IV Fluid Bags Market Size and Growth

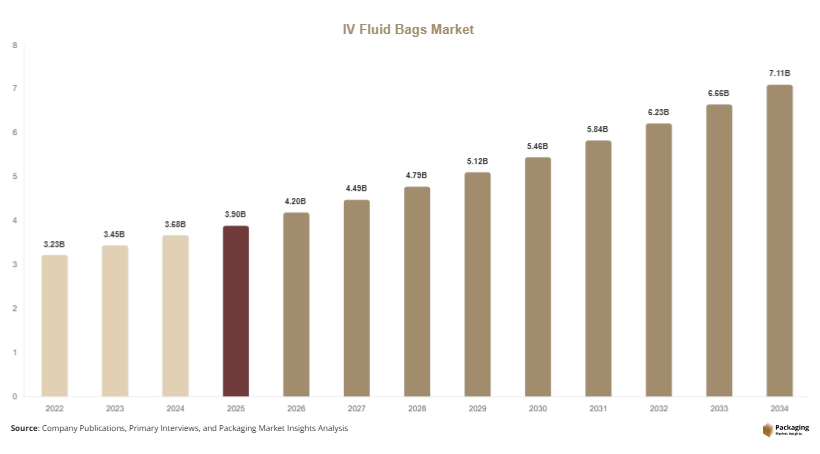

The global IV fluid bags market size is estimated at USD 3.9 billion in 2025 and is projected to reach USD 4.2 billion in 2026. Over the forecast period, the market is expected to grow steadily and reach approximately USD 7.6 billion by 2034, registering a CAGR of 6.8% from 2025 to 2034. This growth reflects increasing healthcare needs, expansion of medical infrastructure, and the rising burden of chronic and acute diseases. The IV fluid bags market is witnessing consistent growth due to the rising demand for intravenous therapies across healthcare systems worldwide. IV fluid bags are widely used for hydration, electrolyte balance, and drug delivery in hospitals, clinics, and home care settings.

One of the major growth factors supporting the IV fluid bags market is the increasing prevalence of chronic diseases such as diabetes, kidney disorders, and cardiovascular conditions. These conditions often require intravenous therapies for fluid management and medication delivery. In addition, the growing number of surgical procedures worldwide is driving demand for IV fluids, which are essential for maintaining patient stability during and after surgery. Another significant factor is the expansion of healthcare infrastructure in emerging economies. Governments and private organizations are investing in hospitals and healthcare facilities, which is increasing the demand for medical consumables, including IV fluid bags.

Key Highlights

- Asia Pacific dominated the market with a 35.9% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

- Large volume IV bags led the type segment with a 48.6% share, while small volume IV bags are expected to grow at a CAGR of 7.5%.

- Plastic materials dominated with a 61.4% share, while non-PVC materials are forecasted to grow at a CAGR of 7.9%.

- Hospital applications led the segment with 52.7% share, while home healthcare is expected to grow at a CAGR of 7.6%.

- China remained the dominant country with a market size of USD 0.9 billion in 2025 and USD 1.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing shift toward non-PVC and eco-friendly IV fluid bags

The IV fluid bags market is experiencing a gradual transition toward non-PVC materials due to concerns regarding environmental impact and patient safety. Traditional PVC-based IV bags contain plasticizers that may pose risks when used for certain medical applications. As a result, manufacturers are developing alternative materials such as polypropylene and polyethylene that offer improved safety profiles. These materials are also more environmentally friendly, aligning with global sustainability goals. Healthcare providers are increasingly adopting non-PVC IV bags to reduce environmental impact and comply with regulatory standards. This trend is expected to gain momentum as awareness about sustainable healthcare practices continues to grow.

Growing adoption of advanced sterile packaging technologies

Advancements in sterile packaging technologies are playing a significant role in shaping the IV fluid bags market. Manufacturers are focusing on improving sterilization methods to ensure product safety and extend shelf life. Technologies such as advanced sealing systems and multi-layer film structures are enhancing the durability and integrity of IV fluid bags. These innovations reduce the risk of contamination and leakage, which is critical in medical applications. In addition, automated manufacturing processes are improving consistency and efficiency in production. As healthcare providers prioritize patient safety and infection control, the demand for advanced sterile packaging solutions is expected to increase.

Market Drivers

Rising prevalence of chronic diseases and surgical procedures

The increasing prevalence of chronic diseases is a key factor driving the growth of the IV fluid bags market. Conditions such as diabetes, cancer, and kidney disorders often require intravenous therapies for treatment and management. In addition, the growing number of surgical procedures worldwide is contributing to the demand for IV fluids. These fluids are essential for maintaining hydration and delivering medications during surgeries. The rising burden of chronic diseases and the increasing demand for surgical interventions are expected to support market growth over the forecast period.

Expansion of healthcare infrastructure and services

The expansion of healthcare infrastructure, particularly in emerging economies, is significantly influencing the IV fluid bags market. Governments and private organizations are investing in hospitals, clinics, and healthcare facilities to improve access to medical services. This is increasing the demand for medical consumables, including IV fluid bags. In addition, the growth of home healthcare services is driving demand for portable and easy-to-use IV solutions. The increasing focus on improving healthcare accessibility and quality is expected to contribute to market growth.

Market Restraint

Risk of contamination and stringent regulatory requirements

The IV fluid bags market faces challenges related to the risk of contamination and strict regulatory requirements. IV fluid bags must meet stringent quality and safety standards to ensure patient safety. Any compromise in product quality can lead to serious health risks, including infections and complications. Manufacturers must adhere to rigorous testing and certification processes, which can increase production costs and complexity. For example, contamination during manufacturing or storage can result in product recalls and financial losses for companies. These challenges can limit market growth and create barriers for new entrants. Companies must invest in advanced manufacturing and quality control systems to mitigate these risks and ensure compliance with regulatory standards.

Market Opportunities

Increasing demand for home healthcare and ambulatory services

The growing demand for home healthcare services presents significant opportunities for the IV fluid bags market. Patients are increasingly opting for home-based treatments due to convenience and cost-effectiveness. IV fluid bags designed for home use are lightweight, portable, and easy to handle, making them suitable for ambulatory care. The aging population and rising prevalence of chronic diseases are further driving demand for home healthcare services. Companies that develop innovative and user-friendly IV solutions can capitalize on this growing trend.

Technological advancements in IV bag design and materials

Technological innovations in IV bag design and materials are creating new opportunities for market growth. Manufacturers are developing advanced IV bags with improved durability, flexibility, and safety features. Innovations such as multi-chamber bags and smart IV systems are enhancing the functionality of these products. These advancements allow for better drug compatibility and controlled delivery, improving patient outcomes. As healthcare providers seek more efficient and reliable solutions, the demand for advanced IV fluid bags is expected to increase.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.9 Billion |

| Market Size in 2026 | USD 4.2 Billion |

| Market Size in 2034 | USD 7.6 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Large volume IV bags dominated the market in 2024, accounting for approximately 48.6% of the share. These bags are widely used in hospitals for fluid replacement and hydration therapies. Their capacity to hold larger volumes makes them suitable for a variety of medical applications. The increasing number of hospital admissions and surgical procedures is driving demand for large volume IV bags.

Small volume IV bags are expected to grow at the fastest CAGR of 7.5% during the forecast period. These bags are used for administering medications and specialized treatments. The growing demand for targeted therapies and precision medicine is supporting the growth of this segment.

By Material

Plastic materials dominated the market in 2024, accounting for 61.4% of the share. Plastic IV bags are lightweight, flexible, and cost-effective, making them widely used in healthcare settings. They offer advantages such as ease of handling and reduced risk of breakage compared to glass bottles.

Non-PVC materials are expected to grow at the fastest CAGR of 7.9%. Increasing concerns about environmental impact and patient safety are driving the adoption of non-PVC IV bags. These materials offer improved safety and sustainability, supporting their growth in the market.

By End-Use

Hospitals dominated the market in 2024, accounting for 52.7% of the share. Hospitals are the primary users of IV fluid bags due to the high volume of patients requiring intravenous therapies. The increasing number of hospital admissions is driving demand for these products.

Home healthcare is expected to grow at the fastest CAGR of 7.6%. The increasing preference for home-based treatments is driving demand for portable and easy-to-use IV solutions. This trend is expected to support market growth.

IV Fluid Bags Market Segmentations

By Type

- Large Volume IV Bags

- Small Volume IV Bags

By Material

- Plastic

- Non-PVC

By End-Use

- Hospitals

- Clinics

- Home Healthcare

Regional Analysis

North America

North America accounted for a market share of 32.5% in 2025 and is expected to grow at a CAGR of 6.3% during the forecast period. The region benefits from a well-established healthcare system and high healthcare expenditure. The presence of leading medical device manufacturers and advanced technologies supports market growth. Increasing demand for intravenous therapies is driving the adoption of IV fluid bags.

The United States dominates the regional market due to its large healthcare infrastructure and high number of surgical procedures. A key growth factor is the increasing adoption of advanced medical technologies, which is improving patient care and driving demand for high-quality IV fluid bags.

Europe

Europe held a market share of 26.7% in 2025 and is projected to grow at a CAGR of 6.1%. The region is characterized by strong regulatory frameworks and a focus on patient safety. The increasing prevalence of chronic diseases is driving demand for IV therapies. The presence of established healthcare systems supports market growth.

Germany leads the European market due to its advanced healthcare infrastructure and strong medical device industry. A unique growth factor is the increasing adoption of non-PVC IV bags, which aligns with environmental and safety regulations.

Asia Pacific

Asia Pacific dominated the market with a 35.9% share in 2025 and is projected to grow at a CAGR of 7.1%. Rapid urbanization, increasing healthcare investments, and a growing population are driving demand for IV fluid bags. The expansion of healthcare facilities further supports market growth.

China is the dominant country in the region due to its large population and growing healthcare sector. A key growth factor is the government’s investment in healthcare infrastructure, which is increasing the demand for medical consumables.

Middle East & Africa

The Middle East and Africa region held a market share of 2.3% in 2025 and is expected to grow at a CAGR of 6.5%. The region is experiencing gradual growth due to increasing healthcare investments and improving infrastructure. The demand for IV therapies is rising with the expansion of healthcare services.

Saudi Arabia is a leading market in the region due to its focus on healthcare development. A unique growth factor is the increasing investment in hospital infrastructure, which is driving demand for IV fluid bags.

Latin America

Latin America accounted for 2.6% of the market share in 2025 and is projected to grow at a CAGR of 7.2%. The region is witnessing growth due to improving healthcare access and increasing demand for medical treatments. The expansion of healthcare facilities supports market growth.

Brazil dominates the Latin American market due to its large population and growing healthcare sector. A key growth factor is the increasing demand for intravenous therapies, which is driving the adoption of IV fluid bags.

Competitive Landscape

The IV fluid bags market is moderately competitive, with several global and regional players focusing on product innovation and expansion strategies. Baxter International Inc. is recognized as a leading player due to its strong product portfolio and global presence. The company continues to invest in research and development to introduce advanced IV solutions.

Other major players include B. Braun Melsungen AG, Fresenius Kabi AG, ICU Medical Inc., and Renolit SE. These companies are focusing on strategic partnerships and product launches to strengthen their market position. A recent development includes the introduction of non-PVC IV fluid bags to address environmental and safety concerns. The competitive landscape is characterized by continuous innovation and a focus on improving product quality and safety.

Key Players List

- Baxter International Inc.

- B. Braun Melsungen AG

- Fresenius Kabi AG

- ICU Medical Inc.

- Renolit SE

- JW Life Science

- Otsuka Pharmaceutical Co., Ltd.

- Kraton Corporation

- Sippex IV bag manufacturer

- Shanghai Solve Care Co., Ltd.

- PolyCine GmbH

- Sealed Air Corporation

- Amcor plc

- West Pharmaceutical Services, Inc.

- Pfizer CentreOne