Supplement And Nutrition Packaging Market Size and Growth

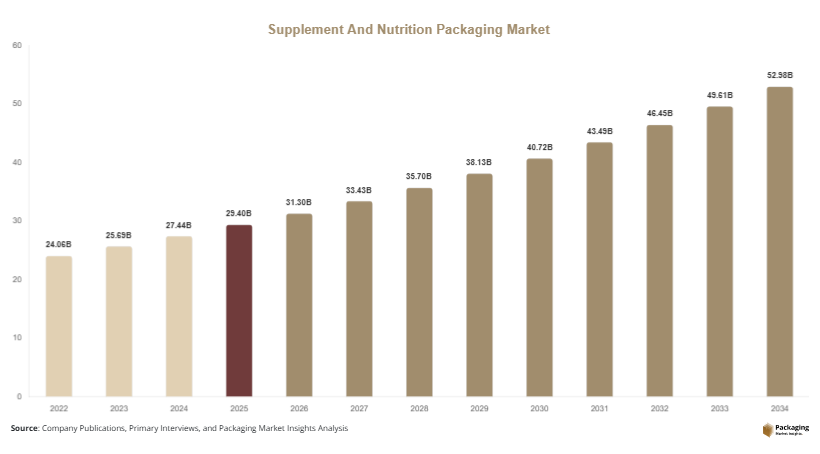

The global supplement and nutrition packaging market size was valued at approximately USD 29.4 billion in 2025 and is expected to reach USD 31.3 billion in 2026. By 2034, the market is forecasted to achieve nearly USD 56.8 billion, expanding at a CAGR of 6.8% during 2025–2034. Rising demand for sports nutrition products, increasing consumption of vitamins and dietary supplements, and growth in e-commerce health product sales are major factors supporting market expansion.

The supplement and nutrition packaging market is witnessing substantial growth due to increasing consumer awareness regarding health, fitness, preventive healthcare, and nutritional supplementation. Packaging solutions for dietary supplements, vitamins, protein powders, functional beverages, and nutritional products are evolving rapidly to meet demands for product safety, convenience, sustainability, and shelf-life extension. Manufacturers are increasingly adopting advanced packaging formats such as stand-up pouches, recyclable bottles, blister packs, sachets, and high-barrier flexible packaging to protect sensitive nutritional ingredients from moisture, oxygen, and contamination.

Key Highlights

- Asia Pacific dominated the market with a 35.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Plastic bottles and containers led the type segment with a 38.4% share.

- Plastic-based packaging materials dominated the market with a 54.2% share.

- Dietary supplements and vitamins led the end-use segment with 42.8% share.

- The US remained the dominant country with a market size of USD 6.3 billion in 2025 and USD 6.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Demand for Sustainable and Recyclable Supplement Packaging

A major trend shaping the supplement and nutrition packaging market is the growing adoption of sustainable and recyclable packaging materials. Consumers are increasingly preferring environmentally responsible packaging solutions for vitamins, protein powders, and nutraceutical products. Packaging manufacturers are reducing the use of virgin plastics and introducing recyclable PET containers, paper-based cartons, and bio-based flexible films. For example, supplement brands in Europe and North America are launching refill pouch systems that reduce plastic waste while improving transportation efficiency. Retailers are also encouraging sustainable packaging adoption to align with corporate ESG targets. This trend is expected to accelerate over the forecast period as governments implement stricter packaging waste regulations and consumers continue to prioritize eco-friendly product choices.

Growth of Smart and Personalized Packaging Solutions

Another significant trend is the increasing use of personalized and smart packaging technologies for nutritional supplements. Brands are integrating QR codes, digital authentication systems, and dosage tracking features into packaging formats to improve customer engagement and product transparency. Personalized nutrition subscription services are also driving demand for custom-labeled sachets, portion packs, and monthly supplement kits. For instance, nutrition brands in the United States and Japan are offering subscription-based vitamin packs packaged in single-use daily sachets with personalized dosage information. The future impact of this trend is expected to include greater integration of connected packaging technologies and enhanced consumer convenience across online supplement distribution channels.

Market Drivers

Rising Consumer Focus on Preventive Healthcare and Wellness

The increasing global emphasis on preventive healthcare is a major driver for the supplement and nutrition packaging market. Consumers are actively purchasing vitamins, minerals, herbal supplements, and immunity-boosting products to maintain long-term health and wellness. This growing supplement consumption directly increases demand for secure and moisture-resistant packaging solutions. Packaging formats such as tamper-evident bottles, blister packs, and resealable pouches are becoming increasingly important for preserving product quality and safety. For example, vitamin manufacturers in the United States and Germany are adopting high-barrier packaging technologies to improve shelf stability for sensitive formulations. As wellness trends continue to expand globally, supplement packaging demand is expected to rise consistently.

Expansion of E-Commerce Sales for Nutritional Products

The rapid growth of e-commerce platforms for health and wellness products is another important market driver. Online supplement retailers require packaging solutions that protect products during shipping while maintaining visual appeal and brand differentiation. Lightweight flexible packaging and durable plastic containers are increasingly preferred because they reduce transportation costs and minimize product damage. In countries such as India and China, online sales of protein powders and dietary supplements are expanding rapidly due to increasing internet penetration and smartphone usage. Packaging companies are responding by developing leak-resistant, compact, and sustainable packaging solutions optimized for direct-to-consumer distribution models.

Market Restraint

Volatility in Raw Material Prices and Regulatory Compliance Challenges

One of the major restraints affecting the supplement and nutrition packaging market is the fluctuation in raw material prices and increasing regulatory compliance requirements. Packaging materials such as PET, HDPE, aluminum foil, and multilayer flexible films are subject to price volatility linked to petroleum markets and global supply chain disruptions. These cost fluctuations can reduce profit margins for supplement manufacturers and packaging suppliers. In addition, strict regulations related to labeling, child-resistant closures, tamper-evident packaging, and food-grade material standards increase production complexity and operational expenses. For example, nutritional supplement companies exporting products to Europe and North America must comply with detailed packaging and labeling regulations that differ across regions. Smaller manufacturers may face difficulties adapting to these requirements due to higher compliance costs and limited access to advanced packaging technologies. These factors may slow market expansion in price-sensitive markets and create operational challenges for packaging producers.

Market Opportunities

Expansion of Single-Serve and Portable Nutrition Packaging

The growing demand for portable and convenient nutritional products presents a significant opportunity for the supplement and nutrition packaging market. Consumers with active lifestyles increasingly prefer single-serve protein powders, vitamin sachets, meal replacement drinks, and nutritional gummies packaged in compact formats. Flexible stand-up pouches, stick packs, and travel-size containers are gaining popularity because they improve convenience and reduce product waste. Sports nutrition brands in North America and Asia Pacific are introducing portable packaging solutions targeted at gym users and athletes. This trend is expected to create long-term opportunities for lightweight and resealable packaging innovations across the supplement industry.

Increasing Adoption of Pharmaceutical-Grade Packaging Technologies

The use of pharmaceutical-grade packaging technologies in the nutraceutical sector offers strong future growth opportunities. Nutritional supplements containing probiotics, omega-3 oils, and herbal extracts often require advanced moisture and oxygen barrier protection to maintain product stability. Packaging manufacturers are developing high-barrier blister packs, desiccant-integrated containers, and UV-resistant packaging solutions to improve shelf life. Countries such as Japan and Switzerland are witnessing rising demand for premium supplement packaging with enhanced safety and traceability features. As consumers increasingly prioritize product quality and authenticity, pharmaceutical-grade supplement packaging is expected to gain broader commercial adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 29.4 Billion |

| Market Size in 2026 | USD 31.3 Billion |

| Market Size in 2034 | USD 56.8 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic bottles and containers dominated the market in 2024 with approximately 38.4% share due to their durability, moisture resistance, and compatibility with tablets, capsules, powders, and gummies. These packaging formats are widely used across vitamins, herbal supplements, and sports nutrition products because they provide strong product protection and long shelf life. Manufacturers prefer HDPE and PET bottles due to their lightweight structure, resealable functionality, and cost efficiency. Supplement brands in North America and Europe increasingly use tamper-evident closures and child-resistant caps to comply with regulatory requirements. In addition, bottles and containers offer excellent branding opportunities through custom labeling and printed shrink sleeves, making them highly suitable for retail shelf visibility and e-commerce distribution channels.

Flexible stand-up pouches are expected to be the fastest-growing type segment, registering a CAGR of 7.5% during the forecast period. Consumers increasingly prefer lightweight and portable packaging solutions for protein powders, nutritional drink mixes, and gummy supplements. Stand-up pouches reduce packaging material usage while lowering transportation and storage costs. Sports nutrition brands are adopting resealable zipper pouches and refill packaging systems to improve convenience and sustainability. In countries such as Japan, the United States, and Australia, supplement manufacturers are launching premium pouch packaging with matte finishes and digital printing features to attract younger consumers. Rising demand for sustainable and travel-friendly packaging solutions is expected to drive future segment growth.

By Material

Plastic-based packaging materials dominated the market in 2024 with a market share of approximately 54.2%. Plastic materials such as PET, HDPE, and polypropylene are widely used due to their strength, moisture resistance, lightweight structure, and affordability. These materials are commonly used for supplement bottles, jars, flexible pouches, and blister packaging applications. Packaging manufacturers continue to improve plastic barrier performance to protect sensitive nutritional ingredients from humidity, oxygen, and UV exposure. In addition, plastic materials support high-speed automated packaging operations, making them suitable for large-scale supplement manufacturing. Growing global demand for affordable and durable supplement packaging continues to support segment dominance across retail and online distribution channels.

Recyclable paper-based materials are projected to be the fastest-growing material segment with a CAGR of 7.2% during the forecast period. Sustainability regulations and consumer preference for environmentally responsible packaging are encouraging supplement brands to adopt paperboard cartons, fiber-based containers, and recyclable labels. Companies are investing in hybrid paper-plastic packaging systems that reduce overall plastic consumption while maintaining product protection. Nutraceutical companies in Europe and Canada are increasingly introducing paper-based refill packaging for vitamins and powdered supplements. In addition, advancements in moisture-resistant paper coatings are improving the commercial viability of paper-based supplement packaging. Continued growth in sustainable packaging initiatives is expected to accelerate segment expansion over the coming years.

By End-Use

Dietary supplements and vitamins dominated the global market in 2024 with approximately 42.8% share due to rising consumer awareness regarding immunity, wellness, and preventive healthcare. Vitamin tablets, capsules, gummies, and herbal supplements require protective packaging solutions that preserve product stability and prevent contamination. Packaging formats such as plastic bottles, blister packs, and sachets are widely used across retail pharmacies, supermarkets, and e-commerce platforms. Consumers increasingly prefer portable and resealable packaging for daily supplement usage. Countries including the United States, Germany, and China continue to witness high demand for packaged dietary supplements due to aging populations and growing wellness trends. Strong retail distribution networks and online health product sales are further supporting segment dominance.

Sports nutrition products are expected to emerge as the fastest-growing end-use segment, registering a CAGR of 7.4% during the forecast period. Rising gym memberships, active lifestyles, and fitness awareness are increasing demand for protein powders, energy supplements, and meal replacement products. Packaging manufacturers are developing large-capacity tubs, lightweight pouches, and single-serve stick packs to improve convenience and portability for athletes and fitness consumers. Sports nutrition brands are also investing in premium packaging aesthetics, transparent labeling, and recyclable materials to strengthen brand identity. In Asia Pacific and Latin America, growing youth populations and expanding fitness culture are expected to create strong long-term growth opportunities for sports nutrition packaging solutions.

Supplement And Nutrition Packaging Market Segmentations

By Type

- Plastic Bottles & Containers

- Flexible Stand-Up Pouches

- Blister Packs

- Sachets & Stick Packs

By Material

- Plastic-Based Materials

- Paper-Based Materials

- Aluminum Foil

- Glass Packaging

By End-User

- Dietary Supplements & Vitamins

- Sports Nutrition Products

- Functional Foods

- Herbal Supplements

- Nutritional Beverages

Regional Analysis

North America

North America accounted for approximately 27.4% of the global market share in 2025 and is projected to grow at a CAGR of 6.3% during the forecast period. The region benefits from strong consumer awareness regarding dietary supplements, sports nutrition products, and preventive healthcare solutions. The United States and Canada continue to witness rising demand for protein powders, immunity supplements, and personalized nutrition products. E-commerce platforms and specialty nutrition retailers are increasing sales of packaged nutraceutical products, creating demand for durable and visually attractive packaging solutions. Packaging companies in the region are investing heavily in recyclable containers, smart labeling systems, and tamper-evident packaging technologies to meet regulatory and consumer expectations.

The United States dominates the North American market due to its large nutraceutical industry and high supplement consumption rates. A unique growth driver in the country is the increasing popularity of subscription-based vitamin and wellness products. Nutrition brands are introducing personalized daily supplement packs packaged in single-use sachets and portable containers. Online supplement retailers are also investing in premium packaging designs that improve customer experience and brand differentiation. Rising demand for clean-label wellness products and sustainable packaging solutions is expected to continue supporting market expansion in the United States.

Europe

Europe represented nearly 22.6% market share in 2025 and is expected to expand at a CAGR of 5.9% through 2034. The region is characterized by strong regulatory standards, growing demand for organic supplements, and increasing adoption of sustainable packaging solutions. Consumers across Germany, France, and the Nordic countries are increasingly purchasing vitamins, herbal supplements, and nutritional beverages packaged in recyclable containers and paper-based cartons. Packaging companies are developing lightweight packaging formats to reduce material usage and improve transportation efficiency. In addition, pharmaceutical-grade supplement packaging demand is rising due to strict safety and traceability requirements in the European Union.

Germany remains the dominant country in the European market due to its advanced nutraceutical manufacturing sector and strong consumer focus on preventive healthcare. A unique growth factor in Germany is the increasing use of eco-friendly refill systems for vitamins and dietary supplements. Retailers and supplement brands are introducing refillable packaging models that reduce plastic waste and improve sustainability performance. In addition, packaging manufacturers are integrating digital authentication technologies to prevent counterfeit supplement products. These innovations are expected to strengthen long-term market growth across the country.

Asia Pacific

Asia Pacific dominated the global supplement and nutrition packaging market with a 35.9% share in 2025 and is projected to register a CAGR of 7.3% during the forecast period. Rapid urbanization, increasing disposable income, and rising health awareness are driving strong demand for dietary supplements and nutritional products across the region. Countries such as China, India, Japan, and South Korea are witnessing increasing consumption of vitamins, herbal supplements, protein powders, and functional nutrition products. Expansion of e-commerce retail and online wellness platforms is further accelerating demand for secure and lightweight packaging solutions. Packaging manufacturers are also investing in high-barrier flexible films and recyclable plastic containers to support regional market growth.

China remains the leading country in the Asia Pacific market due to its large consumer base and expanding online supplement industry. A unique growth driver in China is the increasing demand for immunity-boosting and traditional herbal nutritional products packaged in convenient sachets and portable bottles. Domestic supplement brands are investing in premium packaging designs and anti-counterfeit labeling systems to improve consumer trust. In addition, government initiatives supporting healthcare awareness and domestic nutraceutical production are encouraging further market expansion. Growth in cross-border e-commerce sales of nutritional supplements is also supporting demand for durable export packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.9% market share in 2025 and is projected to expand at a CAGR of 6.7% through 2034. Rising healthcare awareness, increasing fitness culture, and growing demand for imported nutritional supplements are contributing to market growth across the region. Urban consumers are increasingly purchasing vitamins, sports nutrition products, and immunity supplements through pharmacies, supermarkets, and online retail channels. Packaging demand is also increasing due to expansion of regional healthcare and wellness industries. Manufacturers are introducing moisture-resistant packaging and portable supplement containers designed for hot climate conditions and long-distance transportation.

Saudi Arabia dominates the regional market because of rising disposable income and increasing consumer interest in wellness products. A unique growth factor in the country is the rapid expansion of fitness centers and sports nutrition retail stores. Supplement brands are introducing premium packaging formats for protein powders, energy supplements, and nutritional drinks targeted at younger consumers. In addition, regional distributors are increasing imports of international supplement brands packaged in pharmaceutical-grade containers and flexible packaging systems. Continued growth in health-conscious consumer behavior is expected to support market expansion across Saudi Arabia and neighboring Gulf countries.

Latin America

Latin America held approximately 7.2% market share in 2025 and is expected to register the fastest growth at a CAGR of 7.1% during the forecast period. Increasing health awareness, rising gym memberships, and growing demand for affordable nutritional supplements are supporting market expansion across Brazil, Mexico, and Argentina. Retail pharmacies, supermarkets, and online wellness stores are expanding distribution of packaged vitamins and protein products. Packaging manufacturers are also investing in lightweight flexible packaging and cost-effective plastic containers to meet rising regional demand. Government initiatives promoting preventive healthcare and nutritional awareness are further contributing to market growth.

Brazil remains the dominant country in the Latin American market due to its expanding sports nutrition industry and growing dietary supplement consumption. A unique growth driver in Brazil is the increasing popularity of protein supplements and meal replacement products among fitness-conscious consumers. Local supplement brands are introducing resealable stand-up pouches and single-serve packaging formats to improve affordability and convenience. In addition, the country is witnessing rising investments in domestic nutraceutical manufacturing and sustainable packaging solutions. Expanding retail penetration and increasing online supplement sales are expected to continue supporting market demand.

Competitive Landscape

The global supplement and nutrition packaging market is moderately fragmented, with leading companies focusing on sustainable packaging technologies, advanced barrier materials, and customized packaging formats for nutraceutical and wellness brands. Major packaging manufacturers are investing in recyclable plastics, lightweight flexible packaging, digital printing technologies, and tamper-evident solutions to strengthen their competitive positions. Strategic collaborations with supplement brands and e-commerce retailers are also becoming increasingly important as online sales continue to expand globally.

Amcor plc remains one of the leading companies in the market due to its broad flexible and rigid packaging portfolio, global manufacturing presence, and ongoing investments in sustainable packaging innovation. Berry Global Inc., Gerresheimer AG, AptarGroup Inc., and Constantia Flexibles are also major market participants focusing on pharmaceutical-grade packaging, child-resistant closures, and high-barrier flexible materials. Companies are increasingly introducing smart packaging technologies, QR-based traceability systems, and refill packaging solutions to improve consumer engagement and regulatory compliance.

Key Players List

- Amcor plc

- Berry Global Inc.

- Gerresheimer AG

- AptarGroup Inc.

- Constantia Flexibles

- Sonoco Products Company

- Alpha Packaging

- Comar LLC

- SGD Pharma

- Huhtamaki Oyj

- ProAmpac LLC

- West Pharmaceutical Services, Inc.

- CCL Industries Inc.

- Graham Packaging Company

- Silgan Holdings Inc.