Spoon In Lid Packaging Market Size and Growth

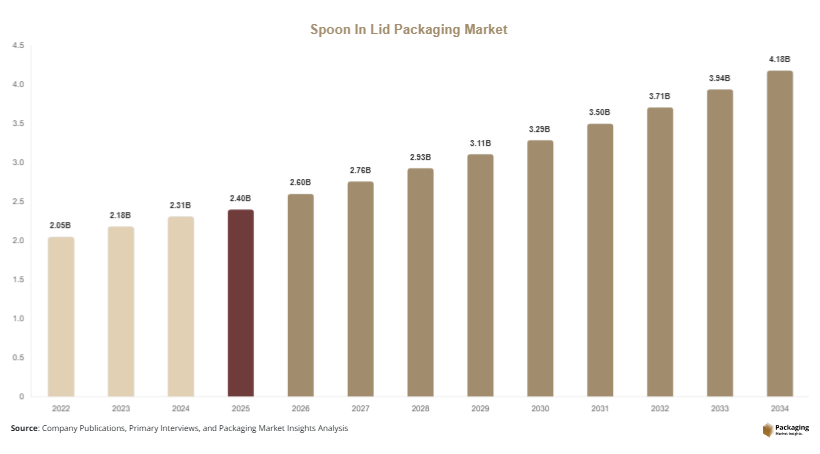

The global spoon in lid packaging market was valued at USD 2.4 billion in 2025 and is projected to reach USD 4.1 billion by 2034, expanding at a CAGR of 6.1% during the forecast period from 2025 to 2034. The market is witnessing stable expansion due to the growing demand for convenient, hygienic, and portable food packaging solutions across dairy products, desserts, ready-to-eat meals, and nutritional products. Spoon in lid packaging integrates disposable cutlery directly into the lid structure, enabling consumers to consume products without requiring external utensils. This packaging design has gained strong popularity in urban retail markets and on-the-go consumption channels.

In 2026, the market is estimated to reach USD 2.6 billion as food manufacturers continue investing in value-added packaging differentiation strategies. Rising consumption of yogurt cups, instant cereals, ice cream products, and snack desserts is contributing significantly to market growth. Foodservice operators and retail brands are increasingly focusing on compact packaging formats that improve convenience while reducing handling complexity during transportation and storage.

Key Highlights

- Asia Pacific dominated the spoon in lid packaging market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.8% during the forecast period.

- Plastic-based spoon integrated lids led the material segment with a 58.4% share.

- Dairy and yogurt applications dominated the end-use segment with a 41.7% market share.

- Injection molded spoon lid systems accounted for the largest type share at 46.8% in 2025 due to superior durability and production scalability.

- The US remained the dominant country market with a size of USD 540 million in 2025 and USD 572 million in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Spoon Integrated Packaging

Sustainability is becoming a major trend in the spoon in lid packaging market as food manufacturers increasingly adopt recyclable and biodegradable packaging materials. Companies are replacing conventional virgin plastics with recyclable polypropylene, PET blends, paper composites, and biodegradable polymers to comply with environmental regulations and corporate sustainability targets. Consumers are showing stronger preference for environmentally responsible packaging, particularly in dairy snacks and single-serve dessert categories.

Several yogurt and dairy brands are introducing lightweight spoon-in-lid systems that reduce total plastic usage while maintaining product integrity. Packaging suppliers are also developing detachable spoon structures that simplify recycling processes. In Europe, food packaging producers are investing in mono-material packaging solutions that improve recyclability across municipal waste streams. Future demand for sustainable integrated packaging is expected to rise further as governments impose stricter restrictions on single-use plastics and encourage circular packaging systems.

Growth of On-the-Go and Single-Serve Food Packaging

The growing popularity of portable food products is significantly influencing the spoon in lid packaging market. Consumers increasingly prefer compact and convenient food packaging formats that support mobility, travel, and workplace consumption. Single-serve yogurt cups, instant breakfast products, puddings, nutritional supplements, and ready-to-eat snacks are increasingly using integrated spoon lids to enhance user convenience.

Foodservice operators and retail chains are expanding grab-and-go product offerings, especially in airports, convenience stores, supermarkets, and vending channels. Manufacturers are designing ergonomic spoon lid systems that improve functionality while maintaining compact packaging dimensions. In Asia Pacific, urban consumers are increasingly purchasing packaged meal replacements and snack products that support busy work schedules. The future impact of this trend is expected to accelerate demand for customizable packaging designs, tamper-evident lids, and lightweight transport-friendly packaging formats across multiple food categories.

Market Drivers

Expansion of Convenience Food Consumption

The rapid expansion of convenience food consumption is a major driver for the spoon in lid packaging market. Urban consumers increasingly demand portable packaging solutions that simplify food consumption during travel, office work, educational activities, and outdoor usage. Integrated spoon lids eliminate the need for separate utensils, improving customer convenience and reducing operational complexity for retailers and foodservice providers.

Dairy products, instant cereals, and dessert snacks are among the leading categories adopting spoon-integrated packaging formats. Food manufacturers are investing heavily in innovative packaging features to improve product differentiation and brand visibility. For example, yogurt brands are launching multi-compartment cups with integrated spoons for fruit-and-granola combinations. The growth of e-commerce grocery delivery services is further supporting demand because integrated packaging reduces the need for additional cutlery distribution during online fulfillment operations.

Increasing Focus on Hygiene and Food Safety

Rising consumer awareness regarding hygiene and food safety is another important growth driver for the market. Spoon in lid packaging provides enhanced sanitation because utensils remain sealed within the packaging structure until product usage. This reduces contamination risks associated with externally packed disposable cutlery.

Food manufacturers are increasingly prioritizing hygienic packaging solutions for dairy products, baby food, healthcare nutrition products, and institutional foodservice packaging. Hospitals, airlines, and educational institutions are adopting sealed spoon-integrated packaging formats to improve cleanliness standards and operational efficiency. Packaging companies are also investing in antimicrobial coating technologies and tamper-evident lid designs that improve consumer trust. As global food safety regulations continue evolving, demand for protected and contamination-resistant packaging formats is expected to expand steadily throughout the forecast period.

Market Restraint

Volatility in Raw Material Prices and Plastic Regulations

One of the major restraints affecting the spoon in lid packaging market is the volatility in raw material prices, particularly polypropylene and PET resins. Packaging manufacturers face increasing cost pressure due to fluctuating crude oil prices, supply chain disruptions, and transportation expenses. Since spoon integrated packaging requires precise molding and durable material performance, resin quality plays a critical role in production consistency.

In addition, growing environmental regulations regarding single-use plastics are creating operational challenges for packaging manufacturers. Several countries are implementing stricter recycling requirements and plastic waste reduction policies, forcing companies to redesign existing packaging systems. Smaller manufacturers often struggle with the investment costs associated with transitioning toward recyclable or biodegradable materials.

For example, food packaging producers in Europe and North America are required to comply with extended producer responsibility regulations and recycled content mandates. These compliance requirements increase operational complexity and product development costs. As sustainability expectations rise, companies that fail to adapt quickly may experience slower adoption rates and reduced competitiveness in environmentally conscious markets.

Market Opportunities

Development of Biodegradable Spoon Lid Solutions

The increasing demand for eco-friendly packaging presents a major opportunity for manufacturers operating in the spoon in lid packaging market. Companies are investing in biodegradable spoon lid systems made from paper composites, PLA materials, and plant-based polymers to address sustainability concerns and regulatory requirements.

Food brands are actively seeking packaging suppliers capable of delivering environmentally compliant solutions without compromising durability or consumer convenience. Biodegradable spoon-integrated packaging is gaining strong interest in premium dairy products, organic food categories, and health-focused snack segments. Packaging companies are also exploring compostable spoon technologies that improve disposal efficiency.

Future opportunities are expected to expand significantly as retailers adopt sustainability procurement standards. Emerging economies are also increasing investment in green packaging infrastructure, creating additional demand for recyclable and biodegradable packaging systems across foodservice and retail applications.

Expansion in Emerging Retail and E-Commerce Markets

Rapid retail modernization and e-commerce growth in developing economies are creating strong opportunities for spoon integrated packaging manufacturers. Countries across Asia Pacific, Latin America, and the Middle East are experiencing increasing demand for packaged convenience foods due to rising disposable incomes and urbanization.

Supermarkets, hypermarkets, and online grocery platforms are expanding their offerings of ready-to-eat snacks, yogurt products, desserts, and nutritional foods that benefit from integrated spoon packaging formats. Food brands are using spoon-in-lid systems to improve product portability and enhance customer experience during online delivery.

Manufacturers also have opportunities to develop customized packaging solutions for airline catering, institutional foodservice, and vending machine applications. Future growth is expected to be supported by rising investment in cold chain logistics, organized retail infrastructure, and automated packaging technologies in emerging consumer markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.4 Billion |

| Market Size in 2026 | USD 2.6 Billion |

| Market Size in 2034 | USD 4.1 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Injection molded spoon lid systems dominated the type segment with a 46.8% share in 2024. These products remain highly preferred due to their structural durability, leak resistance, and large-scale manufacturing efficiency. Injection molding enables manufacturers to create complex spoon-locking mechanisms while maintaining dimensional consistency across high production volumes. Dairy packaging companies extensively use injection molded lids for yogurt cups, nutritional products, and dessert containers because they provide superior consumer convenience and tamper resistance. The technology also supports branding customization through embossed logos and ergonomic spoon designs. Growing demand for compact and portable packaging in retail food applications continues supporting segment dominance across developed and emerging economies.

Thermoformed spoon lid systems are projected to register the fastest CAGR of 6.9% during the forecast period. These products are gaining popularity because they use less material and support lightweight packaging designs. Thermoforming technologies reduce production costs while enabling manufacturers to improve sustainability performance through lower resin consumption. Food companies increasingly prefer thermoformed packaging for snack desserts and low-cost dairy products targeted at high-volume retail channels. Future growth is expected to be driven by increasing adoption of recyclable PET and bio-based materials in thermoformed packaging applications. Advancements in high-speed thermoforming equipment are also expected to improve manufacturing productivity and packaging design flexibility.

By Material

Plastic materials accounted for the largest market share of 58.4% in 2024 due to their durability, moisture resistance, lightweight properties, and cost efficiency. Polypropylene and PET remain widely used because they provide strong structural performance while supporting complex molding designs required for integrated spoon systems. Plastic spoon lids are extensively utilized in yogurt packaging, ice cream products, nutritional foods, and instant snack applications. Food manufacturers prefer plastic packaging because it supports high-volume production and maintains product integrity during transportation and storage. Additionally, advancements in recycled resin technologies are enabling manufacturers to improve sustainability performance while retaining packaging functionality.

Biodegradable and paper-based materials are expected to witness the fastest CAGR of 7.2% during the forecast period. Rising environmental awareness and stricter plastic waste regulations are encouraging manufacturers to develop sustainable spoon integrated packaging alternatives. Companies are increasingly investing in compostable polymers, molded fiber materials, and paper composite technologies that reduce environmental impact. Premium organic food brands are particularly adopting biodegradable spoon lid systems to strengthen sustainable brand positioning. Future demand is expected to increase as retailers implement sustainable packaging procurement standards and consumers prioritize environmentally responsible food packaging products. Innovations in barrier coatings and moisture-resistant paper materials are further improving commercial feasibility across multiple applications.

By End-Use

Dairy and yogurt applications dominated the end-use segment with a 41.7% share in 2024. The segment benefits from strong global demand for single-serve yogurt products, flavored dairy snacks, probiotic drinks, and protein-rich nutritional foods. Spoon integrated packaging is highly preferred in dairy products because it improves portability and eliminates the need for separate disposable utensils. Large dairy manufacturers are increasingly introducing premium packaging formats with attached spoons and multi-compartment designs to enhance consumer convenience. Rising consumption of healthy snack products and breakfast alternatives is further supporting segment growth. Supermarkets and convenience retailers continue expanding shelf space for spoon-integrated dairy packaging solutions.

Ready-to-eat meal packaging is projected to grow at the fastest CAGR of 6.9% during the forecast period. The growth is driven by rising demand for portable meal products among urban consumers and working professionals. Food manufacturers are increasingly launching instant breakfast bowls, snack cereals, and meal replacement products that incorporate spoon lid systems for improved usability. The expansion of online grocery delivery and travel food consumption is further accelerating adoption. Future growth opportunities are expected in airline catering, institutional foodservice, and vending machine distribution channels. Manufacturers are also introducing microwave-compatible spoon integrated packaging formats that improve product versatility across convenience meal applications.

Spoon In Lid Packaging Market Segmentations

By Type

- Injection Molded Spoon Lid Packaging

- Thermoformed Spoon Lid Packaging

- Snap-Fit Spoon Lid Systems

- Peelable Spoon Lid Packaging

By Material

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polystyrene (PS)

- Paper-Based Materials

- Biodegradable Polymers

By End-User

- Dairy & Yogurt Products

- Ready-to-Eat Meals

- Ice Cream & Desserts

- Nutritional & Healthcare Foods

- Snack & Cereal Packaging

Regional Analysis

North America

North America accounted for 24.8% of the spoon in lid packaging market share in 2025 and is projected to grow at a CAGR of 5.7% during the forecast period. The region benefits from strong demand for portable food products, advanced packaging technologies, and high consumption of dairy snacks and ready-to-eat meals. Consumers increasingly prefer convenient packaging solutions that support busy lifestyles and mobile consumption habits. The growth of organized retail chains, vending systems, and online grocery platforms is strengthening demand for spoon integrated packaging across the United States and Canada. Manufacturers are also focusing on recyclable packaging innovations to comply with environmental sustainability initiatives.

The United States remained the dominant country in North America due to strong packaged food consumption and extensive retail distribution networks. One unique driver in the country is the increasing demand for functional dairy snacks and protein-rich meal replacements. Major yogurt brands are launching single-serve products with integrated spoon packaging to improve portability and reduce accessory packaging waste. Airlines and institutional catering services are also expanding adoption of hygienic spoon lid solutions. In addition, automation investments in packaging manufacturing facilities are improving production efficiency and reducing operational costs across the regional packaging industry.

Europe

Europe held a 22.3% share of the spoon in lid packaging market in 2025 and is expected to register a CAGR of 5.5% through 2034. Strong environmental regulations and increasing preference for sustainable food packaging solutions are driving regional market growth. European food manufacturers are investing heavily in recyclable and biodegradable packaging formats to comply with circular economy policies. Demand for portion-controlled dairy products and premium desserts continues to support spoon-integrated packaging adoption across supermarkets and convenience stores. The region also benefits from advanced thermoforming and injection molding technologies that enable lightweight and customizable packaging designs.

Germany dominated the European market due to its strong food processing industry and packaging innovation ecosystem. A key regional growth driver is the rapid expansion of recyclable mono-material packaging solutions. Food packaging manufacturers are collaborating with recycling firms to improve post-consumer waste recovery and material reuse rates. German dairy brands are increasingly introducing eco-friendly spoon integrated yogurt cups using recycled polypropylene materials. Additionally, rising demand for premium convenience foods in urban retail environments is strengthening investment in value-added packaging technologies throughout the region.

Asia Pacific

Asia Pacific dominated the spoon in lid packaging market with a 39.1% share in 2025 and is projected to witness a CAGR of 6.7% during the forecast period. Rapid urbanization, rising disposable incomes, and growing demand for convenience foods are major growth contributors in the region. Expanding supermarket penetration and increasing consumption of dairy snacks, desserts, and instant meals are accelerating demand for spoon integrated packaging solutions. Countries across Asia Pacific are also witnessing rising investment in food packaging automation and flexible manufacturing systems that support large-scale packaging production.

China emerged as the dominant country market due to the rapid expansion of packaged food manufacturing and retail distribution networks. One unique driver in the country is the strong growth of e-commerce grocery delivery services. Food manufacturers are increasingly adopting compact and durable spoon lid packaging formats that improve transportation efficiency and customer convenience. Chinese dairy companies are introducing innovative multi-compartment packaging designs for yogurt and cereal combinations targeted at younger consumers. Rising demand for hygienic food packaging in urban centers is also encouraging investment in advanced sealing and molding technologies.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the global spoon in lid packaging market in 2025 and is projected to grow at a CAGR of 5.9% during the forecast period. Growth is supported by increasing urban food consumption, rising tourism activities, and expanding quick-service restaurant sectors. Food packaging demand is increasing steadily across Gulf countries due to growing reliance on imported packaged foods and convenience meal products. The region is also witnessing gradual adoption of modern retail infrastructure and cold chain logistics systems that improve distribution efficiency for dairy and snack products.

Saudi Arabia remained the dominant market within the region due to strong investments in food processing and retail modernization. A major growth driver is the expansion of convenience-oriented dairy product consumption among younger urban populations. Retailers are increasingly introducing portable yogurt and dessert products packaged with integrated spoons to improve customer convenience. Hospitality and airline catering industries are also contributing to packaging demand as they seek hygienic and space-efficient foodservice packaging formats. Manufacturers are gradually increasing investments in recyclable packaging materials to align with sustainability goals across Gulf markets.

Latin America

Latin America represented 7.0% of the spoon in lid packaging market in 2025 and is forecast to grow at the fastest CAGR of 6.8% through 2034. Rising urbanization, growing supermarket penetration, and expanding packaged dairy product consumption are driving market development across the region. Consumers increasingly prefer affordable and portable food packaging formats for snacks and meal replacement products. Packaging suppliers are also expanding regional manufacturing capabilities to support rising demand from food processing companies and retail chains.

Brazil dominated the Latin American market due to its strong dairy processing industry and growing retail food sector. One unique growth factor is the increasing demand for affordable single-serve dairy snacks among middle-income consumers. Yogurt manufacturers are expanding production of spoon-integrated packaging formats to improve product accessibility in supermarkets and convenience stores. In addition, regional growth in school meal programs and institutional food distribution is encouraging adoption of hygienic portion-controlled packaging systems. Local packaging firms are also investing in lightweight materials and automated production technologies to improve operational efficiency.

Competitive Landscape

The spoon in lid packaging market is moderately consolidated, with global packaging manufacturers competing through material innovation, lightweight product development, sustainable packaging technologies, and customized food packaging solutions. Companies are focusing on improving production efficiency, reducing resin consumption, and enhancing consumer convenience through ergonomic spoon-integrated lid designs. Strategic partnerships with dairy producers, ready-to-eat food manufacturers, and retail brands remain an important growth strategy across major regional markets.

Berry Global Inc. is recognized as one of the leading companies in the market due to its extensive food packaging portfolio, advanced injection molding capabilities, and strong global manufacturing network. The company continues investing in recyclable packaging materials and lightweight lid technologies to strengthen its market position. Berry Global has also expanded its sustainable packaging portfolio by increasing the use of post-consumer recycled content in food packaging applications.

Amcor plc remains another important participant, focusing on sustainable flexible and rigid food packaging solutions. The company is developing recyclable mono-material packaging systems that support circular economy goals while maintaining product durability and hygiene performance. Greiner Packaging International GmbH is strengthening its presence through customized dairy packaging solutions designed for yogurt and dessert manufacturers.

Coveris Holdings S.A. is investing in advanced thermoforming technologies to improve lightweight spoon-lid packaging efficiency. Meanwhile, Huhtamaki Oyj continues expanding its foodservice packaging business with recyclable and fiber-based packaging innovations targeted at sustainable food packaging applications. Companies are also increasing investments in automation, digital printing technologies, and smart packaging features to improve operational competitiveness and product differentiation.

Key Players List

- Berry Global Inc.

- Amcor plc

- Greiner Packaging International GmbH

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Sonoco Products Company

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- Printpack Inc.

- ALPLA Group

- Sealed Air Corporation

- Genpak LLC

- Constantia Flexibles Group GmbH

- Winpak Ltd.

- RPC Group Plc

- Sabert Corporation

- Faerch A/S

- Takween Advanced Industries