Active Smart And Intelligent Packaging Market Size and Growth

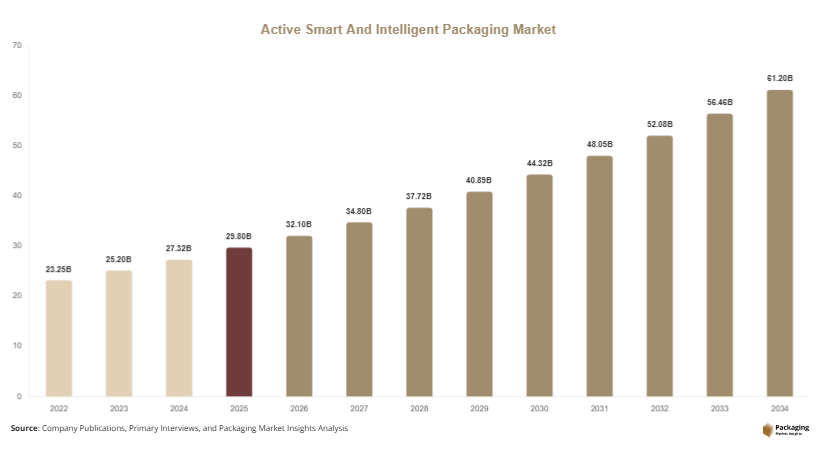

The global active smart and intelligent packaging market size is estimated at USD 29.8 billion in 2025 and is projected to reach USD 32.1 billion in 2026. By 2034, the market is forecast to reach approximately USD 61.4 billion, registering a CAGR of 8.4% during the forecast period (2025–2034). Rising concerns regarding food waste, increasing demand for supply chain transparency, and growing adoption of connected packaging technologies are among the major factors driving market expansion.

One of the primary growth factors is the increasing implementation of intelligent packaging solutions in food and pharmaceutical industries. Temperature indicators, freshness sensors, RFID tags, and QR-code-enabled packaging are helping manufacturers improve product monitoring and consumer trust. Another significant growth factor is the rapid expansion of e-commerce and omnichannel retailing, which requires advanced tracking and authentication technologies. Additionally, stricter regulations concerning food safety, pharmaceutical integrity, and product traceability are encouraging the adoption of smart packaging technologies worldwide.

Key Market Insights

- Asia Pacific dominated the market with a 39.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 9.0%.

- Active packaging led the type segment with a 36.8% share.

- Plastic-based materials dominated with a 50.6% share.

- Food & beverage applications led the end-use segment with 45.1% share.

- The US remained the dominant country with a market size of USD 5.8 billion in 2025 and USD 6.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Connected Packaging Through IoT and Digital Technologies

The active smart and intelligent packaging market is witnessing rapid adoption of connected packaging technologies that utilize IoT, NFC, RFID, and QR-code integration. Brands are increasingly embedding digital features into packaging to improve supply chain visibility and consumer interaction. For example, food manufacturers are deploying smart labels that allow consumers to verify product authenticity, monitor freshness, and access detailed sourcing information through mobile devices. Pharmaceutical companies are also implementing connected packaging systems to improve product traceability and combat counterfeiting. The future impact of this trend is expected to be significant as digital transformation accelerates across industries. Connected packaging will likely become an essential tool for real-time product monitoring, consumer engagement, and data-driven supply chain management.

Growing Adoption of Active Packaging for Shelf-Life Extension

Active packaging technologies designed to extend product shelf life are gaining momentum across food and healthcare sectors. Oxygen scavengers, moisture absorbers, antimicrobial agents, and ethylene absorbers are increasingly integrated into packaging systems to preserve product quality. For instance, fresh produce suppliers are utilizing active packaging solutions to reduce spoilage during transportation and retail display. This trend is helping companies minimize food waste while improving product safety and distribution efficiency. Looking ahead, advancements in biodegradable active packaging materials and smart preservation technologies are expected to further strengthen adoption. As sustainability and waste reduction become strategic priorities, active packaging will continue to play an increasingly important role in modern packaging systems.

Market Drivers

Rising Demand for Product Traceability and Supply Chain Transparency

Increasing demand for transparency throughout product supply chains is a major driver of the active smart and intelligent packaging market. Consumers, regulators, and retailers are seeking greater visibility into product origin, storage conditions, and distribution pathways. Intelligent packaging solutions provide real-time information regarding product status and authenticity. For example, pharmaceutical companies utilize RFID-enabled packaging to track medicines throughout distribution channels, reducing counterfeiting risks and improving compliance. The cause-and-effect relationship is clear: growing traceability requirements create demand for advanced monitoring technologies, which in turn drives market growth. As global supply chains become more complex, the need for intelligent packaging systems is expected to increase significantly.

Increasing Focus on Food Safety and Waste Reduction

Food safety concerns and efforts to reduce food waste are driving widespread adoption of active packaging technologies. Manufacturers are implementing packaging solutions capable of monitoring freshness and controlling environmental conditions to maintain product quality. For example, oxygen scavenger packaging is widely used in processed foods to prevent spoilage and extend shelf life. This not only reduces waste throughout the supply chain but also improves consumer satisfaction. Governments and regulatory agencies are also emphasizing food safety standards, encouraging adoption of advanced packaging technologies. The resulting demand for active packaging solutions is expected to remain a key market growth driver throughout the forecast period.

Market Restraint

High Implementation Costs and Technical Complexity

One of the primary restraints affecting the active smart and intelligent packaging market is the relatively high cost associated with advanced packaging technologies. Smart sensors, RFID tags, printed electronics, and active packaging components often increase production expenses compared to conventional packaging systems. Small and medium-sized manufacturers may face challenges in adopting these technologies due to budget limitations and technical expertise requirements. Additionally, integrating intelligent packaging systems into existing manufacturing and logistics operations can be complex. For example, pharmaceutical companies implementing RFID-based tracking systems must invest in compatible infrastructure and data management platforms. These additional costs can slow adoption, particularly in price-sensitive markets. Although technology costs are gradually declining, affordability and integration challenges remain important barriers influencing market penetration across several industries.

Market Opportunities

Growth of Smart Packaging in Pharmaceutical Applications

The pharmaceutical sector presents a major growth opportunity for active smart and intelligent packaging providers. Rising concerns regarding counterfeit medicines, product integrity, and regulatory compliance are increasing demand for intelligent packaging technologies. Smart labels, temperature indicators, and track-and-trace systems are becoming essential components of pharmaceutical supply chains. Future applications may include real-time patient monitoring, medication adherence tracking, and personalized healthcare packaging solutions. As biologics, specialty medicines, and temperature-sensitive therapies continue to expand globally, demand for advanced pharmaceutical packaging technologies is expected to increase substantially.

Development of Sustainable Intelligent Packaging Solutions

Sustainability initiatives are creating opportunities for the development of environmentally responsible active and intelligent packaging systems. Manufacturers are investing in biodegradable sensors, recyclable smart labels, and renewable material-based active packaging technologies. Brands increasingly seek solutions that combine functionality with reduced environmental impact. For example, paper-based intelligent packaging integrated with QR codes and digital authentication technologies is gaining traction among consumer goods manufacturers. Future opportunities are expected to emerge from circular economy initiatives and stricter environmental regulations. Companies capable of delivering sustainable smart packaging solutions are likely to benefit from growing demand across multiple industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 29.8 Billion |

| Market Size in 2026 | USD 32.1 Billion |

| Market Size in 2034 | USD 61.4 Billion |

| CAGR | 8.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Active packaging dominated the active smart and intelligent packaging market in 2024, accounting for approximately 36.8% of total market revenue. Its leadership is primarily attributed to widespread adoption across food and beverage applications where shelf-life extension and product preservation are critical. Technologies such as oxygen scavengers, moisture absorbers, antimicrobial packaging, and ethylene control systems are extensively utilized to maintain product freshness. Food manufacturers increasingly rely on active packaging to reduce spoilage and support long-distance distribution. Industry examples include fresh produce packaging, meat packaging, dairy products, and ready-to-eat meals. Regulatory pressure to reduce food waste and improve food safety further supports demand. Continuous innovation in active preservation technologies and sustainable packaging materials is reinforcing the segment's dominant market position.

Intelligent packaging is projected to be the fastest-growing type segment, expanding at a CAGR of 9.3% through 2034. Growth is being driven by increasing demand for product traceability, anti-counterfeiting solutions, and consumer engagement technologies. Intelligent packaging systems incorporate sensors, indicators, RFID tags, NFC technologies, and digital tracking features. Companies across pharmaceutical, food, and consumer goods industries are investing heavily in these solutions to improve supply chain visibility. Future growth will be supported by advances in printed electronics, IoT integration, and cloud-based data analytics. As digital transformation continues across packaging ecosystems, intelligent packaging technologies are expected to experience accelerated adoption globally.

By Material

Plastic-based materials held the largest market share in 2024, representing approximately 50.6% of total revenue. These materials remain widely used because of their durability, flexibility, barrier properties, and compatibility with active and intelligent packaging technologies. Plastic substrates provide reliable platforms for integrating sensors, indicators, RFID tags, and preservation agents. Food packaging applications account for a significant portion of demand, particularly in products requiring extended shelf life and contamination protection. Industry examples include packaged meats, dairy products, pharmaceuticals, and consumer goods. Ongoing innovations in multilayer plastics and recyclable polymer materials continue to enhance performance, supporting the segment's leadership position.

Paper-based materials are expected to register the fastest CAGR of 8.9% through 2034. Increasing environmental concerns and sustainability initiatives are encouraging manufacturers to transition toward renewable packaging materials. Paper-based intelligent packaging solutions integrated with printed electronics, QR codes, and digital authentication technologies are gaining popularity. Growth is particularly strong in retail packaging and consumer goods applications where sustainability influences purchasing decisions. Future innovations are expected to focus on improving barrier properties and compatibility with active packaging technologies. As regulatory pressure regarding plastic waste intensifies, paper-based materials are anticipated to gain substantial market share.

By End-Use

Food & beverage applications accounted for the largest market share in 2024, contributing approximately 45.1% of total revenue. The segment benefits from increasing demand for food safety, freshness monitoring, and shelf-life extension technologies. Active packaging systems help manufacturers maintain product quality throughout transportation and storage while reducing waste. Intelligent packaging solutions also enable consumers to access information regarding freshness, sourcing, and authenticity. Industry examples include fresh produce, meat products, dairy products, beverages, and packaged snacks. Growing consumer expectations regarding transparency and product quality continue to strengthen demand. As food distribution networks become increasingly globalized, adoption of advanced packaging technologies is expected to remain strong.

Pharmaceutical applications are expected to be the fastest-growing end-use segment, registering a CAGR of 9.5% through 2034. Rising concerns regarding counterfeit drugs, regulatory compliance, and temperature-sensitive medicines are driving adoption of smart packaging technologies. Pharmaceutical manufacturers are implementing RFID-enabled packaging, temperature indicators, and track-and-trace systems to improve product integrity. Future growth opportunities include medication adherence monitoring, connected healthcare packaging, and personalized medicine applications. As pharmaceutical supply chains become more sophisticated, intelligent packaging technologies are expected to play a critical role in ensuring product safety and regulatory compliance.

Active Smart And Intelligent Packaging Market Segmentations

By Type

- Active Packaging

- Smart Packaging

- Intelligent Packaging

By Material

- Plastic-Based Materials

- Paper-Based Materials

- Metal-Based Materials

- Glass-Based Materials

By End-User

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Consumer Electronics

- Industrial Products

Regional Analysis

North America

North America accounted for approximately 28.6% of the global active smart and intelligent packaging market share in 2025 and is projected to expand at a CAGR of 7.8% through 2034. The region benefits from advanced packaging technology adoption, mature retail infrastructure, and strong investments in digital supply chain solutions. Food manufacturers, pharmaceutical companies, and consumer goods brands are increasingly implementing intelligent packaging systems to improve traceability and product monitoring. Growing consumer demand for transparency regarding product quality and sourcing is further supporting market growth. The region also benefits from strong innovation ecosystems that facilitate commercialization of smart packaging technologies across various industries.

The United States dominates the North American market. A unique growth driver is the increasing deployment of anti-counterfeiting packaging technologies within pharmaceutical and healthcare sectors. Drug manufacturers are integrating RFID tags and digital authentication systems into packaging to improve regulatory compliance and product security. A notable industry trend involves connected packaging solutions that allow consumers and healthcare providers to verify product authenticity through mobile applications. This growing emphasis on pharmaceutical security is expected to strengthen demand for intelligent packaging technologies throughout the forecast period.

Europe

Europe held approximately 25.4% market share in 2025 and is expected to grow at a CAGR of 8.0% during the forecast period. Market expansion is supported by stringent food safety regulations, sustainability initiatives, and increasing demand for traceable packaging solutions. European manufacturers are actively investing in smart packaging technologies that improve product monitoring while supporting environmental goals. Growing adoption of recyclable and reusable packaging materials is also contributing to market development. Additionally, the region's well-established food processing industry continues to drive demand for active packaging systems designed to reduce spoilage and extend product shelf life.

Germany remains the dominant market within Europe. A unique growth factor is the country's leadership in industrial automation and digital manufacturing technologies. Packaging companies are increasingly integrating printed electronics and intelligent sensing technologies into packaging systems for industrial and consumer applications. An emerging trend involves the use of smart labels in premium food and beverage products to provide detailed product information and authenticity verification. This technological integration continues to create growth opportunities across the regional market.

Asia Pacific

Asia Pacific dominated the market with a 39.2% share in 2025 and is projected to register a CAGR of 9.1% through 2034. The region benefits from rapid industrialization, expanding consumer goods manufacturing, and increasing investments in packaging innovation. Strong growth in e-commerce and retail sectors is creating substantial demand for intelligent packaging solutions capable of enhancing product tracking and customer engagement. Food safety concerns and growing pharmaceutical production are also supporting adoption. Several countries are investing heavily in digital supply chain infrastructure, which further strengthens the market outlook.

China leads the Asia Pacific market due to its large manufacturing base and expanding packaging industry. A unique growth driver is the rapid adoption of QR-code-enabled packaging in consumer goods and food products. Brands are increasingly using digital packaging solutions to enhance consumer interaction and strengthen product authentication. Industry trends indicate growing integration of smart packaging with e-commerce platforms, allowing companies to collect valuable consumer insights. This development is expected to accelerate market expansion throughout the forecast period.

Middle East & Africa

The Middle East & Africa accounted for approximately 3.9% of the global market in 2025 and is forecast to grow at a CAGR of 8.2%. Increasing investments in food security, healthcare infrastructure, and retail modernization are supporting market growth. Governments across the region are implementing initiatives aimed at reducing food waste and improving supply chain efficiency. These efforts are creating opportunities for active packaging solutions capable of preserving product quality in challenging climatic conditions. Rising imports of packaged food and pharmaceutical products are also contributing to demand for intelligent packaging systems.

The United Arab Emirates is the dominant market within the region. A unique growth factor is the country's growing role as a logistics and distribution hub for international trade. Companies operating within the UAE are increasingly utilizing smart packaging technologies to improve shipment visibility and product integrity. An industry trend involves deployment of intelligent packaging solutions for imported food products, helping retailers monitor freshness and quality. This growing emphasis on supply chain optimization is expected to drive market growth.

Latin America

Latin America represented approximately 2.9% market share in 2025 and is expected to register the fastest CAGR of 9.0% during the forecast period. Market growth is driven by expanding food processing industries, increasing retail modernization, and growing consumer awareness regarding product safety. Manufacturers are investing in active packaging technologies to improve shelf life and reduce distribution losses. Rising adoption of packaged foods and pharmaceuticals is also supporting demand. Improvements in logistics infrastructure and increasing foreign investment are further contributing to regional market expansion.

Brazil dominates the Latin American market. A unique growth driver is the increasing use of active packaging technologies within agricultural export supply chains. Exporters are adopting oxygen scavengers and moisture-control solutions to maintain product quality during international transportation. Industry trends indicate growing implementation of intelligent packaging systems for fresh produce exports. This focus on export quality and supply chain efficiency is expected to support sustained market growth throughout the forecast period.

Competitive Landscape

The active smart and intelligent packaging market is characterized by strong competition among packaging manufacturers, technology providers, and materials companies. Market participants are focusing on digital innovation, sustainability, product differentiation, and strategic partnerships to strengthen their market positions.

Amcor plc remains one of the leading companies in the market due to its extensive global packaging portfolio and continued investment in intelligent packaging technologies. The company recently expanded its smart packaging solutions portfolio through partnerships focused on digital consumer engagement and supply chain traceability.

Other major participants include Sealed Air Corporation, Avery Dennison Corporation, BASF SE, and WestRock Company. These companies continue investing in RFID integration, active preservation technologies, printed electronics, and sustainable packaging materials. Strategic acquisitions and collaborations remain common approaches for expanding technological capabilities and geographic reach. Companies are also focusing on recyclable intelligent packaging solutions to address evolving sustainability requirements. Continuous innovation in connected packaging and active preservation technologies is expected to remain a primary competitive strategy throughout the forecast period.

Key Players List

- Amcor plc

- Sealed Air Corporation

- Avery Dennison Corporation

- BASF SE

- WestRock Company

- Smurfit Westrock

- Ball Corporation

- Huhtamaki Oyj

- Multisorb Technologies

- Thinfilm Electronics ASA

- Stora Enso Oyj

- AptarGroup Inc.

- Crown Holdings Inc.

- Toppan Holdings Inc.

- International Paper Company

- Graphic Packaging International

- Zebra Technologies Corporation

- Checkpoint Systems Inc.