Rigid Substrate Market Size and Growth

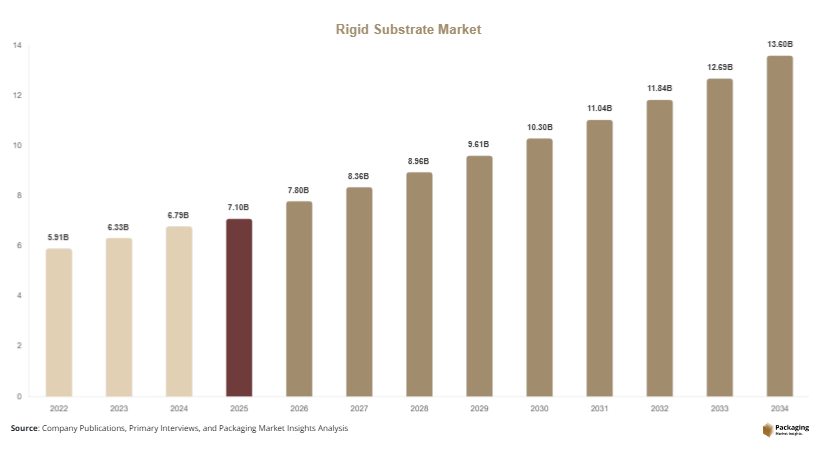

The global rigid substrate market size is estimated at approximately USD 7.1 billion in 2025 and is projected to reach around USD 7.8 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to reach nearly USD 14.6 billion, registering a compound annual growth rate (CAGR) of 7.2%. The rigid substrate market is witnessing steady expansion driven by rising demand across electronics, automotive, packaging, and industrial applications.

Rigid substrates are widely used as foundational materials in printed circuit boards, display panels, semiconductor packaging, and structural packaging applications. Their mechanical stability, thermal resistance, and dimensional precision make them essential in advanced manufacturing environments where reliability and durability are critical.

Key Highlights:

- The market size reached USD 7.1 billion in 2025, reflecting steady expansion across electronics, automotive, and industrial applications. This growth is supported by rising demand for high-performance electronic components globally.

- The market is expected to reach USD 14.6 billion by 2034, indicating strong long-term growth potential. Increasing use of advanced substrates in semiconductor and circuit applications is driving this expansion.

- The market is projected to register a CAGR of 7.2% during the forecast period from 2025 to 2034. Consistent demand from key end-use industries is supporting this stable growth trajectory.

- Strong demand from the electronics and automotive sectors is a key growth driver. Both industries rely heavily on rigid substrates for performance, stability, and thermal management.

- Increasing adoption in electric vehicles (EVs) and industrial automation systems is further boosting market growth. These applications require durable and high-precision substrate materials for reliable operation.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

One significant trend in the rigid substrate market is the increasing adoption of high-density interconnect (HDI) substrates in advanced electronics manufacturing. As devices become smaller and more powerful, manufacturers are shifting toward HDI designs that allow greater circuit density and improved electrical performance. Rigid substrates used in these applications are engineered with finer line spacing and multilayer architectures. This trend is particularly visible in smartphones, tablets, and high-performance computing devices where space optimization is critical. The demand for HDI-compatible rigid substrates is expected to continue rising as semiconductor complexity increases.

Another important trend is the growing integration of ceramic-based rigid substrates in high-temperature and high-power applications. Industries such as automotive electronics, aerospace systems, and industrial power modules require substrates that can withstand extreme thermal and mechanical stress. Ceramic substrates such as aluminum nitride and alumina are gaining traction due to their excellent thermal conductivity and insulation properties. Manufacturers are investing in advanced ceramic processing technologies to enhance performance and reduce production costs. This trend is reshaping substrate selection in high-reliability environments.

Market Drivers

A major driver of the rigid substrate market is the rapid growth of the consumer electronics industry. The increasing penetration of smartphones, smart wearables, gaming devices, and connected appliances is creating strong demand for reliable circuit board materials. Rigid substrates provide the structural base for these devices, ensuring electrical stability and thermal management. As device functionality expands and processing power increases, the need for high-quality substrates becomes more critical. This growth is further supported by continuous product innovation cycles and frequent device upgrades.

Another key driver is the expansion of electric mobility and automotive electronics. Modern vehicles are increasingly equipped with advanced driver assistance systems, infotainment platforms, and battery management systems. These technologies rely heavily on rigid substrates for stable performance under varying temperature and vibration conditions. The transition toward electric and autonomous vehicles is accelerating substrate demand across automotive manufacturing ecosystems. As vehicle architectures become more electronically driven, rigid substrates play an increasingly central role in system reliability.

Market Restraint

One of the primary restraints in the rigid substrate market is the high cost of advanced materials and manufacturing processes. Production of high-performance substrates, especially ceramic and multilayer variants, involves complex fabrication techniques and expensive raw materials. This increases overall production costs and limits adoption in price-sensitive applications.

The impact of this restraint is particularly visible in emerging markets where manufacturers prioritize cost efficiency over advanced performance features. For example, small-scale electronics producers may opt for lower-cost flexible alternatives instead of rigid substrates in non-critical applications. Additionally, fluctuations in raw material prices such as copper, glass fiber, and ceramic compounds can further affect profitability. This cost sensitivity can slow market penetration in certain industrial segments.

Market Opportunities

One major opportunity in the rigid substrate market lies in the rapid expansion of 5G infrastructure and next-generation communication technologies. 5G networks require high-frequency, low-loss electronic components that depend on advanced rigid substrates. These substrates are essential in base stations, antennas, and signal processing units. As global telecom operators continue expanding 5G coverage, demand for high-performance substrate materials is expected to increase significantly. Manufacturers developing low-loss dielectric materials are well positioned to benefit from this trend.

Another promising opportunity is the growth of renewable energy systems and smart grid infrastructure. Solar inverters, wind turbine controllers, and energy storage systems require robust electronic components capable of operating in harsh environments. Rigid substrates offer the durability and thermal stability needed for such applications. As governments worldwide invest in clean energy transitions, the demand for reliable electronic infrastructure will continue to rise, creating new avenues for substrate manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 7.1 Billion |

| Market Size in 2026 | USD 7.8 Billion |

| Market Size in 2034 | USD 14.6 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Regional Analysis

North America

North America accounted for approximately 28% of the global rigid substrate market in 2025 and is expected to grow at a CAGR of 6.8% during the forecast period. The region benefits from a strong semiconductor industry and high adoption of advanced electronics across automotive and industrial sectors.

The United States dominates the regional market due to its leadership in electronics innovation and semiconductor design. A key growth factor is the rapid expansion of electric vehicle manufacturing, which is driving demand for high-performance rigid substrates in battery and control systems.

Europe

Europe held around 23% of the market share in 2025 and is projected to grow at a CAGR of 6.5%. The region’s strong automotive industry and emphasis on industrial automation support steady demand for rigid substrates.

Germany leads the European market due to its advanced manufacturing base. A unique growth factor is the integration of Industry 4.0 technologies, which is increasing the use of smart sensors and electronic control systems requiring durable substrate materials.

Asia Pacific

Asia Pacific accounted for approximately 34% of the global market share in 2025 and is expected to grow at a CAGR of 8.1%. The region is the largest manufacturing hub for electronics and semiconductors.

China dominates the regional market due to its massive electronics production ecosystem. A key growth factor is the expansion of consumer electronics exports, which is driving demand for cost-efficient and high-performance rigid substrates.

Middle East & Africa

The Middle East & Africa region held around 8% of the market share in 2025 and is projected to grow at a CAGR of 7.0%. The market is supported by growing industrialization and investments in telecommunications infrastructure.

The United Arab Emirates is a leading market in the region. A unique growth factor is the expansion of smart city initiatives, which require advanced electronic systems built on rigid substrate technologies.

Latin America

Latin America accounted for approximately 7% of the market share in 2025 and is expected to grow at a CAGR of 6.9%. The region is experiencing gradual growth in electronics manufacturing and automotive assembly.

Brazil dominates the regional market due to its expanding industrial base. A key growth factor is the increasing adoption of consumer electronics and telecommunications devices, which is boosting demand for rigid substrates.

Rigid Substrate Market Segmentations

By Material Type

- Organic Substrates

- Ceramic Substrates

- Metal-Based Substrates

By Application

- Printed Circuit Boards (PCBs)

- Semiconductor Packaging

- LED and Display Systems

By End-Use Industry

- Consumer Electronics

- Automotive Electronics

- Industrial Equipment

- Telecommunications

Segmental Analysis

By Material Type

Organic substrates dominated the market in 2024, accounting for approximately 56% of the total share. These include epoxy resin-based laminates and glass-reinforced materials widely used in printed circuit boards. Their cost-effectiveness, mechanical stability, and compatibility with mass production processes make them highly preferred in consumer electronics and industrial applications. Organic substrates are extensively used in smartphones, laptops, and household electronics due to their balance of performance and affordability. Manufacturers continue to enhance resin formulations to improve heat resistance and signal integrity.

Ceramic substrates are the fastest-growing segment, expected to register a CAGR of 8.3%. These substrates offer superior thermal conductivity and electrical insulation, making them ideal for high-power and high-frequency applications. Growth is driven by increasing use in electric vehicles, aerospace electronics, and power modules. As device power density increases, ceramic substrates are becoming essential for heat dissipation and reliability. Continuous advancements in ceramic processing technologies are also reducing production costs, further supporting adoption.

By Application

Printed circuit boards (PCBs) dominated the market in 2024, accounting for approximately 60% of total demand. PCBs form the backbone of most electronic devices, and rigid substrates are widely used in their production. The increasing complexity of electronic circuits and miniaturization of devices are driving demand for advanced substrate materials. PCBs using rigid substrates are critical in consumer electronics, automotive systems, and industrial machinery.

Semiconductor packaging is the fastest-growing application segment, projected to register a CAGR of 8.6%. The rise of advanced computing, artificial intelligence, and 5G infrastructure is increasing demand for high-performance semiconductor packaging solutions. Rigid substrates provide the structural integrity and thermal management needed for chip packaging. Growth is supported by continuous innovation in chip design and increasing demand for high-speed data processing.

By End-Use

Consumer electronics dominated the market in 2024, accounting for approximately 54% of total share. Smartphones, laptops, tablets, and wearable devices heavily rely on rigid substrates for circuit integration. Rapid product cycles and increasing device functionality are driving continuous demand for high-quality substrate materials.

Automotive electronics is the fastest-growing end-use segment, with a CAGR of 8.2%. The shift toward electric and autonomous vehicles is increasing reliance on electronic systems such as ADAS, infotainment, and battery management systems. Rigid substrates ensure reliability under harsh automotive conditions, supporting their growing adoption.

Competitive Landscape

The rigid substrate market is moderately consolidated, with major players focusing on technological innovation, capacity expansion, and strategic partnerships. Companies are investing in advanced material research to improve thermal and electrical performance.

Isola Group is a key leader in the market, known for its high-performance laminate materials used in advanced electronics. The company recently expanded its production facilities to meet rising demand from automotive and semiconductor industries. Other players are focusing on developing low-loss dielectric materials and high-frequency substrates to support 5G and AI applications.

Key Players List

- Isola Group

- Rogers Corporation

- Panasonic Holdings Corporation

- Shengyi Technology Co., Ltd.

- TUC (Taiwan Union Technology Corporation)

- Nan Ya Plastics Corporation

- ITEQ Corporation

- Panasonic Electronic Materials

- Doosan Corporation Electro-Materials

- Wazam New Material

- Kingboard Holdings Limited

- MEIKO Electronics Co., Ltd.

- Shengyi Electronics

- Elite Material Co., Ltd.

- Ventec International Group