Shrink And Stretch Sleeve Labels Market Size and Growth

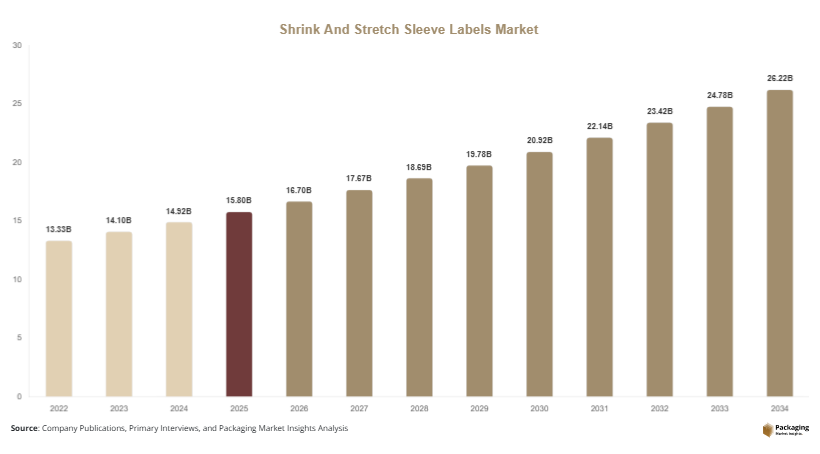

The global shrink and stretch sleeve labels market was valued at approximately USD 15.8 billion in 2025 and is estimated to reach USD 16.7 billion in 2026. The market is projected to expand at a CAGR of 5.8% from 2025 to 2034, reaching nearly USD 27.6 billion by the end of the forecast period. Demand for high-impact product packaging, growing beverage consumption, and rapid expansion of organized retail channels are contributing to sustained market growth across both developed and emerging economies.

Shrink and stretch sleeve labels are widely used across food, beverage, healthcare, cosmetics, personal care, and household product packaging because they provide 360-degree branding visibility and support complex container shapes. Manufacturers are increasingly adopting sleeve labeling solutions to improve shelf differentiation while also enabling tamper evidence and multilingual branding. Growth in flexible packaging formats and the expansion of premium packaging strategies are also influencing demand across several industries.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Shrink sleeve labels led the type segment with a 63.7% share.

- PETG material dominated with a 34.8% share.

- Food and beverage applications led the segment with 48.5% share.

- The US remained the dominant country in North America with a market size of USD 2.9 billion in 2025 and USD 3.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Adoption of Sustainable Sleeve Label Materials

Sustainability initiatives are significantly reshaping the shrink and stretch sleeve labels market. Packaging manufacturers are increasingly introducing recyclable shrink films, floatable polyolefin sleeves, and downgauged label materials to meet regulatory standards and corporate sustainability targets. Many beverage companies are redesigning packaging structures to improve recyclability, especially in North America and Europe where circular economy policies are becoming stricter. Traditional PVC-based shrink sleeves are gradually being replaced with PETG and polyolefin materials that are easier to recycle and produce lower environmental impact.

Several multinational beverage and personal care companies have already shifted toward eco-friendly sleeve solutions for bottled water, detergents, and cosmetic products. Packaging suppliers are also investing in wash-off inks and perforation technologies that simplify recycling processes. Over the next decade, sustainability-focused innovations are expected to influence purchasing decisions across the packaging value chain. This trend is likely to encourage additional investments in bio-based films, lightweight labeling systems, and low-energy shrink tunnel technologies.

Growth of Digital Printing and Custom Packaging

Digital printing is becoming a major trend in the shrink and stretch sleeve labels market due to increasing demand for customization and shorter production cycles. Brands are using digital sleeve printing to create seasonal packaging, regional marketing campaigns, and limited-edition products without requiring large-scale inventory investments. This trend is particularly visible in the beverage, nutraceutical, and cosmetics industries where product differentiation plays a central role in consumer engagement.

The adoption of high-speed digital presses is enabling packaging converters to produce vibrant graphics with reduced setup time and improved flexibility. Companies are also using variable data printing to support traceability, QR-code-based marketing, and smart packaging initiatives. For example, energy drink manufacturers are increasingly introducing localized promotional campaigns through digitally printed shrink sleeves. In the future, advancements in ink technologies and automation systems are expected to reduce production costs and improve adoption among small and medium-sized packaging companies.

Market Drivers

Rising Demand for Premium Packaging in Beverage Applications

The rapid growth of packaged beverages is a major driver for the shrink and stretch sleeve labels market. Beverage manufacturers are increasingly focusing on shelf appeal and brand visibility to compete in highly saturated retail environments. Shrink sleeve labels provide full-body decoration and support complex bottle designs, making them suitable for carbonated drinks, juices, sports beverages, flavored milk, and bottled water products.

In emerging economies, rising disposable income and urban retail expansion are increasing consumption of packaged beverages. Manufacturers are launching premium product variants with visually attractive packaging to strengthen brand recognition. For example, several beverage producers in Asia Pacific have adopted high-gloss shrink sleeves with metallic finishes to improve product differentiation. The ability of sleeve labels to provide tamper evidence and moisture resistance also supports their growing use in refrigerated beverage packaging. Continued growth in ready-to-drink beverages and functional drinks is expected to sustain demand over the forecast period.

Expansion of Organized Retail and E-Commerce Packaging

The expansion of supermarkets, convenience stores, and e-commerce channels is contributing to higher demand for advanced packaging solutions, including shrink and stretch sleeve labels. Organized retail environments require products with strong visual impact and clear branding to attract consumer attention. Sleeve labels allow companies to maximize branding space while maintaining packaging durability during transportation and storage.

E-commerce growth is also influencing packaging design strategies because products must maintain visual quality throughout shipping and handling processes. Sleeve labels provide abrasion resistance and protect printed information from moisture and environmental exposure. Household products, personal care items, and nutritional supplements increasingly use sleeve labeling to improve brand recognition in digital and physical retail channels. Packaging converters are responding by developing high-performance films and faster application technologies that support large-scale production. This retail transformation is expected to continue supporting market expansion across developing economies.

Market Restraint

Volatility in Raw Material Prices and Recycling Challenges

Fluctuations in raw material prices remain a significant restraint for the shrink and stretch sleeve labels market. Sleeve labels are primarily manufactured using petroleum-based materials such as PVC, PETG, OPS, and polyolefin films. Changes in crude oil prices directly influence production costs, creating pricing pressure for label manufacturers and packaging converters. Small and medium-sized companies often face difficulty maintaining profit margins during periods of raw material inflation.

Recycling challenges also create operational and regulatory concerns. Some shrink sleeve materials interfere with PET bottle recycling systems because labels may not separate efficiently during processing. Regulatory agencies in Europe and North America are increasing scrutiny on packaging waste, encouraging companies to redesign labeling structures and adopt recyclable materials. However, transitioning to sustainable materials often requires additional investments in machinery, inks, and processing technologies.

For example, beverage manufacturers using traditional PVC shrink sleeves may need to upgrade equipment to support polyolefin-based alternatives. These conversion costs can delay adoption among cost-sensitive manufacturers. In addition, inconsistent recycling infrastructure in developing economies limits the large-scale collection and recovery of sleeve-labeled packaging waste. These challenges may slow market penetration in certain regions during the forecast period.

Market Opportunities

Increasing Adoption in Pharmaceutical and Healthcare Packaging

The healthcare and pharmaceutical industries present strong growth opportunities for the shrink and stretch sleeve labels market. Pharmaceutical manufacturers require packaging solutions that provide durability, product authentication, and tamper evidence. Sleeve labels support these requirements while also enabling detailed product information and multilingual instructions. Growing pharmaceutical production in India, China, and Southeast Asia is expected to generate additional demand for advanced labeling technologies.

Healthcare packaging companies are increasingly integrating serialization codes, anti-counterfeit features, and track-and-trace systems into sleeve labels. These technologies improve supply chain transparency and support regulatory compliance. The rise in over-the-counter healthcare products and nutritional supplements is also expanding packaging requirements. Future opportunities are likely to emerge from smart labeling technologies that integrate QR codes, NFC tags, and temperature-sensitive indicators for sensitive medical products.

Expansion of Sustainable Packaging Solutions in Emerging Economies

Emerging economies are creating significant opportunities for sustainable sleeve labeling solutions. Governments in countries such as India, Brazil, Indonesia, and South Africa are strengthening regulations related to plastic waste reduction and recyclable packaging materials. This regulatory shift is encouraging consumer goods manufacturers to invest in recyclable and lightweight sleeve labels.

Packaging suppliers are introducing downgauged films and recyclable polyolefin sleeves to meet these changing market requirements. Food and beverage companies in emerging economies are increasingly adopting sustainable packaging to strengthen brand image and align with export standards. In addition, rising investments in modern recycling infrastructure are expected to improve recovery rates for labeled packaging materials. Over the long term, demand for environmentally compatible sleeve labeling systems is likely to accelerate among regional manufacturers seeking cost-effective sustainability strategies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Size in 2026 | USD 16.7 Billion |

| Market Size in 2034 | USD 27.6 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Shrink sleeve labels dominated the type segment and accounted for approximately 63.7% of the global market share in 2024. Their dominance is mainly attributed to superior graphic coverage, high compatibility with complex container shapes, and strong demand from beverage packaging applications. Shrink sleeves provide 360-degree branding, which improves shelf visibility and supports premium packaging strategies across carbonated drinks, bottled water, dairy beverages, and personal care products. Manufacturers also prefer shrink sleeves because they offer tamper evidence and moisture resistance, making them suitable for refrigerated products. Major beverage companies continue to adopt high-definition shrink sleeves with metallic finishes and transparent effects to strengthen brand identity. Packaging converters are increasingly investing in automated shrink tunnel systems and high-speed application equipment to improve production efficiency and support rising demand from large-scale consumer goods manufacturers.

Stretch sleeve labels are projected to register the fastest CAGR of 6.1% during the forecast period. Growth is being driven by rising demand for environmentally compatible labeling solutions that reduce energy consumption during application. Unlike shrink sleeves, stretch sleeves do not require heat tunnels, making them attractive for manufacturers seeking lower operational costs and improved sustainability performance. Demand is particularly increasing in dairy products, bottled water, and household cleaning products where high-speed packaging operations are essential. Packaging companies are developing advanced elastic film materials that improve label durability and application precision. In addition, the growing adoption of recyclable polyolefin stretch sleeves is expected to support future market expansion. Emerging economies are likely to witness stronger demand for stretch sleeve technologies because of increasing investments in cost-efficient packaging infrastructure.

By Material

PETG material dominated the market with a 34.8% share in 2024 due to its excellent shrink performance, transparency, and print quality. PETG sleeves are widely used in beverage, cosmetics, and healthcare packaging because they support vibrant graphics and conform effectively to irregular container designs. The material also offers strong durability and moisture resistance, making it suitable for cold-chain beverage packaging and premium consumer goods. Many global beverage brands prefer PETG sleeves for energy drinks, flavored water, and sports beverages because they deliver high shelf visibility. Packaging manufacturers are also improving PETG formulations to support downgauging strategies and lower material consumption. Advanced printing technologies combined with PETG films enable detailed branding and promotional packaging campaigns, particularly in retail-focused industries.

Polyolefin materials are expected to witness the fastest CAGR of 6.6% during the forecast period because of increasing sustainability requirements and recycling compatibility. Polyolefin sleeves are gaining popularity as companies move away from traditional PVC-based labeling solutions. These materials provide lower density, improved recyclability, and reduced environmental impact compared to conventional alternatives. Beverage companies in North America and Europe are increasingly adopting polyolefin shrink sleeves to align with circular economy initiatives and packaging waste reduction targets. The material is also suitable for lightweight containers and supports efficient separation during recycling processes. Future growth is expected to be supported by technological improvements in film strength, clarity, and shrink performance. Packaging suppliers are investing in recyclable polyolefin solutions that combine environmental compliance with strong visual presentation.

By End-Use

Food and beverage applications accounted for nearly 48.5% of the global shrink and stretch sleeve labels market in 2024, making it the dominant end-use segment. Strong demand for packaged beverages, dairy products, ready-to-eat meals, and nutritional products continues to support segment growth. Sleeve labels are extensively used because they improve product visibility, enable full-body branding, and perform well in refrigerated environments. Beverage manufacturers frequently use shrink sleeves for flavored water, soft drinks, sports beverages, and alcoholic mixers due to their ability to support vibrant graphics and tamper-evident packaging. Rising urbanization and changing consumer lifestyles are increasing packaged food consumption in Asia Pacific and Latin America, further strengthening demand. Packaging companies are also integrating digital printing technologies to support seasonal branding campaigns and promotional packaging strategies for food and beverage producers.

Healthcare packaging is expected to register the fastest CAGR of 6.3% through 2034 due to growing pharmaceutical production and increasing demand for product authentication features. Sleeve labels are becoming more common in pharmaceutical bottles, nutraceutical packaging, and over-the-counter healthcare products because they provide durability and extensive information display capabilities. Manufacturers are integrating serialization codes, anti-counterfeit features, and multilingual labeling into sleeve formats to improve regulatory compliance and consumer safety. Growth in pharmaceutical exports from India and China is also contributing to rising demand for advanced labeling technologies. Future opportunities are expected to emerge from smart healthcare packaging applications that integrate QR codes and track-and-trace systems. Increasing investments in healthcare infrastructure across developing economies are likely to create additional demand for specialized sleeve labeling solutions.

Shrink And Stretch Sleeve Labels Market Segmentations

By Type

- Shrink Sleeve Labels

- Stretch Sleeve Labels

By Material

- PETG

- PVC

- Polyolefin

- OPS

- PLA

By End-User

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Household Products

- Industrial Packaging

Regional Analysis

North America

North America accounted for approximately 24.6% of the global shrink and stretch sleeve labels market in 2025 and is projected to expand at a CAGR of 5.1% through 2034. The region benefits from advanced packaging infrastructure, high packaged beverage consumption, and widespread adoption of premium branding strategies. Demand for sleeve labels is particularly strong across carbonated drinks, bottled water, personal care products, and household chemicals. Growth is also supported by increasing investments in recyclable packaging materials and automated labeling systems. Major beverage companies in the United States and Canada are adopting lightweight packaging structures to improve transportation efficiency and reduce packaging waste. In addition, digital printing technologies are improving customization capabilities for regional packaging converters.

The United States remains the dominant country within the regional market due to its large beverage manufacturing sector and advanced retail network. A major growth driver is the increasing adoption of sustainable packaging solutions by multinational consumer goods companies. Several beverage producers are replacing PVC shrink sleeves with recyclable PETG and polyolefin alternatives to comply with sustainability targets. The growing popularity of ready-to-drink coffee, energy drinks, and flavored water products is also increasing demand for full-body sleeve labeling. Regional packaging suppliers are expanding production facilities to support growing demand for digitally printed sleeves and high-speed application technologies.

Europe

Europe represented nearly 22.3% of the global shrink and stretch sleeve labels market in 2025 and is expected to register a CAGR of 5.3% during the forecast period. The regional market is influenced by strict environmental regulations, strong recycling infrastructure, and increasing demand for premium food packaging. Countries across Western Europe are promoting circular economy policies that encourage the use of recyclable label materials and reduced plastic consumption. The cosmetics and personal care sectors are also contributing significantly to market growth because sleeve labels support high-quality graphics and decorative packaging formats.

Germany remains the leading country in the European market due to its advanced packaging manufacturing industry and strong industrial automation capabilities. One unique growth driver in the region is the rising adoption of smart packaging technologies. European beverage and pharmaceutical companies are integrating QR codes and authentication features into sleeve labels to improve consumer engagement and product traceability. Demand for organic food and sustainable household products is also increasing the use of recyclable sleeve labels across retail channels. Packaging converters in Germany and France are investing in energy-efficient printing technologies and solvent-free inks to align with environmental compliance standards.

Asia Pacific

Asia Pacific dominated the global shrink and stretch sleeve labels market with a 38.1% share in 2025 and is projected to maintain strong growth at a CAGR of 6.3% through 2034. Rapid urbanization, population growth, and expanding consumer goods industries are major factors supporting regional demand. The region has become a major manufacturing hub for beverages, pharmaceuticals, and personal care products, resulting in large-scale adoption of sleeve labeling technologies. Growth in organized retail and convenience store networks is further increasing demand for visually attractive packaging. Rising middle-class income levels in countries such as China, India, Indonesia, and Vietnam are also contributing to higher packaged product consumption.

China remains the dominant country in the regional market due to its extensive beverage manufacturing base and large-scale packaging production capabilities. One unique growth driver is the rapid expansion of e-commerce and online grocery retailing. Companies are investing in durable and visually appealing packaging solutions that maintain product integrity during transportation. Chinese packaging manufacturers are also increasing investments in digital printing and automated sleeve application systems to improve operational efficiency. India is emerging as another high-growth market because of rising pharmaceutical production and increasing consumption of packaged food products. Regional governments are encouraging investments in sustainable packaging materials to reduce environmental impact and strengthen export competitiveness.

Middle East & Africa

The Middle East & Africa accounted for around 7.5% of the global shrink and stretch sleeve labels market in 2025 and is anticipated to grow at a CAGR of 5.6% through 2034. Increasing urbanization, rising food imports, and growth in packaged consumer goods are supporting regional market development. Beverage companies are expanding production capacity across Gulf countries and African economies to address growing demand from young consumer populations. The region is also witnessing increasing investments in retail infrastructure, including supermarkets and convenience store chains, which support demand for attractive product packaging.

Saudi Arabia remains the dominant country in the regional market due to expanding beverage production and strong investments in industrial diversification initiatives. One important growth driver is the increasing demand for halal-certified packaged products with multilingual labeling requirements. Sleeve labels allow manufacturers to include extensive branding and regulatory information while maintaining attractive product presentation. In Africa, rising consumption of bottled water and affordable personal care products is contributing to market expansion. Regional packaging companies are increasingly partnering with international suppliers to improve access to advanced printing technologies and recyclable film materials.

Latin America

Latin America held approximately 7.5% of the global shrink and stretch sleeve labels market in 2025 and is forecast to expand at the fastest CAGR of 6.4% during the assessment period. The region is benefiting from increasing packaged beverage consumption, expanding retail distribution networks, and rising investments in local packaging manufacturing. Countries across the region are experiencing higher demand for flavored drinks, dairy beverages, and packaged food products, all of which require visually competitive packaging. Sleeve labels are increasingly preferred because they support vibrant graphics and perform well in humid transportation environments.

Brazil remains the leading country in the Latin American market because of its strong beverage and food processing industries. One unique growth driver is the expansion of local craft beverage production, including flavored water, juices, and specialty soft drinks. These products rely heavily on attractive packaging to strengthen brand differentiation in retail stores. Regional packaging companies are also adopting digital printing technologies to support shorter production runs and promotional packaging campaigns. Mexico is emerging as another important market because of growing exports of packaged consumer goods to North America. Sustainability initiatives and improvements in recycling infrastructure are expected to create additional growth opportunities across the region.

Competitive Landscape

The shrink and stretch sleeve labels market is moderately fragmented, with global and regional packaging companies competing through material innovation, printing technologies, and strategic partnerships. Leading companies are focusing on recyclable sleeve materials, lightweight films, and digital printing capabilities to strengthen market positioning. Investments in automated production lines and sustainable packaging technologies are increasing across the competitive landscape.

CCL Industries remains one of the leading companies in the market due to its broad global presence, diversified labeling portfolio, and strong investments in sustainable packaging technologies. The company has expanded its recyclable sleeve labeling solutions for beverage and personal care applications. Other major companies are also increasing research and development activities to improve print quality, reduce film thickness, and support recycling compatibility.

Berry Global and Fuji Seal International are focusing on advanced shrink sleeve materials and high-speed labeling technologies to address rising beverage packaging demand. Multi-Color Corporation is strengthening digital printing capabilities to support short-run promotional packaging campaigns. Klockner Pentaplast is expanding production of recyclable films and environmentally compatible packaging solutions for consumer goods manufacturers.

Strategic collaborations between packaging converters and beverage manufacturers are becoming more common as companies seek customized sleeve solutions with improved sustainability performance. Capacity expansion projects in Asia Pacific and Latin America are also increasing as regional demand for packaged consumer goods continues to rise.

Key Players List

- CCL Industries

- Fuji Seal International

- Berry Global

- Multi-Color Corporation

- Klockner Pentaplast

- Huhtamaki Oyj

- Allen Plastic Industries

- Macfarlane Group

- Hammer Packaging

- Fort Dearborn Company

- Polysack Flexible Packaging

- Cenveo Corporation

- Paris Art Label Company

- Resource Label Group

- Brook + Whittle

- Constantia Flexibles