Vehicle Wrapping Pvc Film Market Size and Growth

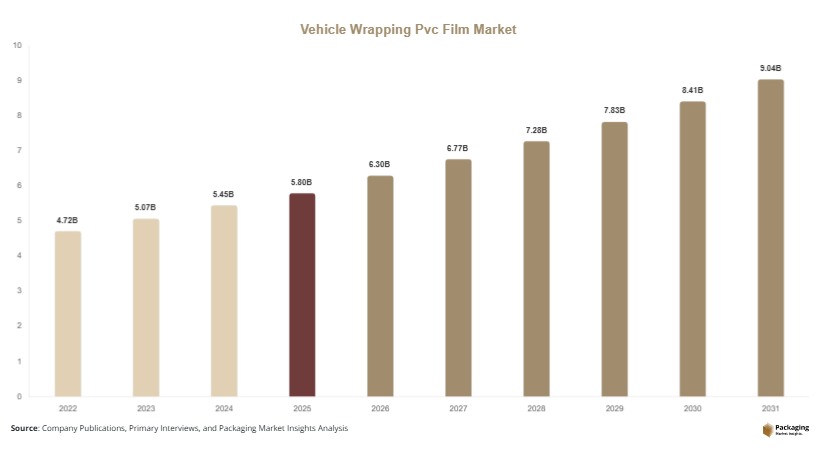

The vehicle wrapping pvc film market size was valued at USD 5.8 billion in 2025 and is expected to reach approximately USD 6.3 billion in 2026. Over the forecast period, the market is projected to reach USD 11.9 billion by 2034, expanding at a compound annual growth rate (CAGR) of 7.5% from 2025 to 2034. The increasing use of vehicle wraps for branding, protection, and aesthetic enhancement is contributing significantly to market expansion. The vehicle wrapping pvc film market is witnessing steady growth due to rising demand for cost-effective vehicle customization and advertising solutions.

One of the key growth factors is the growing popularity of vehicle advertising, particularly among small and medium enterprises. Vehicle wraps provide a cost-efficient alternative to traditional advertising methods, offering high visibility and long-term exposure. Businesses are increasingly adopting this medium to enhance brand recognition without recurring advertising costs.

Key Highlights:

- The market size was valued at USD 5.8 billion in 2025 and is projected to reach USD 11.9 billion by 2034. This growth reflects increasing adoption across both commercial and personal vehicle segments globally.

- The market is expected to register a CAGR of 7.5% during the forecast period from 2025 to 2034. Steady expansion is supported by rising investments in automotive customization and advertising solutions.

- The increasing adoption of vehicle wraps for advertising and branding purposes is driving demand. Businesses are leveraging mobile advertising to enhance visibility and reach a broader audience cost-effectively.

- Rising demand for vehicle customization and aesthetic enhancements is contributing to market growth. Consumers are opting for wraps to achieve unique designs without permanently altering the vehicle’s original paint.

- Advancements in PVC film technology are improving durability and performance. Innovations such as enhanced UV resistance and self-healing properties are extending product lifespan and usability.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

One significant trend in the vehicle wrapping pvc film market is the growing adoption of digitally printed wraps. Businesses are increasingly using high-resolution printing technologies to create customized designs for advertising and branding purposes. Digital printing allows for detailed graphics, vibrant colors, and complex patterns, making vehicle wraps more visually appealing and effective as marketing tools. This trend is particularly prominent among logistics companies, ride-sharing services, and delivery fleets, which use branded wraps to increase visibility. As printing technologies continue to advance, the demand for digitally compatible PVC films is expected to rise steadily.

Another notable trend is the increasing demand for eco-friendly and recyclable PVC films. With rising environmental concerns, manufacturers are focusing on developing sustainable alternatives that reduce environmental impact. This includes the use of non-toxic materials, reduced solvent emissions, and recyclable film structures. Regulatory pressures in regions such as Europe and North America are encouraging companies to adopt environmentally responsible production practices. As a result, the market is witnessing a gradual shift toward sustainable solutions, which is expected to influence product development and purchasing decisions in the coming years.

Market Drivers

A primary driver of the vehicle wrapping pvc film market is the expansion of the automotive aftermarket industry. As vehicle ownership continues to increase globally, the demand for aftermarket customization products is rising. Vehicle wraps offer a flexible and cost-effective way to modify the appearance of vehicles without permanent changes. This has led to increased adoption among car enthusiasts and professional service providers. Additionally, the availability of a wide range of colors, finishes, and textures has further boosted consumer interest in vehicle wrapping solutions.

Another key driver is the growing use of vehicle wraps in commercial advertising. Companies across various industries are leveraging vehicle wraps as mobile billboards to reach a wider audience. This form of advertising offers continuous exposure and is often more cost-effective than traditional media channels. Fleet operators, in particular, are adopting wraps to promote their brands while maintaining a consistent visual identity. The increasing emphasis on cost-efficient marketing strategies is expected to drive continued demand for PVC wrapping films.

Market Restraint

One of the major restraints in the vehicle wrapping pvc film market is the limited durability of PVC films under extreme environmental conditions. While modern films offer improved resistance to UV rays and weathering, prolonged exposure to harsh sunlight, high temperatures, and humidity can lead to fading, cracking, or peeling. This affects the overall lifespan and performance of the wraps, leading to additional maintenance or replacement costs.

The impact of this restraint is particularly evident in regions with extreme climates, where vehicle wraps may require frequent replacement. For example, commercial fleets operating in hot and humid environments may experience reduced film durability, increasing operational expenses. Additionally, improper installation or low-quality materials can further exacerbate these issues, affecting customer satisfaction and market adoption. Manufacturers are addressing this challenge by investing in research and development to enhance film durability and performance.

Market Opportunities

One significant opportunity in the vehicle wrapping pvc film market lies in the increasing adoption of electric vehicles (EVs). As the EV market continues to grow, manufacturers and owners are seeking innovative ways to differentiate their vehicles. Vehicle wraps provide a cost-effective solution for branding and customization, particularly for EV fleets used in ride-sharing and delivery services. This trend is expected to create new demand for PVC wrapping films, especially in urban areas with high EV adoption rates.

Another key opportunity is the expansion of the market in emerging economies. Countries in Asia Pacific, Latin America, and the Middle East are experiencing rapid urbanization and growth in vehicle ownership. This creates a favorable environment for the adoption of vehicle wrapping solutions. Additionally, the increasing presence of local advertising agencies and customization service providers is supporting market growth. As disposable incomes rise and consumer preferences evolve, the demand for vehicle wraps is expected to increase significantly in these regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Size in 2026 | USD 6.3 Billion |

| Market Size in 2034 | USD 11.9 Billion |

| CAGR | 7.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Cast PVC films dominated the market, accounting for approximately 60% of the market share in 2024. These films are widely preferred due to their superior flexibility, durability, and conformability. Cast films can easily adapt to complex vehicle surfaces, making them suitable for full wraps and intricate designs. Additionally, their resistance to shrinking and cracking enhances their lifespan, making them a preferred choice for professional applications. The increasing demand for high-quality wraps in commercial advertising and vehicle customization further supports the dominance of this segment.

Calendered PVC films are expected to be the fastest-growing subsegment, with a projected CAGR of 8.2% during the forecast period. These films are more cost-effective compared to cast films, making them suitable for short-term applications such as promotional campaigns. The growing demand for budget-friendly wrapping solutions among small businesses is driving the adoption of calendered films. Additionally, advancements in manufacturing processes are improving their performance and durability.

By Application

Advertising and branding applications accounted for the largest share of around 65% in 2024. Vehicle wraps are widely used as mobile advertising platforms, offering continuous exposure and high visibility. Businesses across various industries are adopting this medium to enhance brand recognition and reach a wider audience. The increasing emphasis on cost-effective marketing strategies is driving the demand for PVC wrapping films in this segment.

Personal vehicle customization is expected to be the fastest-growing subsegment, with a CAGR of 8.7%. The rising interest in vehicle aesthetics and individuality is encouraging consumers to opt for custom wraps. The availability of diverse colors, finishes, and textures supports this trend. Additionally, the ease of application and removal makes wraps an attractive alternative to traditional paint.

By End-Use

Commercial fleets dominated the market, holding approximately 62% of the share in 2024. Fleet operators use vehicle wraps for branding and advertising purposes, ensuring consistent visibility across different locations. The increasing number of delivery and logistics vehicles is driving demand for wrapping solutions. Additionally, wraps help protect the original paint, reducing maintenance costs.

Individual consumers represent the fastest-growing segment, with a CAGR of 8.9%. The growing popularity of vehicle customization among car enthusiasts is a key factor driving this growth. Consumers are increasingly opting for wraps to personalize their vehicles and enhance their appearance. This trend is expected to continue as awareness and availability of wrapping solutions increase.

Vehicle Wrapping Pvc Film Market Segmentations

By Type

- Cast PVC Films

- Calendered PVC Films

By Application

- Advertising & Branding

- Personal Vehicle Customization

By End-User

- Commercial Fleets

- Individual Consumers

Regional Analysis

North America

North America held a significant share of approximately 35% in the vehicle wrapping pvc film market in 2025 and is expected to grow at a CAGR of 7.2% during the forecast period. The region benefits from a well-established automotive aftermarket industry and high adoption of vehicle advertising solutions. The presence of advanced printing technologies and skilled service providers further supports market growth. Additionally, increasing demand for premium customization options contributes to the expansion of the market.

The United States dominates the North American market due to its large vehicle fleet and strong advertising industry. A unique growth factor in this region is the widespread use of vehicle wraps in political campaigns and event promotions. This creates consistent demand for high-quality PVC films, supporting market expansion.

Europe

Europe accounted for around 28% of the global market share in 2025 and is projected to grow at a CAGR of 6.8% through 2034. The region is characterized by strong regulatory frameworks and increasing focus on sustainability. The adoption of eco-friendly PVC films is gaining traction, supported by government initiatives and consumer awareness. Additionally, the presence of leading automotive manufacturers contributes to market growth.

Germany is a key market in Europe, driven by its robust automotive industry. A unique growth factor is the increasing demand for protective wraps that preserve vehicle paint quality. This trend is particularly prominent among luxury vehicle owners, supporting the adoption of advanced PVC films.

Asia Pacific

Asia Pacific is expected to witness the fastest growth, with a CAGR of 8.5% during the forecast period. The region accounted for approximately 24% of the market share in 2025. Rapid urbanization, increasing vehicle ownership, and expanding advertising industries are key factors driving growth. Additionally, the availability of cost-effective materials and labor supports market expansion.

China leads the Asia Pacific market due to its large automotive industry and growing advertising sector. A unique growth factor is the increasing use of vehicle wraps in e-commerce delivery fleets. This trend is driving demand for durable and visually appealing PVC films.

Middle East & Africa

The Middle East & Africa region held a market share of around 7% in 2025 and is projected to grow at a CAGR of 6.5% during the forecast period. The market is driven by increasing investments in advertising and automotive sectors. The demand for vehicle customization is rising, particularly in urban areas. Additionally, the growing tourism industry supports the use of branded vehicles.

The United Arab Emirates is a dominant market in this region. A unique growth factor is the high demand for luxury vehicle customization, which drives the adoption of premium PVC wrapping films.

Latin America

Latin America accounted for approximately 6% of the global market in 2025 and is expected to grow at a CAGR of 6.9% through 2034. The region is witnessing gradual growth due to increasing vehicle ownership and expanding advertising activities. The rising popularity of vehicle wraps as a marketing tool supports market development.

Brazil is the leading market in Latin America, driven by its growing automotive sector. A unique growth factor is the increasing adoption of vehicle wraps by small businesses for local advertising, boosting demand for cost-effective PVC films.

Competitive Landscape

The vehicle wrapping pvc film market is characterized by moderate competition, with several global and regional players focusing on product innovation and strategic partnerships. Companies are investing in research and development to introduce advanced films with improved durability, ease of application, and environmental sustainability. The market also witnesses collaborations between film manufacturers and printing technology providers to enhance product offerings.

3M Company is a leading player in the market, known for its extensive range of high-performance wrapping films. The company recently introduced a new line of eco-friendly PVC films designed to reduce environmental impact while maintaining performance standards. Other key players are focusing on expanding their distribution networks and strengthening their presence in emerging markets to capture growth opportunities.

Key Players List

- 3M Company

- Avery Dennison Corporation

- Arlon Graphics LLC

- Orafol Group

- Hexis S.A.S

- Ritrama S.p.A.

- Vvivid Vinyl

- KPMF Limited

- LINTEC Corporation

- JMR Graphics

- Fellers LLC

- Kay Premium Marking Films

- Grafityp Selfadhesive Products

- Guangzhou Carbins Film Co., Ltd.

- Zhejiang Kinlong New Material Co., Ltd.