Biodegradable Paper Plastic Packaging Market Size and Growth

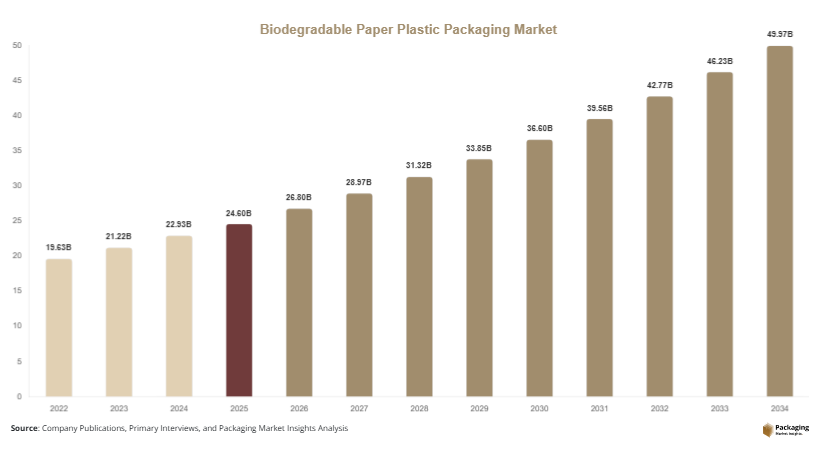

The global biodegradable paper plastic packaging market size is estimated at USD 24.6 billion in 2025 and is projected to reach USD 26.8 billion in 2026. By 2034, the market is expected to attain approximately USD 49.7 billion, registering a CAGR of 8.1% during the forecast period (2025–2034). Market growth is being driven by increasing regulatory pressure to reduce plastic pollution, advancements in biodegradable material technologies, and rising demand from sustainable consumer product brands.

One of the primary growth factors is the global shift toward circular economy initiatives, encouraging businesses to adopt packaging materials that can decompose naturally after disposal. Another major growth driver is the expansion of sustainable food service packaging, where restaurants, retailers, and food delivery companies are replacing conventional plastics with biodegradable alternatives. Additionally, continuous innovation in biodegradable polymers, coated paper packaging, and compostable packaging structures is improving functionality and expanding application opportunities.

Key Market Insights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 8.8%.

- Biodegradable plastic packaging led the type segment with a 56.2% share.

- Paper-based materials dominated the material segment with a 53.4% share.

- Food & beverage applications led the end-use segment with a 47.3% share.

- The US remained the dominant country with a market size of USD 4.9 billion in 2025 and USD 5.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Compostable Packaging Solutions

A major trend shaping the biodegradable paper plastic packaging market is the growing adoption of compostable packaging across food service, retail, and e-commerce sectors. Governments and corporations are implementing sustainability programs that prioritize materials capable of decomposing under industrial or home composting conditions. Food delivery companies, coffee chains, and grocery retailers are increasingly replacing conventional packaging with compostable paper containers, trays, and biodegradable films. For example, several global food service brands have introduced compostable packaging for takeaway products to reduce landfill waste. The future impact of this trend is expected to be substantial as composting infrastructure expands globally and consumers increasingly demand environmentally responsible packaging alternatives.

Development of High-Performance Bio-Based Materials

Manufacturers are investing heavily in the development of advanced bio-based packaging materials that combine sustainability with strong functional performance. Traditional biodegradable materials often faced challenges related to moisture resistance and durability, but new innovations are improving their commercial viability. For instance, biodegradable coatings and multilayer bio-based films are being developed to support food preservation and industrial packaging requirements. Companies are introducing packaging solutions made from renewable feedstocks such as corn starch, sugarcane, cellulose, and agricultural residues. Looking forward, continued material innovation is expected to broaden the application scope of biodegradable packaging and enable greater replacement of conventional petroleum-based plastics.

Market Drivers

Stringent Regulations on Single-Use Plastics

Government regulations restricting the use of single-use plastics are a major driver of the biodegradable paper plastic packaging market. Many countries have introduced bans, taxes, and compliance standards targeting traditional plastic packaging materials. These regulatory measures are encouraging businesses to transition toward biodegradable alternatives that align with environmental objectives. For example, food retailers and consumer goods manufacturers are replacing plastic bags, containers, and wrapping materials with biodegradable options to comply with evolving regulations. The direct effect of these policies is increased investment in sustainable packaging innovation and expanded market demand. As environmental legislation becomes stricter, adoption of biodegradable packaging solutions is expected to accelerate further.

Growing Consumer Preference for Sustainable Packaging

Consumers are increasingly considering sustainability when making purchasing decisions, creating strong demand for biodegradable packaging solutions. Environmental awareness campaigns and concerns regarding plastic pollution have encouraged consumers to favor brands that demonstrate responsible packaging practices. Companies across food, cosmetics, and household product industries are responding by incorporating biodegradable paper and plastic packaging into product offerings. For example, organic food brands frequently utilize compostable packaging as part of their sustainability positioning. This growing consumer preference directly influences packaging procurement strategies and supports long-term market growth. As sustainability becomes a core brand value, demand for biodegradable packaging is expected to continue rising globally.

Market Restraint

Higher Production Costs Compared to Conventional Packaging

A significant restraint affecting the biodegradable paper plastic packaging market is the higher production cost associated with biodegradable materials compared to conventional plastics. Biodegradable polymers, specialty coatings, and renewable raw materials often require more complex manufacturing processes and higher input costs. These expenses can create pricing challenges, particularly in cost-sensitive industries where packaging budgets are tightly controlled. For example, small and medium-sized food manufacturers may hesitate to transition fully to biodegradable packaging due to concerns about increased operational expenses. Limited composting infrastructure in certain regions further complicates adoption, reducing the perceived value proposition for some end users. Although economies of scale and technological advancements are gradually lowering costs, price competitiveness remains a key challenge that may limit market penetration in some segments during the forecast period.

Market Opportunities

Expansion of Sustainable E-Commerce Packaging

The rapid growth of e-commerce presents a significant opportunity for biodegradable packaging manufacturers. Online retailers are under increasing pressure to reduce packaging waste generated by shipping operations. Biodegradable paper mailers, compostable protective packaging, and sustainable cushioning materials are gaining popularity as alternatives to traditional plastic-based shipping materials. Major retailers are incorporating environmentally friendly packaging strategies to meet sustainability commitments and improve brand perception. Future growth opportunities are expected to emerge from cross-border e-commerce, subscription services, and direct-to-consumer business models, all of which require innovative and sustainable packaging solutions.

Rising Adoption in Healthcare and Pharmaceutical Packaging

Healthcare and pharmaceutical sectors represent an emerging opportunity for biodegradable packaging solutions. Increasing focus on sustainability within healthcare supply chains is encouraging adoption of eco-friendly packaging materials for medical products, over-the-counter medications, and healthcare consumables. Biodegradable paper and bio-based plastic packaging are being evaluated for applications requiring environmental responsibility without compromising product protection. Future innovations in barrier coatings, sterilization-compatible materials, and bio-based protective packaging are expected to support broader adoption. As healthcare organizations strengthen sustainability initiatives, biodegradable packaging suppliers are likely to benefit from expanding application opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 24.6 Billion |

| Market Size in 2026 | USD 26.8 Billion |

| Market Size in 2034 | USD 49.7 Billion |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Biodegradable plastic packaging dominated the market in 2024, accounting for approximately 56.2% of total revenue. The segment's leadership is driven by its ability to offer functionality similar to conventional plastics while providing improved environmental performance. Biodegradable plastic packaging is widely utilized in food containers, flexible films, shopping bags, and protective packaging applications. Manufacturers increasingly favor biodegradable plastics because they can often be integrated into existing packaging formats with minimal design changes. Industry examples include compostable food service products and biodegradable e-commerce packaging materials. Ongoing material innovation is improving durability, barrier performance, and processing efficiency, further strengthening the segment's market position.

Biodegradable paper packaging is expected to register the fastest CAGR of 8.9% through 2034. Growth is being driven by rising consumer preference for fiber-based packaging and increasing restrictions on plastic usage. Paper packaging solutions are gaining popularity across food service, retail, and consumer goods sectors due to their renewable nature and high recyclability. Manufacturers are introducing advanced coated paper products capable of delivering moisture resistance and enhanced performance. Future growth is expected to be supported by innovations in barrier technology and increasing investments in sustainable forestry and paper production.

By Material

Paper-based materials held the largest market share in 2024, representing approximately 53.4% of total market revenue. The dominance of this segment reflects strong demand for renewable and recyclable packaging solutions. Paper materials are extensively used for cartons, bags, wrapping materials, trays, and e-commerce packaging. The segment benefits from established recycling infrastructure and widespread consumer acceptance. Industry examples include paper takeaway containers, corrugated packaging, and molded fiber packaging solutions. Continuous improvements in paper processing technologies and biodegradable coatings are enhancing functionality and supporting broader adoption across multiple industries.

Starch-based biodegradable plastics are projected to be the fastest-growing material segment, expanding at a CAGR of 9.2% through 2034. Increasing demand for compostable materials and renewable feedstocks is supporting growth. These materials are derived from agricultural resources such as corn and potatoes, making them attractive alternatives to petroleum-based plastics. Packaging manufacturers are utilizing starch-based materials for films, bags, and food packaging applications. Future opportunities are expected to arise from advances in material formulations that improve strength, flexibility, and moisture resistance while maintaining biodegradability.

By End-Use

Food & beverage applications accounted for the largest market share in 2024, contributing approximately 47.3% of total revenue. The segment benefits from growing demand for sustainable packaging solutions capable of reducing environmental impact while maintaining food quality. Restaurants, food delivery providers, and packaged food manufacturers are increasingly adopting biodegradable packaging products. Industry examples include compostable trays, biodegradable cups, paper containers, and bio-based flexible packaging. Regulatory pressure to reduce plastic waste and increasing consumer preference for sustainable food packaging continue to support segment growth. As global food consumption rises, demand for biodegradable packaging solutions is expected to remain strong.

Healthcare packaging is anticipated to be the fastest-growing end-use segment, registering a CAGR of 8.7% during the forecast period. Sustainability initiatives within healthcare systems are encouraging adoption of biodegradable packaging materials for medical products and pharmaceutical applications. Manufacturers are developing specialized biodegradable packaging capable of meeting healthcare performance standards while reducing environmental impact. Future growth is expected to be supported by innovations in sterile packaging, protective materials, and bio-based barrier technologies. Increasing environmental commitments among healthcare providers will likely accelerate adoption over the coming years.

Biodegradable Paper Plastic Packaging Market Segmentations

By Type

- Biodegradable Plastic Packaging

- Biodegradable Paper Packaging

By Material

- Paper-Based Materials

- Starch-Based Biodegradable Plastics

- PLA-Based Materials

- Cellulose-Based Materials

- Other Bio-Based Materials

By End-User

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- E-Commerce

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 27.8% of the global biodegradable paper plastic packaging market share in 2025 and is expected to expand at a CAGR of 7.6% through 2034. Market growth is supported by strong consumer demand for environmentally friendly products, increasing corporate sustainability commitments, and expanding adoption of compostable packaging solutions. Food service providers, retailers, and e-commerce companies are actively replacing traditional plastic packaging with biodegradable alternatives. Growing investments in packaging innovation and waste reduction initiatives are further contributing to regional growth. The region also benefits from increasing collaboration between packaging manufacturers and consumer goods companies focused on achieving sustainability targets.

The United States dominates the regional market. A unique growth driver is the widespread adoption of corporate environmental, social, and governance (ESG) strategies. Major consumer brands are implementing sustainable packaging goals that prioritize biodegradable materials. A notable industry trend involves the use of compostable mailers and paper-based packaging solutions within the e-commerce sector. As sustainability reporting requirements become increasingly important, businesses are expected to accelerate investments in biodegradable packaging technologies.

Europe

Europe held approximately 26.1% market share in 2025 and is forecast to grow at a CAGR of 7.9% during the forecast period. The region benefits from strict environmental regulations, ambitious plastic waste reduction targets, and high levels of consumer environmental awareness. Governments are encouraging the adoption of biodegradable packaging through policy initiatives and sustainability frameworks. Food packaging, personal care products, and retail packaging are among the major application areas driving market demand. Growing investments in composting infrastructure and recycling systems are also supporting the adoption of biodegradable materials across European markets.

Germany remains the dominant country in Europe. A unique growth factor is the country's advanced circular economy initiatives that encourage sustainable packaging innovation. Packaging companies are increasingly investing in biodegradable barrier papers and compostable plastic alternatives to meet environmental targets. An emerging trend involves partnerships between retailers and packaging suppliers to introduce biodegradable packaging for private-label products. This collaborative approach continues to strengthen market growth across the country.

Asia Pacific

Asia Pacific dominated the market with a 38.6% share in 2025 and is projected to register a CAGR of 8.9% through 2034. Rapid urbanization, growing packaged food consumption, and increasing environmental awareness are supporting regional demand. Governments across several countries are introducing policies aimed at reducing plastic waste and promoting sustainable materials. Expanding manufacturing capabilities and rising investments in bio-based material production are also contributing to market growth. The region's large consumer base and strong industrial activity create substantial opportunities for biodegradable packaging manufacturers.

China leads the Asia Pacific market. A unique growth driver is the country's large-scale restrictions on non-degradable plastic products. Packaging manufacturers are investing heavily in biodegradable plastics and paper-based alternatives to meet regulatory requirements. Industry trends indicate increasing adoption of biodegradable packaging within food delivery and retail sectors. These developments are expected to support continued market expansion throughout the forecast period.

Middle East & Africa

The Middle East & Africa represented approximately 3.8% of global market revenue in 2025 and is anticipated to grow at a CAGR of 8.1%. Increasing awareness regarding environmental sustainability and growing demand for packaged consumer products are supporting market growth. Governments and businesses are beginning to explore alternatives to traditional plastics, particularly within food service and retail applications. Rising tourism activities and hospitality sector expansion are also contributing to demand for sustainable packaging products. Investments in waste management infrastructure are expected to support future adoption of biodegradable packaging solutions.

The United Arab Emirates is the leading country within the region. A unique growth factor is the government's emphasis on sustainability initiatives aimed at reducing plastic waste. Hospitality operators, retailers, and food service companies are increasingly implementing biodegradable packaging solutions to align with environmental goals. Industry trends include the introduction of eco-friendly packaging programs by major retail chains. Such developments are expected to strengthen regional demand over the coming years.

Latin America

Latin America accounted for approximately 3.7% market share in 2025 and is expected to register the fastest CAGR of 8.8% through 2034. Growth is supported by increasing environmental awareness, expanding retail sectors, and growing demand for sustainable consumer products. Food packaging remains a key application area, with manufacturers seeking biodegradable alternatives to conventional plastic packaging. Regulatory initiatives focused on reducing plastic waste are also encouraging adoption. Rising foreign investment in sustainable packaging manufacturing is contributing to market expansion across several countries.

Brazil dominates the Latin American market. A unique growth driver is the availability of renewable agricultural feedstocks used in bio-based packaging production. Packaging companies are utilizing sugarcane-derived materials and agricultural by-products to produce biodegradable packaging solutions. An emerging trend involves the growing use of biodegradable packaging for fresh produce exports. This focus on sustainable agricultural supply chains is expected to support long-term market growth.

Competitive Landscape

The biodegradable paper plastic packaging market is characterized by growing competition among packaging manufacturers, material suppliers, and sustainability-focused innovators. Companies are investing in research and development, production capacity expansion, and strategic collaborations to strengthen market positions and address increasing demand for environmentally responsible packaging solutions.

Mondi plc is recognized as a leading participant in the market due to its broad portfolio of sustainable packaging products and continued investments in biodegradable and recyclable materials. The company recently expanded its paper-based packaging solutions portfolio to support growing demand from food and consumer goods sectors.

Other major companies include Smurfit Kappa Group, Amcor plc, Stora Enso Oyj, and Huhtamaki Oyj. These organizations are focusing on material innovation, renewable feedstocks, compostable packaging technologies, and strategic partnerships with consumer brands. Capacity expansion initiatives and investments in bio-based materials remain key competitive strategies. Sustainability certifications and circular economy initiatives are increasingly influencing competitive positioning across the market.

Key Players List

- Mondi plc

- Smurfit Kappa Group

- Amcor plc

- Stora Enso Oyj

- Huhtamaki Oyj

- DS Smith plc

- WestRock Company

- International Paper Company

- Graphic Packaging International

- UPM-Kymmene Corporation

- TIPA Corp Ltd.

- NatureWorks LLC

- Novamont S.p.A.

- Vegware Ltd.

- Biopak Pty Ltd.

- Sealed Air Corporation

- BASF SE

- Berry Global Inc.