Sterilized Packaging Market Size and Growth

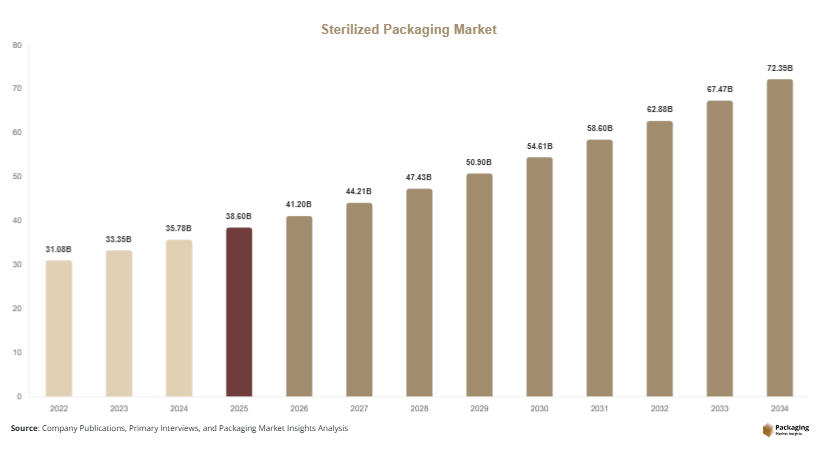

The global sterilized packaging market was valued at USD 38.6 billion in 2025 and is projected to reach USD 41.2 billion in 2026. The market is forecasted to attain USD 72.4 billion by 2034, registering a CAGR of 7.3% during the forecast period from 2025 to 2034. The market growth is being supported by rising demand for contamination-free medical products, increasing pharmaceutical production, and expanding healthcare infrastructure across emerging economies.

Sterilized packaging plays a critical role in preserving product integrity, preventing microbial contamination, and extending shelf life for sensitive products. The market has gained significant momentum due to growing adoption in healthcare, pharmaceutical, food processing, and biotechnology sectors. Hospitals and healthcare facilities are increasingly utilizing sterile barrier systems to minimize hospital-acquired infections and improve patient safety standards. At the same time, regulatory agencies are implementing stricter packaging and sterilization requirements for medical devices and pharmaceutical products, creating sustained demand for advanced sterilized packaging solutions.

Key Market Insights

- Asia Pacific dominated the sterilized packaging market with a 36.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 8.1% during the forecast period.

- Plastic-based sterilized packaging led the material segment with a 54.2% market share.

- Thermoform trays dominated the type segment with a 31.6% share.

- Pharmaceutical end-use applications accounted for 41.7% of total market share.

- The US remained the dominant country in North America with a market size of USD 9.6 billion in 2025 and USD 10.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Sterilized Packaging Materials

Sustainability has emerged as a major trend shaping the sterilized packaging market. Healthcare providers and pharmaceutical manufacturers are increasingly adopting recyclable and bio-based packaging materials to reduce medical waste and comply with environmental regulations. Traditional sterilized packaging materials often rely heavily on multilayer plastics that are difficult to recycle. As a result, packaging companies are investing in mono-material structures, recyclable polyethylene solutions, and paper-based sterile barrier systems.

Several manufacturers are introducing low-carbon packaging technologies designed to maintain sterilization efficiency while minimizing environmental impact. For example, medical packaging producers in Europe are developing recyclable sterilization wraps for surgical instruments and medical kits. Hospitals are also implementing waste reduction initiatives that favor lightweight and recyclable sterile packaging systems. This trend is expected to encourage wider commercialization of environmentally responsible sterilized packaging formats over the next decade, particularly in developed healthcare markets.

Rising Integration of Smart Packaging Technologies

Smart packaging integration is becoming increasingly important in sterilized packaging applications. Healthcare and pharmaceutical companies are adopting packaging systems equipped with tracking indicators, temperature monitoring technologies, and sterilization validation features. These technologies improve supply chain transparency and ensure product safety during transportation and storage.

Radio-frequency identification tags, QR codes, and chemical sterilization indicators are being integrated into medical packaging to reduce contamination risks and improve inventory management. Pharmaceutical companies handling vaccines and biologic drugs are especially utilizing intelligent packaging systems to maintain product integrity. For example, temperature-sensitive injectable medications now commonly include sterilization verification indicators that alert healthcare professionals about storage failures. Future adoption of connected packaging systems is expected to enhance traceability, reduce product recalls, and improve compliance with global healthcare regulations.

Market Drivers

Expanding Global Pharmaceutical Manufacturing Activities

Rapid expansion of pharmaceutical manufacturing facilities is one of the major drivers supporting the sterilized packaging market. Pharmaceutical companies are increasing production capacities for injectable drugs, vaccines, biologics, and specialty medicines, all of which require sterile packaging solutions to maintain product safety and efficacy. Rising global healthcare expenditure and increasing demand for advanced therapies are contributing to higher pharmaceutical output across both developed and emerging economies.

The expansion of contract manufacturing organizations has further accelerated demand for sterilized packaging products. Pharmaceutical manufacturers increasingly rely on sterile blister packs, pouches, vials, and trays to meet strict regulatory requirements regarding contamination prevention. For example, several Asian pharmaceutical manufacturers have expanded sterile injectable production facilities to support global vaccine distribution and oncology drug manufacturing. The growing pharmaceutical export industry is expected to continue driving strong demand for validated sterile packaging systems over the forecast period.

Increasing Incidence of Hospital-Acquired Infections

Growing concerns regarding hospital-acquired infections are significantly increasing demand for sterilized medical packaging solutions. Healthcare providers are implementing stricter infection prevention measures to improve patient safety and reduce treatment costs associated with contaminated medical devices and surgical products. Sterilized packaging helps maintain product sterility throughout handling, transportation, and storage, thereby reducing contamination risks in hospitals and clinics.

Demand for single-use surgical instruments, sterile gloves, syringes, and catheters has increased substantially across healthcare systems worldwide. Hospitals are increasingly adopting advanced sterilization wraps, rigid containers, and peelable pouches to maintain compliance with infection control standards. For instance, healthcare facilities in North America and Europe are investing in sterile barrier packaging systems designed to withstand repeated sterilization cycles while ensuring durability. Continued growth in surgical procedures and expanding healthcare access are expected to sustain demand for high-performance sterilized packaging products.

Market Restraint

High Costs Associated with Sterile Packaging Validation and Compliance

High operational and compliance costs remain a major restraint for the sterilized packaging market. Manufacturers must comply with strict sterilization validation procedures, material testing standards, and regulatory documentation requirements, which significantly increase production expenses. Sterilized packaging products used for pharmaceutical and medical applications require extensive testing to ensure microbial barrier protection, seal integrity, and compatibility with sterilization methods such as ethylene oxide, gamma radiation, and steam sterilization.

Small and medium-sized packaging manufacturers often face difficulties in maintaining compliance with international healthcare regulations due to limited financial resources. Additionally, fluctuations in raw material prices, especially medical-grade plastics and specialty films, further increase operational costs. For example, companies supplying sterile packaging for implantable medical devices must undergo lengthy qualification processes before commercialization. These challenges may limit market entry for smaller suppliers and slow product innovation in cost-sensitive regions. Despite strong long-term demand, pricing pressures and compliance complexities continue to impact overall profitability within the industry.

Market Opportunities

Rising Demand for Sterile Packaging in Biopharmaceutical Applications

The growing biopharmaceutical industry presents substantial opportunities for sterilized packaging manufacturers. Increasing production of biologics, gene therapies, cell therapies, and personalized medicines requires highly specialized sterile packaging systems capable of preserving sensitive formulations. Biopharmaceutical products are particularly vulnerable to contamination and environmental exposure, creating strong demand for advanced sterile barrier packaging solutions.

Packaging companies are developing high-barrier sterile containers, cryogenic packaging systems, and flexible sterile pouches specifically designed for biologic drugs. Expansion of biotechnology research centers and biopharmaceutical manufacturing facilities in countries such as the United States, China, and South Korea is expected to accelerate adoption of customized sterile packaging formats. Future growth in temperature-sensitive pharmaceutical products will further strengthen opportunities for packaging companies specializing in sterile transport and storage solutions.

Expansion of Healthcare Infrastructure in Emerging Economies

Rapid healthcare infrastructure development across emerging economies is creating significant growth opportunities for the sterilized packaging market. Governments in Asia Pacific, Latin America, and the Middle East are increasing investments in hospitals, diagnostic laboratories, pharmaceutical manufacturing facilities, and medical device production. These investments are generating higher demand for sterilized packaging products across healthcare supply chains.

Countries including India, Brazil, Saudi Arabia, and Indonesia are expanding healthcare access and increasing domestic pharmaceutical production capabilities. This trend is encouraging local packaging manufacturers to invest in sterile packaging technologies and automated production systems. Rising medical tourism in developing countries is also increasing the use of sterile surgical products and disposable medical devices. Over the next decade, emerging economies are expected to become major growth centers for sterilized packaging suppliers due to expanding healthcare consumption and improving industrial capabilities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.6 Billion |

| Market Size in 2026 | USD 41.2 Billion |

| Market Size in 2034 | USD 72.4 Billion |

| CAGR | 7.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Thermoform trays dominated the sterilized packaging market in 2024 with a market share of 31.6%. These trays are widely used for surgical instruments, pharmaceutical products, and medical devices due to their durability, contamination resistance, and compatibility with multiple sterilization methods. Thermoform trays provide excellent barrier protection and structural integrity during transportation and storage, making them highly suitable for sensitive healthcare applications. Hospitals and pharmaceutical manufacturers increasingly prefer thermoform trays because they can be customized for different device configurations while maintaining sterility standards. Growth in surgical procedures and rising demand for pre-packaged sterile medical kits have further strengthened adoption. Medical device manufacturers are also utilizing multilayer thermoformed packaging solutions that improve visibility and product security. The segment continues to benefit from increasing healthcare investments and expanding global production of sterile medical equipment.

Sterilized pouches are projected to witness the fastest growth, registering a CAGR of 8.4% during the forecast period. The segment is gaining momentum due to increasing demand for lightweight, flexible, and cost-efficient sterile packaging solutions. Sterilized pouches are widely utilized for disposable medical instruments, diagnostic products, and pharmaceutical packaging because they offer convenient handling and easy sterilization validation. Manufacturers are introducing high-barrier pouch materials with enhanced puncture resistance and peelable sealing technologies that improve usability in healthcare environments. Demand is also increasing for recyclable pouch materials as healthcare organizations focus on sustainability initiatives. Growth in home healthcare services and outpatient treatment facilities is expected to further accelerate adoption of sterile pouch packaging over the next decade.

By Material

Plastic-based sterilized packaging held the largest market share of 54.2% in 2024 due to its strong barrier properties, flexibility, and compatibility with multiple sterilization processes. Materials such as polyethylene, polypropylene, and polyethylene terephthalate are widely used in sterile packaging because they provide durability and effective microbial protection. Plastic materials are extensively utilized in pharmaceutical blister packs, sterile medical pouches, thermoform trays, and protective wraps. The dominance of this segment is also supported by the widespread availability of medical-grade polymers and the ability to manufacture customized packaging structures for different healthcare applications. Pharmaceutical companies continue to rely on plastic-based sterile packaging solutions because they offer superior moisture resistance and product visibility. Additionally, increasing demand for lightweight packaging in medical exports has strengthened the adoption of plastic materials across global healthcare supply chains.

Paper-based materials are expected to register the fastest CAGR of 7.8% through 2034. The growth of this segment is being driven by rising environmental concerns and increasing demand for recyclable medical packaging solutions. Healthcare providers and packaging manufacturers are investing in sustainable sterile barrier systems that reduce plastic consumption without compromising sterility performance. Paper-based sterile wraps and pouches are gaining popularity in hospitals and surgical centers due to their biodegradability and lower environmental impact. Technological advancements in coated medical papers and fiber-based barrier materials are improving strength, durability, and sterilization compatibility. Future growth is expected to accelerate as governments implement stricter sustainability regulations for healthcare packaging waste management.

By End-Use

Pharmaceutical applications accounted for the largest share of the sterilized packaging market in 2024, representing 41.7% of total revenue. The segment’s dominance is attributed to increasing production of injectable drugs, vaccines, biologics, and over-the-counter medicines requiring contamination-free packaging systems. Pharmaceutical manufacturers rely heavily on sterile packaging solutions to maintain product stability, prevent microbial exposure, and comply with global healthcare regulations. Demand for sterile blister packs, vials, pouches, and flexible packaging systems has increased substantially due to rising global pharmaceutical trade. Expansion of contract manufacturing organizations and increasing exports of generic medicines have also strengthened packaging demand. Additionally, pharmaceutical companies are investing in advanced sterile packaging automation systems that improve operational efficiency and quality assurance throughout production and distribution processes.

Biotechnology applications are projected to witness the fastest growth, expanding at a CAGR of 8.6% during the forecast period. Rising development of cell therapies, biologics, and personalized medicines is significantly increasing the need for specialized sterile packaging solutions. Biotechnology products are highly sensitive to contamination and environmental exposure, creating demand for high-barrier sterile containers and temperature-controlled packaging systems. Research laboratories and biopharmaceutical manufacturers are increasingly utilizing sterile flexible packaging for sample storage, transport, and processing applications. Growth in clinical research activities and expansion of biotechnology manufacturing facilities across Asia Pacific and North America are expected to further accelerate market demand. Innovations in cryogenic sterile packaging and advanced biologic transport systems are likely to create additional opportunities for segment expansion.

Sterilized Packaging Market Segmentations

By Type

- Thermoform Trays

- Sterilized Pouches

- Clamshells

- Sterile Bottles & Containers

- Wraps & Lids

By Material

- Plastic

- Paper & Paperboard

- Aluminum Foil

- Glass

- Composite Materials

By End-Use

- Pharmaceutical

- Biotechnology

- Medical Devices

- Hospitals & Clinics

- Food Processing

Regional Analysis

North America

North America accounted for 29.4% of the global sterilized packaging market share in 2025 and is projected to register a CAGR of 6.8% through 2034. The region benefits from a highly developed healthcare infrastructure, strong pharmaceutical manufacturing capabilities, and advanced regulatory frameworks governing sterile medical packaging. Demand for sterilized packaging is increasing due to rising surgical procedures, expanding biologics production, and growing use of disposable medical products. Healthcare providers across the United States and Canada are increasingly adopting sterile barrier systems that improve contamination prevention and patient safety. Additionally, the presence of major medical device manufacturers and contract pharmaceutical packaging companies continues to support stable regional demand for high-performance sterile packaging materials.

The United States remained the dominant country within North America due to its extensive pharmaceutical and medical device manufacturing industry. One of the key growth drivers in the country is the rapid increase in biologic drug production requiring specialized sterile packaging systems. Pharmaceutical companies are investing heavily in sterile fill-finish operations and advanced packaging automation technologies. For example, vaccine and injectable drug manufacturers are increasingly utilizing high-barrier sterile trays and flexible sterile pouches to maintain product integrity during transportation. The expansion of outpatient healthcare facilities and ambulatory surgical centers is also contributing to higher consumption of sterile disposable medical products throughout the country.

Europe

Europe represented 24.7% of the global sterilized packaging market in 2025 and is anticipated to grow at a CAGR of 6.5% during the forecast period. The region’s market growth is being driven by stringent healthcare regulations, rising demand for sustainable medical packaging, and increasing pharmaceutical exports. European healthcare systems emphasize infection prevention and environmental sustainability, encouraging the adoption of recyclable sterile packaging materials and low-emission sterilization technologies. Countries across Western Europe are implementing stricter standards for sterile barrier systems used in hospitals and pharmaceutical manufacturing facilities. In addition, growth in elderly populations and chronic disease treatment is increasing demand for sterile medical devices and pharmaceutical products requiring advanced packaging protection.

Germany emerged as the dominant country in the European market due to its strong pharmaceutical manufacturing sector and advanced industrial packaging capabilities. A major growth driver in Germany is the increasing investment in sustainable medical packaging technologies. Packaging manufacturers are focusing on recyclable sterile wraps, paper-based barrier systems, and reduced-plastic packaging solutions to meet environmental compliance targets. For instance, several healthcare packaging companies in Germany have expanded production of recyclable sterile pouches used for surgical instruments and medical kits. The country’s growing medical technology exports and strong healthcare innovation ecosystem continue to strengthen regional demand for high-quality sterilized packaging products.

Asia Pacific

Asia Pacific dominated the global sterilized packaging market with a 36.8% market share in 2025 and is expected to register a CAGR of 8.2% through 2034. The region is witnessing rapid expansion in pharmaceutical manufacturing, healthcare infrastructure development, and medical device production. Growing population levels, rising healthcare spending, and increasing awareness regarding infection prevention are contributing to strong demand for sterilized packaging products across developing economies. Countries throughout the region are investing in domestic pharmaceutical manufacturing capabilities to reduce import dependency and support healthcare security. Demand for sterile packaging materials is also increasing within the food processing and biotechnology industries due to stricter quality control standards and expanding export activities.

China remained the leading country in Asia Pacific due to its large-scale pharmaceutical manufacturing industry and rapidly expanding healthcare sector. One of the primary growth drivers in China is the increasing production of sterile injectable drugs and biologic medicines for both domestic and export markets. Pharmaceutical manufacturers are investing in advanced sterile packaging lines and automated cleanroom production systems to improve product quality and regulatory compliance. For example, several Chinese pharmaceutical companies have expanded vaccine production facilities that require large volumes of sterile vials, trays, and medical-grade packaging films. India is also emerging as a major contributor due to its expanding generic drug manufacturing industry and growing healthcare investments.

Middle East & Africa

The Middle East & Africa accounted for 4.8% of the global sterilized packaging market share in 2025 and is projected to grow at a CAGR of 7.1% during the forecast period. Increasing healthcare investments, rising pharmaceutical imports, and growing awareness regarding infection control are supporting market growth across the region. Governments in Gulf Cooperation Council countries are expanding healthcare infrastructure through the development of hospitals, pharmaceutical manufacturing facilities, and diagnostic centers. Demand for sterile medical packaging is increasing due to higher surgical volumes, growing use of disposable healthcare products, and rising adoption of modern sterilization technologies.

Saudi Arabia emerged as the dominant country in the region due to extensive healthcare modernization initiatives and growing pharmaceutical production investments. A key growth driver in the country is the expansion of local pharmaceutical manufacturing supported by government industrial diversification programs. Healthcare companies are increasingly adopting sterile packaging systems to comply with international healthcare standards and improve export competitiveness. For instance, domestic pharmaceutical firms are investing in sterile packaging equipment for injectable medications and surgical products. South Africa is also witnessing increasing demand for sterile packaging solutions due to rising healthcare consumption and improvements in medical supply chain infrastructure.

Latin America

Latin America held 4.3% of the global sterilized packaging market in 2025 and is forecasted to record the fastest CAGR of 8.1% through 2034. The market is benefiting from expanding healthcare access, increasing pharmaceutical production, and growing investments in medical infrastructure. Rising healthcare awareness and government-supported immunization programs are increasing demand for sterile pharmaceutical packaging across the region. Food safety concerns and growing processed food consumption are also encouraging adoption of sterile flexible packaging systems within the food industry.

Brazil remained the dominant country in the Latin American market due to its large healthcare sector and expanding pharmaceutical manufacturing activities. One major growth driver in Brazil is the increasing domestic production of generic medicines and vaccines requiring validated sterile packaging systems. Pharmaceutical companies are modernizing packaging operations to improve product quality and meet international export standards. For example, healthcare packaging suppliers in Brazil are expanding production capacities for sterilized pouches and thermoform trays used in surgical applications. Mexico is also experiencing strong market growth due to rising medical device manufacturing activities and increasing healthcare exports to North America.

Competitive Landscape

The sterilized packaging market is moderately consolidated, with leading companies focusing on product innovation, strategic partnerships, and expansion of healthcare packaging production capacities. Major market participants are investing in sustainable packaging technologies, automated sterile packaging systems, and advanced barrier materials to strengthen their market position.

Amcor plc remains one of the leading companies in the market due to its extensive global healthcare packaging portfolio and strong pharmaceutical customer base. The company continues to invest in recyclable sterile packaging solutions and lightweight medical packaging materials. Other major players are also emphasizing acquisitions and regional expansion strategies to improve manufacturing capabilities and strengthen distribution networks.

Berry Global has expanded its medical packaging production facilities to meet rising demand for sterile healthcare packaging in North America and Europe. DuPont focuses heavily on high-performance sterile barrier materials used for medical devices and pharmaceutical applications. Sonoco Products Company continues to develop customized thermoform sterile packaging systems for surgical and diagnostic products. Meanwhile, Sealed Air is investing in automation and sustainable sterile packaging technologies to improve operational efficiency and reduce packaging waste.

Competition within the market is expected to intensify as manufacturers prioritize sustainable material innovation, digital packaging technologies, and advanced sterilization compatibility solutions.

Key Players List

- Amcor plc

- Berry Global Inc.

- DuPont

- Sonoco Products Company

- Sealed Air Corporation

- Mondi Group

- West Pharmaceutical Services

- SteriPack Group

- Nelipak Healthcare Packaging

- Oliver Healthcare Packaging

- Wipak Group

- Tekni-Plex

- Billerud

- ProAmpac

- Coveris