Rigid Tray Market Size and Growth

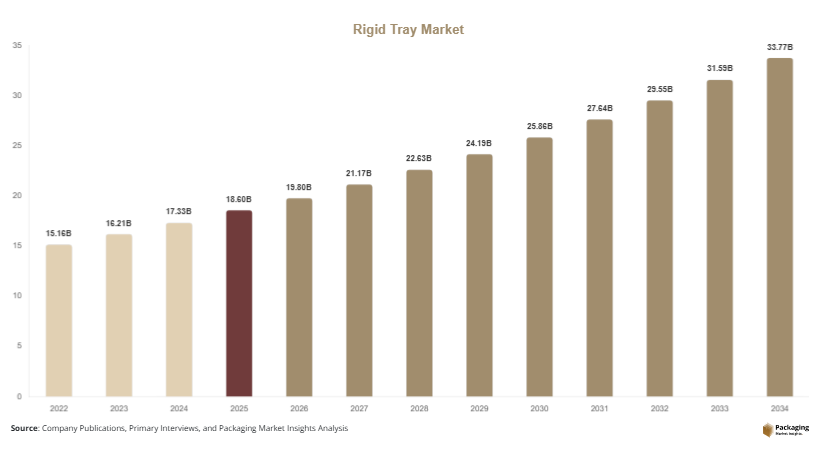

The global rigid tray market size is estimated at USD 18.6 billion in 2025, reflecting strong demand from food processing and retail-ready packaging sectors. By 2026, the market is projected to reach USD 19.8 billion, driven by rapid adoption in ready-to-eat meals, pharmaceutical blister packaging, and industrial component handling. Looking ahead, the market is forecasted to reach USD 34.2 billion by 2034, expanding at a CAGR of 6.9% (2025–2034).

Several structural growth drivers are shaping the market trajectory. First, the increasing consumption of packaged and convenience foods is boosting demand for rigid trays in portion control and microwave-safe packaging formats. Second, expansion of e-commerce grocery delivery services is accelerating the need for protective and stackable packaging solutions. Third, sustainability regulations are pushing manufacturers toward recyclable PET, PP, and molded fiber trays, reducing environmental impact while maintaining product integrity.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 12.4 billion in 2025 and USD 13.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Recyclable Rigid Tray Materials

A major trend shaping the rigid tray market is the rapid transition toward sustainable packaging materials. Manufacturers are increasingly replacing conventional plastics with recyclable PET, bio-based polymers, and molded fiber solutions. This shift is largely driven by regulatory restrictions on single-use plastics and growing consumer preference for eco-friendly packaging. For instance, food delivery companies and supermarket chains are introducing compostable rigid trays for fresh produce and ready meals. In Europe, several retailers have adopted fiber-based trays for meat and bakery products, reducing reliance on plastic foam alternatives. In the future, innovations in bio-resins and closed-loop recycling systems are expected to further strengthen sustainable packaging adoption, making eco-compliant rigid trays a standard in global supply chains.

Expansion of Smart and Functional Packaging Integration

Another significant trend is the integration of smart features into rigid trays, enhancing traceability, safety, and user interaction. RFID tags, QR codes, and temperature-sensitive indicators are increasingly embedded in rigid packaging formats, particularly in pharmaceuticals and premium food segments. For example, cold-chain logistics providers use smart rigid trays to monitor temperature-sensitive vaccines during transportation. Similarly, premium food brands are adopting QR-enabled trays that provide product origin, nutritional information, and storage instructions. This trend is expected to expand as IoT-enabled packaging becomes more affordable and scalable. Over time, smart rigid trays will support inventory management, reduce food waste, and improve supply chain transparency across industries.

Market Drivers

Rising Demand for Convenience and Ready-to-Eat Food Packaging

The growing consumption of ready-to-eat and packaged meals is a primary driver of the rigid tray market. Urbanization, busy lifestyles, and increasing dual-income households have significantly boosted demand for convenient food packaging formats. Rigid trays are widely used in frozen meals, bakery packaging, and pre-cooked meal kits due to their structural strength and heat resistance. For example, supermarkets in North America and Asia increasingly offer microwave-safe rigid trays for single-serve meals, enhancing consumer convenience. Food delivery platforms are also contributing to this demand by standardizing meal packaging into compartmentalized rigid trays. As convenience food penetration increases globally, rigid trays will remain a preferred solution for safe, portion-controlled, and visually appealing food packaging.

Growth in Healthcare and Pharmaceutical Packaging Applications

The healthcare sector is another major driver of rigid tray adoption. Pharmaceutical companies rely on rigid trays for sterile packaging, blister packs, and medical device protection. The increasing distribution of vaccines, biologics, and sensitive drugs has intensified the need for contamination-resistant packaging formats. For instance, hospitals and diagnostic labs use rigid trays for organizing surgical kits and diagnostic instruments. Additionally, global vaccine distribution programs have highlighted the importance of temperature-stable and tamper-evident packaging systems. Regulatory compliance standards such as GMP and FDA packaging requirements further encourage the use of rigid trays in medical logistics. This growing reliance on secure and hygienic packaging is expected to significantly drive long-term market growth.

Market Restraint

High Raw Material Volatility and Production Cost Pressure

A key restraint impacting the rigid tray market is the volatility in raw material prices, particularly plastics such as PET, PP, and polystyrene. Fluctuations in crude oil prices directly influence production costs, making pricing stability difficult for manufacturers. Additionally, the shift toward sustainable materials like bio-polymers and molded fiber often involves higher production costs and limited scalability. Small and medium-sized packaging companies face challenges in adopting advanced manufacturing technologies due to capital-intensive equipment requirements. For example, converting from conventional thermoforming lines to eco-friendly fiber molding systems requires significant investment, limiting adoption in developing economies. These cost pressures can slow down market penetration, particularly in price-sensitive regions, and create barriers for widespread sustainability adoption.

Market Opportunities

Expansion of E-commerce Grocery and Meal Delivery Services

The rapid growth of online grocery platforms and food delivery services presents a major opportunity for the rigid tray market. Companies require durable, spill-resistant, and stackable packaging to ensure product integrity during last-mile delivery. Rigid trays are increasingly used for meal kits, fresh produce, and frozen foods due to their protective properties. For example, e-commerce platforms in Asia and North America are standardizing compartmentalized rigid trays for subscription-based meal delivery services. The increasing demand for hygienic and tamper-proof packaging is expected to accelerate innovation in sealed and insulated rigid trays. Over time, this segment will become one of the most profitable applications for rigid tray manufacturers.

Adoption of Advanced Manufacturing and Lightweight Design Technologies

Technological advancements in thermoforming, injection molding, and lightweight composite design are creating new opportunities for the rigid tray market. Manufacturers are focusing on reducing material usage while maintaining strength and durability, resulting in cost-efficient and eco-friendly products. For instance, advanced ribbed structural designs allow trays to use less plastic without compromising load-bearing capacity. Additionally, automation and AI-driven manufacturing systems are improving production efficiency and reducing waste. These innovations are expected to open new opportunities in industrial packaging, automotive components, and electronics logistics. In the future, lightweight rigid trays will become a key focus area for manufacturers aiming to balance performance and sustainability.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.8 Billion |

| Market Size in 2034 | USD 34.2 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic rigid trays dominated the market with a 2024 share of 54.1%, driven by their durability, cost efficiency, and versatility across industries. These trays are widely used in food packaging, electronics, and pharmaceutical applications due to their moisture resistance and structural integrity. For example, PET-based trays are commonly used in supermarkets for meat and bakery packaging, ensuring product visibility and freshness. Industrial manufacturers also rely on plastic trays for component handling and storage due to their stackability and lightweight properties. Their dominance is further supported by advanced thermoforming technologies that enable mass production at lower costs.

The fastest-growing subsegment is molded fiber rigid trays, projected to grow at a CAGR of 7.3%. This growth is driven by sustainability mandates and increasing demand for biodegradable packaging solutions. Companies are investing in fiber molding technologies to replace plastic-based trays in foodservice and retail applications. For example, quick-service restaurants are adopting fiber trays for takeaway meals to reduce environmental impact. Future outlook suggests strong expansion in Europe and North America due to strict environmental regulations and consumer preference for eco-friendly packaging.

By Material

Polyethylene terephthalate (PET) dominated the material segment with a 2024 share of 38.6%, due to its recyclability, transparency, and food-grade safety. PET rigid trays are extensively used in food packaging applications such as salads, fruits, and ready meals. Their ability to maintain product freshness and visual appeal makes them highly preferred in retail environments. For example, supermarket chains use PET trays for premium produce packaging, enhancing shelf visibility and consumer engagement.

Molded fiber materials represent the fastest-growing segment with a CAGR of 7.5%, driven by increasing sustainability initiatives. These trays are made from recycled paper pulp and are gaining traction in foodservice and healthcare packaging. Companies are investing in fiber-based innovation to reduce plastic dependency and meet regulatory requirements. The future outlook indicates strong adoption in Europe and Asia Pacific, where environmental compliance is accelerating material substitution.

By End-Use

Food and beverage dominated the end-use segment with a 2024 share of 45.2%, driven by strong demand for packaged food, frozen meals, and bakery products. Rigid trays are widely used in supermarkets, restaurants, and food delivery platforms due to their durability and hygiene benefits. For example, ready-to-eat meal providers rely on compartmentalized trays for portion control and microwave-safe packaging.

The healthcare segment is the fastest-growing, with a CAGR of 6.8%, driven by increasing pharmaceutical distribution and medical device packaging requirements. Hospitals and laboratories use rigid trays for sterile storage and transportation of instruments. Growth is supported by rising vaccine distribution and strict regulatory compliance in medical packaging.

Rigid Tray Market Segmentations

By Type

- Plastic Rigid Trays

- Paper-Based Rigid Trays

- Molded Fiber Trays

- Hybrid Composite Trays

By Material

- PET (Polyethylene Terephthalate)

- PP (Polypropylene)

- Polystyrene

- Molded Fiber

- Bio-based Polymers

By End-Use

- Food & Beverage

- Healthcare & Pharmaceuticals

- Industrial Packaging

- Retail & E-commerce

- Electronics

By Distribution Channel

- Supermarkets & Hypermarkets

- Online Retail

- Specialty Stores

- Food Service Providers

- Direct B2B Sales

Regional Analysis

North America

North America accounted for approximately 28.1% of the global rigid tray market in 2025, with a projected CAGR of 6.4% from 2025 to 2034. The region benefits from strong demand in packaged food, pharmaceuticals, and e-commerce logistics. Increasing consumer preference for convenience foods and ready-to-eat meals continues to drive rigid tray adoption across retail chains and foodservice providers. Additionally, sustainability initiatives are encouraging the use of recyclable PET and molded fiber trays, especially in the United States and Canada.

The United States dominates the regional market due to its advanced packaging infrastructure and strong presence of major food brands. A key growth driver is the rapid expansion of online grocery delivery platforms, which require durable and tamper-resistant packaging formats. For example, subscription meal services increasingly rely on compartmentalized rigid trays to maintain freshness and portion control. The integration of smart packaging in pharmaceutical logistics also strengthens regional demand.

Europe

Europe held a market share of 24.7% in 2025, with a forecast CAGR of 6.2% through 2034. The region is strongly influenced by environmental regulations promoting recyclable and biodegradable packaging solutions. Countries such as Germany, France, and the UK are leading the adoption of sustainable rigid trays made from molded fiber and recycled plastics. The European market is also characterized by high demand for premium food packaging and strict food safety standards.

Germany leads the regional market, driven by its strong manufacturing base and advanced packaging technology ecosystem. A unique growth driver is the widespread adoption of circular economy practices in packaging production. For instance, supermarket chains in Germany are actively replacing plastic trays with compostable alternatives for meat and fresh produce. This regulatory and consumer-driven transition is reshaping packaging strategies across the region.

Asia Pacific

Asia Pacific dominated the global market with a 37.4% share in 2025 and is expected to grow at a CAGR of 7.8% during 2025–2034. Rapid urbanization, expanding middle-class population, and growing food delivery services are major drivers of demand. Countries such as China, India, Japan, and South Korea are witnessing significant growth in packaged food consumption and pharmaceutical logistics.

China remains the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026. A key growth driver is the massive expansion of online food delivery platforms and cold-chain logistics infrastructure. For example, Chinese e-commerce giants rely heavily on rigid trays for meal kits and fresh produce packaging, ensuring product quality during long-distance transportation.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the global market in 2025, with a projected CAGR of 6.5% through 2034. Growth is driven by increasing food import dependence, tourism-driven hospitality demand, and expanding retail infrastructure. Gulf countries such as the UAE and Saudi Arabia are witnessing strong adoption of rigid trays in premium food packaging and airline catering services.

The UAE leads the regional market due to its strong logistics hub and hospitality sector. A key driver is the expansion of cold-chain distribution systems supporting imported food products. For instance, airline catering services in Dubai increasingly use rigid trays for meal standardization and hygiene compliance.

Latin America

Latin America held a 3.0% market share in 2025, but is expected to register the fastest CAGR of 6.9% through 2034. Growth is driven by expanding retail modernization, rising packaged food consumption, and increasing e-commerce penetration. Brazil and Mexico are leading markets in the region, supported by growing urban populations and food delivery platforms.

Brazil dominates the regional market due to its large food processing industry. A unique growth factor is the expansion of supermarket chains adopting rigid trays for ready-to-eat and frozen food packaging. For example, Brazilian retailers are increasingly using recyclable PET trays to meet sustainability goals while supporting high-volume food distribution networks.

Competitive Landscape

The rigid tray market is moderately consolidated with key players focusing on sustainability, innovation, and capacity expansion. Leading companies include Amcor plc, Berry Global Inc., WestRock Company, DS Smith Plc, and Sonoco Products Company. Among these, Amcor plc is the market leader due to its extensive global footprint and strong portfolio of recyclable packaging solutions.

Companies are adopting strategies such as mergers, product innovation, and investment in bio-based materials. For example, several firms are expanding molded fiber production facilities to meet growing demand for sustainable trays. Recent developments include partnerships with food delivery platforms to design customized rigid packaging solutions and investments in AI-driven manufacturing systems to improve efficiency and reduce waste.

Key Players

- Amcor plc

- Berry Global Inc.

- WestRock Company

- DS Smith Plc

- Sonoco Products Company

- Smurfit Kappa Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Mondi Group

- Greiner Packaging

- Pactiv Evergreen Inc.

- Sabert Corporation

- Faerch A/S

- Placon Corporation

- Winpak Ltd.