Semiconductor Assembly Packaging Equipment Market Size and Growth

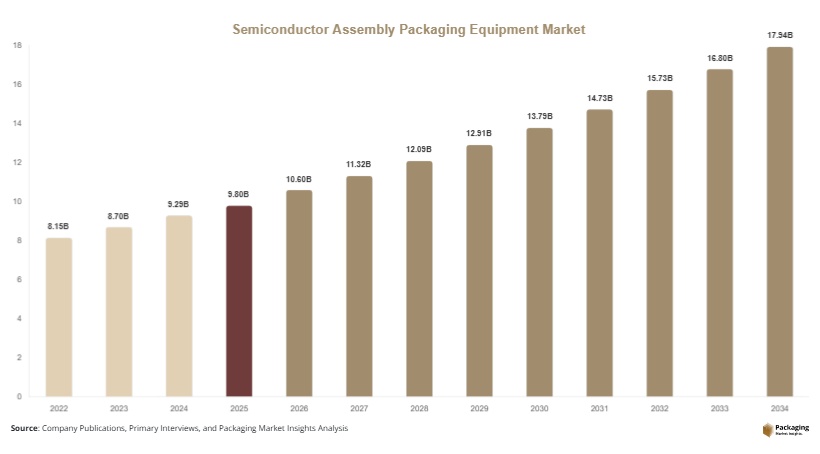

The global semiconductor assembly packaging equipment market size was valued at USD 9.8 billion in 2025 and is estimated to reach USD 10.6 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to grow at a CAGR of 6.8%, reaching approximately USD 18.9 billion by 2034. This growth trajectory reflects sustained investments in semiconductor fabrication and backend processes, especially in regions strengthening domestic chip production capabilities. The semiconductor assembly packaging equipment market is witnessing steady expansion as the semiconductor industry evolves toward higher performance, miniaturization, and integration.

One of the major factors supporting market expansion is the increasing demand for high-performance consumer electronics, including smartphones, tablets, and wearable devices. These products require compact and efficient semiconductor packaging solutions, which directly drives the adoption of advanced assembly equipment. Another important growth factor is the rise of electric vehicles and automotive electronics, where semiconductors play a critical role in power management, safety systems, and infotainment. Additionally, the expansion of cloud computing and hyperscale data centers is accelerating the demand for advanced chips, thereby boosting the need for packaging equipment.

Key Highlights

- Asia Pacific dominated the market with a 41.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.1%.

- Advanced packaging equipment led the type segment with a 34.8% share, while wafer-level packaging is expected to grow at a CAGR of 7.5%.

- Consumer electronics dominated with a 46.5% share, while automotive electronics is forecasted to grow at a CAGR of 7.9%.

- Integrated device manufacturers led the end-use segment with 39.7% share, while OSAT companies are expected to grow at a CAGR of 7.2%.

- China remained the dominant country with a market size of USD 3.1 billion in 2025 and USD 3.4 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing adoption of advanced semiconductor packaging technologies

The market is experiencing a transition toward advanced packaging technologies such as 2.5D integration, 3D packaging, and system-in-package solutions. These technologies enable higher performance and better thermal management while maintaining compact designs. As applications like artificial intelligence, 5G communication, and high-performance computing continue to expand, traditional packaging methods are becoming less effective. This shift is pushing manufacturers to adopt more sophisticated equipment capable of handling complex designs. The integration of multiple chips into a single package also enhances functionality and reduces power consumption, which is becoming essential for next-generation devices. As a result, equipment providers are continuously innovating to support these advanced processes.

Increasing integration of automation and smart manufacturing systems

Automation and smart manufacturing are becoming central to semiconductor packaging operations. Manufacturers are integrating robotics, artificial intelligence, and real-time monitoring systems to improve efficiency and reduce production errors. These technologies enable predictive maintenance and better quality control, which are critical in semiconductor manufacturing. Smart factories also allow for higher scalability and flexibility in production, making it easier to adapt to changing market demands. As competition intensifies, companies are focusing on optimizing their production processes to reduce costs and improve yield rates. This shift toward digitalization is expected to play a significant role in shaping the future of the semiconductor assembly packaging equipment market.

Market Drivers

Rising demand for consumer electronics and connected devices

The continuous growth of consumer electronics remains a key factor influencing the semiconductor assembly packaging equipment market. Devices such as smartphones, laptops, wearables, and smart home systems are becoming more advanced and compact, requiring efficient semiconductor packaging solutions. The increasing penetration of IoT devices is also contributing to this demand, as these products rely heavily on miniaturized and high-performance chips. Manufacturers are investing in advanced packaging technologies to meet these requirements, which is driving demand for specialized equipment. Additionally, rapid product innovation cycles are pushing companies to adopt flexible and scalable packaging solutions, further supporting market expansion.

Expansion of semiconductor usage in automotive and mobility sectors

The automotive industry is undergoing a major transformation with the rise of electric vehicles, connected cars, and autonomous driving technologies. These developments are significantly increasing the use of semiconductors in vehicles. Applications such as advanced driver-assistance systems, battery management systems, and infotainment require reliable and high-performance chips. This, in turn, is driving the need for advanced packaging equipment capable of meeting stringent automotive standards. The growing focus on vehicle safety and energy efficiency is further accelerating semiconductor adoption. As automotive production continues to evolve, the demand for assembly and packaging equipment is expected to grow steadily.

Market Restraint

High capital investment and operational complexity

The semiconductor assembly packaging equipment market faces challenges due to the high cost of advanced equipment and the complexity of operations. Establishing and maintaining semiconductor packaging facilities requires significant capital investment, which can be a barrier for smaller companies. The need for continuous upgrades to keep pace with technological advancements further increases financial pressure. Additionally, operating advanced packaging systems requires skilled labor and specialized knowledge, adding to operational complexity. These factors can limit the adoption of new technologies, particularly in developing regions. For example, smaller semiconductor firms may struggle to invest in cutting-edge packaging equipment, which can affect their competitiveness and slow overall market growth.

Market Opportunities

Expansion of semiconductor manufacturing in emerging economies

Emerging economies are becoming important growth areas for the semiconductor assembly packaging equipment market. Governments in regions such as Asia, Latin America, and the Middle East are investing in semiconductor manufacturing to reduce reliance on imports and strengthen local industries. Incentives such as tax benefits, subsidies, and infrastructure development are attracting global players to establish production facilities in these regions. This expansion is creating strong demand for assembly and packaging equipment. Additionally, the growth of electronics manufacturing in these economies is further supporting market development. As these regions continue to industrialize, they are expected to contribute significantly to global market growth.

Rising demand for high-performance computing and AI applications

The increasing adoption of artificial intelligence and high-performance computing is creating new opportunities in the market. These applications require advanced semiconductor packaging solutions that can handle high processing speeds and efficient heat dissipation. As industries such as healthcare, finance, and telecommunications adopt AI-driven technologies, the demand for advanced chips is rising. This is encouraging semiconductor manufacturers to invest in innovative packaging techniques and equipment. The growth of data centers and cloud computing infrastructure is also contributing to this trend. Equipment providers are focusing on developing solutions tailored to these applications, which is expected to drive market growth in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.8 Billion |

| Market Size in 2026 | USD 10.6 Billion |

| Market Size in 2034 | USD 18.9 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Advanced packaging equipment accounted for the largest share of 34.8% in 2024, driven by the increasing demand for high-performance semiconductor devices. These technologies enable better integration, improved performance, and reduced size, making them essential for modern electronics. The growing complexity of semiconductor designs is further driving the adoption of advanced packaging solutions. Manufacturers are focusing on enhancing their capabilities to meet industry requirements, which is supporting the growth of this segment.

Wafer-level packaging is expected to witness the fastest growth with a CAGR of 7.5% during the forecast period. This growth is attributed to the increasing demand for compact and efficient electronic devices. Wafer-level packaging offers advantages such as reduced footprint, improved electrical performance, and cost efficiency. As industries continue to evolve, the demand for such solutions is expected to rise, driving the adoption of advanced packaging equipment.

By Application

Consumer electronics held the largest share of 46.5% in 2024, driven by the high demand for smartphones, tablets, and wearable devices. These products require advanced semiconductor components that rely on efficient packaging solutions. The growing adoption of smart devices and IoT technologies is further contributing to the segment’s dominance. Manufacturers are continuously innovating to meet consumer demands, which is supporting the growth of this segment.

Automotive electronics is expected to grow at the fastest CAGR of 7.9% during the forecast period. The increasing adoption of electric vehicles and advanced driver-assistance systems is driving demand for semiconductor components. These applications require reliable and high-performance packaging solutions, which is encouraging investments in advanced equipment. This trend is expected to continue, supporting segment growth.

By End-Use

Integrated device manufacturers accounted for 39.7% of the market share in 2024, reflecting their strong control over semiconductor production processes. These companies are investing heavily in advanced packaging technologies to enhance efficiency and maintain competitiveness. The growing demand for high-performance chips is further supporting this segment.

OSAT companies are expected to grow at a CAGR of 7.2% during the forecast period. The increasing trend of outsourcing semiconductor packaging and testing services is driving demand for these companies. They offer cost-effective solutions and specialized expertise, making them an attractive option for manufacturers. This is encouraging investments in advanced packaging equipment, supporting segment growth.

Semiconductor Assembly Packaging Equipment Market Segmentations

By Type

- Advanced Packaging Equipment

- Wafer-Level Packaging Equipment

- Die-Attach Equipment

- Wire Bonding Equipment

By Application

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Healthcare Devices

By End-Use

- Integrated Device Manufacturers

- OSAT Companies

- Foundries

Regional Analysis

North America

North America held a significant share of 22.6% in the semiconductor assembly packaging equipment market in 2025 and is projected to grow at a CAGR of 6.4% during the forecast period. The region benefits from strong technological infrastructure and a well-established semiconductor ecosystem. Increasing investments in research and development, along with government initiatives aimed at boosting domestic chip manufacturing, are supporting market growth. The demand for advanced packaging solutions is also rising due to the expansion of data centers and high-performance computing applications.

The United States remains the dominant contributor in this region, supported by its strong presence of semiconductor companies and innovation-driven environment. A key factor driving growth is the increasing focus on reshoring semiconductor manufacturing to reduce supply chain dependencies. This shift is encouraging investments in advanced packaging equipment, helping the country maintain its competitive position in the global market.

Europe

Europe accounted for 18.3% of the semiconductor assembly packaging equipment market share in 2025 and is expected to grow at a CAGR of 6.1% through 2034. The region is focusing on strengthening its semiconductor supply chain, particularly in response to global disruptions. Investments in automotive and industrial electronics are driving demand for packaging equipment. European manufacturers are also adopting advanced technologies to enhance efficiency and meet evolving industry standards.

Germany leads the European market due to its strong industrial base and advanced manufacturing capabilities. A unique growth factor in this region is the rapid adoption of electric vehicles, which require advanced semiconductor components. This is driving the demand for specialized packaging equipment, supporting the overall market growth in Europe.

Asia Pacific

Asia Pacific dominated the semiconductor assembly packaging equipment market with a 41.2% share in 2025 and is projected to grow at a CAGR of 7.2%. The region’s dominance is attributed to its extensive semiconductor manufacturing base and strong presence of electronics producers. Countries such as China, Japan, South Korea, and Taiwan play a major role in driving market growth. The increasing demand for consumer electronics and supportive government policies are key factors contributing to the region’s leadership.

China stands out as the leading country in Asia Pacific, driven by significant investments in semiconductor infrastructure. A major factor supporting growth is the country’s focus on achieving self-reliance in semiconductor production. This is encouraging domestic companies to expand their capabilities, leading to increased demand for assembly and packaging equipment.

Middle East & Africa

The Middle East & Africa held a market share of 7.4% in 2025 and is expected to grow at a CAGR of 6.7%. The region is gradually developing its semiconductor capabilities, supported by investments in technology and infrastructure. Governments are focusing on diversifying their economies and promoting advanced industries, which is driving interest in semiconductor manufacturing and packaging.

The United Arab Emirates is emerging as a key market in this region, supported by its emphasis on innovation and digital transformation. A notable growth factor is the development of smart cities and advanced infrastructure projects, which require sophisticated electronic components. This is increasing demand for semiconductor packaging equipment, contributing to regional market growth.

Latin America

Latin America captured 10.5% of the semiconductor assembly packaging equipment market share in 2025 and is projected to grow at the fastest CAGR of 7.1%. The region is experiencing growth in electronics manufacturing, which is driving demand for packaging equipment. Government initiatives aimed at industrial development and technological advancement are further supporting the market.

Brazil leads the market in Latin America due to its expanding electronics and automotive sectors. A key growth factor is the increasing demand for consumer electronics and vehicle components, which rely on semiconductor technologies. This is encouraging manufacturers to invest in advanced packaging equipment, supporting the overall market expansion.

Competitive Landscape

The semiconductor assembly packaging equipment market is moderately consolidated, with key players focusing on innovation, partnerships, and expansion strategies. Leading companies are investing in advanced technologies to improve efficiency and meet evolving industry requirements. ASM Pacific Technology is considered a leading player due to its strong portfolio and continuous focus on research and development. The company has recently introduced advanced packaging solutions aimed at improving production efficiency.

Other major players are also focusing on automation and digitalization to enhance their capabilities. Strategic collaborations and acquisitions are common as companies aim to strengthen their market position. The competitive environment is expected to remain dynamic, with technological advancements playing a key role in shaping market competition.

Key Players List

- ASM Pacific Technology

- Applied Materials, Inc.

- Tokyo Electron Limited

- Kulicke & Soffa Industries, Inc.

- BE Semiconductor Industries N.V.

- Hitachi High-Technologies Corporation

- DISCO Corporation

- Canon Machinery Inc.

- Panasonic Corporation

- Shinkawa Ltd.

- Palomar Technologies

- Hanmi Semiconductor

- SUSS MicroTec SE

- Nordson Corporation

- Mycronic AB