US Black Rigid Plastic Packaging Report Size and Growth

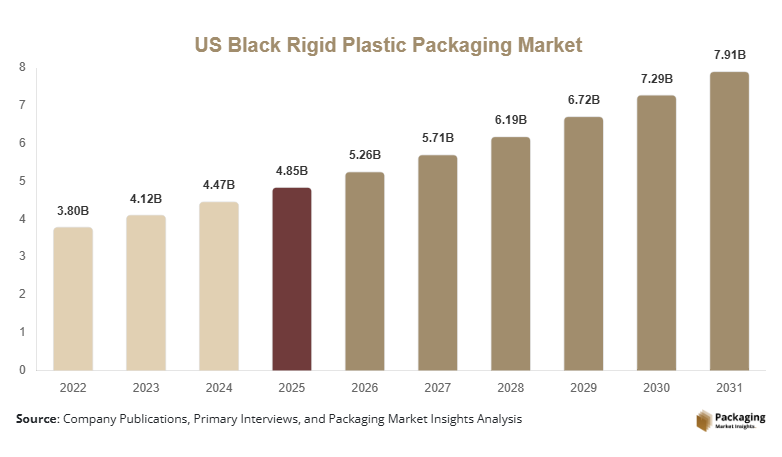

The US Black Rigid Plastic Packaging Market was valued at USD 4.85 billion in 2025 and is projected to reach USD 7.92 billion by 2031, expanding at a CAGR of 8.5% during the forecast period (2025–2031). Black rigid plastic packaging is widely used across food, personal care, healthcare, and industrial sectors due to its durability, aesthetic appeal, light-blocking properties, and ability to protect sensitive products. Containers, trays, jars, and bottles manufactured using materials such as polypropylene (PP), polyethylene terephthalate (PET), and high-density polyethylene (HDPE) form the backbone of this packaging segment.

A major global factor supporting market expansion is the rapid growth of organized retail and e-commerce supply chains, which require durable packaging capable of maintaining product quality during storage and transportation. Black rigid plastic packaging provides enhanced UV protection and premium shelf appearance, making it highly suitable for cosmetics, ready-to-eat meals, and pharmaceutical packaging.

In addition, advancements in recyclable and carbon-neutral plastics, combined with improved black pigment technologies that allow automated sorting during recycling, have improved sustainability credentials. These innovations are encouraging manufacturers and brand owners to adopt black rigid plastic packaging solutions while complying with environmental guidelines.

Key Highlights

- North America accounted for the dominant regional share of 38.6% in 2025, while Asia Pacific is expected to grow at the fastest CAGR of 9.4% during the forecast period.

- By material, polypropylene (PP) held the leading share of 32.4% in 2024, whereas recycled PET (rPET) is expected to record the fastest CAGR of 10.1%.

- By product type, bottles and containers dominated the market with 36.8% share in 2024, while rigid trays are projected to expand at 9.6% CAGR.

- By end-use industry, food & beverage remained the dominant segment with 41.2% share, while personal care & cosmetics will grow the fastest at 9.2% CAGR.

- The United States remained the dominant country market, valued at USD 4.85 billion in 2025 and USD 5.23 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Recyclable Black Plastic Technologies

One of the most notable trends shaping the US Black Rigid Plastic Packaging Market is the development of recyclable black plastic formulations compatible with optical sorting systems used in recycling facilities. Traditionally, carbon-black pigments made black plastic difficult to detect in recycling streams. However, newer pigment technologies enable packaging to be recognized by near-infrared sorting systems.

Packaging manufacturers are increasingly investing in recyclable PP and PET containers with alternative pigments that maintain the premium black appearance while improving recyclability. Retail brands and food companies are adopting these materials to meet sustainability commitments and reduce landfill waste.

Premiumization in Food and Cosmetic Packaging

Another significant trend influencing the US Black Rigid Plastic Packaging Market growth is the rising demand for premium packaging aesthetics. Black packaging is widely perceived as sophisticated and high-end, which makes it particularly attractive for cosmetics, gourmet foods, and luxury personal care products.

Companies are increasingly using matte-finish black containers, textured surfaces, and minimalist designs to enhance brand identity. The trend toward premium product positioning in retail channels is expected to accelerate demand for visually distinctive rigid plastic packaging formats.

Market Drivers

Growing Demand from Food Packaging Industry

The expansion of the ready-to-eat meals and convenience food sector is a key factor driving the US Black Rigid Plastic Packaging Market size. Black rigid plastic trays and containers provide superior heat resistance and visual appeal for packaged meals, particularly in refrigerated and microwaveable food products.

Food service operators and grocery retailers increasingly rely on durable plastic trays and bowls for deli products, salads, and prepared meals. The material’s ability to maintain structural integrity during heating and storage makes it suitable for modern food distribution systems.

Increasing Use in Personal Care and Cosmetic Packaging

The personal care industry is also contributing significantly to US Black Rigid Plastic Packaging Market growth. Black packaging is widely used for shampoos, lotions, cosmetic jars, and fragrance containers due to its ability to protect light-sensitive formulations.

Brands also prefer black packaging to reinforce premium brand positioning. The growing demand for skincare products, men's grooming products, and specialty cosmetics in the United States continues to stimulate the adoption of black rigid plastic containers.

Market Restraint

Environmental Concerns and Recycling Limitations

A major restraint affecting the US Black Rigid Plastic Packaging Market is the environmental concerns associated with plastic waste management. Despite technological improvements, black plastics historically posed recycling challenges due to sorting limitations and contamination in recycling streams.

Regulatory authorities and environmental organizations are increasing pressure on packaging producers to improve recyclability and reduce the environmental footprint of plastic packaging. Compliance with sustainability targets and extended producer responsibility programs may increase operational costs for packaging manufacturers.

These challenges may encourage the gradual shift toward alternative materials such as paperboard and biodegradable polymers in certain packaging applications.

Market Opportunities

Development of Sustainable Recycled Plastics

The growing availability of recycled polymers such as rPET and recycled polypropylene is creating new opportunities for manufacturers operating in the US Black Rigid Plastic Packaging Market. These materials allow companies to reduce virgin plastic usage while maintaining packaging strength and appearance.

Brand owners are increasingly committing to packaging made with recycled content to meet sustainability goals and consumer expectations. As supply chains for recycled plastics become more efficient, adoption across packaging applications is expected to accelerate.

Growth in Pharmaceutical Packaging Applications

Another emerging opportunity is the expanding use of black rigid plastic packaging in pharmaceutical and healthcare products. Certain medicines and nutraceuticals require protection from light exposure, which black plastic containers can provide.

The rising demand for over-the-counter medicines, vitamins, and dietary supplements in the United States is expected to increase demand for protective packaging solutions. Manufacturers developing high-barrier and UV-resistant containers are likely to benefit from this trend.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.85 Billion |

| Market Size in 2026 | USD 5.26 Billion |

| Market Size in 2031 | USD 7.29 Billion |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polypropylene (PP) held the dominant position in the US Black Rigid Plastic Packaging Market with a 32.4% share in 2024. The material was widely used in rigid containers, trays, and caps due to its chemical resistance, durability, and cost efficiency. Polypropylene packaging maintained its leadership position as manufacturers relied on its ability to withstand heat and maintain structural strength in food and industrial applications.

The recycled polyethylene terephthalate (rPET) segment is expected to witness the fastest expansion with a projected CAGR of 10.1% during the forecast period. This growth will be supported by increasing demand for sustainable packaging materials. Manufacturers will continue investing in recycled plastic processing technologies to produce high-quality packaging materials suitable for food and beverage applications.

By Product Type

The bottles and containers segment dominated the US Black Rigid Plastic Packaging Market share with 36.8% in 2024. These packaging formats were widely used in beverages, personal care products, pharmaceuticals, and household chemicals. Bottles offer structural stability, ease of transportation, and compatibility with automated filling lines.

The rigid trays segment will experience the fastest growth, expanding at a projected CAGR of 9.6%. The increasing popularity of packaged ready-to-eat meals and fresh produce packaging will drive demand for rigid plastic trays. These packaging solutions provide durability and product visibility, making them suitable for modern food retail environments.

By End-Use Industry

The food and beverage industry accounted for the largest share of the US Black Rigid Plastic Packaging Market with 41.2% in 2024. Black plastic trays and containers were extensively used in deli products, bakery items, and ready meals. Their ability to protect products from light exposure and maintain freshness contributed to their widespread adoption.

The personal care and cosmetics segment will record the fastest growth with a projected CAGR of 9.2%. Increasing consumer demand for skincare products and premium cosmetic packaging will drive the adoption of aesthetically appealing black plastic containers across beauty brands.

US Black Rigid Plastic Packaging Market Segmentations

By Material

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Polystyrene (PS)

- Recycled Plastics

By Product Type

- Bottles & Containers

- Jars

- Trays

- Caps & Closures

- Tubs

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- Household Products

- Industrial Packaging

Regional Analysis

North America

North America accounted for 38.6% of the global market share in 2025 in the US Black Rigid Plastic Packaging Market analysis. The region’s packaging industry has historically benefited from strong manufacturing infrastructure, advanced recycling capabilities, and a high level of consumer packaged goods consumption. Over the forecast period, the regional market will grow at a CAGR of 8.2% between 2025 and 2033.

Demand within North America is primarily driven by the presence of large food processing companies, pharmaceutical manufacturers, and personal care brands that rely on rigid plastic packaging solutions. The region also has a strong network of packaging manufacturers and technology providers developing innovative rigid packaging materials.

The United States remained the dominant country in this region due to the scale of its consumer goods market and retail sector. A distinct growth factor for the US market is the increasing adoption of advanced packaging automation and lightweight container designs, which improve efficiency in production and logistics operations. The integration of automated filling and sealing lines across food and cosmetic packaging plants continues to encourage demand for standardized rigid plastic packaging formats.

Europe

Europe held approximately 24.7% of the global market share in 2025. The region has a mature packaging sector supported by strict environmental regulations and strong consumer demand for sustainable packaging. The European market will grow at a projected CAGR of 7.8% during 2025–2033.

Several European countries are implementing circular economy initiatives aimed at improving recycling rates and reducing plastic waste. These policies are influencing the adoption of recyclable plastics and improved packaging designs. The shift toward recyclable materials is gradually reshaping the packaging supply chain across the region.

Within Europe, Germany represented the dominant country market due to its well-established manufacturing sector and large consumer packaged goods industry. A key factor supporting market expansion in Germany is the country’s focus on high-performance packaging materials used in automotive components, industrial chemicals, and consumer goods. This industrial demand continues to sustain the growth of rigid plastic packaging formats.

Asia Pacific

Asia Pacific represented 21.5% of the global market share in 2025 and is expected to register the fastest CAGR of 9.4% between 2025 and 2033. Rapid industrialization, urban population growth, and expansion of the food processing industry are contributing to increasing packaging demand across the region.

The region is experiencing a surge in retail modernization and packaged food consumption, which has increased the need for reliable packaging solutions. Manufacturers are expanding production facilities to serve growing demand from consumer goods industries.

China remained the dominant country in Asia Pacific due to its large manufacturing base and expanding consumer market. The country’s strong growth factor is the rapid development of food processing and export industries, which require durable packaging materials capable of maintaining product quality during transportation and storage.

Middle East & Africa

The Middle East & Africa region accounted for 7.6% of the global market share in 2025. Although smaller in comparison to other regions, the market is supported by increasing urbanization and rising demand for packaged consumer goods. The region will grow at a CAGR of 7.2% between 2025 and 2033.

Infrastructure improvements and investment in retail supply chains are gradually increasing demand for rigid plastic packaging solutions. Food and beverage companies operating in the region are expanding production to meet the needs of growing populations.

Within this region, the United Arab Emirates emerged as the dominant country market due to its role as a regional trade hub. A distinct factor driving market development in the UAE is the expansion of modern retail formats and food import distribution networks, which require reliable packaging solutions to maintain product quality across long supply chains.

Latin America

Latin America held approximately 7.6% of the global market share in 2025. The regional packaging industry is supported by increasing consumption of packaged foods and personal care products. Over the forecast period, the market will grow at a CAGR of 7.5% between 2025 and 2033.

Growth in the region is influenced by improvements in manufacturing capacity and the expansion of retail distribution channels. Consumer goods companies are investing in packaging technologies that improve product shelf life and reduce transportation damage.

Brazil remained the leading country in Latin America due to its large consumer market and growing food processing industry. A key factor supporting market growth in Brazil is the expansion of domestic packaged food production, which requires durable packaging containers capable of maintaining product integrity during transportation.

Competitive Landscape

The US Black Rigid Plastic Packaging Market features a competitive landscape with several packaging manufacturers operating across multiple industries. Companies compete based on product innovation, sustainability initiatives, and manufacturing capabilities.

Berry Global Inc. is considered a leading participant in the market, supported by its extensive product portfolio and advanced plastic processing technologies. The company recently introduced recyclable black plastic packaging solutions designed for improved compatibility with recycling systems, strengthening its sustainability positioning.

Other major players focus on expanding manufacturing capacity, developing lightweight packaging formats, and improving recycled plastic integration into packaging product.

Key Players

- Berry Global Inc.

- Amcor plc

- Silgan Holdings Inc.

- Plastipak Holdings Inc.

- Sonoco Products Company

- ALPLA Group

- Greiner Packaging

- Graham Packaging Company

- Pact Group Holdings Ltd.

- IPL Plastics Inc.

- Mauser Packaging Solutions

- Alpha Packaging

- Container Corporation of Canada

- Pretium Packaging LLC

- AptarGroup Inc.