Semiconductor And Ic Packaging Materials Market Size and Growth

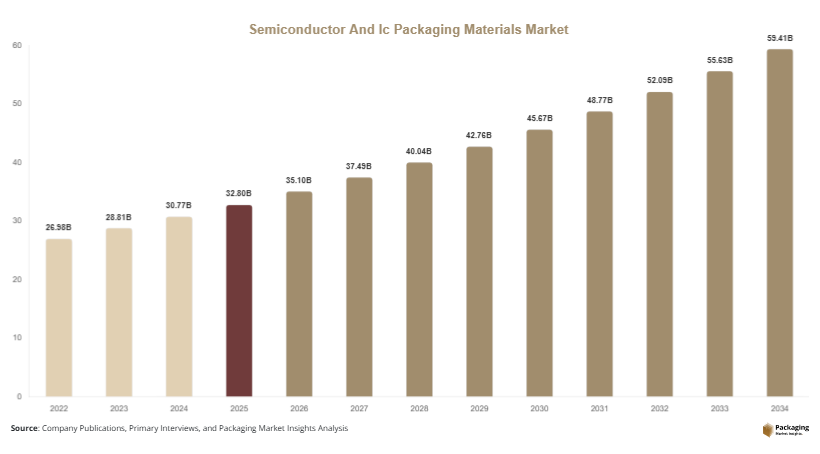

The global semiconductor and Ic packaging materials market size was valued at approximately USD 32.8 billion in 2025 and is estimated to reach USD 35.1 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to grow at a CAGR of 6.8%, reaching nearly USD 63.7 billion by 2034. This growth reflects the growing importance of packaging materials such as substrates, encapsulants, bonding wires, and leadframes in ensuring performance, durability, and efficiency of semiconductor devices. The semiconductor and Ic packaging materials market is experiencing consistent expansion due to rising semiconductor demand across multiple industries and the increasing complexity of integrated circuits.

A key factor supporting market growth is the increasing demand for advanced computing technologies including artificial intelligence, cloud computing, and high-performance data processing. These applications require compact and efficient semiconductor packaging solutions with enhanced thermal and electrical properties. Another important growth driver is the expansion of consumer electronics, particularly smartphones, wearables, and connected devices, which rely heavily on miniaturized semiconductor components. Additionally, the automotive sector is contributing significantly, as electric vehicles and advanced driver-assistance systems depend on high-reliability semiconductor packaging materials.

Key Highlights:

- Asia Pacific dominated the market with a 41.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.1%.

- Organic substrates led the type segment with a 34.7% share, while encapsulation resins are expected to grow at a CAGR of 7.3%.

- Consumer electronics dominated the application segment with a 46.5% share, while automotive electronics are forecasted to grow at a CAGR of 7.6%.

- Integrated device manufacturers led the end-use segment with 49.8% share, while outsourced semiconductor assembly and test providers are expected to grow at a CAGR of 7.0%.

- China remained the dominant country with a market size of USD 9.6 billion in 2025 and USD 10.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising adoption of advanced packaging architectures

The semiconductor and Ic packaging materials market is increasingly influenced by the adoption of advanced packaging architectures such as 2.5D, 3D integration, fan-out wafer-level packaging, and system-in-package solutions. These approaches allow multiple chips to be integrated into a single package, improving functionality while reducing size and power consumption. As chipmakers aim to overcome the physical limitations of traditional scaling, advanced packaging has emerged as a practical alternative. This shift is driving demand for high-performance materials with superior thermal conductivity, electrical insulation, and mechanical reliability. Materials such as advanced substrates and specialized encapsulants are being developed to support these architectures, enabling improved chip performance and integration capabilities.

Growing emphasis on sustainable and compliant materials

Sustainability is becoming an important focus area within the semiconductor and Ic packaging materials market. Manufacturers are increasingly adopting environmentally friendly materials to meet regulatory requirements and reduce environmental impact. This includes the development of halogen-free flame retardants, recyclable substrates, and low-emission encapsulation compounds. Companies are also optimizing production processes to reduce waste and energy consumption. The growing demand for green electronics, particularly in regions with strict environmental regulations, is encouraging innovation in material design. Sustainable packaging materials are expected to gain wider acceptance as companies align their operations with global environmental standards.

Market Drivers

Expansion of consumer electronics ecosystem

The growth of the consumer electronics industry continues to play a significant role in driving the semiconductor and Ic packaging materials market. Devices such as smartphones, tablets, laptops, and wearable technologies require compact and efficient semiconductor components that rely on advanced packaging materials. As consumers demand higher performance, faster processing speeds, and improved connectivity, manufacturers are focusing on innovative packaging solutions. These solutions depend on materials that provide excellent thermal management, electrical conductivity, and durability. The increasing penetration of smart devices and connected technologies is creating consistent demand for packaging materials, supporting long-term market expansion.

Increasing integration of semiconductor components in automotive systems

The automotive sector is undergoing rapid transformation with the adoption of electric mobility and advanced safety technologies. Semiconductor components are essential for battery management systems, power electronics, and driver-assistance features. This shift is increasing the demand for high-performance packaging materials capable of withstanding harsh operating conditions. Automotive applications require materials with enhanced reliability, thermal resistance, and durability. As vehicles become more electronically advanced, the role of semiconductor packaging materials becomes more critical. This ongoing transformation in the automotive industry is expected to significantly contribute to market growth over the forecast period.

Market Restraints

High cost associated with advanced material development

The semiconductor and Ic packaging materials market faces challenges related to the high cost of advanced materials and manufacturing processes. Materials used in next-generation packaging, such as high-performance substrates and specialized encapsulants, require complex production techniques and strict quality control. These factors increase overall costs, making it difficult for smaller manufacturers to adopt advanced solutions. Additionally, fluctuations in raw material prices and supply chain disruptions can further impact cost structures. For example, rising prices of copper and specialty chemicals have affected production expenses, creating pressure on profit margins. These cost-related challenges may limit widespread adoption of advanced packaging materials in certain market segments.

Market Opportunities

Increasing demand for high-performance computing applications

The growing adoption of high-performance computing applications presents a strong opportunity for the semiconductor and Ic packaging materials market. Technologies such as artificial intelligence, data analytics, and cloud computing require semiconductor devices with high processing capabilities and efficient thermal management. Packaging materials that support these requirements are in high demand. Innovations in advanced substrates, thermal interface materials, and high-density interconnects are enabling the development of next-generation semiconductor devices. As industries continue to adopt digital technologies, the demand for advanced packaging materials is expected to increase significantly.

Expansion of semiconductor manufacturing in emerging economies

Emerging economies are investing in semiconductor manufacturing infrastructure to strengthen their technological capabilities and reduce reliance on imports. Governments are offering incentives to attract investments in fabrication and assembly facilities, creating new opportunities for packaging material suppliers. As new manufacturing plants are established, the demand for semiconductor packaging materials is expected to rise. This trend is particularly evident in regions focusing on building domestic semiconductor ecosystems. The expansion of manufacturing capacity in these regions is likely to create long-term growth opportunities for market participants.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 32.8 Billion |

| Market Size in 2026 | USD 35.1 Billion |

| Market Size in 2034 | USD 63.7 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Organic substrates accounted for the largest share of the semiconductor and Ic packaging materials market in 2024, contributing approximately 34.7% of the total market. These materials are widely used due to their cost efficiency, flexibility, and compatibility with advanced packaging technologies. Organic substrates support high-density interconnects and provide reliable electrical performance, making them suitable for a wide range of semiconductor applications. The increasing adoption of flip-chip and ball grid array packaging has further strengthened demand for these materials.

Encapsulation resins are projected to experience the fastest growth, with a CAGR of 7.3% during the forecast period. These materials are essential for protecting semiconductor devices from environmental factors such as moisture, heat, and mechanical stress. As semiconductor devices become more complex, the need for advanced encapsulation solutions increases. Innovations in resin formulations are improving performance and reliability, supporting growth in this segment.

By Application

Consumer electronics represented the largest share of the semiconductor and Ic packaging materials market in 2024, accounting for approximately 46.5% of total demand. The widespread use of semiconductor components in devices such as smartphones, laptops, and wearables is driving demand for packaging materials. Manufacturers are focusing on developing compact and efficient packaging solutions to meet evolving consumer expectations.

Automotive electronics is expected to grow at the fastest rate, with a projected CAGR of 7.6%. The increasing adoption of electric vehicles and advanced safety systems is driving demand for semiconductor components. Packaging materials used in automotive applications must meet strict requirements for reliability and thermal performance, supporting growth in this segment.

By End-Use

Integrated device manufacturers accounted for the largest share of the semiconductor and Ic packaging materials market in 2024, representing approximately 49.8% of total demand. These companies manage both fabrication and packaging processes, allowing greater control over product quality and performance. The increasing demand for high-performance semiconductor devices is driving growth in this segment.

Outsourced semiconductor assembly and test providers are expected to grow at the fastest rate, with a CAGR of 7.0%. These companies offer specialized packaging services, enabling semiconductor manufacturers to focus on design and fabrication. The increasing complexity of packaging technologies is driving demand for outsourced services, supporting segment growth.

Semiconductor And Ic Packaging Materials Market Segmentations

By Type

- Organic Substrates

- Bonding Wires

- Leadframes

- Encapsulation Resins

By Application

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Healthcare Devices

By End-Use

- Integrated Device Manufacturers

- Outsourced Semiconductor Assembly and Test Providers

Regional Analysis

North America

North America accounted for approximately 22.5% of the semiconductor and Ic packaging materials market share in 2025 and is projected to grow at a CAGR of 6.3% through 2034. The region benefits from strong demand across data centers, aerospace, and defense sectors. Continuous investment in semiconductor research and development supports the adoption of advanced packaging materials. The presence of leading technology firms also contributes to steady demand for high-performance materials used in next-generation semiconductor devices.

The United States leads the regional market due to its advanced semiconductor ecosystem and strong innovation capabilities. A key growth factor is the increasing focus on domestic semiconductor manufacturing, supported by policy initiatives and funding programs. This emphasis on local production is driving demand for packaging materials, as companies aim to strengthen supply chain resilience and reduce dependence on external sources.

Europe

Europe held around 18.7% share of the semiconductor and Ic packaging materials market in 2025 and is expected to grow at a CAGR of 6.1% during the forecast period. The region’s growth is largely driven by the automotive and industrial sectors, which require reliable semiconductor components. European manufacturers emphasize quality and durability, leading to increased adoption of high-performance packaging materials.

Germany dominates the European market due to its strong automotive manufacturing base and advanced engineering capabilities. A unique growth factor is the region’s commitment to sustainability and environmental standards. Companies are focusing on eco-friendly materials and production methods, which is influencing market trends and encouraging the development of sustainable packaging solutions.

Asia Pacific

Asia Pacific accounted for the largest share of 41.2% in 2025 and is projected to grow at a CAGR of 7.2% through 2034. The region benefits from a well-established semiconductor manufacturing ecosystem and strong demand from consumer electronics and automotive industries. Countries such as China, Japan, South Korea, and Taiwan play a central role in driving market growth.

China remains the dominant country in the region, supported by large-scale semiconductor production and government initiatives aimed at boosting domestic manufacturing. A key growth factor is the rapid expansion of electronics manufacturing hubs, which increases demand for packaging materials. The presence of major foundries and assembly facilities further strengthens the region’s leadership position.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.3% of the semiconductor and Ic packaging materials market in 2025 and is expected to grow at a CAGR of 5.8% over the forecast period. Growth in this region is supported by increasing adoption of digital technologies and infrastructure development. Governments are investing in smart city projects and digital transformation initiatives, which require semiconductor components.

The United Arab Emirates is a leading market within the region, driven by its focus on technological advancement and innovation. A unique growth factor is the increasing deployment of IoT devices and connected infrastructure. These developments are creating demand for semiconductor components and packaging materials, contributing to regional market growth.

Latin America

Latin America held around 11.3% share of the semiconductor and Ic packaging materials market in 2025 and is projected to grow at the fastest CAGR of 7.1% through 2034. The region is witnessing rising demand for consumer electronics and automotive technologies, which is supporting market expansion. Increasing investments in manufacturing and infrastructure are also contributing to growth.

Brazil dominates the regional market due to its expanding electronics manufacturing sector. A key growth factor is the increasing presence of local production facilities and foreign investments. Improving economic conditions and rising adoption of advanced technologies are further supporting demand for semiconductor packaging materials across the region.

Competitive Landscape

The semiconductor and Ic packaging materials market is moderately competitive, with several global players focusing on innovation and capacity expansion. ASE Group holds a leading position due to its strong technological capabilities and extensive service offerings. The company continues to invest in advanced packaging technologies and material innovation to maintain its market position. Recent developments include partnerships with semiconductor manufacturers to develop next-generation packaging solutions.

Other companies are also focusing on research and development to improve material performance and reduce costs. Strategic collaborations and product innovations are common approaches used by market participants to strengthen their competitive position.

Key Players List

- ASE Group

- Amkor Technology

- TSMC

- Samsung Electronics

- Intel Corporation

- Sumitomo Chemical

- Hitachi Chemical

- DuPont

- Henkel AG

- Shin-Etsu Chemical

- BASF SE

- LG Chem

- Kyocera Corporation

- Ibiden Co., Ltd.

- JCET Group