Single Use Glass Packaging Market Size and Growth

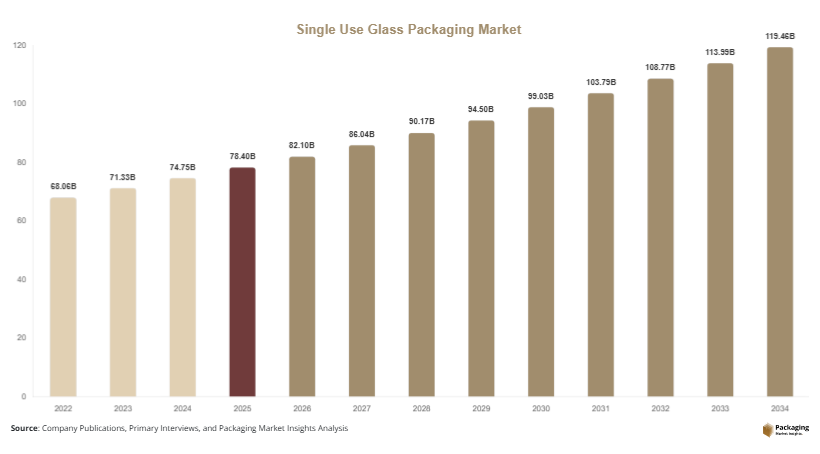

The global single use glass packaging market size was valued at approximately USD 78.4 billion in 2025 and is projected to reach USD 82.1 billion in 2026, reflecting consistent consumption across global end-use industries. Over the forecast period from 2025 to 2034, the market is expected to grow at a CAGR of 4.8%, reaching nearly USD 124.6 billion by 2034. This growth is supported by increasing demand for safe packaging formats, premium product positioning, and expanding beverage consumption worldwide. The single use glass packaging market is witnessing steady expansion as industries continue to rely on inert, hygienic, and premium packaging solutions for beverages, pharmaceuticals, and food applications.

One of the primary growth factors is the rising demand for bottled beverages, particularly in urban and semi-urban regions. Carbonated drinks, juices, alcoholic beverages, and mineral water continue to be packaged in single-use glass due to its ability to preserve taste and prevent chemical interaction. This makes it a preferred material in premium beverage segments.

Key Highlights:

- The market size reached USD 78.4 billion in 2025, supported by strong consumption across beverage, pharmaceutical, and food packaging applications. Demand remains steady due to the widespread use of glass in premium and safe packaging formats.

- It is projected to reach USD 124.6 billion by 2034, driven by consistent growth in end-use industries and rising preference for glass-based packaging solutions. Expansion in both developed and emerging regions supports this long-term outlook.

- The market is expected to register a CAGR of 4.8% during 2025–2034, indicating stable and sustained growth. This reflects balanced demand across industrial, commercial, and consumer packaging segments.

- Strong demand from beverage, pharmaceutical, and food industries continues to be a key growth driver. These sectors rely on glass packaging for product safety, preservation, and premium positioning.

- There is rising adoption of glass packaging in premium product categories, especially in alcoholic beverages, cosmetics, and specialty foods. This is driven by brand differentiation and consumer preference for high-quality packaging.

- High chemical stability and recyclability of glass materials further support market growth. These properties make glass a preferred choice in applications requiring purity, safety, and environmental compatibility.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Use of Lightweight Glass Manufacturing Technologies

A major trend in the single use glass packaging market is the adoption of lightweight glass production technologies. Manufacturers are focusing on reducing the thickness of glass bottles and containers without compromising structural integrity. This helps lower transportation costs and reduces carbon emissions during logistics. Lightweight glass is increasingly used in beverage packaging, particularly in wine, beer, and bottled water segments. Technological improvements in glass molding and strengthening processes have enabled manufacturers to produce thinner yet durable packaging solutions. This trend is also aligned with sustainability goals, as reduced material usage contributes to lower environmental impact.

Expansion of Premium Branding Through Decorative Glass Packaging

Another key trend is the growing use of decorative and customized glass packaging for premium branding. Companies are investing in embossed designs, colored glass, and unique bottle shapes to enhance brand identity and shelf appeal. This is particularly prominent in the alcoholic beverage and cosmetic industries, where packaging plays a critical role in consumer purchasing decisions. Glass packaging is increasingly being used as a marketing tool to differentiate products in competitive retail environments. Advances in printing and surface treatment technologies are further enabling high-quality customization at scale.

Market Drivers

Strong Demand from Beverage Industry

The beverage industry is a major driver for the single use glass packaging market. Glass bottles are widely used for alcoholic beverages, soft drinks, juices, and mineral water due to their ability to preserve flavor and ensure product purity. Consumers often associate glass packaging with higher quality and better taste retention compared to plastic alternatives. Rising consumption of premium alcoholic beverages and craft drinks is further supporting demand. Urbanization and increasing disposable income levels are also contributing to higher beverage consumption, strengthening the overall market outlook.

Growth in Pharmaceutical Packaging Applications

The pharmaceutical sector is another key driver of market growth. Glass is extensively used in the packaging of injectable drugs, vaccines, and laboratory chemicals due to its chemical inertness and high resistance to contamination. The global rise in chronic diseases and increasing demand for biologics have significantly expanded the need for safe and sterile packaging solutions. Glass vials and ampoules are preferred in critical medical applications where product stability is essential. This ongoing expansion of healthcare infrastructure globally continues to support market growth.

Market Restraint

High Fragility and Transportation Costs

One of the major restraints in the single use glass packaging market is the fragility of glass materials, which increases the risk of breakage during transportation and handling. This leads to higher logistics costs and requires additional protective packaging, increasing overall operational expenses.

For example, beverage manufacturers often need to invest in reinforced cartons and cushioning materials to prevent damage during shipping. This increases packaging complexity and cost, especially for long-distance transportation. Additionally, the heavier weight of glass compared to alternatives such as plastic or aluminum contributes to higher fuel consumption and logistics expenses. These factors limit adoption in cost-sensitive markets and create challenges for manufacturers operating at large scale.

Market Opportunities

Growth in Craft Beverage and Specialty Food Segments

The expansion of craft beverages and specialty food products presents a significant opportunity for the single use glass packaging market. Small breweries, wineries, and artisanal food producers often prefer glass packaging to enhance product authenticity and premium appeal. Glass bottles help differentiate products in a crowded marketplace and align with consumer preferences for natural and high-quality goods. Increasing consumer interest in craft beer, organic juices, and specialty sauces is expected to drive demand. Additionally, regional brands are using glass packaging to strengthen brand identity and build customer loyalty.

Innovation in Smart Glass Packaging Solutions

Technological advancements are creating opportunities in smart glass packaging solutions. Manufacturers are integrating features such as QR codes, NFC tags, and digital labeling on glass containers to enhance consumer engagement and traceability. These innovations are particularly useful in pharmaceuticals and premium beverages, where product authentication and supply chain tracking are important. Smart packaging also enables brands to provide interactive consumer experiences, such as product information access and promotional content. This trend is expected to create new growth avenues in the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.4 Billion |

| Market Size in 2026 | USD 82.1 Billion |

| Market Size in 2034 | USD 124.6 Billion |

| CAGR | 4.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Bottles dominated the market in 2024, accounting for approximately 55% share of the global single use glass packaging market. Glass bottles are extensively used in beverages such as beer, wine, soft drinks, and juices due to their superior ability to preserve taste, maintain carbonation, and prevent chemical interaction. Their strong brand positioning and premium appearance further enhance adoption across global markets. Additionally, pharmaceutical companies rely heavily on glass bottles for syrups and liquid medicines, strengthening this segment’s dominance across multiple end-use industries.

Vials & ampoules are expected to be the fastest-growing subsegment, expanding at a CAGR of 5.6% during 2025–2034. Growth is driven by rising demand in the pharmaceutical and healthcare sector, particularly for injectable drugs, vaccines, and biologics. These formats provide high sterility, chemical stability, and contamination resistance, making them essential in critical healthcare applications. Increasing global vaccine production and expansion of biopharmaceutical manufacturing are further accelerating demand for glass-based medical packaging solutions.

By Application

Beverage packaging dominated the application segment in 2024 with approximately 62% share. Glass packaging is widely used in alcoholic beverages such as beer, wine, and spirits, as well as non-alcoholic drinks including juices and mineral water. The ability of glass to preserve flavor integrity and support premium branding continues to drive its dominance in this segment. Consumer preference for high-quality packaging further strengthens adoption across both mass and premium beverage categories.

Pharmaceutical packaging is projected to be the fastest-growing application segment, registering a CAGR of 5.4% during the forecast period. Growth is driven by rising demand for injectable drugs, biologics, and sterile medications. Glass packaging is preferred in this segment due to its non-reactive nature and ability to maintain drug stability over time. Expanding healthcare infrastructure and increasing global focus on advanced drug delivery systems are further supporting segment growth.

By End-Use Industry

The food and beverage industry dominated in 2024 with approximately 58% share of the global market. Glass packaging is widely used in beverages, sauces, spreads, and processed food products due to its safety, hygiene, and premium appeal. Its ability to maintain product freshness and enhance brand perception makes it a preferred packaging choice across both retail and commercial channels.

The healthcare and pharmaceuticals industry is expected to be the fastest-growing end-use segment, expanding at a CAGR of 5.7% during 2025–2034. This growth is supported by increasing demand for sterile packaging solutions for injectable drugs, vaccines, and laboratory products. Glass packaging ensures chemical stability and prevents contamination, making it highly suitable for sensitive medical applications in a rapidly expanding global healthcare sector.

Single Use Glass Packaging Market Segmentations

By Product Type

- Bottles

- Jars

- Vials & Ampoules

- Containers

By Application

- Beverage Packaging

- Pharmaceutical Packaging

- Food Packaging

- Cosmetics Packaging

By End-Use Industry

- Food & Beverage

- Healthcare & Pharmaceuticals

- Cosmetics & Personal Care

- Industrial Applications

Regional Analysis

North America

North America accounted for approximately 25% market share in 2025, with the region projected to grow at a CAGR of 4.3% during 2025–2034. The market is supported by strong demand from beverage bottling, pharmaceutical packaging, and premium food applications. High consumer preference for packaged drinks and increasing consumption of craft beverages continue to support glass packaging adoption across the region.

The United States dominates the North American market due to its large beverage industry and established glass manufacturing infrastructure. A key growth factor is the rising demand for premium alcoholic beverages, including craft beer and specialty spirits, which heavily rely on glass bottles for branding, taste preservation, and product differentiation in competitive retail environments.

Europe

Europe held around 30% market share in 2025, with a projected CAGR of 4.5% during the forecast period. The region benefits from strong environmental awareness, well-established glass recycling systems, and a mature beverage industry. Glass packaging remains a preferred choice in food and beverage applications due to regulatory support and consumer preference for sustainable materials.

Germany leads the European market due to its advanced glass production facilities and strong industrial base. A key growth factor is the high consumption of wine and beer, where glass bottles remain the standard packaging format. Additionally, stringent packaging quality regulations further support demand for durable and safe glass packaging solutions.

Asia Pacific

Asia Pacific accounted for approximately 28% market share in 2025, with the highest regional CAGR of 5.6%. Rapid urbanization, rising disposable income, and increasing consumption of packaged beverages are key factors driving market expansion. The region also benefits from expanding pharmaceutical manufacturing and export activities.

China dominates the Asia Pacific market due to its large-scale beverage production and growing healthcare sector. A key growth factor is the increasing preference for premium packaged drinks among urban consumers, along with expanding retail distribution networks that favor glass packaging for brand positioning and product quality perception.

Middle East & Africa

The Middle East & Africa region held approximately 9% market share in 2025, with a projected CAGR of 4.2%. Market growth is driven by rising beverage imports, expanding hospitality sectors, and increasing urban population. Glass packaging is widely used in hotels, restaurants, and retail beverage distribution channels.

Saudi Arabia leads the regional market due to strong growth in tourism and hospitality infrastructure. A key growth factor is increasing demand for packaged beverages in hotels, restaurants, and airlines, where glass packaging is preferred for premium presentation and product safety standards.

Latin America

Latin America accounted for nearly 8% market share in 2025, with a projected CAGR of 4.6%. Growth is supported by expanding beverage production, particularly in beer and soft drinks, along with rising food processing activities. Economic development and urbanization are also contributing to increased packaged product consumption.

Brazil dominates the region due to its strong alcoholic beverage industry and large consumer base. A key growth factor is the high consumption of bottled beer and carbonated drinks, where glass packaging is widely used to maintain product taste and support premium branding strategies.

Competitive Landscape

The single use glass packaging market is moderately consolidated, with key players focusing on production efficiency, lightweight glass innovation, and sustainability initiatives. Companies are investing in advanced furnace technologies and energy-efficient manufacturing processes.

O-I Glass, Inc. is a leading player in the market, known for its global glass bottle production capabilities. The company has recently expanded its lightweight glass manufacturing capacity to support beverage industry demand. Other players are focusing on automation and recycling integration to improve efficiency.

Key Players List

- O-I Glass, Inc.

- Ardagh Group S.A.

- Verallia

- Vetropack Holding AG

- Sisecam Group

- Nihon Yamamura Glass Co.

- Piramal Glass

- Saverglass

- Stoelzle Glass Group

- Bormioli Rocco

- Anchor Glass Container Corporation

- Consol Glass

- Vidrala S.A.

- Rockwood Glass

- Heinz-Glas GmbH