomic closures, custom-molded caps, and value-added dispensing formats that improve consumer convenience and brand positioning. This premiumization trend continues to create strong closure innovation demand across U.S. beverage packaging markets.

Europe

Europe represented 21.5% market share in 2025 and is forecast to expand at a CAGR of 5.0% during the forecast period. The region is being shaped by strict packaging sustainability regulation, rising adoption of recyclable closure systems, and steady demand from food, beverages, pharmaceuticals, and personal care industries. Lightweight cap designs and tethered closures are gaining rapid acceptance as brands align with waste reduction goals. The region also has a strong presence of specialty closure manufacturers focused on premium dispensing systems, dosage-control technologies, and sustainable closure engineering. Packaging recyclability targets are significantly influencing closure redesign and resin selection strategies.

Germany remains the dominant country in Europe. A unique growth factor is strong industrial packaging demand, especially for automotive chemicals, industrial lubricants, specialty coatings, and precision chemical packaging that require high-integrity closure systems with leak resistance and controlled dispensing. Industrial packaging closures in Germany increasingly emphasize safety sealing, chemical compatibility, and durability under transport stress. This industrial packaging specialization provides a distinct demand base beyond conventional consumer packaging.

Asia Pacific

Asia Pacific held the leading 38.6% share in 2025 and is expected to register a CAGR of 5.8% through 2034, supported by rapid urbanization, rising packaged food consumption, expanding beverage manufacturing, and strong pharmaceutical production growth. Large-scale packaging production ecosystems across the region support cost-efficient closure manufacturing at high volume. Increasing bottled water demand, dairy beverage growth, condiment packaging expansion, and personal care product consumption are creating sustained demand for caps and closures. Manufacturers are also expanding recyclable closure production and lightweight designs to align with changing regulatory and sustainability requirements.

China dominates Asia Pacific because of its large beverage, food, and healthcare packaging industries. A unique growth driver is large-scale growth in ready-to-drink packaged tea, dairy beverages, and wellness beverage categories, all of which require specialized resealable closures and high-volume cap manufacturing capacity. Domestic packaging manufacturers continue investing in lightweight resin closure technologies, automated molding systems, and customized dispensing solutions to meet evolving brand requirements in China’s rapidly expanding packaged goods market.

Middle East & Africa

Middle East & Africa accounted for 6.3% of market share in 2025 and is projected to grow at a CAGR of 5.6% over the forecast period. Growth is being driven by increasing bottled water demand, expansion of packaged dairy products, and rising pharmaceutical packaging needs. Closure demand is also increasing in edible oils, sauces, cleaning chemicals, and personal hygiene products as packaged product penetration rises. Regional converters are investing in domestic cap manufacturing to reduce import dependence and improve supply responsiveness. Lightweight beverage closures and tamper-evident packaging systems are becoming increasingly common across food and healthcare applications.

The United Arab Emirates leads the regional market. A unique growth factor is the expansion of premium bottled water and wellness beverage exports, where high-quality closure systems are essential for shelf appeal, product safety, and export compliance. Premium beverage brands increasingly use custom-designed caps, enhanced tamper-evidence systems, and premium closure finishes to improve product differentiation in export markets, supporting strong specialized closure demand.

Latin America

Latin America accounted for 8.8% market share in 2025 and is projected to register the fastest CAGR of 6.1% through 2034, supported by rising packaged beverage consumption, increasing pharmaceutical production, and growing penetration of branded packaged food products. Demand for caps and closures is rising across bottled water, juices, edible oils, sauces, and home care packaging. Regional beverage bottlers are also investing in lightweight closure systems to reduce packaging cost and improve sustainability performance. Growth in urban retail and packaged convenience goods is expanding closure demand across multiple packaging formats.

Brazil dominates the Latin American market. A unique growth driver is strong expansion in fruit beverage and ready-to-drink juice packaging, where resealable closures, controlled-pour caps, and ergonomic threaded closure systems are seeing higher adoption. Beverage manufacturers are increasingly investing in branded closure design and lightweight molding technologies to improve shelf appeal while reducing packaging cost, creating strong long-term demand for closure innovation in Brazil.

Competitive Landscape

The global caps and closure market remains moderately consolidated, with multinational packaging companies competing through material innovation, lightweight closure engineering, dispensing technology development, and sustainability-focused portfolio expansion. Companies are increasingly investing in tethered closures, recyclable mono-material systems, premium dispensing caps, and smart packaging-enabled closure technologies to strengthen market positioning. Strategic acquisitions, regional manufacturing expansion, and long-term supply partnerships with beverage, pharmaceutical, and consumer packaged goods brands remain core competitive strategies.

Berry Global Inc. remains a leading player in the market due to its extensive global manufacturing footprint, advanced closure molding capabilities, and broad portfolio spanning beverage caps, dispensing closures, pharmaceutical closures, and industrial packaging systems. The company has recently expanded development of tethered beverage caps and lightweight recyclable closure solutions aligned with evolving sustainability regulations.

Amcor plc continues strengthening its closure portfolio through recyclable packaging integration and advanced dispensing systems. AptarGroup, Inc. maintains strong positioning in premium dispensing and pharmaceutical closure solutions. Silgan Holdings Inc. remains highly competitive in metal and plastic closure systems across beverage and food packaging, while Closure Systems International continues expanding lightweight beverage closure innovation for large bottling customers globally.

Key Players List

- Berry Global Inc.

- Amcor plc

- AptarGroup, Inc.

- Silgan Holdings Inc.

- Closure Systems International

- O.Berk Company

- Crown Holdings, Inc.

- Guala Closures Group

- Bericap GmbH & Co. KG

- Albéa Group

- UNITED CAPS

- Mold-Rite Plastics

- CL Smith Company

- Georg MENSHEN GmbH & Co. KG

- Weener Plastics Group

- Pact Group Holdings Ltd.

- Comar LLC

- Tecnocap Group