Through Silicon Via (TSV) IC Packaging Market Size and Growth

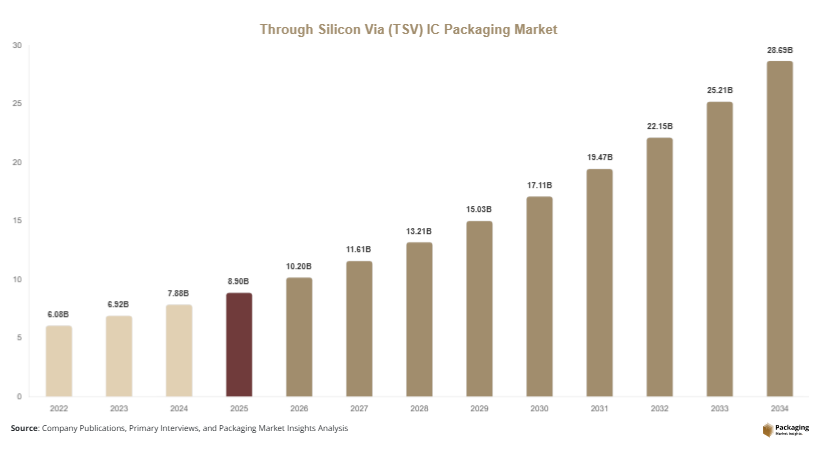

The global Through Silicon Via (TSV) IC Packaging Market size was valued at approximately USD 8.9 billion in 2025 and is projected to reach USD 10.2 billion in 2026. With increasing adoption across consumer electronics, automotive, and data center applications, the market is forecasted to reach USD 28.6 billion by 2034, registering a CAGR of 13.8% during the forecast period (2025–2034). The through silicon via (TSV) IC packaging market is gaining traction as semiconductor manufacturers shift toward advanced packaging technologies to address the rising demand for high-performance computing and compact device architectures. The through silicon via (TSV) IC packaging market is gaining traction as semiconductor manufacturers shift toward advanced packaging technologies to address the rising demand for high-performance computing and compact device architectures.

The growth of the market is primarily driven by the need for higher bandwidth, reduced power consumption, and miniaturization of electronic devices. TSV technology enables vertical stacking of integrated circuits, reducing signal delays and improving performance efficiency compared to traditional packaging methods. This makes it particularly valuable in high-performance computing, artificial intelligence, and memory-intensive applications.

Key Highlights:

- The market size reached USD 8.9 billion in 2025 and is projected to grow significantly, reaching USD 28.6 billion by 2034. This reflects strong expansion driven by increasing demand across semiconductor and advanced electronics industries.

- The market is expected to register a CAGR of 13.8% during the forecast period from 2025 to 2034. This steady growth rate highlights rising investments in advanced packaging technologies and innovation.

- There is a growing demand for high-performance and compact semiconductor solutions across industries such as consumer electronics and data centers. This is pushing manufacturers to adopt advanced packaging methods like TSV technology.

- The rising adoption of TSV technology in AI, 5G, and automotive applications is further accelerating market growth. These sectors require faster processing, improved efficiency, and higher integration density, which TSV enables effectively.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of 3D IC Integration

One of the prominent trends in the through silicon via (TSV) IC packaging market is the increasing adoption of 3D integrated circuit (IC) architectures. This trend is driven by the need to enhance performance while reducing footprint in modern electronic systems. TSV technology enables vertical stacking of dies, allowing shorter interconnect lengths and improved signal transmission speed. As industries such as artificial intelligence, machine learning, and high-performance computing demand faster processing capabilities, 3D IC integration is becoming a preferred solution. Additionally, this approach supports energy efficiency, which is critical for data centers and mobile devices. The trend is further reinforced by ongoing research and development in advanced packaging technologies.

Rising Focus on Advanced Memory Packaging Solutions

Another key trend shaping the market is the growing focus on advanced memory packaging, particularly high-bandwidth memory (HBM). TSV-based packaging plays a crucial role in enabling efficient stacking of memory dies, resulting in improved bandwidth and reduced latency. This is particularly relevant for applications such as gaming, graphics processing, and data-intensive workloads. Semiconductor companies are increasingly investing in memory-centric architectures to meet the evolving demands of end users. The integration of TSV technology in memory solutions is expected to enhance overall system performance while supporting next-generation computing requirements. This trend is anticipated to drive significant growth in the market over the forecast period.

Market Drivers

Growing Demand for High-Performance Computing

The increasing demand for high-performance computing (HPC) is a major driver of the through silicon via (TSV) IC packaging market. Industries such as cloud computing, artificial intelligence, and scientific research require advanced processing capabilities to handle complex workloads. TSV technology enables faster data transfer and improved power efficiency, making it an ideal solution for HPC applications. As organizations continue to invest in data centers and advanced computing infrastructure, the need for efficient semiconductor packaging solutions is expected to rise. This driver is further supported by the rapid growth of big data analytics and edge computing technologies.

Expansion of Consumer Electronics and 5G Devices

The rapid expansion of consumer electronics and 5G-enabled devices is also fueling market growth. Smartphones, wearables, and connected devices require compact and efficient semiconductor solutions to deliver enhanced performance. TSV packaging allows for higher integration density and improved thermal management, which are essential for modern electronic devices. The rollout of 5G networks is accelerating the demand for high-speed data processing and low-latency communication, further driving the adoption of TSV technology. As consumer expectations for performance and functionality continue to evolve, manufacturers are increasingly adopting advanced packaging solutions to remain competitive.

Market Restraint

High Manufacturing Costs and Complex Fabrication Processes

Despite its advantages, the through silicon via (TSV) IC packaging market faces challenges related to high manufacturing costs and complex fabrication processes. TSV technology requires precise drilling, insulation, and filling processes, which increase production complexity and cost. This can be a barrier for small and medium-sized semiconductor manufacturers, limiting widespread adoption. Additionally, the need for specialized equipment and skilled workforce further adds to operational expenses. These factors can impact profit margins and slow down market growth, particularly in price-sensitive regions.

For example, companies attempting to integrate TSV technology into standard production lines often encounter yield issues due to defects in via formation. Such challenges can lead to increased production time and cost overruns. While ongoing advancements in manufacturing techniques are expected to address these issues, cost-related constraints remain a key concern for industry stakeholders.

Market Opportunities

Growth in Automotive Electronics and Autonomous Vehicles

The increasing adoption of advanced electronics in the automotive sector presents significant opportunities for the through silicon via (TSV) IC packaging market. Modern vehicles are equipped with sophisticated systems such as advanced driver-assistance systems (ADAS), infotainment, and autonomous driving technologies. These systems require high-performance and reliable semiconductor solutions, which can be effectively supported by TSV packaging. The ability to integrate multiple functionalities within a compact design makes TSV technology highly suitable for automotive applications. As the automotive industry continues to evolve toward electrification and automation, the demand for advanced packaging solutions is expected to increase.

Emerging Applications in IoT and Edge Computing

Another promising opportunity lies in the growing adoption of Internet of Things (IoT) devices and edge computing solutions. These technologies require efficient data processing capabilities at the edge of networks, where space and power constraints are critical considerations. TSV packaging enables high-density integration and improved performance, making it an ideal choice for such applications. The proliferation of smart homes, industrial automation, and connected devices is driving the need for compact and efficient semiconductor solutions. As IoT ecosystems continue to expand, the demand for TSV-based packaging is expected to grow significantly.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.9 Billion |

| Market Size in 2026 | USD 10.2 Billion |

| Market Size in 2034 | USD 28.6 Billion |

| CAGR | 13.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The via-first TSV process segment dominated the market in 2024, accounting for approximately 42% of the total share. This segment is widely adopted due to its ability to integrate TSV formation early in the semiconductor manufacturing process, resulting in improved alignment and performance. Via-first technology is particularly suitable for applications requiring high precision and reliability, such as memory devices and high-performance processors. The segment benefits from advancements in fabrication techniques and increasing demand for compact and efficient semiconductor solutions. Additionally, the ability to achieve higher integration density makes it a preferred choice among manufacturers.

The via-middle TSV process is the fastest-growing segment, expected to register a CAGR of 14.5% during the forecast period. This growth is driven by its flexibility in integrating TSVs after front-end processing while maintaining cost efficiency. The segment is gaining traction in applications requiring a balance between performance and cost. Increasing adoption in consumer electronics and automotive applications is further supporting its growth. The ability to reduce manufacturing complexity while maintaining performance is a key factor contributing to the rapid expansion of this segment.

By Application

The consumer electronics segment held the largest market share in 2024, accounting for approximately 46% of the total market. The widespread use of TSV technology in smartphones, tablets, and wearable devices is driving growth in this segment. The demand for compact and high-performance devices is encouraging manufacturers to adopt advanced packaging solutions. TSV technology enables efficient integration of multiple components, resulting in improved device performance and reduced power consumption. This segment continues to benefit from rapid technological advancements and increasing consumer demand for innovative electronic products.

The automotive segment is the fastest-growing application, with a projected CAGR of 15.2% during the forecast period. The increasing adoption of advanced electronics in vehicles, including ADAS and autonomous driving systems, is driving demand for TSV-based packaging solutions. The need for reliable and high-performance semiconductor components is encouraging automotive manufacturers to adopt advanced technologies. Additionally, the transition toward electric vehicles is further supporting the growth of this segment, as these vehicles require efficient and compact electronic systems.

By End-Use

The integrated device manufacturers (IDMs) segment dominated the market in 2024, accounting for approximately 48% of the total share. IDMs have significant control over the entire semiconductor manufacturing process, allowing them to integrate TSV technology effectively. This segment benefits from strong research and development capabilities and the ability to invest in advanced fabrication facilities. The growing demand for high-performance semiconductor solutions is encouraging IDMs to adopt TSV-based packaging technologies.

The outsourced semiconductor assembly and test (OSAT) segment is the fastest-growing, expected to register a CAGR of 14.9% during the forecast period. This growth is driven by increasing outsourcing of semiconductor packaging processes by fabless companies. OSAT providers offer cost-effective and scalable solutions, making them an attractive option for manufacturers. The rising complexity of semiconductor packaging is encouraging companies to rely on specialized service providers, thereby driving growth in this segment.

Through Silicon Via (TSV) IC Packaging Market Segmentations

By Type

- Via-First TSV

- Via-Middle TSV

- Via-Last TSV

By Application

- Consumer Electronics

- Automotive

- Telecommunications

- Healthcare

- Industrial

By End-Use

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT)

- Fabless Companies

Regional Analysis

North America

North America accounted for approximately 28% of the global through silicon via (TSV) IC packaging market share in 2025 and is expected to register a CAGR of 12.9% during the forecast period. The region benefits from a strong presence of semiconductor companies and advanced research infrastructure. Increasing investments in data centers and artificial intelligence technologies are driving demand for high-performance packaging solutions. The adoption of TSV technology is also supported by government initiatives aimed at strengthening domestic semiconductor manufacturing capabilities.

The United States dominates the regional market due to its robust technology ecosystem and high demand for advanced computing solutions. A key growth factor is the increasing deployment of hyperscale data centers, which require efficient and high-density semiconductor packaging. This trend is encouraging companies to adopt TSV-based solutions to enhance performance and energy efficiency.

Europe

Europe held around 20% of the market share in 2025 and is projected to grow at a CAGR of 12.3% through 2034. The region is witnessing steady growth due to increasing demand for advanced electronics in automotive and industrial applications. European countries are focusing on strengthening their semiconductor supply chains, which is expected to boost the adoption of TSV technology. The presence of established automotive manufacturers further supports market growth.

Germany leads the European market, driven by its strong automotive industry. A unique growth factor is the increasing integration of semiconductor technologies in electric vehicles and industrial automation systems. This is creating a demand for reliable and high-performance packaging solutions, thereby supporting the growth of the TSV IC packaging market.

Asia Pacific

Asia Pacific dominated the global market with a share of approximately 38% in 2025 and is expected to register the highest CAGR of 14.6% during the forecast period. The region is a major hub for semiconductor manufacturing, with countries such as China, Japan, South Korea, and Taiwan playing a significant role. Increasing investments in advanced fabrication facilities and growing demand for consumer electronics are driving market growth.

China is the dominant country in the region, supported by large-scale semiconductor production and government initiatives. A key growth factor is the rapid expansion of the electronics manufacturing sector, which is driving demand for advanced packaging technologies. This is encouraging the adoption of TSV solutions across various applications.

Middle East & Africa

The Middle East & Africa region accounted for around 7% of the market share in 2025 and is expected to grow at a CAGR of 11.5% during the forecast period. The market is gradually expanding due to increasing adoption of digital technologies and infrastructure development. Investments in smart cities and telecommunications are contributing to the demand for advanced semiconductor solutions.

The United Arab Emirates is a leading country in the region, driven by its focus on technological innovation. A unique growth factor is the development of smart city projects, which require efficient and high-performance electronic systems. This is creating opportunities for TSV-based packaging solutions in the region.

Latin America

Latin America held approximately 7% of the global market share in 2025 and is projected to grow at a CAGR of 11.8% through 2034. The region is experiencing moderate growth due to increasing adoption of consumer electronics and industrial automation. Governments are investing in digital transformation initiatives, which is expected to support market expansion.

Brazil dominates the regional market, supported by its growing electronics industry. A key growth factor is the increasing demand for connected devices and smart technologies. This is driving the need for advanced semiconductor packaging solutions, including TSV technology.

Competitive Landscape

The through silicon via (TSV) IC packaging market is moderately competitive, with several key players focusing on innovation and strategic collaborations to strengthen their market position. The market is characterized by continuous investments in research and development to enhance TSV technology and improve manufacturing efficiency. Companies are also expanding their production capacities to meet growing demand from various end-use industries.

A leading player in the market is Intel Corporation, which has been actively investing in advanced packaging technologies, including TSV solutions. The company recently announced the expansion of its advanced packaging facilities to support next-generation semiconductor applications. Other major players are focusing on partnerships and acquisitions to enhance their technological capabilities and expand their global presence.

Key Players List

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Samsung Electronics

- ASE Technology Holding Co., Ltd.

- Amkor Technology

- STMicroelectronics

- Broadcom Inc.

- Texas Instruments Incorporated

- IBM Corporation

- Micron Technology

- SK Hynix Inc.

- JCET Group Co., Ltd.

- Powertech Technology Inc.

- GlobalFoundries

- United Microelectronics Corporation (UMC)