Rigid Packaging Market Report Size and Growth

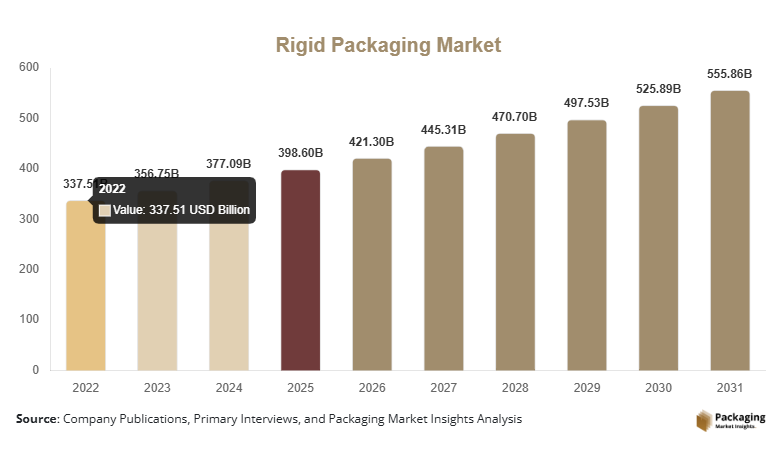

The Rigid Packaging Market was valued at USD 398.6 billion in 2025 and is projected to reach USD 552.4 billion by 2030, expanding at a CAGR of 5.7% during the forecast period (2025–2031). Rigid packaging refers to packaging solutions that maintain their shape and structural integrity during handling, storage, and transportation. Common formats include bottles, containers, trays, cans, and jars manufactured using materials such as plastic, metal, glass, and paperboard.

The global market has experienced steady expansion due to increasing demand from food and beverage manufacturers, pharmaceutical companies, and personal care brands that require durable packaging with extended shelf-life protection. Rigid packaging solutions offer superior barrier protection, enhanced product stability, and convenient transportation advantages compared to flexible alternatives. Additionally, improvements in automated manufacturing and container molding technologies have improved packaging consistency and reduced production costs.

A major global factor supporting market growth has been the rapid expansion of packaged food consumption, particularly in urban regions. Changing lifestyles, increasing working populations, and rising demand for ready-to-eat meals have significantly increased the need for reliable rigid containers capable of preserving product freshness and preventing contamination. Food processors and beverage companies increasingly rely on rigid packaging formats to meet safety standards and maintain product quality across long distribution chains.

Key Highlights

- Asia Pacific dominated the market with 38.2% share in 2025, while Latin America is projected to register the fastest growth with a CAGR of 6.8%.

- By material, Plastic accounted for the largest share at 44.6%, while Paperboard is projected to grow fastest with 7.1% CAGR.

- By product type, Bottles & Containers held the dominant share, while Rigid trays are projected to expand at 6.9% CAGR.

- China represented the leading national market, valued at USD 71.4 billion in 2025 and estimated to reach USD 75.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable Rigid Packaging

Sustainability initiatives have become a defining trend shaping the Rigid Packaging Market. Manufacturers and brand owners are increasingly focusing on recyclable, reusable, and biodegradable materials to reduce environmental impact. Governments across multiple regions have implemented packaging waste regulations that encourage the use of recyclable plastics, lightweight glass containers, and paperboard alternatives.

Companies are introducing rigid packaging formats made from recycled PET (rPET), post-consumer recycled plastics, and molded fiber solutions. These innovations are helping reduce raw material consumption while meeting consumer demand for environmentally responsible packaging. Additionally, manufacturers are redesigning containers to use less material without compromising durability, which lowers transportation costs and carbon emissions.

Smart Packaging and Advanced Manufacturing Technologies

Technological advancements are transforming the rigid packaging manufacturing ecosystem. Automation, digital printing, and smart packaging technologies are increasingly integrated into production processes. Smart packaging elements such as QR codes, tamper-evident closures, and freshness indicators are being incorporated into rigid packaging formats to enhance consumer engagement and supply chain transparency.

Advanced molding techniques, including injection molding and blow molding, allow manufacturers to produce high-precision containers at scale. These innovations enable faster production cycles and improved packaging uniformity. As brands seek stronger differentiation on retail shelves, customized rigid packaging designs and digitally printed containers are becoming increasingly prevalent across food, beverage, and personal care industries.

Market Drivers

Rising Demand from Food and Beverage Industry

The expansion of global food processing industries has strongly supported the growth of the Rigid Packaging Market. Food manufacturers require packaging solutions that ensure structural protection, extended shelf life, and contamination prevention during distribution.

Rigid packaging formats such as plastic containers, glass jars, and metal cans are widely used in packaged foods, dairy products, sauces, beverages, and ready-to-eat meals. Their ability to maintain product integrity during storage and transportation makes them essential in large-scale food distribution networks. As consumer demand for convenience foods increases globally, the need for durable packaging formats continues to rise.

Expansion of Pharmaceutical and Healthcare Packaging

Another significant driver supporting the Rigid Packaging Market is the rapid expansion of pharmaceutical manufacturing. Medicines, vaccines, and healthcare products require packaging solutions that maintain strict safety and hygiene standards.

Rigid containers such as plastic bottles, glass vials, and blister packs help protect pharmaceutical products from contamination, moisture, and external damage. Growing healthcare spending and the expansion of pharmaceutical manufacturing facilities across emerging markets are increasing the demand for reliable rigid packaging solutions that comply with regulatory requirements.

Market Restraint

Environmental Concerns and Plastic Waste Regulations

Despite strong demand across multiple industries, the Rigid Packaging Market faces challenges related to environmental sustainability and plastic waste management. Regulatory authorities in many countries have introduced strict policies aimed at reducing plastic consumption and improving recycling infrastructure.

Plastic-based rigid packaging formats account for a significant share of the market, particularly in food and beverage applications. However, concerns regarding landfill accumulation and ocean pollution have prompted governments to introduce restrictions on single-use plastics and promote alternative packaging materials.

Compliance with evolving environmental regulations requires manufacturers to invest heavily in sustainable materials, recycling programs, and production upgrades. These investments can increase operational costs and reduce profit margins for packaging companies. Additionally, consumers are increasingly shifting toward environmentally friendly packaging solutions, which may create pressure on manufacturers that rely heavily on traditional plastic packaging formats.

As sustainability requirements continue to evolve, companies in the rigid packaging ecosystem must develop innovative materials and circular packaging solutions to maintain market competitiveness.

Market Opportunities

Growth of E-Commerce Packaging Applications

The rapid growth of global e-commerce platforms is creating new opportunities for the Rigid Packaging Market. Online retail requires packaging solutions capable of protecting products during long shipping distances and multiple handling stages.

Rigid packaging containers, protective trays, and molded containers are increasingly used to safeguard products such as electronics, cosmetics, and food products during delivery. As e-commerce continues to expand in emerging economies, demand for durable packaging solutions is expected to increase significantly.

Expansion of Recyclable and Paper-Based Packaging

The increasing shift toward sustainable packaging materials presents another opportunity for market expansion. Paperboard-based rigid packaging formats are gaining traction as eco-friendly alternatives to plastic containers.

Many consumer goods companies are adopting recyclable rigid packaging to meet sustainability commitments and improve brand perception among environmentally conscious consumers. Innovations in molded fiber technology and reinforced paperboard containers are enabling manufacturers to produce rigid packaging formats with comparable durability to traditional materials.

These developments are expected to create new revenue streams for packaging manufacturers that invest in sustainable material innovations

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 398.6 Billion |

| Market Size in 2026 | USD 421.3 Billion |

| Market Size in 2031 | USD 554.6 Billion |

| CAGR | 5.7% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Plastic had accounted for the largest share of 44.6% of the Rigid Packaging Market in 2024. The dominance of plastic packaging was attributed to its lightweight structure, durability, and cost efficiency. Plastic containers are widely used in beverage packaging, dairy products, household chemicals, and personal care items. Their ability to be molded into complex shapes and provide strong barrier protection has made plastic materials highly suitable for rigid packaging applications.

Paperboard is projected to be the fastest-growing material segment with a CAGR of 7.1% during the forecast period. The increasing shift toward sustainable packaging solutions will support the adoption of paper-based rigid containers. Innovations in molded fiber and reinforced paperboard packaging will enable manufacturers to produce durable containers that meet environmental regulations and consumer sustainability preferences.

By Product Type

Bottles and containers represented the largest product segment, accounting for 39.5% of the Rigid Packaging Market share in 2024. These packaging formats are widely used across beverage, food, pharmaceutical, and personal care industries. Their rigid structure ensures product protection during transportation and storage, making them suitable for large-scale distribution networks.

Rigid trays are projected to become the fastest-growing product type with a CAGR of 6.9% during the forecast period. These trays are widely used in ready-to-eat food packaging, bakery products, and meat packaging. Their ability to maintain product arrangement and prevent contamination will support growing demand in food processing industries.

By End-Use Industry

The food and beverage industry had accounted for 41.8% of the Rigid Packaging Market share in 2024, making it the dominant end-use segment. Rigid containers, bottles, and cans are widely used to package beverages, dairy products, sauces, and packaged meals. These packaging formats help maintain freshness and protect products during transportation across long supply chains.

The pharmaceutical industry is projected to be the fastest-growing end-use segment with a CAGR of 6.5% during the forecast period. Rising healthcare demand and expanding pharmaceutical production will increase the need for rigid packaging formats such as medicine bottles, vials, and containers that meet regulatory safety standards.

Rigid Packaging Market Segmentations

By Material

- Plastic

- Metal

- Glass

- Paperboard

- Others

By Product Type

- Bottles & Containers

- Trays

- Cans

- Jars

- Caps & Closures

By End-Use Industry

- Food & Beverage

- Pharmaceutical

- Personal Care & Cosmetics

- Household Chemicals

- Industrial

Regional Analysis

North America

North America accounted for 22.5% of the global Rigid Packaging Market share in 2025. The regional market had been supported by strong demand from food processing, pharmaceutical manufacturing, and consumer goods industries. Over the forecast period, the regional market will expand at a CAGR of 4.9% between 2025 and 2033.

The United States dominated the North American market due to its well-established packaging manufacturing ecosystem and large consumer goods industry. The country’s growth has been supported by high consumption of packaged beverages and ready-to-eat meals. Major food processing companies rely heavily on rigid containers to maintain product safety and shelf life. Additionally, the presence of advanced packaging manufacturing facilities and automation technologies has supported production efficiency across the region.

Europe

Europe represented 20.7% of the global Rigid Packaging Market share in 2025. The market had been driven by strong regulatory standards for food safety and packaging quality. Over the forecast period, the regional market will grow at a CAGR of 4.6% between 2025 and 2033.

Germany emerged as the dominant country within the European rigid packaging industry. The country’s packaging manufacturing sector has benefited from strong industrial infrastructure and advanced recycling systems. German packaging producers have focused on developing recyclable rigid containers made from aluminum, glass, and recycled plastics. Additionally, increasing demand from pharmaceutical manufacturers has contributed to the growth of rigid packaging solutions in the region.

Asia Pacific

Asia Pacific held the largest share of the Rigid Packaging Market at 38.2% in 2025. The region had been driven by rapid industrialization, urbanization, and increasing consumption of packaged goods. During the forecast period, the regional market will expand at a CAGR of 6.3% between 2025 and 2033.

China dominated the regional market due to its large manufacturing base and extensive consumer goods production capacity. The country has become a global hub for food processing, beverage manufacturing, and consumer product packaging. Rapid expansion of urban retail networks and convenience stores has increased the demand for rigid packaging containers used in beverages, dairy products, and packaged foods.

Middle East & Africa

The Middle East & Africa accounted for 9.8% of the global Rigid Packaging Market share in 2025. The market had been influenced by increasing demand for packaged food and beverage products. Over the forecast period, the regional market will grow at a CAGR of 5.4% between 2025 and 2033.

Saudi Arabia represented the leading country within the regional market. The country’s growth has been supported by expanding food processing industries and increasing investments in local manufacturing. Government initiatives aimed at strengthening domestic food production have increased the demand for packaging solutions capable of preserving product quality in hot climates.

Latin America

Latin America captured 8.8% of the global Rigid Packaging Market share in 2025. The regional market had been supported by expanding beverage production and consumer goods manufacturing. Over the forecast period, the market will grow at the fastest CAGR of 6.8% between 2025 and 2033.

Brazil dominated the Latin American market due to its large food and beverage manufacturing sector. The country’s beverage industry relies heavily on rigid plastic bottles and aluminum cans for product distribution. Increasing urban populations and growing supermarket chains have strengthened the demand for rigid packaging solutions across the region.

Competitive Landscape

The Rigid Packaging Market is characterized by the presence of several global packaging manufacturers that focus on expanding production capacity, developing sustainable materials, and forming strategic partnerships with consumer goods companies.

Amcor plc has emerged as a leading company in the market due to its broad packaging portfolio and strong global manufacturing network. The company recently expanded its recyclable rigid packaging product line to support sustainability initiatives across food and beverage industries.

Other key players include Berry Global Inc., Ball Corporation, Silgan Holdings Inc., and Crown Holdings Inc. These companies are investing in advanced manufacturing technologies and recyclable packaging materials to strengthen their market position. Strategic acquisitions and product innovations remain key competitive strategies among major rigid packaging manufacturers.

Key Players in the Rigid Packaging Market

- Amcor plc

- Berry Global Inc.

- Ball Corporation

- Crown Holdings Inc.

- Silgan Holdings Inc.

- Sonoco Products Company

- Ardagh Group

- Alpla Group

- Plastipak Holdings Inc.

- DS Smith plc

- O-I Glass Inc.

- Graham Packaging Company

- Reynolds Group Holdings

- Mauser Packaging Solutions

- Toyo Seikan Group Holdings