VCI Anti Corrosion Film Market Size and Growth

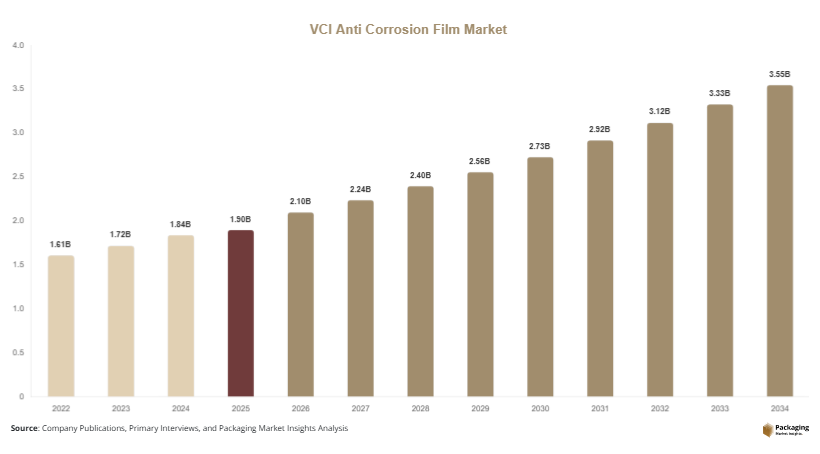

The global VCI anti corrosion film market size was valued at USD 1.9 billion in 2025 and is projected to reach USD 2.1 billion in 2026, further expanding to approximately USD 3.8 billion by 2034, registering a CAGR of 6.8% during the forecast period (2025–2034). VCI (Volatile Corrosion Inhibitor) films are widely used to prevent corrosion of metal components during storage and transportation by releasing corrosion-inhibiting vapors that form a protective layer on metal surfaces. The VCI anti corrosion film market is witnessing steady expansion due to increasing demand for protective packaging solutions across industries such as automotive, electronics, metal processing, and aerospace.

A key growth factor driving the VCI anti corrosion film market is the rapid expansion of global manufacturing industries. Increased production of automotive components, machinery, and industrial equipment has heightened the need for effective corrosion protection during logistics and warehousing. Another important factor is the growth in international trade, which requires reliable packaging solutions to protect metal goods over long transit periods. Additionally, rising awareness regarding product quality and durability is encouraging manufacturers to adopt advanced packaging materials such as VCI films.

Key Highlights:

- Asia Pacific dominated the market with a 39.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

- Polyethylene-based films led the type segment with a 48.3% share, while biodegradable VCI films are expected to grow at a CAGR of 7.5%.

- Flexible packaging dominated with a 55.6% share, while rigid packaging is forecasted to grow at a CAGR of 6.1%.

- Automotive applications led the segment with 44.7% share, while electronics applications are expected to grow at a CAGR of 6.9%.

- China remained the dominant country with a market size of USD 0.6 billion in 2025 and USD 0.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing development of eco-friendly and recyclable VCI films

The VCI anti corrosion film market is experiencing a shift toward environmentally sustainable products. Manufacturers are focusing on developing recyclable and biodegradable VCI films to align with global environmental regulations and corporate sustainability goals. Traditional plastic-based films are being replaced or modified with eco-friendly alternatives that maintain corrosion protection efficiency while reducing environmental impact. This trend is gaining traction in regions with strict environmental policies, such as Europe and North America. Companies are investing in research to create films that degrade faster without compromising performance. This movement toward sustainability is expected to influence product innovation and drive long-term market growth.

Growing demand from global logistics and export-oriented industries

The increasing globalization of trade is significantly impacting the demand for VCI anti corrosion films. Industries involved in exporting metal components require reliable packaging solutions to prevent corrosion during long-distance transportation. VCI films provide an efficient and cost-effective method of protecting products without the need for additional coatings or oils. The growth of e-commerce in industrial goods and expansion of supply chains are further contributing to demand. Logistics providers are also adopting advanced packaging materials to reduce product damage and returns. This trend is expected to continue as international trade volumes increase and supply chains become more complex.

Market Drivers

Expansion of automotive and industrial manufacturing sectors

The growth of automotive and industrial manufacturing sectors is a major factor driving the VCI anti corrosion film market. These industries produce large volumes of metal components that require protection from corrosion during storage and transportation. VCI films offer a convenient and efficient solution, reducing the need for additional protective measures. The increasing production of vehicles, machinery, and equipment is directly contributing to demand. Additionally, manufacturers are focusing on improving product quality and reducing maintenance costs, which further supports the adoption of VCI films. This driver is particularly strong in emerging economies with expanding industrial bases.

Rising focus on reducing product damage and maintenance costs

Companies are increasingly prioritizing the reduction of product damage and associated costs. Corrosion can lead to significant financial losses, especially in industries dealing with high-value metal components. VCI anti corrosion films help prevent such losses by providing reliable protection throughout the supply chain. The adoption of these films reduces the need for rework, repairs, and replacements, resulting in cost savings. Additionally, the ease of use and efficiency of VCI films make them an attractive option for manufacturers and logistics providers. This focus on cost optimization is expected to drive market growth.

Market Restraint

Limited awareness and higher initial costs in developing regions

One of the key challenges facing the VCI anti corrosion film market is the limited awareness of advanced corrosion protection solutions in developing regions. Many small and medium-sized enterprises continue to rely on traditional methods such as oils and coatings, which are often less effective but cheaper. The higher initial cost of VCI films can deter adoption, particularly in price-sensitive markets. Additionally, lack of technical knowledge about the benefits and application methods of VCI films further restricts market penetration. This restraint can slow growth in emerging economies, despite the increasing need for corrosion protection solutions.

Market Opportunities

Increasing adoption in electronics and precision engineering industries

The growing demand for VCI films in electronics and precision engineering industries presents a significant opportunity for market expansion. These industries require high levels of protection for sensitive metal components, which are prone to corrosion. VCI films provide a clean and efficient solution without leaving residues, making them ideal for such applications. As the production of electronic devices and precision equipment increases, the demand for advanced packaging solutions is expected to rise. This opportunity is particularly relevant in regions with strong electronics manufacturing sectors.

Technological advancements in multi-layer and high-performance films

Advancements in film technology are creating new opportunities for the VCI anti corrosion film market. Manufacturers are developing multi-layer films with enhanced barrier properties and longer protection durations. These innovations are improving the performance and reliability of VCI films, making them suitable for a wider range of applications. Additionally, the integration of smart packaging technologies is enabling real-time monitoring of product conditions. These technological developments are expected to drive market growth by offering more efficient and advanced corrosion protection solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.9 Billion |

| Market Size in 2026 | USD 2.1 Billion |

| Market Size in 2034 | USD 3.8 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyethylene-based VCI films accounted for the largest share of approximately 48.3% in 2024. These films are widely used due to their durability, flexibility, and cost-effectiveness. They provide reliable corrosion protection for a wide range of metal components, making them a preferred choice across industries. The segment’s dominance is also supported by the availability of raw materials and established manufacturing processes.

Biodegradable VCI films are expected to grow at the fastest CAGR of 7.5% during the forecast period. Increasing environmental concerns and regulatory pressure are driving the adoption of sustainable alternatives. These films offer effective corrosion protection while reducing environmental impact, making them an attractive option for industries seeking eco-friendly solutions.

By Application

The automotive segment held the largest share of 44.7% in 2024. The high volume of metal components used in vehicle manufacturing drives demand for corrosion protection solutions. VCI films are widely used to protect parts during storage and transportation, ensuring product quality and reducing maintenance costs.

The electronics segment is projected to grow at a CAGR of 6.9%, driven by increasing production of electronic devices. The need for clean and residue-free corrosion protection is encouraging the adoption of VCI films in this segment.

By End-Use

The industrial segment accounted for 55.6% of the market share in 2024. This includes manufacturing, logistics, and heavy industries that require effective corrosion protection solutions. The segment’s dominance is driven by the high volume of metal products handled in these industries.

The export packaging segment is expected to grow at a CAGR of 6.7%. Increasing global trade and the need for reliable packaging solutions during long-distance transportation are driving demand in this segment.

VCI Anti Corrosion Film Market Segmentations

By Product Type

- Polyethylene-Based VCI Films

- Biodegradable VCI Films

- Other Specialty VCI Films

By Application

- Automotive

- Electronics

- Metal Processing

- Aerospace

By End-Use Industry

- Industrial Manufacturing

- Export Packaging

- Logistics and Warehousing

Regional Analysis

North America

North America accounted for approximately 21.8% of the VCI anti corrosion film market share in 2025 and is projected to grow at a CAGR of 5.8% during the forecast period. The region benefits from a well-established industrial base and strong demand for advanced packaging solutions. Increasing focus on reducing product damage and improving supply chain efficiency is supporting market growth.

The United States dominates the regional market, driven by high demand from automotive and aerospace industries. A unique growth factor is the adoption of advanced logistics systems that require reliable corrosion protection solutions, encouraging the use of VCI films across supply chains.

Europe

Europe held a market share of 23.6% in 2025 and is expected to grow at a CAGR of 6.0%. The region is characterized by strict environmental regulations and a strong emphasis on sustainable packaging solutions. These factors are driving the adoption of eco-friendly VCI films.

Germany is the leading country in the European market, supported by its strong manufacturing sector. A unique growth factor is the region’s focus on high-quality industrial standards, which increases the demand for effective corrosion protection solutions.

Asia Pacific

Asia Pacific dominated the market with a 39.1% share in 2025 and is projected to grow at a CAGR of 7.1%. Rapid industrialization, expanding manufacturing activities, and increasing exports are key drivers of market growth in the region.

China leads the Asia Pacific market due to its large manufacturing base and high export volumes. A unique growth factor is the availability of cost-effective production facilities, which supports the widespread adoption of VCI films.

Middle East & Africa

The Middle East & Africa region accounted for 7.2% of the market share in 2025 and is expected to grow at a CAGR of 6.3%. Growth is driven by increasing industrialization and demand for protective packaging solutions in the oil and gas sector.

The United Arab Emirates is the dominant country in this region, supported by its growing logistics and trade activities. A unique growth factor is the expansion of industrial zones and free trade areas, which increases demand for corrosion protection solutions.

Latin America

Latin America held a market share of 8.3% in 2025 and is projected to grow at the fastest CAGR of 7.2%. The region is experiencing increasing demand for industrial packaging solutions due to expanding manufacturing activities.

Brazil dominates the Latin American market, supported by its growing industrial sector. A unique growth factor is the increasing investment in infrastructure development, which drives demand for corrosion protection materials.

Competitive Landscape

The VCI anti corrosion film market is moderately competitive, with several key players focusing on innovation and expansion strategies. Companies are investing in research and development to improve product performance and develop eco-friendly solutions. Strategic partnerships and acquisitions are also common, enabling companies to expand their market presence.

Cortec Corporation is a leading player in the market, known for its advanced corrosion protection technologies. The company recently introduced a new range of biodegradable VCI films, aligning with sustainability trends. Other major players are also expanding their product portfolios and strengthening their distribution networks to remain competitive.

Key Players List

- Cortec Corporation

- NTIC (Northern Technologies International Corporation)

- Daubert Cromwell

- Armor Protective Packaging

- Aicello Corporation

- Branopac GmbH

- MetPro Group

- Protective Packaging Corporation

- Green Packaging Inc.

- RustX USA

- Zerust Excor

- Transilwrap Company Inc.

- Polymer Packaging Inc.

- LPS Industries LLC

- OJI Intertech Inc.