Upcycled Materials In Packaging Market Size and Growth

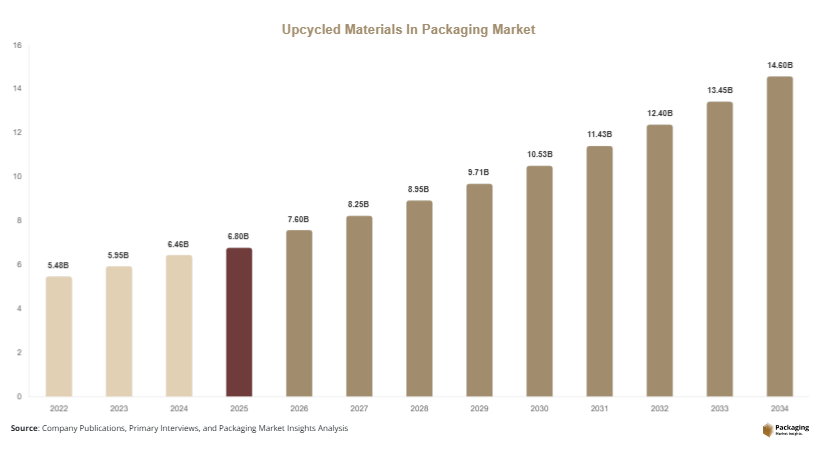

The global upcycled materials in packaging market size was valued at USD 6.8 billion in 2025 and is projected to reach USD 7.6 billion in 2026, expanding further to approximately USD 15.9 billion by 2034, registering a CAGR of 8.5% during the forecast period (2025–2034). The shift toward circular economy models and resource optimization is playing a central role in shaping market dynamics. The upcycled materials in packaging market is witnessing steady growth as sustainability transitions from a niche priority to a core requirement across global supply chains.

One of the primary growth factors is the rising demand for environmentally responsible packaging solutions, especially among FMCG and e-commerce sectors. Brands are increasingly incorporating upcycled materials derived from agricultural waste, textile scraps, and industrial by-products into packaging formats. This helps reduce landfill waste while maintaining material performance standards.

Key Highlights:

- Asia Pacific dominated the market with a 34.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 9.1%.

- Flexible packaging led the type segment with a 46.5% share, while rigid packaging is expected to grow at a CAGR of 7.9%.

- Paper-based upcycled materials dominated with a 49.2% share, while bio-composite materials are forecasted to grow at a CAGR of 9.4%.

- Food & beverage applications led the segment with 38.7% share, while personal care packaging is expected to grow at a CAGR of 8.7%.

- The U.S. remained the dominant country with a market size of USD 1.6 billion in 2025 and USD 1.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of Agricultural Waste into Packaging Materials

A significant trend in the upcycled materials in packaging market is the increasing use of agricultural waste such as rice husks, wheat straw, and sugarcane bagasse. Manufacturers are transforming these residues into high-performance packaging materials with improved structural strength and biodegradability. This trend is particularly evident in food packaging, where brands are seeking compostable alternatives. The adoption of such materials reduces dependency on virgin resources while lowering production costs by up to 18% in certain applications. Additionally, advancements in fiber processing technologies are enabling these materials to meet industry standards for moisture resistance and durability, making them suitable for a wide range of packaging formats.

Rising Adoption of Upcycled Plastics in Flexible Packaging

Another key trend is the growing utilization of upcycled plastics derived from post-industrial and post-consumer waste streams. These materials are increasingly used in flexible packaging formats such as pouches, wraps, and films. Companies are investing in advanced sorting and cleaning technologies to improve the quality and consistency of upcycled plastic resins. As a result, upcycled plastics are now being used in high-barrier applications, including food and pharmaceutical packaging. This trend is supported by corporate sustainability commitments, with over 55% of global packaging companies targeting recycled or upcycled content integration by 2030, thereby driving demand across multiple industries.

Market Drivers

Increasing Regulatory Pressure for Sustainable Packaging

Government regulations aimed at reducing environmental impact are a major driver for the upcycled materials in packaging market. Policies such as plastic bans, extended producer responsibility (EPR), and recycling mandates are pushing companies to adopt alternative materials. For instance, regulations requiring minimum 30% recycled or upcycled content in packaging by 2030 are influencing procurement strategies. These regulatory frameworks are not only driving demand but also encouraging innovation in material science. Companies are investing in research and development to create packaging solutions that comply with evolving standards while maintaining cost efficiency and performance.

Growing Consumer Preference for Eco-Friendly Products

Consumer awareness and demand for sustainable products are significantly influencing market growth. Studies show that nearly 68% of millennials are willing to pay a premium of 5–10% for sustainable packaging, which is encouraging brands to adopt upcycled materials. This shift in consumer behavior is particularly strong in sectors such as food & beverage, cosmetics, and personal care. Companies are leveraging this trend to enhance brand image and customer loyalty. Moreover, sustainability claims supported by visible packaging changes are proving effective in driving sales, further reinforcing the adoption of upcycled materials.

Market Restraint

Limited Supply Chain Standardization and Material Consistency

One of the key challenges in the upcycled materials in packaging market is the lack of standardized supply chains and variability in raw material quality. Upcycled materials often originate from diverse waste streams, which can lead to inconsistencies in composition, color, and mechanical properties. This variability makes it difficult for manufacturers to maintain uniform quality across large production volumes. Additionally, the absence of standardized certification systems for upcycled materials can create challenges in regulatory compliance and market acceptance. For example, food-grade packaging applications require strict safety and quality standards, which are difficult to achieve with inconsistent raw materials. These issues can increase production costs by up to 12–15%, limiting adoption among cost-sensitive industries and slowing overall market growth.

Market Opportunities

Expansion in E-commerce Packaging Solutions

The rapid growth of e-commerce is creating significant opportunities for upcycled materials in packaging. With global e-commerce shipments increasing by over 14% annually, there is a growing need for sustainable packaging solutions that can reduce environmental impact. Upcycled materials offer a viable alternative for protective packaging, mailers, and cushioning materials. Companies are developing lightweight yet durable packaging solutions using upcycled fibers and plastics, which can reduce shipping costs while enhancing sustainability credentials. This trend is expected to drive substantial demand, particularly in regions with strong online retail penetration.

Opportunity 2: Innovation in Bio-Composite and Hybrid Materials

Technological advancements in bio-composite materials are opening new avenues for market growth. These materials combine upcycled fibers with biodegradable polymers to create high-performance packaging solutions. Bio-composites offer improved strength, flexibility, and barrier properties, making them suitable for a wide range of applications, including food and pharmaceutical packaging. The development of such materials is attracting investments from both startups and established companies. With ongoing research, these materials are expected to achieve cost parity with traditional packaging by 2030, creating significant growth opportunities for the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.8 Billion |

| Market Size in 2026 | USD 7.6 Billion |

| Market Size in 2034 | USD 15.9 Billion |

| CAGR | 8.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible packaging dominated the market, accounting for 46.5% share in 2024, driven by its lightweight nature and cost efficiency. Upcycled materials such as recycled plastics and fibers are widely used in pouches, wraps, and films. These formats are preferred in industries such as food and beverage due to their convenience and ability to extend shelf life. The demand for flexible packaging is also supported by the growth of e-commerce and retail sectors, where lightweight packaging solutions help reduce transportation costs.

Rigid packaging is the fastest-growing segment, expected to register a CAGR of 7.9% during the forecast period. This growth is driven by increasing demand for durable and reusable packaging solutions. Upcycled materials such as molded fiber and bio-composites are being used in containers, bottles, and trays. The growing focus on sustainability in industries such as cosmetics and pharmaceuticals is further supporting the adoption of rigid packaging solutions.

By Material Type

Paper-based upcycled materials held the largest share of 49.2% in 2024, driven by their biodegradability and wide availability. These materials are commonly used in cartons, boxes, and wrapping paper. The increasing demand for sustainable packaging in the food and beverage industry is a key factor driving this segment. Additionally, advancements in paper processing technologies are improving the strength and durability of these materials.

Bio-composite materials are the fastest-growing segment, with a projected CAGR of 9.4%. These materials combine natural fibers with biodegradable polymers to create high-performance packaging solutions. The growing demand for eco-friendly packaging in premium product segments is driving the adoption of bio-composites. Their ability to offer improved barrier properties and structural strength makes them suitable for a wide range of applications.

By End-Use Industry

The food and beverage industry dominated the market with a 38.7% share in 2024, driven by the high demand for sustainable packaging solutions. Upcycled materials are increasingly used in packaging for snacks, beverages, and ready-to-eat meals. The need to reduce environmental impact while maintaining product quality is a key factor driving this segment.

The personal care and cosmetics industry is the fastest-growing segment, expected to register a CAGR of 8.7%. The increasing demand for sustainable and premium packaging solutions is driving the adoption of upcycled materials in this sector. Companies are focusing on innovative packaging designs that enhance brand image while reducing environmental impact.

Upcycled Materials In Packaging Market Segmentations

By Type

- Flexible Packaging

- Rigid Packaging

By Material Type

- Paper-Based Upcycled Materials

- Plastic-Based Upcycled Materials

- Bio-Composite Materials

By End-Use Industry

- Food & Beverage

- Personal Care & Cosmetics

- Pharmaceuticals

- E-commerce

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 28.6% of the market share in 2025, with a projected CAGR of 7.9% during the forecast period. The region benefits from strong regulatory frameworks and high consumer awareness regarding sustainability. The presence of established packaging manufacturers and advanced recycling infrastructure further supports market growth. Investments in material innovation and circular economy initiatives are also contributing to the expansion of upcycled packaging solutions across industries.

The United States dominates the regional market, driven by corporate sustainability commitments and technological advancements. A unique growth factor is the increasing adoption of upcycled packaging in premium product segments, particularly in cosmetics and specialty foods. Companies are leveraging upcycled materials to differentiate their products and meet consumer expectations for environmentally responsible packaging.

Europe

Europe held a 26.4% market share in 2025 and is expected to grow at a CAGR of 8.1%. The region’s stringent environmental regulations and strong focus on sustainability are key drivers. Policies promoting recycling and upcycling are encouraging manufacturers to adopt innovative materials. Additionally, government incentives for sustainable packaging are supporting market expansion.

Germany is the leading country in the region, supported by its advanced manufacturing capabilities and strong environmental policies. A unique growth factor is the integration of upcycled materials into industrial packaging applications, where companies are focusing on reducing carbon footprints and improving resource efficiency.

Asia Pacific

Asia Pacific dominated the market with a 34.8% share in 2025 and is projected to grow at a CAGR of 9.0%. Rapid industrialization, increasing population, and rising consumer awareness are driving demand for sustainable packaging solutions. The region is also witnessing significant investments in recycling and upcycling infrastructure.

China leads the regional market, driven by large-scale manufacturing and government initiatives promoting circular economy practices. A unique growth factor is the availability of abundant agricultural waste, which is being utilized to produce cost-effective upcycled packaging materials, supporting both environmental and economic objectives.

Middle East & Africa

The Middle East & Africa accounted for 5.2% of the market share in 2025, with a projected CAGR of 7.4%. The region is gradually adopting sustainable packaging practices, supported by government initiatives and increasing awareness. Investments in waste management infrastructure are also contributing to market growth.

The United Arab Emirates is a key market, driven by sustainability initiatives and growing demand for eco-friendly packaging. A unique growth factor is the adoption of upcycled materials in luxury packaging, particularly in the cosmetics and retail sectors, where sustainability is becoming an important value proposition.

Latin America

Latin America held a 5.0% market share in 2025 and is expected to grow at the fastest CAGR of 9.1%. The region is witnessing increasing adoption of sustainable packaging solutions, driven by regulatory developments and consumer awareness. The growth of the food and beverage industry is also contributing to demand.

Brazil dominates the regional market, supported by its large agricultural sector and availability of raw materials for upcycling. A unique growth factor is the use of agro-based waste in packaging production, which helps reduce costs and supports local economies while promoting sustainability.

Competitive Landscape

The upcycled materials in packaging market is moderately fragmented, with several global and regional players competing based on innovation, material quality, and sustainability initiatives. Key companies are focusing on expanding their product portfolios and investing in advanced material processing technologies. Strategic collaborations and partnerships are also common, enabling companies to enhance their market presence and access new customer segments.

One of the leading players in the market is a major global packaging company that has recently introduced a new line of bio-composite packaging solutions made from agricultural waste. This development reflects the industry’s focus on innovation and sustainability. Other companies are investing in recycling and upcycling infrastructure to improve material availability and reduce costs. Overall, competition is driven by the ability to deliver high-performance, cost-effective, and environmentally responsible packaging solutions.

Key Players List

- Amcor plc

- Mondi Group

- Smurfit Kappa Group

- DS Smith plc

- WestRock Company

- Stora Enso Oyj

- Tetra Pak International

- UPM-Kymmene Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- Berry Global Inc.

- Sealed Air Corporation

- International Paper Company

- Coveris Holdings S.A.

- Constantia Flexibles Group