Smart Labels Market Size and Growth

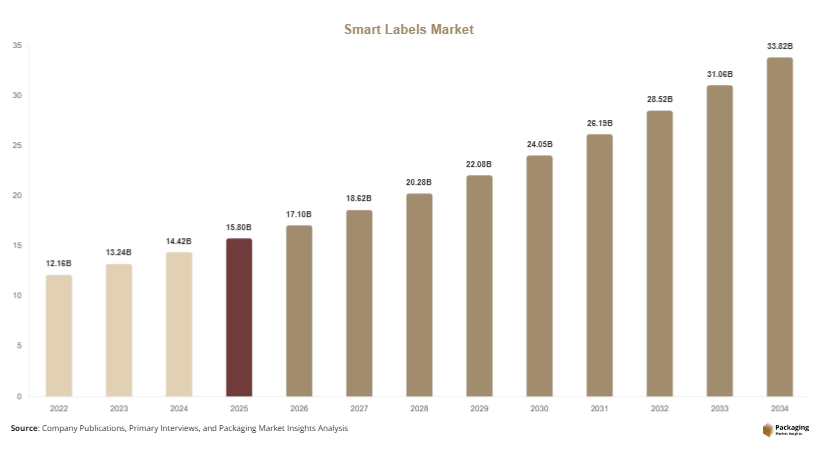

The global smart labels market was valued at USD 15.8 billion in 2025 and is estimated to reach USD 17.1 billion in 2026. The market is projected to attain USD 33.9 billion by 2034, expanding at a CAGR of 8.9% during the forecast period from 2025 to 2034. The market is witnessing strong growth due to rising adoption of intelligent packaging technologies across retail, healthcare, logistics, food & beverages, and industrial sectors. Smart labels integrate technologies such as RFID, NFC, electronic article surveillance, and sensing components to improve inventory tracking, product authentication, consumer engagement, and supply chain transparency.

The increasing demand for real-time inventory visibility has become a major factor supporting market expansion. Retailers and logistics providers continue to deploy RFID-enabled smart labels to reduce inventory losses, improve warehouse automation, and optimize distribution operations. E-commerce growth has also accelerated the use of smart tracking labels for parcel monitoring and product verification. Large retailers are increasingly implementing digital supply chain systems that rely on smart labeling infrastructure to improve operational efficiency and reduce manual scanning errors.

Key Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 9.4%.

- RFID labels led the type segment with a 46.8% share.

- Plastic-based labels dominated with a 58.6% share.

- Retail & logistics applications led the segment with 41.7% share.

- The US remained the dominant country with a market size of USD 4.1 billion in 2025 and USD 4.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Integration of RFID Technology in Retail Operations

Retail companies are increasingly deploying RFID-enabled smart labels to improve inventory accuracy, reduce stock-outs, and streamline warehouse operations. Large supermarket chains and apparel retailers are implementing automated inventory systems that depend on RFID labels for real-time stock visibility. Smart labels are helping retailers manage omnichannel distribution networks more effectively while reducing labor-intensive manual scanning processes. Fashion retailers are using RFID labels to monitor product movement from manufacturing facilities to retail shelves, improving operational transparency and reducing shrinkage rates.

The trend is expected to accelerate as retailers expand automated checkout systems and smart shelf technologies. Companies are also integrating RFID systems with cloud-based analytics platforms to improve forecasting accuracy and demand planning. Future adoption is likely to increase in developing markets as RFID tag costs continue to decline and supply chain digitization expands across mid-sized retailers.

Increasing Adoption of NFC-Based Consumer Engagement Labels

Brands across food, beverages, cosmetics, and healthcare industries are increasingly adopting NFC-enabled smart labels to improve customer interaction and product transparency. Consumers can scan NFC labels using smartphones to access product origin details, authentication data, sustainability information, and promotional content. Beverage manufacturers are using smart labels for interactive marketing campaigns, while pharmaceutical companies are implementing NFC labels to improve medicine verification and patient education.

This trend is expected to reshape brand communication strategies over the next decade. Smart packaging integrated with digital experiences is becoming an important differentiator in premium product categories. Future developments in printed electronics and low-cost sensor integration are expected to expand NFC label adoption across mass-market consumer products. The growing use of connected packaging in e-commerce and direct-to-consumer business models will further strengthen market demand.

Market Drivers

Expansion of Global E-commerce and Logistics Networks

The rapid expansion of e-commerce platforms and global logistics operations continues to drive demand for smart labels. Logistics providers require advanced tracking technologies to manage growing shipment volumes, improve delivery visibility, and reduce package losses. RFID and barcode-enabled smart labels help warehouse operators automate sorting systems and improve operational accuracy. The growth of same-day delivery services has increased the importance of real-time tracking systems across distribution networks.

Major logistics companies are investing heavily in warehouse automation and digital supply chain technologies that rely on smart labeling systems. Retailers are also deploying smart labels to support reverse logistics and return management operations. The increasing adoption of cross-border e-commerce is expected to further strengthen demand for intelligent tracking solutions across international shipping networks.

Growing Need for Product Authentication and Traceability

Counterfeit products continue to create significant challenges for pharmaceutical, electronics, and luxury goods manufacturers. Smart labels provide advanced authentication features that help companies protect brand integrity and comply with regulatory standards. Pharmaceutical companies are increasingly using serialized RFID and NFC labels to monitor drug distribution and prevent counterfeit medicine circulation.

Food manufacturers are also implementing traceability systems to improve supply chain transparency and meet consumer safety expectations. Governments in multiple countries are strengthening regulations related to product tracking and labeling compliance. These developments are encouraging manufacturers to adopt intelligent labeling technologies that improve traceability, quality assurance, and operational visibility across supply chains.

Market Restraint

High Initial Implementation and Integration Costs

The high cost associated with smart label implementation remains a significant challenge for small and medium-sized enterprises. RFID infrastructure, software integration, cloud connectivity systems, and sensor-enabled labels require substantial capital investment. Many smaller manufacturers and retailers continue to rely on conventional barcode labeling systems due to budget limitations and operational complexity concerns.

The integration of smart labeling systems into existing supply chain infrastructure can also create technical challenges. Companies often require specialized software platforms, employee training programs, and system upgrades to support intelligent packaging operations. In emerging economies, limited digital infrastructure and lower automation adoption rates further restrict market penetration. For example, small-scale food manufacturers and regional retailers in developing markets often face difficulties implementing RFID tracking systems due to high deployment costs and limited technical expertise. These factors may slow adoption rates in cost-sensitive industries during the forecast period.

Market Opportunities

Growth of Smart Healthcare Packaging Applications

Healthcare packaging applications present major growth opportunities for the smart labels market. Pharmaceutical companies are increasingly deploying temperature-sensitive labels, RFID-enabled drug tracking systems, and NFC authentication technologies to improve supply chain monitoring and patient safety. Smart labels help healthcare providers monitor medicine storage conditions and reduce the risk of counterfeit drug distribution.

The increasing global demand for biologics, vaccines, and specialty medicines is expected to accelerate adoption of advanced smart labeling systems. Hospitals and pharmacies are also integrating RFID tracking solutions to improve inventory management and reduce medication errors. Future developments in printed biosensors and connected medical packaging technologies may further expand market opportunities across healthcare supply chains.

Expansion of Sustainable Smart Label Technologies

The development of recyclable and biodegradable smart labels is creating new growth opportunities for packaging manufacturers. Companies are investing in paper-based RFID labels, solvent-free adhesives, and low-energy printed electronics to align with sustainability targets. Retailers and consumer goods manufacturers are increasingly demanding eco-friendly intelligent packaging solutions that support circular economy initiatives.

Future opportunities are expected to emerge in reusable packaging systems and sustainable logistics applications. Smart labels integrated with reusable containers can improve asset tracking and reduce packaging waste. The growing focus on carbon footprint reduction and environmental transparency is likely to support long-term adoption of sustainable smart labeling technologies across multiple industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Size in 2026 | USD 17.1 Billion |

| Market Size in 2034 | USD 33.9 Billion |

| CAGR | 8.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

RFID labels dominated the type segment with a 46.8% market share in 2024 due to their widespread adoption across retail, logistics, healthcare, and industrial sectors. RFID smart labels improve inventory visibility, automate warehouse management, and reduce manual scanning errors. Large retailers are increasingly deploying RFID-enabled systems to improve operational efficiency and optimize supply chain performance. Apparel companies and consumer electronics manufacturers continue to use RFID labels for inventory tracking and anti-theft applications. The technology also supports automated checkout systems and smart shelving infrastructure in retail stores. Logistics providers are integrating RFID labels into shipping operations to improve parcel tracking and delivery visibility. The declining cost of RFID chips and increasing cloud integration capabilities continue to strengthen adoption across large-scale commercial operations.

Sensing labels are projected to register the fastest CAGR of 10.2% during the forecast period due to growing demand for temperature monitoring, freshness detection, and environmental sensing applications. Pharmaceutical and food manufacturers are increasingly deploying sensor-enabled smart labels to monitor storage conditions and improve product quality assurance. These labels help companies reduce spoilage risks and strengthen regulatory compliance in temperature-sensitive supply chains. Future growth is expected to be supported by advancements in printed electronics and flexible sensor technologies. Smart sensing labels are also gaining traction in cold chain logistics, vaccine transportation, and healthcare packaging. The increasing focus on food safety and real-time monitoring capabilities is expected to further accelerate market adoption.

By Material

Plastic-based smart labels accounted for 58.6% of the market share in 2024 due to their durability, flexibility, and compatibility with RFID and NFC technologies. Plastic substrates provide strong moisture resistance and extended product life, making them suitable for industrial, logistics, and retail applications. Packaging manufacturers continue to use polyethylene and polypropylene materials for smart label production because of their ability to support embedded electronic components and printed circuits. Retail companies widely deploy plastic-based RFID labels in inventory management systems due to their reliability in high-volume operations. The increasing use of smart labels in shipping, industrial packaging, and consumer electronics also contributes to the dominance of plastic materials across the market.

Paper-based smart labels are expected to grow at the fastest CAGR of 9.1% during the forecast period due to increasing sustainability initiatives and regulatory pressure to reduce plastic waste. Manufacturers are investing in recyclable RFID labels and biodegradable smart packaging technologies to align with environmental goals. Paper-based labels are gaining popularity across food, beverages, cosmetics, and healthcare packaging applications. Advances in conductive inks and printed electronics are enabling the development of sustainable intelligent labeling solutions with improved performance capabilities. Retailers and consumer goods companies are increasingly adopting paper-based smart labels to strengthen environmental branding strategies and reduce packaging-related carbon emissions.

By End-Use

Retail & logistics dominated the end-use segment with a 41.7% market share in 2024 due to increasing demand for inventory automation, warehouse optimization, and shipment tracking technologies. E-commerce growth has accelerated the adoption of RFID-enabled smart labels across distribution centers and retail supply chains. Smart labels help logistics companies improve parcel visibility, reduce delivery errors, and optimize operational efficiency. Retailers are increasingly integrating intelligent labeling systems with cloud-based analytics platforms to improve demand forecasting and inventory planning. Large supermarket chains and apparel retailers continue to deploy RFID smart shelves and automated checkout systems to enhance customer experience and operational productivity. The ongoing expansion of omnichannel retailing is expected to maintain strong demand for intelligent packaging technologies.

Healthcare is projected to register the fastest CAGR of 10.4% during the forecast period due to increasing pharmaceutical serialization requirements and growing demand for temperature-sensitive drug monitoring systems. Smart labels are increasingly used in vaccine distribution, biologics transportation, and medical device tracking applications. Hospitals and pharmacies are adopting RFID-enabled inventory systems to improve medication management and reduce supply chain inefficiencies. NFC-enabled labels are also gaining popularity in patient engagement and medicine authentication applications. Future growth is expected to be driven by the expansion of connected healthcare infrastructure and increasing investments in digital pharmaceutical supply chain systems. The growing importance of patient safety and counterfeit prevention will further strengthen adoption across healthcare packaging operations.

Smart Labels Market Segmentations

By Type

- RFID Labels

- Electronic Article Surveillance Labels

- Sensing Labels

- NFC Smart Labels

- Dynamic Display Labels

By Material

- Plastic

- Paper

- Metal Foil

- Polymer Films

By End-User

- Food & Beverage

- Healthcare & Pharmaceuticals

- Retail & E-commerce

- Logistics & Transportation

- Consumer Electronics

- Automotive

Regional Analysis

North America

North America accounted for 29.8% of the global smart labels market share in 2025 and is expected to grow at a CAGR of 8.4% during the forecast period. The region benefits from strong adoption of RFID technologies across retail, healthcare, and logistics sectors. The presence of advanced supply chain infrastructure and large-scale e-commerce networks continues to support market growth. Retailers across the United States and Canada are increasingly deploying smart shelf systems, automated checkout technologies, and intelligent inventory tracking platforms. Pharmaceutical serialization regulations and food traceability requirements are also driving regional demand for smart labeling solutions. Investments in Industry 4.0 automation systems are further strengthening adoption across warehousing and manufacturing industries.

The United States remained the dominant country in North America due to widespread implementation of RFID tracking technologies across retail and healthcare industries. Major retailers continue to expand digital inventory management systems supported by intelligent labeling infrastructure. The country is also witnessing rising demand for NFC-enabled packaging used in premium beverages, cosmetics, and consumer electronics. Pharmaceutical companies are adopting temperature-monitoring smart labels to improve cold chain management for vaccines and biologic drugs. The expansion of omnichannel retailing and automated logistics operations is expected to create additional growth opportunities across the U.S. smart labels industry.

Europe

Europe represented 24.6% of the global market share in 2025 and is projected to expand at a CAGR of 8.1% through 2034. The region continues to benefit from strict product traceability regulations and increasing adoption of sustainable packaging technologies. Food safety standards and pharmaceutical serialization requirements are encouraging manufacturers to integrate intelligent labeling systems into packaging operations. Retailers across Germany, France, and the United Kingdom are increasingly investing in digital inventory management systems to improve supply chain efficiency and reduce operational losses. The regional focus on circular economy initiatives is also encouraging development of recyclable smart label materials and environmentally responsible packaging technologies.

Germany dominated the European market due to its strong industrial manufacturing base and advanced logistics infrastructure. Automotive, pharmaceutical, and industrial equipment manufacturers are increasingly using RFID-enabled tracking systems to improve warehouse visibility and supply chain coordination. German packaging companies are also investing in recyclable smart labels and low-energy printed electronics to support sustainability targets. Food retailers across the country are implementing intelligent labeling systems to improve product traceability and strengthen consumer confidence. Growing investments in automated industrial facilities and smart manufacturing technologies are expected to further accelerate demand for advanced labeling solutions.

Asia Pacific

Asia Pacific held the largest market share of 39.1% in 2025 and is expected to register a CAGR of 9.3% during the forecast period. The region is experiencing rapid growth due to expanding manufacturing activities, increasing retail automation, and rising e-commerce penetration. China, Japan, South Korea, and India are investing heavily in digital logistics infrastructure and intelligent supply chain technologies. Consumer electronics manufacturers and apparel exporters are increasingly using RFID smart labels to improve inventory visibility and export management efficiency. The growing middle-class population and rising packaged food consumption are also contributing to strong market demand across regional retail sectors.

China remained the leading country in Asia Pacific due to large-scale manufacturing output and rapid adoption of warehouse automation technologies. Chinese e-commerce companies continue to expand smart logistics operations supported by RFID-enabled parcel tracking systems. The country is also witnessing increased deployment of NFC labels in premium consumer goods and food packaging applications. Government investments in industrial digitization and smart factory development are strengthening demand for intelligent labeling solutions across manufacturing industries. In addition, domestic packaging manufacturers are developing lower-cost RFID labels to support wider adoption among small and mid-sized enterprises.

Middle East & Africa

The Middle East & Africa region accounted for 3.9% of the global smart labels market share in 2025 and is projected to grow at a CAGR of 7.5% through 2034. The market is gradually expanding due to rising investments in retail modernization, pharmaceutical manufacturing, and logistics infrastructure development. Gulf countries are increasingly implementing smart warehouse technologies to support growing e-commerce and retail sectors. The adoption of intelligent packaging solutions is also increasing in food exports and cold chain logistics operations. Governments across the region are investing in digital transformation initiatives aimed at improving industrial efficiency and supply chain transparency.

The United Arab Emirates dominated the regional market due to rapid expansion of logistics hubs and retail distribution networks. Large-scale warehousing facilities in Dubai and Abu Dhabi are increasingly integrating RFID tracking systems to improve shipment management and reduce operational delays. Retailers in the UAE are also adopting NFC-enabled packaging to improve customer engagement and product authentication. Growth in pharmaceutical imports and temperature-sensitive healthcare products is further supporting demand for smart labeling technologies. The continued expansion of regional trade and logistics activities is expected to strengthen long-term market growth.

Latin America

Latin America represented 2.6% of the global market share in 2025 and is anticipated to register the fastest CAGR of 9.4% during the forecast period. The region is benefiting from increasing investments in retail digitization, food exports, and pharmaceutical supply chain modernization. Brazil, Mexico, and Chile are expanding adoption of RFID technologies in logistics and retail operations to improve inventory management efficiency. The growing popularity of e-commerce platforms is also creating demand for intelligent parcel tracking solutions. Food exporters are increasingly using smart labels to improve traceability and comply with international export standards.

Brazil emerged as the dominant country in Latin America due to the expansion of organized retail networks and food processing industries. Retail chains are increasingly implementing RFID systems to improve stock visibility and warehouse automation. Pharmaceutical companies in Brazil are also adopting serialization technologies supported by smart labels to comply with product tracking regulations. The country is witnessing increased investment in digital logistics infrastructure aimed at supporting growing online retail activity. Rising exports of processed food and agricultural products are expected to further strengthen smart label adoption across the Brazilian packaging industry.

Competitive Landscape

The smart labels market is highly competitive, with companies focusing on RFID innovation, printed electronics development, and sustainable intelligent packaging technologies. Avery Dennison Corporation remains the market leader due to its extensive RFID product portfolio, strong global distribution network, and continuous investment in smart packaging innovation. The company continues to expand its RFID manufacturing capacity to meet growing retail and logistics demand.

CCL Industries and Zebra Technologies are strengthening their market presence through strategic acquisitions and digital labeling solutions for industrial applications. Checkpoint Systems is expanding RFID-based retail inventory solutions aimed at improving loss prevention and warehouse automation. SATO Holdings Corporation continues to invest in healthcare labeling technologies and smart traceability systems.

Companies are increasingly focusing on recyclable smart labels, cloud-integrated tracking systems, and NFC-enabled consumer engagement technologies. Strategic partnerships between packaging companies and software providers are becoming more common as demand for connected packaging solutions continues to rise. The market is also witnessing increased investment in low-cost printed electronics and flexible sensing technologies to support broader commercial adoption.

Key Players List

- Avery Dennison Corporation

- CCL Industries Inc.

- Zebra Technologies Corporation

- Checkpoint Systems Inc.

- SATO Holdings Corporation

- Honeywell International Inc.

- Smartrac Technology GmbH

- Invengo Information Technology Co., Ltd.

- Alien Technology LLC

- Thin Film Electronics ASA

- Multi-Color Corporation

- Identiv Inc.

- William Frick & Company

- Jiangsu Smart Label Technology Co., Ltd.

- Graphic Label Inc.