Wafer Level Packaging Market Size and Growth

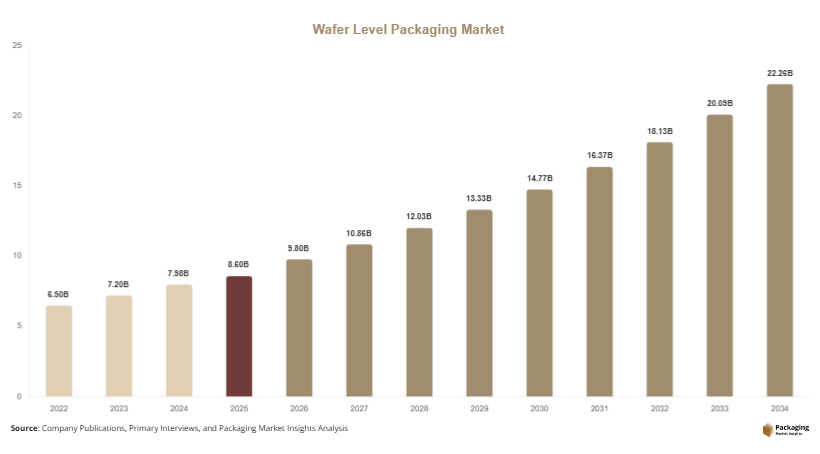

The Wafer Level Packaging Market is gaining momentum as semiconductor manufacturers seek advanced packaging solutions that improve performance, reduce size, and lower manufacturing costs. The market size was valued at approximately USD 8.6 billion in 2025 and is projected to reach USD 9.8 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to expand at a CAGR of 10.8%, reaching nearly USD 24.7 billion by 2034. This growth reflects increasing demand for compact and efficient semiconductor packaging solutions across industries such as consumer electronics, automotive, and telecommunications.

One of the primary growth factors driving the wafer level packaging market is the rising demand for miniaturized electronic devices. Smartphones, wearables, and IoT devices require smaller and more efficient components, which wafer-level packaging supports by enabling high-density integration. Another key factor is the expansion of the automotive electronics sector, particularly with the growth of electric vehicles and advanced driver assistance systems. These applications require high-performance semiconductor components that benefit from wafer-level packaging technologies.

Key Highlights:

- Market size reached USD 8.6 billion in 2025

- Expected to grow to USD 24.7 billion by 2034

- CAGR of 10.8% from 2025 to 2034

- Rising demand for miniaturized electronic devices

- Growth in automotive and 5G applications

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Fan-Out Wafer Level Packaging (FOWLP)

The wafer level packaging market is witnessing growing adoption of fan-out wafer level packaging technologies. FOWLP enables higher I/O density and improved electrical performance compared to traditional fan-in packaging. This technology allows chips to be packaged without the need for a substrate, reducing overall package thickness and improving thermal performance. Manufacturers are increasingly using FOWLP for applications such as mobile devices and high-performance computing. The trend is driven by the need for enhanced performance and miniaturization. As semiconductor devices become more complex, FOWLP is expected to play a significant role in meeting these requirements.

Integration of Heterogeneous Packaging Technologies

Another key trend in the wafer level packaging market is the integration of heterogeneous packaging technologies. This approach involves combining different types of semiconductor components into a single package. It allows for improved functionality and performance by integrating logic, memory, and sensors. Heterogeneous integration supports applications such as artificial intelligence and advanced computing. This trend is driven by the need for higher efficiency and reduced power consumption. As demand for multifunctional devices increases, the adoption of heterogeneous packaging solutions is expected to grow.

Market Drivers

Growth of Consumer Electronics Industry

The rapid growth of the consumer electronics industry is a major driver of the wafer level packaging market. Devices such as smartphones, tablets, and wearables require compact and high-performance semiconductor components. Wafer-level packaging enables manufacturers to meet these requirements by offering smaller package sizes and improved performance. The increasing demand for advanced electronic devices supports the adoption of wafer-level packaging solutions. As consumers continue to demand more features and better performance, the need for efficient packaging technologies will increase.

Rising Demand for Advanced Automotive Electronics

The increasing adoption of advanced automotive electronics is another key driver of the market. Modern vehicles are equipped with electronic systems such as infotainment, safety systems, and autonomous driving technologies. These systems require reliable and high-performance semiconductor components. Wafer-level packaging provides the necessary performance and reliability. The growth of electric vehicles and connected cars further supports this trend. As the automotive industry continues to evolve, the demand for advanced packaging solutions is expected to rise.

Market Restraint

High Initial Investment and Technical Complexity

High initial investment and technical complexity act as significant restraints in the wafer level packaging market. The adoption of wafer-level packaging technologies requires advanced manufacturing equipment and skilled labor. This increases the cost of implementation for manufacturers. Small and medium-sized companies may find it challenging to invest in these technologies. Additionally, the complexity of wafer-level packaging processes can lead to production challenges and lower yields if not managed properly. For example, a semiconductor company implementing fan-out wafer-level packaging may face difficulties in achieving consistent quality during the initial stages. These factors can limit market growth and slow the adoption of advanced packaging technologies.

Market Opportunities

Expansion of 5G and IoT Applications

The expansion of 5G and IoT applications presents significant opportunities for the wafer level packaging market. These technologies require high-performance semiconductor components with compact designs. Wafer-level packaging supports these requirements by enabling high-density integration and improved performance. The increasing deployment of 5G networks and IoT devices is expected to drive demand for advanced packaging solutions. Companies are focusing on developing packaging technologies that meet the specific requirements of these applications. This opportunity is expected to contribute to market growth.

Development of Advanced Packaging Technologies

The development of advanced packaging technologies offers new opportunities in the market. Innovations such as 3D packaging and system-in-package solutions are enhancing the capabilities of wafer-level packaging. These technologies allow for better performance and efficiency. Manufacturers are investing in research and development to create new packaging solutions. The increasing demand for high-performance semiconductor devices supports this trend. As technology continues to evolve, the development of advanced packaging solutions is expected to drive market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.6 Billion |

| Market Size in 2026 | USD 9.8 Billion |

| Market Size in 2034 | USD 24.7 Billion |

| CAGR | 10.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

Fan-in wafer-level packaging dominated the market in 2024, accounting for approximately 55% of the total market share. This type of packaging is widely used due to its cost efficiency and suitability for applications with lower I/O requirements. It provides advantages such as reduced package size and improved performance. The widespread use of fan-in packaging supports its dominance in the market.

Fan-out wafer-level packaging is expected to be the fastest-growing segment, with a CAGR of 12.4% during the forecast period. This type offers higher performance and flexibility. Increasing demand for advanced semiconductor devices drives the growth of this segment.

By Application

Consumer electronics dominated the market in 2024, accounting for approximately 48% of the total market share. The high demand for smartphones and wearable devices supports this segment. Wafer-level packaging provides the necessary performance and compact size required for these applications.

Automotive electronics are expected to grow at the fastest CAGR of 11.9% during the forecast period. The increasing adoption of advanced electronic systems in vehicles drives this growth.

By End-Use

Foundries dominated the market in 2024, with a share of approximately 46%. These companies play a key role in semiconductor manufacturing and packaging. Their demand for efficient packaging solutions supports market growth.

Integrated device manufacturers are expected to grow at the highest CAGR of 11.3% during the forecast period. Increasing investments in advanced technologies drive this segment.

Wafer Level Packaging Market Segmentations

Packaging Type

- Fan-In Wafer Level Packaging

- Fan-Out Wafer Level Packaging

Application

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Telecommunications

End-Use

- Foundries

- Integrated Device Manufacturers

- Outsourced Semiconductor Assembly and Test (OSAT) Providers

Regional Analysis

North America

North America accounted for approximately 34% of the wafer level packaging market share in 2025 and is expected to grow at a CAGR of 10.2% during the forecast period. The region benefits from strong technological infrastructure and high adoption of advanced semiconductor technologies. Demand from industries such as consumer electronics and automotive supports market growth.

The United States dominates the regional market due to its advanced semiconductor industry. A unique growth factor is the increasing investment in research and development for advanced packaging technologies.

Europe

Europe held around 23% of the market share in 2025 and is projected to grow at a CAGR of 9.8% through 2034. The region’s focus on innovation and technological development supports market growth. Industries such as automotive and industrial electronics contribute to demand.

Germany leads the European market, supported by its strong automotive sector. A key growth factor is the increasing adoption of advanced electronics in vehicles.

Asia Pacific

Asia Pacific accounted for approximately 32% of the market share in 2025 and is expected to grow at a CAGR of 12.1% during the forecast period. The region’s large electronics manufacturing base supports market growth. Countries such as China and South Korea are major contributors.

China dominates the Asia Pacific market due to its extensive semiconductor manufacturing capabilities. A unique growth factor is the expansion of consumer electronics production.

Middle East & Africa

The Middle East & Africa region held about 6% of the market share in 2025 and is projected to grow at a CAGR of 9.5% over the forecast period. The market is driven by increasing investments in technology and infrastructure.

UAE leads the regional market, supported by its growing technology sector. A key growth factor is the adoption of advanced electronic devices.

Latin America

Latin America accounted for nearly 5% of the market share in 2025 and is expected to grow at a CAGR of 9.9% through 2034. Economic development and increasing demand for electronics contribute to market growth.

Brazil dominates the Latin American market due to its expanding electronics industry. A unique growth factor is the increasing adoption of consumer electronics.

Competitive Landscape

The wafer level packaging market is characterized by strong competition among key players focusing on innovation and technological advancements. Companies are investing in research and development to enhance their product offerings and maintain competitive positions. Strategic partnerships and collaborations are common strategies used to expand market presence.

Taiwan Semiconductor Manufacturing Company (TSMC) is a leading player in the market, known for its advanced packaging solutions. The company recently expanded its wafer-level packaging capabilities to support growing demand. Other major players include Intel Corporation, Samsung Electronics Co., Ltd., ASE Technology Holding Co., Ltd., and Amkor Technology, Inc. These companies are focusing on developing new technologies and expanding their production capacities. The competitive landscape is expected to remain dynamic as companies continue to innovate and adapt to changing market demands.

Key Players List

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Samsung Electronics Co., Ltd.

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- JCET Group Co., Ltd.

- STATS ChipPAC Ltd.

- Powertech Technology Inc.

- Texas Instruments Incorporated

- Qualcomm Incorporated

- Broadcom Inc.

- Micron Technology, Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Analog Devices, Inc.