Volatile Corrosion Inhibitors Vci Packaging Market Size and Growth

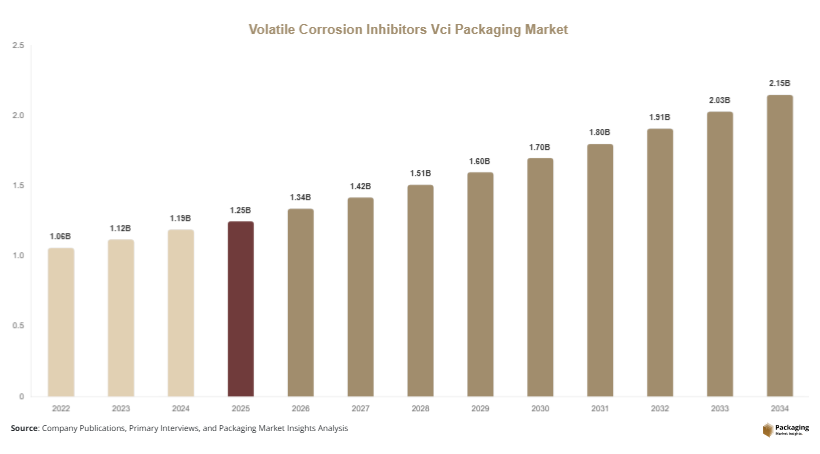

The global volatile corrosion inhibitors Vci packaging market size was estimated at USD 1.25 billion in 2025 and is projected to reach USD 1.34 billion in 2026, with expectations to grow to approximately USD 2.15 billion by 2034, registering a compound annual growth rate (CAGR) of 6.1% from 2025 to 2034. The market continues to evolve as industries prioritize cost-efficient packaging that ensures product integrity during storage and transportation. The volatile corrosion inhibitors Vci packaging market is experiencing steady expansion due to rising industrialization, growing cross-border trade of metal components, and increased demand for effective corrosion prevention solutions.

One of the primary growth factors driving this market is the rapid expansion of the automotive and heavy machinery industries, where metal components require reliable corrosion protection during shipping and warehousing. VCI packaging solutions eliminate the need for greasing or oiling, making them increasingly preferred in manufacturing supply chains. Additionally, the growth of international trade has increased the need for long-duration packaging solutions that can withstand varied climatic conditions, further accelerating demand.

Key Highlights:

- Asia Pacific dominated the market with a 39.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.8%.

- VCI films led the type segment with a 34.7% share, while VCI bags are expected to grow at a CAGR of 6.6%.

- Automotive applications dominated with a 41.5% share, while electronics applications are forecasted to grow at a CAGR of 6.9%.

- Industrial manufacturing led end-use with 46.2% share, while aerospace is expected to grow at a CAGR of 6.4%.

- China remained the dominant country with a market size of USD 320 million in 2025 and USD 345 million in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Recyclable VCI Materials

The market is witnessing a noticeable transition toward environmentally responsible packaging solutions. Manufacturers are developing biodegradable VCI films and recyclable papers to meet increasing environmental regulations and corporate sustainability targets. This trend is gaining traction across Europe and North America, where regulatory pressure is stronger. Companies are investing in research to create water-based and non-toxic VCI formulations that reduce environmental hazards while maintaining corrosion protection efficiency. This shift is not only enhancing brand image but also enabling end-users to align with circular economy principles, ultimately driving adoption across multiple industries.

Integration of Advanced Polymer Technologies in VCI Packaging

Technological innovation is shaping the next phase of growth in the VCI packaging market. Advanced polymer engineering is enabling the development of high-performance films with enhanced barrier properties and longer protection durations. These innovations allow VCI packaging to perform effectively in extreme humidity and temperature conditions. Multi-layer films with controlled release mechanisms are gaining popularity, ensuring consistent vapor emission over extended periods. This trend is particularly important for industries such as aerospace and marine, where long-term storage is critical. As a result, manufacturers are focusing on product differentiation through performance optimization and material innovation.

Market Drivers

Rising Demand from Automotive and Heavy Equipment Industries

The automotive and heavy equipment sectors are key contributors to the growth of the VCI packaging market. Metal components used in these industries are highly susceptible to corrosion, especially during international shipping. VCI packaging offers a clean and efficient alternative to traditional corrosion prevention methods such as oil coatings. With the global automotive supply chain becoming more complex, the need for reliable packaging solutions has increased significantly. Additionally, the rise in electric vehicle production is driving demand for corrosion protection in sensitive components, further supporting market expansion.

Growth in Global Trade and Logistics Infrastructure

The expansion of global trade networks has created a strong demand for advanced packaging solutions that can protect goods over long transit periods. VCI packaging is increasingly used in export-oriented industries to ensure that metal products reach their destination without damage. Improvements in logistics infrastructure, including shipping and warehousing, are also contributing to market growth. As companies expand their international operations, the need for cost-effective and reliable corrosion protection solutions becomes critical. This driver is particularly strong in emerging economies, where industrial exports are growing rapidly.

Market Restraint

High Cost of Advanced VCI Materials and Limited Awareness in Emerging Markets

Despite its advantages, the adoption of VCI packaging is restrained by the relatively high cost of advanced materials compared to conventional packaging solutions. Small and medium-sized enterprises often hesitate to invest in VCI products due to budget constraints, especially in price-sensitive markets. Additionally, limited awareness about the long-term benefits of VCI packaging in emerging economies further restricts market penetration. For instance, manufacturers in developing regions may still rely on traditional corrosion prevention methods such as oil coatings, which are less efficient but more familiar. This lack of awareness, combined with cost concerns, creates a barrier to widespread adoption, slowing overall market growth.

Market Opportunities

Expansion in Electronics and Semiconductor Industries

The rapid growth of the electronics and semiconductor sectors presents significant opportunities for the VCI packaging market. Sensitive electronic components are highly prone to corrosion, especially when exposed to moisture during transportation. VCI packaging provides a clean and residue-free solution, making it ideal for these applications. As global demand for consumer electronics and advanced semiconductor devices continues to rise, the need for reliable corrosion protection solutions is expected to increase. This opportunity is further supported by technological advancements that enable the development of specialized VCI products tailored for electronic components.

Growing Demand for Customized and Application-Specific Solutions

Another major opportunity lies in the development of customized VCI packaging solutions designed for specific industries and applications. Manufacturers are increasingly offering tailored products that cater to the unique requirements of different metals and environmental conditions. This trend is driven by the need for higher efficiency and cost optimization. Customized solutions not only improve performance but also enhance customer satisfaction, leading to long-term business relationships. As industries continue to evolve, the demand for specialized packaging solutions is expected to grow, creating new avenues for market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.25 Billion |

| Market Size in 2026 | USD 1.34 Billion |

| Market Size in 2034 | USD 2.15 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The VCI films segment dominated the market in 2024 with a share of approximately 34.7%. These films are widely used due to their flexibility, durability, and ability to provide uniform corrosion protection. They are commonly used in automotive and industrial applications where large metal components require secure packaging. The growing demand for lightweight and cost-effective packaging solutions is further supporting the dominance of VCI films in the market.

VCI bags are expected to be the fastest-growing subsegment, with a projected CAGR of 6.6% during the forecast period. The growth is driven by their convenience and ease of use in packaging smaller components. These bags are increasingly used in electronics and precision engineering industries, where contamination-free packaging is essential. Their ability to provide effective corrosion protection without additional treatments makes them a preferred choice.

By Application

The automotive segment held the largest market share in 2024, accounting for approximately 41.5%. The need to protect metal components such as engines, gears, and structural parts during transportation is driving demand for VCI packaging in this segment. The expansion of global automotive supply chains is further supporting growth.

The electronics segment is projected to grow at the fastest CAGR of 6.9%. The increasing production of electronic devices and components is driving the demand for advanced packaging solutions. VCI packaging provides a clean and efficient solution for protecting sensitive components, making it ideal for this application.

By End-Use Industry

Industrial manufacturing dominated the market in 2024 with a share of 46.2%. The widespread use of metal components in machinery and equipment requires effective corrosion protection solutions. VCI packaging is widely used in this industry due to its efficiency and ease of use.

The aerospace sector is expected to grow at a CAGR of 6.4%. The need for long-term storage and transportation of high-value components is driving demand for advanced packaging solutions. VCI packaging provides reliable protection, making it suitable for aerospace applications.

Volatile Corrosion Inhibitors Vci Packaging Market Segmentations

By Type

- VCI Films

- VCI Papers

- VCI Bags

- VCI Foam

By Application

- Automotive

- Electronics

- Metal Processing

- Aerospace

By End-Use Industry

- Industrial Manufacturing

- Oil & Gas

- Defense

- Aerospace

Regional Analysis

North America

North America accounted for approximately 24.6% of the global market share in 2025 and is expected to grow at a CAGR of 5.8% during the forecast period. The region benefits from a well-established industrial base and strong demand from automotive and aerospace sectors. The presence of advanced manufacturing technologies and a focus on product quality are supporting the adoption of VCI packaging solutions across industries.

The United States dominates the regional market due to its large manufacturing sector and extensive export activities. A key growth factor in this region is the increasing emphasis on sustainable packaging solutions, which is driving the adoption of eco-friendly VCI materials. Companies are investing in innovative packaging technologies to meet environmental regulations and enhance product performance.

Europe

Europe held a market share of around 21.3% in 2025 and is projected to grow at a CAGR of 5.6%. The region is characterized by stringent environmental regulations and a strong focus on sustainability. These factors are encouraging the adoption of recyclable and biodegradable VCI packaging solutions across industries.

Germany leads the European market due to its robust automotive and industrial manufacturing sectors. A unique growth factor in this region is the strong regulatory framework that promotes the use of environmentally friendly packaging materials. This has led to increased investment in research and development of sustainable VCI products.

Asia Pacific

Asia Pacific dominated the market with a 39.2% share in 2025 and is expected to grow at the highest CAGR of 6.5%. Rapid industrialization, expanding manufacturing activities, and increasing exports are key factors driving market growth in this region. The presence of a large number of manufacturing hubs further supports demand.

China is the leading country in the region, driven by its massive industrial output and export-oriented economy. A unique growth factor is the rapid expansion of the electronics manufacturing sector, which requires advanced corrosion protection solutions. This is significantly boosting the demand for VCI packaging products.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.8% of the market share in 2025 and is projected to grow at a CAGR of 5.9%. The growth is supported by increasing investments in infrastructure and industrial development. The region is gradually adopting advanced packaging solutions to support its growing industrial base.

Saudi Arabia is a key contributor to the regional market, driven by its expanding oil and gas and industrial sectors. A unique growth factor is the increasing focus on industrial diversification, which is creating demand for advanced packaging solutions, including VCI packaging, to protect metal components.

Latin America

Latin America held a market share of around 7.1% in 2025 and is expected to grow at the fastest CAGR of 6.8%. The region is witnessing growth in manufacturing and export activities, which is driving the demand for corrosion protection solutions.

Brazil dominates the regional market due to its strong industrial and automotive sectors. A unique growth factor is the increasing focus on export-oriented manufacturing, which requires reliable packaging solutions to ensure product quality during transportation.

Competitive Landscape

The competitive landscape of the volatile corrosion inhibitors Vci packaging market is moderately fragmented, with several global and regional players competing based on product innovation, quality, and pricing strategies. Leading companies are focusing on expanding their product portfolios and investing in research and development to improve the efficiency of VCI materials.

Cortec Corporation is recognized as a market leader due to its extensive range of VCI products and strong global presence. The company recently introduced a new line of biodegradable VCI films aimed at addressing environmental concerns and regulatory requirements. Other major players are also adopting similar strategies to strengthen their market position and expand their customer base.

Strategic partnerships, mergers, and acquisitions are common in this market, as companies aim to enhance their technological capabilities and geographic reach. The focus on sustainability and innovation is expected to shape the competitive landscape in the coming years.

Key Players List

- Cortec Corporation

- Daubert Cromwell

- Armor Protective Packaging

- Branopac GmbH

- Aicello Corporation

- OJI Paper Co., Ltd.

- MetPro Group

- RustX USA

- Protective Packaging Corporation

- Green Packaging Inc.

- Transcendia Inc.

- Northern Technologies International Corporation

- Shenyang Rustproof Packaging Material Co.

- LPS Industries

- Haver Plastics