Trays Packaging Market Size and Growth

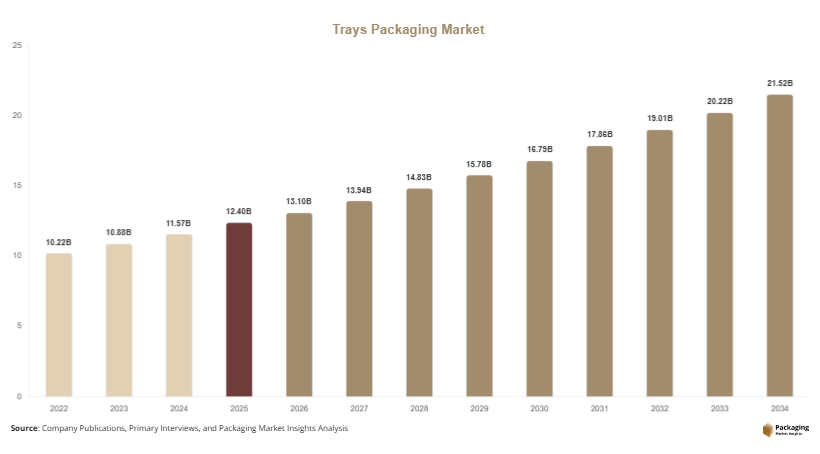

The global market size is estimated at USD 12.4 billion in 2025, and it is projected to reach USD 13.1 billion in 2026. By 2034, the market is expected to reach approximately USD 22.8 billion, registering a CAGR of 6.4% during 2025–2034. Growth is strongly influenced by the expansion of food delivery ecosystems and increasing demand for sustainable packaging alternatives. The trays packaging market is witnessing steady expansion driven by rising demand for convenient food packaging, increased adoption of ready-to-eat meals, and growing use of protective packaging in pharmaceuticals, electronics, and industrial goods. Trays offer structural rigidity, product visibility, and stacking efficiency, making them a preferred packaging format across multiple end-use industries.

One of the key growth factors is the rapid expansion of the foodservice and packaged food industry. Trays are widely used for frozen meals, bakery items, fresh produce, and ready-to-eat meals due to their ability to preserve product integrity and extend shelf life. Another important driver is the growth of e-commerce grocery delivery, which requires durable and tamper-resistant packaging solutions. Trays made from PET, PP, and molded fiber are increasingly used in logistics chains to reduce product damage during transit. A third factor supporting growth is sustainability regulations, which are pushing manufacturers to adopt recyclable and biodegradable tray materials such as paper-based molded fiber and compostable plastics.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Thermoformed plastic trays led the type segment with a 30.8% share.

- Plastic trays dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Fiber-Based Trays

The trays packaging industry is undergoing a significant transition toward sustainable materials, particularly molded fiber and paper-based trays. This shift is driven by increasing regulatory pressure to reduce plastic waste and rising consumer preference for eco-friendly packaging. Food chains in Europe and North America are replacing expanded polystyrene (EPS) trays with compostable alternatives for fresh food and takeaway meals. For example, quick-service restaurants are increasingly adopting sugarcane bagasse trays for hot meals due to their heat resistance and biodegradability. Packaging manufacturers are also investing in water-based coatings to enhance moisture resistance without compromising recyclability. Over the next decade, fiber-based trays are expected to gain significant market share as sustainability becomes a core procurement criterion for retailers and foodservice providers.

Adoption of High-Barrier and Smart Packaging Trays

Another emerging trend is the development of high-barrier and intelligent tray packaging solutions. High-barrier trays are designed to extend shelf life by preventing oxygen and moisture penetration, making them highly suitable for fresh meat, seafood, and ready meals. In parallel, smart packaging technologies such as QR-coded trays and freshness indicators are being integrated into packaging systems to enhance traceability and food safety. For instance, premium seafood exporters in Japan are using modified atmosphere packaging (MAP) trays to maintain freshness during long-distance exports. These innovations are expected to improve supply chain transparency and reduce food waste, driving further adoption of advanced tray packaging solutions.

Market Drivers

Growth of Ready-to-Eat and Convenience Foods

The increasing demand for ready-to-eat and convenience food products is a major driver of the trays packaging market. Urban lifestyles, busy work schedules, and growing dual-income households are fueling consumption of pre-packaged meals and frozen foods. Trays provide portion control, easy handling, and microwave compatibility, making them ideal for this segment. For example, supermarket chains in the United States and Europe heavily rely on thermoformed trays for packaged salads, meats, and microwaveable meals. The expansion of cloud kitchens and meal delivery services further accelerates tray consumption. As food manufacturers expand their product portfolios, demand for customized tray designs is expected to grow significantly.

Expansion of Cold Chain Logistics and E-Commerce Grocery

The rapid growth of cold chain logistics and online grocery delivery platforms is another major driver. Trays play a critical role in maintaining product integrity during transportation, especially for perishable goods such as dairy, meat, and seafood. E-commerce retailers require packaging that is durable, stackable, and resistant to temperature variations. For example, online grocery platforms in India and Southeast Asia are increasingly adopting sealed plastic and fiber trays for fresh produce delivery. The expansion of refrigerated logistics infrastructure in emerging markets is further supporting tray adoption. This trend is expected to continue as digital grocery penetration increases globally.

Market Restraint

Environmental Concerns and Plastic Waste Regulations

A key restraint in the trays packaging market is the increasing regulatory pressure against single-use plastics. Governments across Europe, North America, and parts of Asia are implementing strict policies to reduce plastic consumption, which directly impacts plastic tray manufacturers. While alternatives such as molded fiber and biodegradable plastics are emerging, they are often more expensive and have performance limitations in moisture resistance and durability. For example, food service providers in the European Union face restrictions on EPS foam trays, requiring them to transition to costlier sustainable alternatives. This transition increases operational costs for manufacturers and end-users, slowing adoption in price-sensitive markets. Additionally, recycling infrastructure limitations in developing economies further restrict the efficient disposal of tray packaging waste.

Market Opportunities

Growth in Sustainable Packaging Innovations

The increasing global focus on sustainability presents significant opportunities for eco-friendly tray packaging solutions. Manufacturers are developing biodegradable, compostable, and recyclable trays made from materials such as bagasse, cornstarch, and recycled paper fibers. These innovations are gaining traction in foodservice and retail sectors where environmental compliance is critical. For instance, quick-service restaurants in Europe are adopting fiber-based trays to meet regulatory requirements. As sustainability goals become more stringent, demand for innovative tray materials is expected to rise, creating opportunities for packaging manufacturers to differentiate their offerings.

Expansion in Healthcare and Pharmaceutical Packaging

The healthcare sector presents strong growth potential for tray packaging, particularly for sterile medical device packaging and pharmaceutical blister trays. Trays provide contamination protection and structured organization for surgical instruments and diagnostic kits. Hospitals and medical suppliers are increasingly adopting customized thermoformed trays for efficient storage and transport. For example, medical device manufacturers in Germany and the United States use high-precision trays for orthopedic implants. With rising healthcare expenditure and medical device production, this segment is expected to create long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.4 Billion |

| Market Size in 2026 | USD 13.1 Billion |

| Market Size in 2034 | USD 22.8 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoformed plastic trays dominated the market in 2024 with a 30.8% share due to their cost efficiency, durability, and versatility. These trays are widely used in food packaging for fresh meat, bakery products, and ready meals. Their ability to be produced in high volumes using automated thermoforming lines makes them highly suitable for large-scale food manufacturers. Supermarkets in the United States and Europe rely heavily on thermoformed trays for product visibility and shelf-life extension. Their compatibility with modified atmosphere packaging further enhances their dominance in perishable food segments.

Molded fiber trays are the fastest-growing subsegment with a CAGR of 7.1%. Growth is driven by increasing sustainability regulations and consumer preference for plastic-free packaging. These trays are widely used in foodservice and takeaway applications. Companies in Europe and Asia are investing in advanced fiber molding technologies to improve moisture resistance and durability, expanding their applicability in hot food packaging.

By Material

Plastic trays dominated in 2024 with a 52.3% share, driven by their affordability, strength, and wide applicability across industries. PET and PP-based trays are widely used in food packaging due to their clarity and recyclability. Industrial sectors also use plastic trays for component protection during transport.

Paper-based trays are the fastest-growing subsegment with a CAGR of 6.5%, supported by environmental regulations and sustainability initiatives. Foodservice companies are increasingly shifting to molded paper trays to reduce carbon footprint. Innovations in coating technologies are improving their resistance to grease and moisture.

By End-Use

Food & beverage applications dominated in 2024 with a 43.1% share, driven by high demand for packaged meals, fresh produce, and frozen foods. Retail chains and quick-service restaurants rely heavily on tray packaging for portion control and shelf appeal.

Healthcare packaging is the fastest-growing segment with a CAGR of 6.3%, driven by increasing demand for sterile medical packaging. Trays are widely used for surgical kits, diagnostic instruments, and pharmaceutical blister packs. Hospitals and medical suppliers are adopting customized trays for improved hygiene and efficiency.

Trays Packaging Market Segmentations

By Type

- Thermoformed Trays

- Molded Fiber Trays

- Foam Trays

- Plastic Clamshell Trays

By Material

- Plastic

- Paper & Paperboard

- Biodegradable Materials

- Foam

By End-Use

- Food & Beverage

- Healthcare

- Electronics

- Industrial

Regional Analysis

North America

North America accounted for approximately 28.6% of the trays packaging market in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. The region benefits from a strong packaged food industry, advanced retail infrastructure, and high consumption of ready-to-eat meals. Demand for microwaveable and portion-controlled packaging is particularly strong in urban centers. Sustainability regulations are also influencing material choices, pushing manufacturers toward recyclable and compostable tray formats.

The United States dominates the regional market due to its large food processing and retail ecosystem. A unique growth driver is the expansion of meal kit delivery services, which rely heavily on thermoformed trays for ingredient separation and freshness preservation. Companies such as subscription-based meal providers use customized tray packaging to enhance consumer convenience and product presentation.

Europe

Europe held a market share of 25.1% in 2025 and is expected to grow at a CAGR of 5.6%. The region is heavily influenced by strict environmental regulations targeting plastic waste reduction. This has led to rapid adoption of fiber-based and biodegradable trays across foodservice and retail sectors. Demand is also supported by strong frozen food consumption and supermarket penetration.

Germany leads the European market due to its advanced packaging engineering capabilities. A key growth factor is the widespread adoption of circular economy packaging models, where trays are designed for recyclability and reuse. Supermarket chains in Germany are increasingly shifting to paper-based trays for fresh meat and bakery products.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is expected to grow at a CAGR of 7.0%. Rapid urbanization, rising disposable income, and expansion of packaged food consumption are driving growth. The region also benefits from strong manufacturing capabilities and cost-efficient production of plastic and fiber trays.

China remains the dominant country due to its massive food processing industry. A unique growth driver is the expansion of online food delivery platforms, which require durable and heat-resistant trays for meal transport. Similarly, Japan and South Korea are adopting high-quality MAP trays for premium food exports.

Middle East & Africa

The Middle East & Africa accounted for 4.8% of the market in 2025 and is projected to grow at a CAGR of 6.1%. Growth is driven by expanding food retail chains, rising tourism, and increasing demand for packaged foods in urban centers. Investments in cold chain logistics are also improving distribution efficiency.

The UAE dominates the regional market due to its strong hospitality and tourism sector. A key growth factor is the demand for premium food packaging in airlines and luxury catering services, which rely heavily on high-quality thermoformed trays.

Latin America

Latin America held a 4.1% market share in 2025 and is expected to grow at the fastest CAGR of 6.2%. Growth is supported by expanding food retail infrastructure and increasing consumption of packaged and frozen foods. Brazil and Mexico are the major contributors.

Brazil dominates the region due to its large agrifood industry. A key growth driver is the expansion of export-oriented meat packaging, where trays are used for hygienic storage and international shipping compliance.

Competitive Landscape

The trays packaging market is moderately fragmented, with global and regional players competing on innovation, material development, and sustainability initiatives. Key companies include Amcor plc, Berry Global Inc., Sealed Air Corporation, Huhtamaki Group, and Sonoco Products Company. Among these, Amcor plc holds a leading position due to its extensive product portfolio in flexible and rigid tray packaging solutions and strong global distribution network.

Companies are focusing on sustainable product development, lightweight materials, and automation in tray manufacturing. Strategic partnerships with food retailers and investments in recycling technologies are common approaches. For example, Berry Global has expanded its molded fiber tray production capacity to meet rising demand from foodservice customers.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Huhtamaki Group

- Sonoco Products Company

- DS Smith Plc

- Mondi Group

- Smurfit Kappa Group

- Coveris Holdings

- Pactiv Evergreen Inc.

- Faerch Group

- Winpak Ltd.

- Tekni-Plex Inc.

- Constantia Flexibles

- ProAmpac LLC