Tinplate Packaging Market Size and Growth

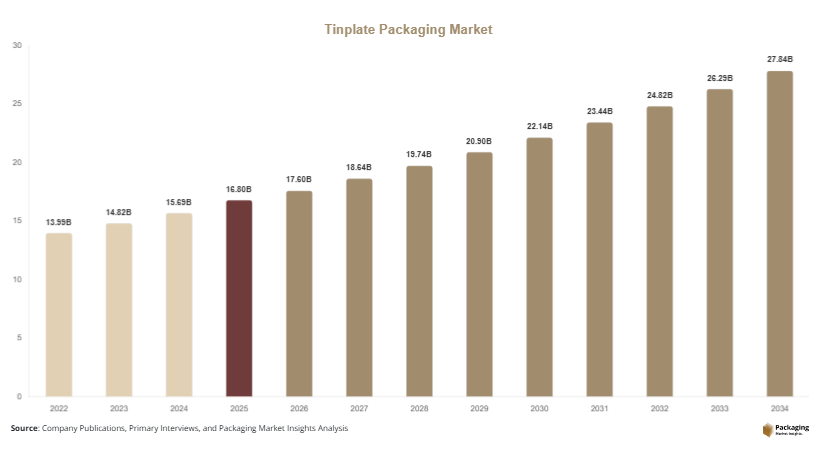

The global tinplate packaging market size is estimated at USD 16.8 billion in 2025, which is projected to reach USD 17.6 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow to USD 29.4 billion in 2034, registering a CAGR of 5.9%. The tinplate packaging market is witnessing consistent expansion due to its strong presence in food preservation, beverage packaging, and industrial storage applications. Tinplate, a thin steel sheet coated with tin, offers excellent corrosion resistance, durability, and recyclability, making it suitable for packaging products that require long shelf life and high protection standards.

One of the primary growth factors driving the market is the increasing demand for canned food and beverages, especially in urban areas where convenience and shelf stability are critical. Another factor is the rising focus on sustainable packaging, as tinplate is fully recyclable and supports circular economy goals. Additionally, the growth of the chemical and industrial sectors is fueling demand for robust packaging solutions that ensure safe transportation and storage.

Key Market Insights:

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5%.

- Food cans led the type segment with a 42.8% share.

- Steel-based tinplate dominated with a 64.7% share.

- Food & beverage applications led the segment with 55.2% share.

- The US remained the dominant country with a market size of USD 3.6 billion in 2025 and USD 3.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of sustainable and recyclable metal packaging

Sustainability is playing a significant role in shaping the tinplate packaging market. Governments and regulatory bodies are encouraging the use of recyclable materials to reduce environmental impact. Tinplate packaging aligns well with these goals, as it can be recycled multiple times without losing its properties. For example, food manufacturers are increasingly shifting from plastic containers to metal cans to meet sustainability targets. This trend is also evident in beverage packaging, where brands are promoting metal packaging as an eco-friendly alternative.

In the future, this trend is expected to drive innovation in recycling technologies and material optimization. Companies are investing in closed-loop recycling systems to improve efficiency and reduce waste. The demand for eco-friendly packaging solutions will continue to grow, supporting long-term market expansion.

Growing demand for convenience food and long shelf-life packaging

The demand for convenience food is increasing globally due to changing lifestyles and urbanization. Tinplate packaging plays a key role in preserving food products and extending shelf life. Ready-to-eat meals, canned vegetables, and processed meat products rely heavily on tinplate packaging for safety and durability. For instance, food processing companies are expanding their canned product lines to cater to busy consumers.

This trend is expected to continue as consumers seek convenient and reliable food options. Advances in packaging technology will further enhance product quality and shelf life. The growing popularity of online grocery platforms is also contributing to demand, as durable packaging is essential for safe transportation.

Market Drivers

Expansion of the global food processing industry

The rapid growth of the food processing industry is a major driver for the tinplate packaging market. Processed food products require packaging that ensures safety, hygiene, and extended shelf life. Tinplate packaging meets these requirements effectively. For example, canned food products such as soups, fruits, and ready meals rely on tinplate containers to maintain freshness and prevent contamination.

As the demand for processed food increases, particularly in emerging markets, the need for reliable packaging solutions is also rising. Governments are supporting food processing industries through investments and policy initiatives, which further boosts demand for tinplate packaging. This trend is expected to continue, supporting steady market growth.

Rising demand for durable industrial and chemical packaging

Tinplate packaging is widely used in industrial and chemical sectors due to its strength and resistance to corrosion. Products such as paints, lubricants, and chemicals require packaging that can withstand harsh conditions. Tinplate containers provide a reliable solution for these applications. For instance, chemical manufacturers use tinplate drums and cans to ensure safe storage and transportation.

The growth of industrial activities and infrastructure development is driving demand for such packaging solutions. As industries expand, the need for durable and safe packaging increases. This is expected to contribute significantly to market growth over the forecast period.

Market Restraint

Fluctuating raw material prices and production costs

One of the key challenges in the tinplate packaging market is the volatility in raw material prices, particularly steel and tin. These fluctuations can significantly impact production costs and profit margins. For example, an increase in steel prices can lead to higher manufacturing expenses, making tinplate packaging less competitive compared to alternative materials such as plastics or paper-based packaging.

Additionally, energy costs and labor expenses contribute to overall production costs. Manufacturers often face challenges in maintaining price stability while ensuring product quality. Small and medium-sized enterprises are particularly affected, as they have limited capacity to absorb cost fluctuations. This restraint may slow market growth, especially in price-sensitive regions.

Market Opportunities

Increasing adoption of lightweight and innovative packaging designs

Innovation in packaging design is creating new opportunities in the tinplate packaging market. Manufacturers are focusing on developing lightweight tinplate containers that reduce material usage without compromising strength. This approach helps lower production costs and improves sustainability. For example, beverage companies are adopting thinner tinplate cans to reduce weight and transportation costs.

Future developments in material science and manufacturing processes are expected to enhance design capabilities. Lightweight packaging solutions will become more common, supporting market growth and improving efficiency across supply chains.

Expansion of emerging markets and urban consumption patterns

Emerging markets present significant growth opportunities for the tinplate packaging industry. Rising disposable incomes and changing consumer preferences are driving demand for packaged food and beverages. Countries in Asia Pacific, Latin America, and Africa are experiencing rapid urbanization, which is increasing consumption of convenience products.

For instance, the growth of retail chains and supermarkets in these regions is boosting demand for packaged goods. This creates opportunities for tinplate packaging manufacturers to expand their presence. In the future, improved infrastructure and distribution networks will further support market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.8 Billion |

| Market Size in 2026 | USD 17.6 Billion |

| Market Size in 2034 | USD 29.4 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Food cans dominated the market in 2024 with a 42.8% share, driven by their widespread use in preserving food products. These cans are essential for packaging items such as fruits, vegetables, and ready meals. Their ability to extend shelf life and maintain product quality makes them highly preferred. For example, food companies rely on tinplate cans to ensure safety and durability during storage and transportation.

Aerosol cans are the fastest-growing segment, with a projected CAGR of 6.3%. These cans are widely used in personal care and household products. The growth is driven by increasing demand for convenience and ease of use. Future innovations in valve systems and coatings are expected to enhance performance and expand applications.

By Material

Steel-based tinplate dominated the market with a 64.7% share in 2024 due to its strength and durability. It is widely used in packaging applications that require high resistance to pressure and corrosion. For instance, industrial products such as paints and chemicals rely on steel-based containers.

Coated specialty tinplate is the fastest-growing segment, with a CAGR of 6.1%. This growth is driven by the need for improved corrosion resistance and product compatibility. Industries are adopting advanced coatings to enhance packaging performance. Future developments in coating technologies are expected to drive growth.

By End-Use

Food & beverage applications accounted for the largest share of 55.2% in 2024, driven by the need for safe and durable packaging. Tinplate packaging is widely used in this sector due to its ability to preserve food quality. For example, beverage companies use metal cans for packaging drinks.

Chemical packaging is the fastest-growing segment, with a CAGR of 6.0%. The demand for safe and reliable packaging solutions is driving growth. Tinplate containers provide protection against leakage and contamination. As industrial activities expand, this segment is expected to grow further.

Tinplate Packaging Market Segmentations

By Product Type

- Food Cans

- Aerosol Cans

- Paint Cans

- Industrial Containers

By Material

- Steel-Based Tinplate

- Coated Specialty Tinplate

- Recycled Tinplate

By End-User

- Food & Beverage

- Chemicals

- Personal Care

- Industrial Goods

Regional Analysis

North America

North America accounted for approximately 24.3% of the global market share in 2025 and is projected to grow at a CAGR of 5.4% through 2034. The region benefits from strong demand for packaged food and beverages, supported by advanced retail infrastructure and high consumer spending. The increasing focus on sustainable packaging is also driving the adoption of tinplate solutions. Manufacturers in the region are investing in recyclable materials and efficient production processes to meet regulatory requirements.

The United States dominates the regional market due to its large food processing industry. A key growth driver is the demand for ready-to-eat meals and canned food products. For example, food companies are expanding their canned product lines to cater to busy lifestyles. This trend is expected to support steady market growth.

Europe

Europe held a 22.1% market share in 2025 and is expected to grow at a CAGR of 5.2% during the forecast period. The region is characterized by strict environmental regulations and a strong emphasis on sustainable packaging. Tinplate packaging is widely used due to its recyclability and compliance with environmental standards.

Germany is the dominant country in the region, driven by its advanced manufacturing sector. A unique growth driver is the adoption of eco-friendly packaging solutions in the food industry. For instance, companies are replacing plastic containers with metal cans. This shift is expected to support market growth.

Asia Pacific

Asia Pacific emerged as the largest regional market with a 39.1% share in 2025 and is projected to grow at a CAGR of 6.3%. Rapid urbanization, population growth, and rising disposable income are driving demand for packaged goods. The expansion of the food processing industry is also contributing to market growth.

China dominates the region due to its large manufacturing base. A significant growth driver is the increasing demand for canned food products. For example, local companies are expanding production to meet growing consumer demand. Government support for industrial development is further boosting the market.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the market share in 2025 and is expected to grow at a CAGR of 5.7%. Growth is driven by increasing investments in food processing and retail sectors. The demand for durable packaging solutions is rising due to expanding industrial activities.

The UAE is a key market, supported by its strong retail sector. A unique growth driver is the demand for packaged food among expatriate populations. For example, supermarkets are increasing their canned food offerings. This trend is expected to support market growth.

Latin America

Latin America held a 7.7% market share in 2025 and is projected to grow at the fastest CAGR of 6.5%. The region is experiencing growth due to rising consumption of packaged food and beverages. Expanding retail networks are also contributing to demand.

Brazil dominates the regional market, supported by its large consumer base. A key growth driver is the growth of the food processing industry. For instance, companies are investing in canned food production. This is expected to drive demand for tinplate packaging.

Competitive Landscape

The tinplate packaging market is moderately competitive, with several global and regional players focusing on innovation and sustainability. Companies are investing in advanced manufacturing technologies and expanding their product portfolios to meet evolving demand.

ArcelorMittal is identified as a market leader due to its strong presence in steel production and packaging solutions. The company focuses on developing high-quality tinplate products and improving production efficiency. Other companies are adopting strategies such as partnerships and product launches to strengthen their market position.

Recent developments include advancements in coating technologies, lightweight packaging designs, and increased focus on recyclable materials. Automation and digitalization are also improving production efficiency and reducing costs.

Key Players

- ArcelorMittal

- Tata Steel

- Nippon Steel Corporation

- JFE Steel Corporation

- POSCO

- Thyssenkrupp AG

- U.S. Steel Corporation

- Baosteel Group

- Nucor Corporation

- Crown Holdings

- Ball Corporation

- Silgan Holdings

- Can-Pack S.A.

- Kian Joo Can Factory Berhad

- Huber Packaging Group