Virgin Plastic Packaging Market Report Size and Growth

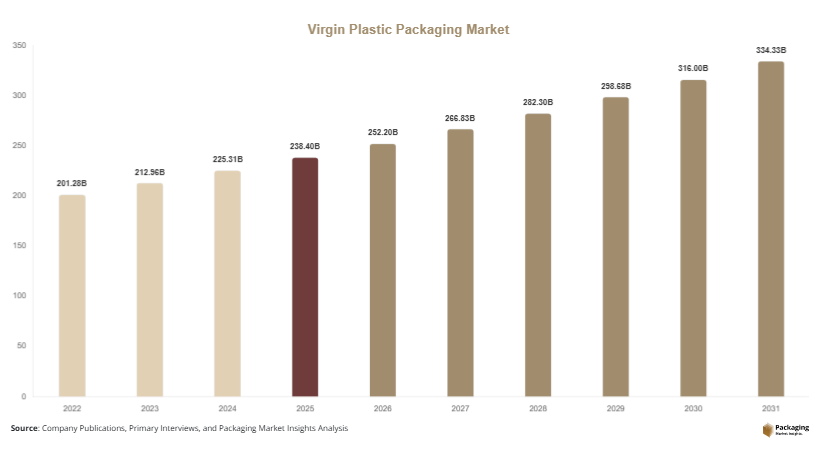

The Virgin Plastic Packaging Market was valued at USD 238.4 billion in 2025 and is projected to reach USD 329.6 billion by 2030, expanding at a compound annual growth rate (CAGR) of 5.8% between 2025 and 2031. Virgin plastic packaging refers to packaging materials produced from newly manufactured polymers rather than recycled plastic. These materials offer superior clarity, strength, and contamination resistance, making them widely used across food, beverage, pharmaceutical, and consumer goods industries.

One major global factor supporting the growth of the Virgin Plastic Packaging Market size is the rising demand for high-performance packaging in food safety and pharmaceutical logistics. Virgin plastics provide consistent structural integrity and barrier properties that are difficult to achieve with recycled alternatives. As global food distribution networks expand and pharmaceutical cold-chain requirements increase, manufacturers continue to rely on virgin plastic packaging solutions to maintain product quality and regulatory compliance.

In addition, emerging economies are witnessing rapid expansion in retail and e-commerce sectors, increasing demand for durable and lightweight packaging materials. The Virgin Plastic Packaging Market growth is also supported by technological improvements in polymer processing and advanced molding techniques that enhance packaging performance while optimizing production costs.

Key Highlights

- Asia Pacific dominated the market with 41.6% share in 2025, while Latin America is projected to record the fastest CAGR of 6.9% during the forecast period.

- Polyethylene (PE) was the leading material segment, accounting for 32.8% share, while polypropylene (PP) is projected to grow at the fastest CAGR of 6.5%.

- Food & beverage packaging was the dominant application segment with 38.4% share, while pharmaceutical packaging is projected to grow at a 7.2% CAGR.

- The United States, the dominant country market, recorded USD 52.6 billion in 2025 and is estimated to reach USD 55.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for High-Barrier Packaging Materials

A notable trend shaping the Virgin Plastic Packaging Market trends is the growing demand for high-barrier packaging materials. Industries such as food processing and pharmaceuticals require packaging that can effectively protect products from moisture, oxygen, and microbial contamination. Virgin plastic materials offer superior barrier properties and structural consistency compared with recycled plastics. As a result, manufacturers increasingly rely on virgin polymer packaging to maintain product safety and extend shelf life. This trend is particularly visible in packaged foods, ready-to-eat meals, and pharmaceutical blister packaging.

Technological Advancements in Polymer Processing

Another important trend influencing the Virgin Plastic Packaging Market analysis is the advancement in polymer processing technologies. Improved extrusion, injection molding, and blow-molding processes allow manufacturers to produce lighter yet stronger packaging materials. These innovations help reduce material consumption while maintaining durability and performance. Additionally, advanced polymer formulations are enabling the development of packaging solutions with improved clarity, flexibility, and chemical resistance. As packaging manufacturers continue to adopt advanced manufacturing technologies, the market is expected to witness steady innovation and improved product efficiency.

Market Drivers

Expanding Global Food Packaging Industry

The rapid expansion of the global food packaging industry has significantly contributed to the Virgin Plastic Packaging Market growth. Packaged food consumption has increased due to urbanization, busy lifestyles, and the growth of modern retail channels. Virgin plastic packaging offers reliable protection against contamination and moisture, ensuring longer shelf life for perishable products. Food manufacturers prefer virgin polymers because of their consistent quality and compliance with food safety standards. This factor continues to drive demand across both developed and developing economies.

Increasing Pharmaceutical Packaging Requirements

The pharmaceutical industry is another key contributor to the Virgin Plastic Packaging Market size. Pharmaceutical packaging requires materials with strict quality standards to prevent chemical reactions and contamination. Virgin plastic materials provide superior purity and stability compared with recycled plastics. As pharmaceutical manufacturing expands globally, demand for sterile and high-quality packaging solutions is increasing. Additionally, the rise in biologics, vaccines, and temperature-sensitive medications is further driving the use of virgin plastic packaging.

Market Restraint

Rising Environmental Concerns and Plastic Waste Regulations

One of the major restraints affecting the Virgin Plastic Packaging Market outlook is the increasing regulatory pressure related to plastic waste management. Governments across many regions are introducing policies to reduce single-use plastics and encourage the adoption of recycled or biodegradable materials. These regulations are influencing packaging manufacturers to reduce reliance on virgin plastic materials.

Environmental concerns about plastic pollution have also increased consumer awareness and demand for sustainable packaging solutions. Companies are gradually integrating recycled plastic content into their packaging strategies to meet sustainability goals and regulatory requirements.

Additionally, waste management challenges associated with plastic disposal have prompted policymakers to impose taxes, bans, or restrictions on certain plastic packaging formats. These factors may limit the growth potential of virgin plastic packaging in some markets. Although demand for high-performance packaging remains strong, regulatory pressures may encourage the development of alternative packaging materials.

Market Opportunities

Growth of E-Commerce Packaging

The rapid expansion of e-commerce platforms presents a significant opportunity for the Virgin Plastic Packaging Market forecast. Online retail requires durable and lightweight packaging materials that can withstand transportation and handling. Virgin plastic packaging provides excellent strength-to-weight ratios, making it suitable for protective packaging solutions. As e-commerce continues to expand globally, demand for reliable packaging materials is expected to increase.

Expansion of Medical and Healthcare Packaging

Another emerging opportunity in the Virgin Plastic Packaging Market industry is the growth of medical and healthcare packaging. Medical devices, diagnostic kits, and pharmaceutical products require packaging materials with strict hygiene and sterility standards. Virgin plastic materials provide contamination-free packaging solutions suitable for healthcare applications. As healthcare systems expand and medical product manufacturing increases, demand for specialized packaging materials is expected to grow steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 238.4 Billion |

| Market Size in 2026 | USD 252.2 Billion |

| Market Size in 2031 | USD 334.4 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polyethylene (PE) dominated the Virgin Plastic Packaging Market share by material, accounting for 32.8% of the global market in 2024. The dominance of polyethylene was attributed to its versatility, flexibility, and chemical resistance. PE is widely used in flexible packaging applications such as bags, pouches, and films. Food manufacturers prefer polyethylene packaging because of its moisture barrier properties and cost efficiency.

Polypropylene (PP) is projected to be the fastest-growing material segment with a CAGR of 6.5% during the forecast period. PP packaging will gain popularity due to its high heat resistance and durability. These properties will make it suitable for microwaveable food containers and pharmaceutical packaging. As demand for rigid and high-temperature packaging solutions increases, polypropylene usage will expand.

By Packaging Type

Rigid packaging represented the dominant packaging type with 56.3% share in 2024. Rigid plastic packaging includes bottles, containers, trays, and jars that provide structural strength and protection for packaged products. The segment’s dominance was supported by strong demand from the beverage, pharmaceutical, and personal care industries.

Flexible packaging is expected to grow at a CAGR of 6.8% during the forecast period. Flexible plastic packaging solutions such as films and pouches will gain popularity due to their lightweight structure and reduced material consumption. These packaging formats will support efficient transportation and storage, making them attractive for food packaging and e-commerce distribution.

By Application

Food & beverage packaging accounted for the largest share of 38.4% in the Virgin Plastic Packaging Market in 2024. The dominance of this segment was driven by high demand for packaging materials used in beverages, snacks, dairy products, and processed foods. Virgin plastic materials provided the necessary hygiene standards and protective barriers required for food packaging.

Pharmaceutical packaging is projected to grow at a CAGR of 7.2% during the forecast period. This growth will be driven by rising pharmaceutical manufacturing and increasing demand for sterile packaging solutions. Pharmaceutical packaging will require high-purity materials that ensure product safety and compliance with regulatory standards.

By End-Use Industry

The consumer goods industry represented the largest end-use segment with 34.7% share in 2024. Packaging materials used for personal care products, household goods, and cosmetics contributed significantly to the segment’s dominance. Virgin plastic packaging provided durability and visual appeal for branded consumer products.

The healthcare industry is expected to grow at a CAGR of 7.4% during the forecast period. Growth in medical device manufacturing and diagnostic product packaging will increase demand for sterile and contamination-free packaging materials. Virgin plastic packaging will play a crucial role in ensuring product integrity and safety.

Competitive Landscape

The Virgin Plastic Packaging Market industry features a competitive landscape with the presence of multinational packaging manufacturers and polymer producers. Companies focus on improving polymer processing technologies and expanding packaging product portfolios to strengthen market presence.

Amcor plc emerged as a prominent market leader due to its global packaging manufacturing capabilities and diverse product offerings. The company recently expanded its advanced polymer packaging solutions to enhance performance and efficiency in food and healthcare packaging applications.

Other major companies such as Berry Global Inc., Sealed Air Corporation, Sonoco Products Company, and Mondi Group maintain strong positions in the market through strategic partnerships, product innovations, and manufacturing expansions. These companies invest in advanced packaging technologies to improve material performance and production efficiency.

Increasing collaboration between polymer manufacturers and packaging converters is also shaping the competitive landscape, enabling the development of specialized packaging solutions tailored to specific industry applications.

Virgin Plastic Packaging Market Segmentations

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Polyvinyl Chloride (PVC)

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Application

- Food & Beverage

- Pharmaceuticals

- Personal Care

- Industrial Packaging

- Consumer Goods

By End-Use Industry

- Food Industry

- Healthcare Industry

- Consumer Goods Industry

- Industrial Sector

Regional Analysis

North America

North America accounted for 26.4% of the Virgin Plastic Packaging Market share in 2025. The regional market growth was supported by strong demand from the food processing and pharmaceutical sectors. During the forecast period, the regional market will expand at a CAGR of 5.4% between 2025 and 2033. Growth in packaged food consumption and advanced manufacturing capabilities will continue to support market expansion in this region.

The United States dominated the regional market due to its well-established packaging industry and strong presence of food processing companies. The country experienced steady demand for high-performance packaging materials that support food safety and pharmaceutical packaging requirements. The expansion of convenience food consumption and retail distribution networks contributed to the country’s market leadership.

Europe

Europe represented 23.1% of the global Virgin Plastic Packaging Market size in 2025. The region’s packaging industry has historically been influenced by strong manufacturing sectors and high demand for packaged consumer goods. Over the forecast period, the European market will grow at a CAGR of 4.9%. Market growth will be influenced by industrial packaging demand and advanced packaging technologies.

Germany emerged as the dominant country market within the region. The country’s strong manufacturing base and well-developed logistics infrastructure supported the demand for durable packaging solutions. German packaging manufacturers also focus on high-quality polymer processing technologies, enabling the production of advanced plastic packaging materials.

Asia Pacific

Asia Pacific held the largest share of 41.6% in the Virgin Plastic Packaging Market in 2025. Rapid industrialization, urban population growth, and expansion of the retail sector contributed to the region’s market leadership. The regional market will grow at a CAGR of 6.3% between 2025 and 2033, supported by increasing packaging demand from food and consumer goods industries.

China dominated the Asia Pacific market due to its large manufacturing sector and extensive packaging supply chains. The country’s food processing industry and export-oriented manufacturing sector created strong demand for reliable packaging materials. Additionally, rapid growth in packaged food consumption supported the expansion of plastic packaging manufacturing capacity.

Middle East & Africa

The Middle East & Africa accounted for 4.7% of the global Virgin Plastic Packaging Market share in 2025. Economic diversification strategies and expanding retail infrastructure contributed to the development of packaging industries in this region. During the forecast period, the regional market will grow at a CAGR of 5.2%.

Saudi Arabia dominated the regional market due to its strong petrochemical industry. The country’s polymer production capacity supported local manufacturing of plastic packaging materials. The expansion of food processing facilities and retail networks contributed to increasing demand for packaging solutions.

Latin America

Latin America represented 4.2% of the global Virgin Plastic Packaging Market in 2025. The region’s packaging demand was driven by growth in the food processing and beverage industries. During the forecast period, the regional market will grow at the fastest CAGR of 6.9%.

Brazil dominated the regional market due to its expanding consumer goods industry. The growth of packaged food consumption and retail distribution channels supported demand for plastic packaging materials. Additionally, improvements in packaging manufacturing infrastructure contributed to the country’s market development.

Competitive Landscape

The Virgin Plastic Packaging Market industry features a competitive landscape with the presence of multinational packaging manufacturers and polymer producers. Companies focus on improving polymer processing technologies and expanding packaging product portfolios to strengthen market presence.

Amcor plc emerged as a prominent market leader due to its global packaging manufacturing capabilities and diverse product offerings. The company recently expanded its advanced polymer packaging solutions to enhance performance and efficiency in food and healthcare packaging applications.

Other major companies such as Berry Global Inc., Sealed Air Corporation, Sonoco Products Company, and Mondi Group maintain strong positions in the market through strategic partnerships, product innovations, and manufacturing expansions. These companies invest in advanced packaging technologies to improve material performance and production efficiency.

Increasing collaboration between polymer manufacturers and packaging converters is also shaping the competitive landscape, enabling the development of specialized packaging solutions tailored to specific industry applications.

Key Players in the Virgin Plastic Packaging Market

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Mondi Group

- Huhtamaki Oyj

- DS Smith Plc

- Constantia Flexibles

- Smurfit Kappa Group

- Silgan Holdings Inc.

- ALPLA Group

- Winpak Ltd.

- AptarGroup Inc.

- Plastipak Holdings Inc.

- Graham Packaging Company