Woven Plastic Packaging Market Size and Growth

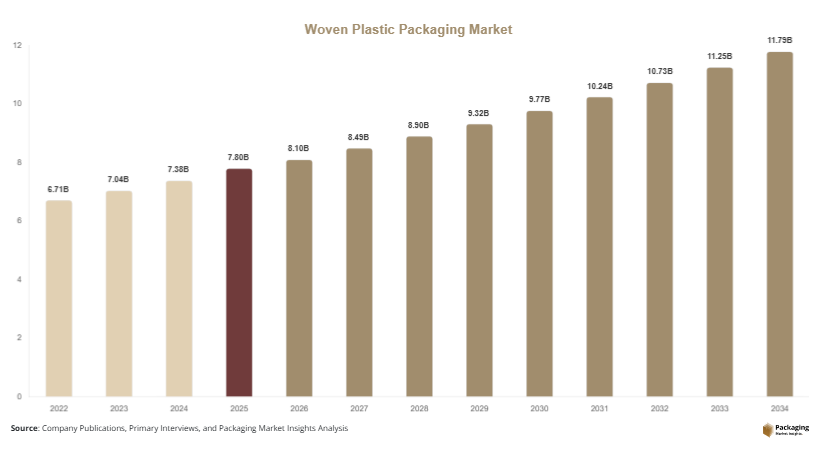

The global woven plastic packaging market was valued at USD 7.8 billion in 2025 and is projected to reach USD 11.9 billion by 2034, expanding at a CAGR of 4.8% during the forecast period from 2025 to 2034. The market is estimated to reach USD 8.1 billion in 2026, driven by rising demand for durable, lightweight, and cost-efficient industrial packaging solutions across agriculture, chemicals, construction, food processing, and retail logistics industries. Woven plastic packaging products such as polypropylene woven sacks, bulk bags, leno bags, and woven rolls are increasingly used for transporting and storing bulk commodities because of their high tensile strength, moisture resistance, and reusability.

Growing international trade activities and rising agricultural exports are major factors driving market growth. Countries with large fertilizer, grain, and cement industries are increasing their adoption of woven plastic sacks to improve packaging efficiency and reduce transportation losses. In addition, the rapid expansion of organized retail and e-commerce logistics is encouraging manufacturers to invest in advanced woven packaging products with improved printability and handling features. Flexible industrial packaging demand is also increasing across emerging economies due to urbanization and industrial expansion.

Key Highlights

- Asia Pacific dominated the market with a 39.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 5.7%.

- Polypropylene woven sacks led the type segment with a 36.4% share.

- Polypropylene dominated the material segment with a 68.3% share.

- Agriculture applications led the end-use segment with a 33.9% share.

- The US remained the dominant country with a market size of USD 1.1 billion in 2025 and USD 1.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recyclable Industrial Packaging

Industrial users are increasingly shifting toward recyclable woven plastic packaging products to comply with sustainability targets and waste reduction policies. Woven polypropylene bags and bulk containers are being reused across agricultural and industrial supply chains due to their durability and extended lifecycle. Manufacturers are also introducing mono-material woven packaging structures that improve recyclability and reduce separation costs during waste processing. Large fertilizer distributors and grain exporters are replacing multilayer conventional packaging with recyclable woven sacks to reduce environmental impact and lower overall packaging expenses.

The trend is particularly visible in Europe and North America where industrial packaging regulations are becoming stricter. Several food grain cooperatives and logistics firms are adopting reusable FIBCs for bulk transportation operations. Future demand for recyclable woven packaging is expected to accelerate as governments promote circular economy practices and industries seek cost-efficient sustainable packaging alternatives.

Automation in Woven Bag Manufacturing

Manufacturers are increasingly investing in automated extrusion, weaving, lamination, and printing technologies to improve production efficiency and packaging consistency. Automated woven sack manufacturing systems help producers reduce labor dependency, minimize material wastage, and improve product quality. Advanced digital printing technologies are also enabling high-resolution branding and traceability features on woven plastic packaging materials.

Countries such as India, China, and Vietnam are witnessing rapid modernization of woven packaging manufacturing facilities to meet growing export demand. Automated production lines are supporting high-volume manufacturing for fertilizer, cement, and food grain packaging applications. In the coming years, Industry 4.0 technologies and AI-driven quality inspection systems are expected to further enhance operational efficiency in woven packaging production facilities.

Market Drivers

Expanding Agricultural and Fertilizer Industries

The growth of global agriculture and fertilizer industries is significantly driving demand for woven plastic packaging products. Agricultural commodities such as rice, wheat, corn, animal feed, and seeds require durable and moisture-resistant packaging for storage and transportation. Woven polypropylene sacks are widely used because they provide high strength and lower transportation damage compared to traditional paper packaging.

Fertilizer producers are also increasing adoption of laminated woven sacks and jumbo bags for bulk handling operations. Countries such as India, Brazil, and Indonesia are witnessing rising agricultural exports, which is creating strong demand for woven packaging solutions. Increasing government investments in food security infrastructure and grain storage facilities are expected to further strengthen market growth during the forecast period.

Growth in Construction and Cement Packaging Demand

Rapid urbanization and infrastructure development are increasing the demand for woven plastic packaging in cement, sand, chemicals, and construction material transportation. Woven sacks provide superior load-bearing capacity and improved resistance against moisture and punctures, making them suitable for construction sector applications.

Large-scale infrastructure projects across Asia Pacific and the Middle East are generating significant demand for industrial woven bags. Cement manufacturers are increasingly adopting block-bottom woven bags with better sealing and stacking capabilities. Rising construction activity in emerging economies is expected to create long-term growth opportunities for woven packaging manufacturers over the next decade.

Market Restraint

Volatility in Raw Material Prices

Fluctuating prices of polypropylene and polyethylene resins remain a major restraint for the woven plastic packaging market. Raw material costs are directly influenced by crude oil price volatility, global supply chain disruptions, and trade restrictions. Sudden increases in resin prices negatively impact profit margins for woven packaging manufacturers, especially small and medium-sized producers operating in price-sensitive markets.

Environmental regulations related to plastic usage also create operational challenges for manufacturers. Several countries are introducing stricter rules on single-use plastics, forcing companies to invest in recyclable and reusable packaging solutions. Additionally, competition from paper-based industrial packaging products is increasing in regions focused on sustainability initiatives. For example, some agricultural exporters in Europe are shifting toward paper sacks for selected applications due to environmental compliance requirements. These factors may limit market expansion in highly regulated economies.

Market Opportunities

Expansion of Bulk Container Packaging

The increasing use of flexible intermediate bulk containers (FIBCs) across chemicals, mining, pharmaceuticals, and food industries presents significant growth opportunities for market participants. Bulk packaging solutions reduce handling costs and improve transportation efficiency for industrial users. Demand for jumbo woven bags is growing due to rising global trade volumes and increased movement of industrial materials.

Manufacturers are developing anti-static and food-grade FIBCs for specialized applications. Pharmaceutical and food processing industries are adopting high-quality woven bulk packaging solutions to maintain hygiene and reduce contamination risks. Growth in global exports of chemicals and industrial powders is expected to support long-term demand for advanced bulk woven packaging products.

Rising Demand for Sustainable Packaging Innovations

The development of recycled woven packaging products and bio-based plastic materials offers substantial future growth potential. Packaging manufacturers are increasingly investing in recycled polypropylene technologies to meet sustainability goals and reduce virgin plastic consumption. Several companies are introducing woven sacks containing post-consumer recycled materials for agriculture and retail applications.

E-commerce and retail logistics sectors are also creating opportunities for lightweight reusable woven packaging products. Advanced woven packaging designs with enhanced durability and improved printing quality are attracting interest from branded consumer goods companies. Over the forecast period, sustainable woven packaging innovations are expected to become a major competitive differentiator in the global market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.8 Billion |

| Market Size in 2026 | USD 8.1 Billion |

| Market Size in 2034 | USD 11.9 Billion |

| CAGR | 4.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polypropylene woven sacks dominated the type segment and accounted for 36.4% of the global woven plastic packaging market share in 2024. These sacks are widely used across agriculture, cement, fertilizer, sugar, and food grain industries because of their high tensile strength, flexibility, and cost efficiency. Polypropylene woven sacks offer superior resistance against moisture, punctures, and rough transportation conditions, making them suitable for bulk industrial packaging applications. Agricultural producers and fertilizer manufacturers continue to rely heavily on woven sacks for large-scale storage and export operations. Laminated woven sacks are also gaining traction for products requiring improved barrier protection and enhanced shelf stability. In countries such as India, China, and Brazil, government-supported grain storage programs are further increasing demand for woven sacks. The segment also benefits from advancements in digital printing technologies that enable high-quality branding and labeling on industrial packaging products.

Flexible intermediate bulk containers (FIBCs) are projected to register the fastest CAGR of 6.1% during the forecast period. Rising global trade volumes and industrial material transportation are driving demand for jumbo woven bulk bags across chemicals, mining, food processing, and pharmaceutical sectors. FIBCs reduce packaging waste and improve warehouse handling efficiency due to their large storage capacity and reusability. Industrial companies are increasingly adopting anti-static and food-grade bulk containers to improve product safety and transportation performance. Manufacturers are also introducing lightweight FIBCs with enhanced lifting strength and discharge systems for automated logistics operations. Growth in international chemical exports and increasing warehouse automation are expected to create long-term opportunities for the segment. The shift toward reusable industrial packaging solutions is further supporting adoption of woven bulk containers in developed and emerging economies.

By Material

Polypropylene dominated the material segment with a 68.3% share in 2024 due to its superior durability, low production cost, and excellent chemical resistance properties. Polypropylene woven packaging materials are extensively used across agriculture, construction, chemicals, and retail logistics applications because they provide high strength while remaining lightweight. The material also supports cost-effective mass production and can be laminated or coated for additional moisture protection. Polypropylene woven sacks are preferred for packaging grains, fertilizers, cement, and animal feed because they maintain product integrity during long-distance transportation and rough handling conditions. Industrial users continue to favor polypropylene due to its recyclability and compatibility with automated packaging systems. Several packaging manufacturers are also investing in UV-resistant polypropylene woven products for outdoor storage applications. Rapid industrialization across Asia Pacific and increasing exports of packaged commodities continue to strengthen the dominance of this segment.

Recycled plastic materials are expected to witness the fastest CAGR of 6.4% through 2034 due to rising sustainability initiatives and growing pressure to reduce virgin plastic consumption. Packaging companies are increasingly incorporating recycled polypropylene content into woven sacks and FIBCs to meet environmental targets and regulatory requirements. Several agricultural exporters and food distributors are adopting recycled-content packaging products to strengthen sustainable supply chain operations. Technological advancements in recycling processes are improving the quality and strength of recycled woven plastic materials, enabling their use in industrial applications. Europe and North America are witnessing strong growth in demand for recyclable woven packaging solutions due to circular economy regulations and corporate sustainability commitments. Future investments in advanced recycling infrastructure are expected to accelerate the adoption of recycled woven packaging materials globally. The segment is likely to gain additional traction as manufacturers continue developing durable and cost-efficient eco-friendly packaging alternatives.

By End-Use

Agriculture dominated the end-use segment and held 33.9% of the woven plastic packaging market share in 2024. Woven plastic packaging products are widely used for storing and transporting grains, rice, seeds, fertilizers, animal feed, and agricultural chemicals. The segment benefits from increasing global food demand and rising agricultural trade activities across Asia Pacific, Latin America, and Africa. Woven polypropylene sacks are preferred in agricultural applications because they provide excellent breathability, moisture resistance, and handling durability. Governments in several developing economies are expanding grain procurement and storage infrastructure, which is further supporting demand for woven agricultural packaging. Agricultural cooperatives and exporters are also investing in laminated woven bags for improved product protection during export transportation. Increasing mechanization in farming and growth in bulk agricultural commodity trading are expected to maintain strong demand for woven packaging products throughout the forecast period.

Food and beverage packaging is anticipated to grow at the fastest CAGR of 5.9% during the study period. Rising consumption of packaged food products and expanding food processing industries are creating strong demand for hygienic and durable woven packaging solutions. Food manufacturers are increasingly adopting food-grade woven sacks and FIBCs for packaging sugar, flour, rice, pulses, starch, and processed food ingredients. Advanced woven packaging materials with improved moisture barriers and contamination resistance are gaining popularity across the food supply chain. The expansion of organized retail and international food exports is further supporting growth in this segment. Manufacturers are also developing customized woven food packaging products with enhanced printing quality and traceability features. Future demand is expected to rise steadily due to increasing packaged food consumption, urbanization, and improvements in cold chain logistics infrastructure worldwide.

Woven Plastic Packaging Market Segmentations

By Type

- Polypropylene Woven Sacks

- Flexible Intermediate Bulk Containers (FIBCs)

- Leno Bags

- Woven Rolls

- Block Bottom Bags

By Material

- Polypropylene

- Polyethylene

- Recycled Plastic Materials

- Laminated Plastic Materials

By End-User

- Agriculture

- Food & Beverage

- Chemicals

- Construction

- Retail & E-commerce

- Pharmaceuticals

Regional Analysis

North America

North America accounted for 24.8% of the global woven plastic packaging market share in 2025 and is expected to expand at a CAGR of 4.3% during the forecast period. The region benefits from strong demand across agriculture, food processing, industrial chemicals, and construction sectors. Rising adoption of bulk packaging systems in logistics operations is supporting regional market growth. Industrial users are increasingly shifting toward reusable woven plastic containers to reduce packaging waste and improve transportation efficiency. The U.S. and Canada are also witnessing increased demand for durable packaging materials in fertilizer and animal feed distribution networks. Technological advancements in automated woven bag manufacturing are further supporting production efficiency across the region.

The U.S. dominates the North American market due to its large agricultural exports and advanced industrial packaging infrastructure. One unique growth driver is the increasing use of FIBCs in chemical transportation and warehouse automation systems. Food grain cooperatives and industrial manufacturers are increasingly adopting woven bulk packaging for improved handling and storage efficiency. Several logistics companies are integrating reusable woven bulk bags into closed-loop supply chains to lower operational costs. Rising infrastructure spending and growth in packaged construction materials are also contributing to long-term demand for woven packaging solutions across the country.

Europe

Europe represented 22.1% of the global woven plastic packaging market in 2025 and is forecast to grow at a CAGR of 4.1% through 2034. The regional market is supported by strong industrial manufacturing activity and growing demand for recyclable packaging materials. Sustainability regulations across the European Union are encouraging manufacturers to develop recyclable woven packaging products with reduced environmental impact. Agricultural exports, industrial chemicals, and specialty food products continue to generate stable demand for woven sacks and bulk containers. Growth in cross-border trade activities within the region is also increasing the need for durable industrial packaging materials capable of handling long-distance transportation.

Germany remains the leading country in the European market due to its advanced manufacturing sector and strong industrial exports. A major regional growth driver is the increasing use of recyclable woven packaging in industrial logistics operations. German chemical manufacturers are increasingly adopting reusable FIBCs to reduce packaging waste and transportation costs. Food processing companies are also investing in high-strength woven bags with advanced barrier protection for bulk ingredients. Expansion of automated warehouse systems across Europe is expected to further support demand for durable woven packaging solutions in the coming years.

Asia Pacific

Asia Pacific dominated the woven plastic packaging market with a 39.6% share in 2025 and is expected to register a CAGR of 5.5% during the forecast period. Rapid industrialization, expanding agricultural output, and rising exports are major factors supporting regional growth. Countries across the region are witnessing increasing demand for woven sacks in fertilizer, rice, sugar, and cement packaging applications. Large-scale manufacturing activities and low production costs are attracting investments in woven packaging production facilities. Growing infrastructure development and increasing food grain storage requirements are also contributing to strong regional demand for industrial woven packaging products.

China leads the Asia Pacific market due to its massive manufacturing base and export-oriented industrial economy. A key regional growth driver is the rapid expansion of industrial packaging exports from China to Southeast Asia, Europe, and Africa. Chinese manufacturers are investing heavily in automated weaving and lamination technologies to improve production capacity and product quality. India is also emerging as a strong market due to rising agricultural exports and government food storage initiatives. Demand for woven polypropylene sacks continues to increase across construction, chemicals, and food processing industries throughout the region.

Middle East & Africa

The Middle East & Africa accounted for 7.9% of the global woven plastic packaging market in 2025 and is projected to grow at a CAGR of 4.9% through 2034. Growth in the region is primarily driven by increasing construction activity, agricultural modernization, and industrial trade expansion. Rising investments in infrastructure projects across Gulf countries are creating strong demand for woven cement and chemical packaging products. Agricultural economies in Africa are also increasing the use of woven sacks for grain storage and fertilizer distribution. Growing industrialization and improvements in logistics networks are further supporting regional packaging demand.

Saudi Arabia dominates the Middle East market due to its large petrochemical and construction industries. One unique growth factor is the growing use of woven plastic bulk bags for industrial chemical exports and warehouse storage operations. Construction companies are increasingly adopting heavy-duty woven sacks for transporting cement and building materials across infrastructure projects. In Africa, countries such as Nigeria and Kenya are witnessing rising demand for woven agricultural packaging due to expanding grain production and fertilizer consumption. The region is expected to experience stable long-term growth as industrial packaging demand continues to expand.

Latin America

Latin America held 5.6% of the global woven plastic packaging market in 2025 and is forecast to grow at the fastest CAGR of 5.7% during the study period. Agricultural exports and food commodity transportation remain the largest contributors to market demand across the region. Brazil, Argentina, and Chile are major consumers of woven sacks for coffee, sugar, grains, and fertilizer packaging applications. Increasing retail distribution and industrial trade activities are also supporting market expansion. Demand for lightweight and reusable industrial packaging materials is increasing as regional exporters seek cost-efficient logistics solutions.

Brazil is the dominant country in the Latin American woven plastic packaging market. A major growth driver is the expansion of agricultural exports and bulk commodity transportation infrastructure. Brazilian grain exporters are increasingly using woven polypropylene bags and FIBCs to improve packaging durability during long-distance shipping. Food processing industries are also investing in advanced woven packaging materials with moisture protection capabilities. Rising industrial development and growing fertilizer imports are expected to strengthen regional demand for woven plastic packaging over the next decade.

Competitive Landscape

The woven plastic packaging market is highly competitive with the presence of global packaging manufacturers and regional industrial packaging producers competing on pricing, product durability, sustainability, and production capacity. Companies are increasingly investing in automation technologies, recyclable material development, and customized industrial packaging solutions to strengthen market positioning. Strategic partnerships with agricultural cooperatives, fertilizer manufacturers, and logistics companies are becoming a key growth strategy among leading participants.

Berry Global Inc. remains one of the leading companies in the market due to its extensive industrial packaging portfolio and strong global manufacturing network. The company continues to invest in recyclable woven packaging solutions and lightweight bulk container technologies. Other major players such as Mondi Group, LC Packaging, and Greif Inc. are expanding their product offerings for food-grade and industrial bulk packaging applications.

Several manufacturers are also focusing on sustainable packaging innovations to meet evolving regulatory requirements and customer expectations. Advanced woven sack printing technologies, UV-resistant coatings, and reusable FIBC systems are becoming important competitive differentiators in the market. Regional manufacturers across Asia Pacific are expanding export capacities to capitalize on growing global demand for industrial woven packaging products.

Key Players List

- Berry Global Inc.

- Mondi Group

- Greif Inc.

- LC Packaging International BV

- Conitex Sonoco

- Muscat Polymers Pvt. Ltd.

- Uflex Ltd.

- Emmbi Industries Ltd.

- Rishi FIBC Solutions Pvt. Ltd.

- Intertape Polymer Group

- Jumbo Bag Ltd.

- Royal NNZ Group

- Shalimar Group

- Al-Tawfiq Company

- Bang Polypack

- Taihua Group

- Palmetto Industries International Inc.

- Flexituff Ventures International Ltd.