Transit Packaging Market Size and Growth

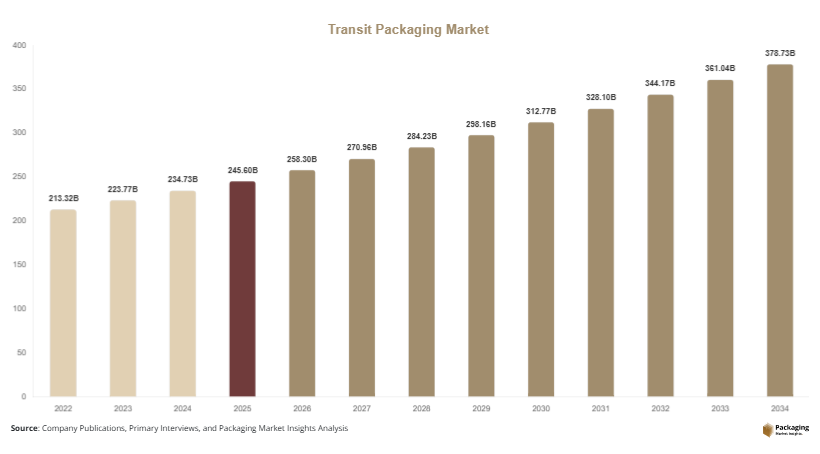

In 2025, the global transit packaging market is valued at USD 245.6 billion, growing to USD 258.3 billion in 2026, and is projected to reach approximately USD 398.7 billion by 2034, reflecting a CAGR of 4.9% between 2025 and 2034. The transit packaging market is experiencing consistent expansion as global trade volumes, industrial output, and e-commerce logistics continue to rise. Transit packaging includes protective and handling solutions such as pallets, crates, corrugated boxes, drums, and cushioning materials that ensure product safety during storage and transportation.

The growth of this market is closely linked to the expansion of global supply chains and the increasing complexity of logistics operations. Industries such as food & beverage, pharmaceuticals, automotive, and consumer electronics rely heavily on transit packaging to maintain product integrity during long-distance shipping. The surge in cross-border trade and industrial exports has significantly increased the need for durable and cost-efficient packaging solutions that can withstand varying environmental conditions.

Key Highlights

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 5.8%

- Pallets led the type segment with a 31.4% share, while protective packaging is expected to grow at a CAGR of 5.6%

- Plastic packaging dominated with a 49.7% share, while paper & paperboard is forecasted to grow at a CAGR of 5.5%

- Food & beverage applications led with 41.3% share, while pharmaceuticals are expected to grow at a CAGR of 6.1%

- China remained the dominant country with a market size of USD 12.6 billion in 2025 and USD 13.3 billion in 2026

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Shift Toward Sustainable Transit Packaging Solutions

Sustainability has become a central theme shaping the evolution of the transit packaging market. Companies are actively transitioning from traditional plastic-based solutions to environmentally responsible alternatives such as corrugated board, molded pulp, and biodegradable polymers. This shift is influenced by stricter environmental regulations and growing pressure from consumers and stakeholders to reduce carbon footprints. Many logistics providers are replacing single-use plastic wraps with recyclable films and reusable pallet covers to minimize waste generation.

In addition, the adoption of circular economy practices is accelerating the use of returnable packaging systems such as reusable crates and pallets. These systems not only reduce environmental impact but also provide long-term cost savings for businesses. For example, automotive manufacturers are increasingly using reusable transit packaging for component transportation within closed-loop supply chains. Over time, this transition is expected to reshape product design and material selection, with manufacturers investing in lightweight yet durable solutions. The long-term impact will be a more sustainable and resource-efficient transit packaging ecosystem.

Growing Integration of Smart Packaging Technologies

The integration of smart technologies into transit packaging is transforming how goods are monitored and managed during transportation. Packaging solutions embedded with IoT-enabled sensors, RFID tags, and GPS tracking systems are enabling real-time monitoring of critical parameters such as temperature, humidity, and location. This is particularly important for industries like pharmaceuticals and food, where product quality is highly sensitive to environmental conditions.

For instance, cold chain logistics providers are adopting smart packaging to ensure temperature-controlled delivery of vaccines and biologics. This not only enhances product safety but also improves regulatory compliance and reduces spoilage risks. The declining cost of sensor technologies is making smart packaging more accessible across various industries. In the coming years, the widespread adoption of connected packaging solutions is expected to improve supply chain transparency, reduce operational inefficiencies, and enable better decision-making through real-time data insights.

Market Drivers

Expansion of E-commerce and High-Volume Logistics Networks

The rapid expansion of e-commerce platforms has significantly increased the demand for transit packaging solutions across the globe. Online retail requires packaging that can endure multiple handling stages, from warehouse sorting to last-mile delivery. This has led to a surge in demand for corrugated boxes, protective cushioning materials, and flexible packaging formats that ensure product safety while maintaining cost efficiency.

As order volumes increase, companies are adopting multi-layer packaging strategies to minimize damage rates and returns. For example, electronics and fragile goods are often shipped using reinforced packaging structures that combine corrugated materials with protective inserts. The direct impact of rising e-commerce penetration is a proportional increase in packaging consumption. Furthermore, logistics providers are optimizing packaging designs to reduce dimensional weight and transportation costs. This ongoing shift is expected to sustain strong demand for innovative transit packaging solutions in the long term.

Increasing Global Trade and Complex Supply Chain Structures

The globalization of trade has resulted in more complex supply chain networks, increasing the need for reliable transit packaging solutions. Goods are often transported across multiple regions and handled through different modes of transportation, including road, rail, sea, and air. This complexity requires packaging solutions that offer durability, standardization, and compatibility with various handling systems.

Industries such as automotive and electronics depend on specialized transit packaging to protect high-value components during international shipping. For instance, precision-engineered parts are transported using custom-designed crates and pallets that prevent damage during transit. The continuous expansion of international trade agreements and manufacturing outsourcing further amplifies this demand. As companies seek to improve supply chain efficiency and reduce product losses, the importance of advanced transit packaging solutions will continue to grow.

Market Restraint

Impact of Raw Material Price Volatility and Regulatory Pressures

Fluctuations in the prices of raw materials such as plastic resins, paper pulp, and wood present a significant challenge for the transit packaging market. These materials form the backbone of packaging production, and any variation in their costs directly affects manufacturing expenses and pricing strategies. For example, an increase in crude oil prices leads to higher costs for plastic-based packaging, which can reduce profit margins for manufacturers.

At the same time, stringent environmental regulations are restricting the use of certain materials, particularly single-use plastics. Compliance with these regulations requires companies to invest in alternative materials and sustainable production processes, which can increase operational costs. Smaller manufacturers often face difficulties in adapting to these changes due to limited financial resources. The combined effect of cost volatility and regulatory pressure can slow down innovation and limit the adoption of new packaging technologies, posing a restraint to overall market growth.

Market Opportunities

Rising Demand Across Emerging Economies

Emerging economies are becoming key growth centers for the transit packaging market due to rapid industrialization and expanding consumer markets. Countries in Asia, Latin America, and Africa are witnessing significant growth in retail, manufacturing, and logistics sectors. This expansion is creating strong demand for efficient and standardized packaging solutions that support large-scale distribution networks.

For instance, the growth of organized retail and online shopping in developing markets is increasing the need for cost-effective and durable transit packaging. Additionally, improvements in infrastructure and transportation networks are facilitating smoother logistics operations, further boosting demand. Companies entering these markets can benefit from lower production costs and increasing domestic consumption. Over the forecast period, emerging economies are expected to play a critical role in driving global market expansion.

Advancements in Reusable and Returnable Packaging Systems

The development of reusable and returnable transit packaging systems presents a significant opportunity for market participants. These solutions are gaining traction in industries with closed-loop supply chains, such as automotive, retail, and manufacturing. Reusable pallets, crates, and containers are designed for multiple usage cycles, reducing waste and offering long-term cost benefits.

For example, large retailers are adopting returnable packaging systems for transporting goods between distribution centers and stores. This approach minimizes packaging waste and improves supply chain efficiency. Additionally, advancements in material science are enabling the development of durable and lightweight reusable packaging solutions. As sustainability becomes a priority for businesses, the adoption of returnable systems is expected to increase, creating new growth avenues for manufacturers and solution providers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 245.6 Billion |

| Market Size in 2026 | USD 258.3 Billion |

| Market Size in 2034 | USD 398.7 Billion |

| CAGR | 4.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pallets represent the dominant subsegment within the type category, accounting for approximately 31.4% of the market share in 2024. Their widespread adoption is attributed to their ability to provide structural stability and facilitate efficient material handling across industries. Pallets are essential in logistics operations as they enable easy movement of goods using forklifts and automated systems. Industries such as food & beverage, automotive, and industrial manufacturing rely heavily on pallets for bulk transportation. Wooden pallets are commonly used for heavy-duty applications, while plastic pallets are preferred in sectors requiring hygiene and durability. The reusability and cost efficiency of pallets further strengthen their dominance in the market.

Protective packaging is emerging as the fastest-growing subsegment, projected to register a CAGR of 5.6% during the forecast period. This growth is driven by the increasing demand for cushioning materials such as foam, bubble wrap, and air pillows, which protect fragile items during transit. The rise of e-commerce has significantly amplified the need for protective packaging, as products undergo multiple handling stages before reaching consumers. Innovations in biodegradable and recyclable cushioning materials are also supporting growth in this segment. As companies focus on reducing product damage and returns, the demand for advanced protective packaging solutions is expected to increase.

By Material

Plastic remains the dominant material segment, accounting for 49.7% of the market share in 2024. Its durability, flexibility, and cost-effectiveness make it a preferred choice for various transit packaging applications. Plastic-based solutions such as crates, pallets, and containers are widely used due to their resistance to moisture and contamination. This makes them particularly suitable for industries such as pharmaceuticals and food, where hygiene is critical. Additionally, the lightweight nature of plastic helps reduce transportation costs, further supporting its widespread adoption.

Paper and paperboard are emerging as the fastest-growing materials, with a projected CAGR of 5.5%. This growth is driven by increasing environmental concerns and regulatory restrictions on plastic usage. Corrugated boxes and paper-based packaging solutions are gaining popularity due to their recyclability and biodegradability. Companies are investing in advanced paper-based materials with enhanced strength and durability to replace traditional plastic packaging. The shift toward sustainable packaging solutions is expected to continue, positioning paper and paperboard as key growth drivers in the transit packaging market.

By End-Use

The food and beverage sector dominates the end-use segment, accounting for 41.3% of the market share in 2024. The high demand for packaged food products and beverages requires reliable transit packaging solutions that ensure product safety and quality. Corrugated boxes, plastic crates, and insulated packaging are widely used for transporting perishable goods. The growth of online food delivery services has further increased the demand for efficient transit packaging solutions. Additionally, strict food safety regulations necessitate the use of packaging that maintains product integrity during transportation.

The pharmaceutical sector is the fastest-growing end-use segment, expected to expand at a CAGR of 6.1%. This growth is driven by the increasing demand for temperature-sensitive packaging solutions used in transporting vaccines, biologics, and other medical products. Cold chain logistics relies heavily on insulated containers and specialized packaging to maintain product efficacy. The expansion of healthcare infrastructure and rising demand for medical products are contributing to the growth of this segment. As the pharmaceutical industry continues to evolve, the need for advanced transit packaging solutions is expected to increase significantly.

Transit Packaging Market Segmentations

By Type

- Pallets

- Crates

- Intermediate Bulk Containers

- Protective Packaging

By Material

- Plastic

- Paper & Paperboard

- Wood

- Metal

By End-User

- Food & Beverage

- Pharmaceuticals

- Automotive

- Consumer Electronics

- Industrial Goods

Regional Analysis

North America

North America accounted for approximately 24.6% of the global transit packaging market share in 2025 and is projected to grow at a CAGR of 4.3% through 2034. The region benefits from a mature logistics infrastructure, high adoption of advanced warehousing systems, and strong demand from sectors such as retail, pharmaceuticals, and manufacturing. The widespread use of automated distribution centers is driving the demand for standardized packaging formats that can seamlessly integrate with conveyor systems and robotic handling equipment. Additionally, the increasing focus on reducing packaging waste is encouraging companies to adopt recyclable and reusable materials, contributing to steady market growth.

The United States remains the dominant contributor to the regional market, supported by its extensive e-commerce ecosystem and high consumer spending levels. A distinct growth driver in this region is the increasing use of automation and robotics in supply chain operations. For instance, fulfillment centers are adopting packaging solutions designed for automated sorting and handling, which enhances operational efficiency and reduces labor dependency. The demand for lightweight and durable packaging formats is also rising as companies aim to optimize shipping costs and improve delivery speed. This trend is expected to sustain long-term growth in the region.

Europe

Europe held a 22.1% market share in 2025 and is expected to expand at a CAGR of 4.1% during the forecast period. The region is characterized by stringent environmental regulations and a strong emphasis on sustainability. Governments and regulatory bodies are promoting the use of recyclable and biodegradable materials, encouraging manufacturers to innovate in eco-friendly transit packaging solutions. The presence of well-established manufacturing industries and extensive cross-border trade networks further supports market growth. Additionally, the increasing adoption of reusable packaging systems is contributing to the expansion of the regional market.

Germany leads the European market due to its robust industrial base and export-oriented economy. A key growth driver in the region is the implementation of circular economy initiatives that encourage resource efficiency and waste reduction. For example, companies are increasingly adopting returnable packaging systems to comply with environmental standards and reduce operational costs. The automotive and industrial sectors are major users of such systems, as they rely on efficient and durable packaging for component transportation. This trend is expected to drive continued innovation and growth in the European transit packaging market.

Asia Pacific

Asia Pacific dominated the global market with a 38.2% share in 2025 and is projected to grow at a CAGR of 5.3% through 2034. The region’s growth is driven by rapid industrialization, expanding manufacturing activities, and the rise of e-commerce platforms. Countries such as China, India, and Japan are major contributors, supported by large consumer bases and increasing demand for packaged goods. The expansion of retail networks and improvements in logistics infrastructure are further boosting the need for transit packaging solutions across the region.

China remains the dominant country, supported by its strong manufacturing sector and high export volumes. A unique growth driver is the rapid expansion of e-commerce, which requires efficient packaging solutions for high-volume shipments. Logistics providers are investing in advanced packaging technologies to manage increasing order volumes and reduce damage rates. Additionally, government initiatives aimed at improving industrial output and infrastructure are supporting market expansion. The combination of these factors is expected to maintain Asia Pacific’s leading position in the global transit packaging market.

Middle East & Africa

The Middle East & Africa region accounted for 7.8% of the global market share in 2025 and is projected to grow at a CAGR of 4.7% over the forecast period. Growth in this region is supported by increasing trade activities, infrastructure development, and expanding retail sectors. Countries such as the United Arab Emirates and South Africa are investing heavily in logistics and transportation networks, which is driving demand for efficient transit packaging solutions. The rising consumption of packaged goods and the development of modern retail formats are further contributing to market growth.

The United Arab Emirates stands out as a key market due to its strategic position as a global trade hub. A distinctive growth driver is the expansion of free trade zones and logistics hubs that facilitate international trade. Businesses operating in these zones require reliable packaging solutions to handle large volumes of goods efficiently. Additionally, the increasing focus on diversifying economies away from oil dependency is leading to growth in manufacturing and industrial sectors, which further boosts demand for transit packaging. This trend is expected to create new opportunities in the region.

Latin America

Latin America held a 7.3% share of the global transit packaging market in 2025 and is expected to grow at a CAGR of 5.8%, making it one of the fastest-growing regions. The growth is driven by expanding retail and e-commerce sectors, along with improvements in logistics infrastructure. Countries such as Brazil and Mexico are witnessing increased demand for packaged goods, which is driving the need for efficient transit packaging solutions. Additionally, the growing focus on sustainability is encouraging the adoption of eco-friendly materials.

Brazil dominates the regional market due to its large population and growing industrial base. A unique growth driver is the increasing penetration of e-commerce platforms, which require cost-effective and durable packaging solutions for product delivery. Companies are adopting lightweight packaging formats to reduce transportation costs and improve efficiency. Furthermore, government initiatives aimed at improving trade and logistics infrastructure are supporting market growth. This combination of factors is expected to drive significant expansion in the Latin American transit packaging market over the forecast period.

Competitive Landscape

The transit packaging market is moderately fragmented, with a mix of global and regional players competing on innovation, cost efficiency, and sustainability. Companies are focusing on expanding their product portfolios to cater to diverse industry requirements while also aligning with environmental regulations. Strategic initiatives such as mergers, acquisitions, and partnerships are commonly adopted to strengthen market presence and enhance technological capabilities.

International Paper Company is recognized as a leading player due to its strong portfolio in corrugated packaging and its commitment to sustainable practices. The company has invested significantly in recycling infrastructure and eco-friendly packaging solutions. Other major players are also emphasizing innovation in reusable and returnable packaging systems to meet growing demand for sustainable logistics solutions.

Additionally, companies are leveraging advanced manufacturing technologies to improve efficiency and reduce production costs. Expansion into emerging markets is another key strategy, as these regions offer significant growth potential due to increasing industrialization and retail expansion. The competitive landscape is expected to remain dynamic, with continuous advancements in materials and packaging technologies shaping the future of the market.

Key Players

- International Paper Company

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- WestRock Company

- Sonoco Products Company

- Sealed Air Corporation

- Amcor Plc

- Nefab Group

- Greif Inc.

- Schoeller Allibert

- Orbis Corporation

- Menasha Corporation

- Packaging Corporation of America

- UFP Technologies Inc.