Rigid IBC Market Size and Growth

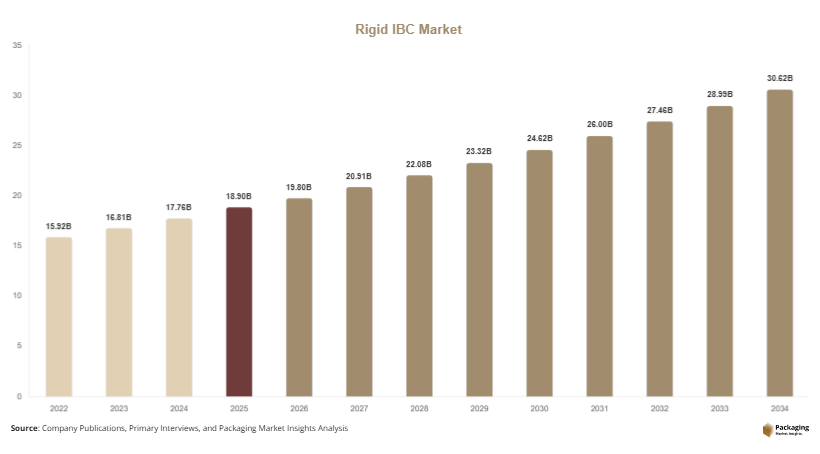

The global rigid IBC market size for rigid IBCs was valued at approximately USD 18.9 billion in 2025 and is expected to reach USD 19.8 billion in 2026, with projections indicating growth to USD 30.6 billion by 2034, expanding at a CAGR of 5.6% during the forecast period from 2025 to 2034. The rigid IBC market is experiencing steady growth driven by rising demand for efficient bulk liquid and semi-solid storage and transportation solutions across industries such as chemicals, food & beverages, pharmaceuticals, and agriculture. Intermediate Bulk Containers (IBCs) offer a balance between durability, reusability, and cost efficiency, making them a preferred choice for industrial logistics.

One of the primary growth factors is the increasing demand from the chemical and petrochemical industries, where rigid IBCs are widely used for safe storage and transportation of hazardous and non-hazardous liquids. Their standardized design ensures compliance with international safety regulations. Another important factor is the expansion of global trade and bulk logistics operations, where efficient handling and storage solutions are essential for reducing operational costs and improving supply chain efficiency. Rigid IBCs provide stackability and compatibility with automated handling systems, enhancing logistics performance.

Key Market Insights:

- Asia Pacific dominated the market with a 39.6% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.3%.

- Plastic rigid IBCs led the type segment with a 46.8% share, while composite IBCs are expected to grow at a CAGR of 6.4%.

- Industrial packaging dominated with a 54.2% share, while food-grade packaging is forecasted to grow at a CAGR of 6.1%.

- Chemical applications led the segment with 41.7% share, while pharmaceutical applications are expected to grow at a CAGR of 6.5%.

- China remained the dominant country with a market size of USD 4.8 billion in 2025 and USD 5.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Preference for Reusable and Sustainable Bulk Containers

Sustainability trends are significantly influencing the rigid IBC market, with companies increasingly focusing on reusable packaging solutions to minimize environmental impact. Rigid IBCs offer long service life and can be reconditioned multiple times, reducing the need for single-use packaging. Industries such as chemicals and food processing are adopting these containers to meet sustainability goals and regulatory requirements. Manufacturers are also integrating recyclable materials and designing IBCs with reduced material usage while maintaining structural integrity. This trend is expected to strengthen as organizations prioritize circular economy practices and seek to lower carbon emissions.

Technological Advancements in Container Design and Safety Features

Technological innovation is another key trend shaping the rigid IBC market. Manufacturers are introducing advanced designs with improved safety features, including leak-proof valves, anti-static materials, and tamper-evident closures. These enhancements are particularly important for transporting hazardous chemicals and sensitive pharmaceutical products. Additionally, smart tracking technologies, such as RFID tags and IoT-enabled monitoring systems, are being integrated into IBCs to improve supply chain visibility. These advancements are enhancing operational efficiency and ensuring compliance with safety regulations, driving market growth.

Market Drivers

Growth of Chemical and Petrochemical Industries

The growth of the chemical and petrochemical industries is a major driver of the rigid IBC market. These industries require reliable and safe packaging solutions for transporting bulk liquids, including hazardous materials. Rigid IBCs provide durability, chemical resistance, and compliance with international safety standards, making them suitable for such applications. Increasing production of chemicals and expansion of industrial activities globally are driving demand for bulk packaging solutions. Additionally, the need for efficient logistics and storage solutions is further supporting market growth.

Expansion of Global Logistics and Supply Chain Networks

The expansion of global logistics and supply chain networks is another significant driver of the rigid IBC market. As international trade continues to grow, the demand for efficient bulk packaging solutions is increasing. Rigid IBCs offer advantages such as stackability, ease of handling, and compatibility with automated systems, making them ideal for logistics operations. Their ability to reduce transportation costs and improve storage efficiency is encouraging adoption across industries. The growth of e-commerce and industrial distribution networks is also contributing to market expansion.

Market Restraint

High Initial Investment and Maintenance Costs

One of the key restraints in the rigid IBC market is the high initial investment required for purchasing these containers. Compared to flexible packaging solutions, rigid IBCs involve higher upfront costs, which can be a barrier for small and medium-sized enterprises. Additionally, maintenance and cleaning processes for reusable IBCs can add to operational expenses. For example, industries handling hazardous chemicals require thorough cleaning and compliance with safety standards, increasing overall costs. While the long-term benefits of durability and reusability can offset these expenses, cost-sensitive industries may hesitate to adopt rigid IBCs, limiting market growth.

Market Opportunities

Rising Demand in Emerging Economies

Emerging economies present significant opportunities for the rigid IBC market due to rapid industrialization and expansion of manufacturing sectors. Countries in Asia Pacific, Latin America, and Africa are witnessing increased demand for bulk packaging solutions driven by growth in chemical, food, and agricultural industries. The development of infrastructure and logistics networks is further supporting market expansion. Companies that invest in these regions can benefit from rising demand and favorable economic conditions.

Increasing Adoption in Food and Pharmaceutical Industries

The growing adoption of rigid IBCs in food and pharmaceutical industries offers promising opportunities for market growth. These industries require high standards of hygiene and safety for packaging and transportation. Rigid IBCs provide contamination-free storage and comply with regulatory requirements. The increasing demand for processed food and pharmaceutical products is driving the need for reliable bulk packaging solutions. Manufacturers are developing food-grade and pharmaceutical-grade IBCs to cater to this demand, creating new growth avenues.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.9 Billion |

| Market Size in 2026 | USD 19.8 Billion |

| Market Size in 2034 | USD 30.6 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic rigid IBCs dominated the market in 2024, accounting for approximately 46.8% of the total share. These containers are widely used due to their lightweight nature, chemical resistance, and cost-effectiveness. They are suitable for transporting a wide range of liquids, including chemicals and food products. Plastic IBCs are also easy to clean and reuse, making them a preferred choice across industries. Their compatibility with automated handling systems further supports their adoption.

Composite IBCs are expected to grow at the fastest CAGR of 6.4% during the forecast period. These containers combine plastic inner containers with metal cages, providing enhanced strength and durability. The increasing demand for safe transportation of hazardous materials is driving the adoption of composite IBCs. Their ability to withstand harsh conditions and provide additional protection is supporting growth in this segment.

By Application

Chemical applications dominated the market in 2024, holding a share of 41.7%. Rigid IBCs are widely used for transporting and storing chemicals due to their durability and compliance with safety standards. The growth of the chemical industry and increasing production of industrial chemicals are driving demand in this segment. Additionally, the need for efficient logistics solutions is supporting the adoption of rigid IBCs.

Pharmaceutical applications are expected to grow at a CAGR of 6.5%. The increasing demand for pharmaceutical products and strict regulatory requirements are driving the need for safe and hygienic packaging solutions. Rigid IBCs provide contamination-free storage and transportation, making them suitable for pharmaceutical applications. Manufacturers are focusing on developing specialized containers to meet industry requirements.

By End-Use

The industrial sector accounted for the largest share of 54.2% in 2024. Rigid IBCs are widely used in industries such as chemicals, oil and gas, and manufacturing for bulk storage and transportation. The increasing demand for efficient packaging solutions and the growth of industrial activities are driving demand in this segment. Additionally, the need for cost-effective and durable packaging is supporting the adoption of rigid IBCs.

The food and beverage sector is projected to grow at a CAGR of 6.1%. The increasing demand for processed and packaged food products is driving the need for bulk packaging solutions. Rigid IBCs provide safe and hygienic storage, making them suitable for food applications. The adoption of food-grade containers is supporting growth in this segment.

Rigid IBC Market Segmentations

By Product Type

- Plastic Rigid IBCs

- Metal Rigid IBCs

- Composite Rigid IBCs

- Food-Grade Rigid IBCs

By Application

- Chemicals

- Food & Beverage

- Pharmaceuticals

- Agriculture

By Distribution Channel

- Direct Sales

- Distributors & Wholesalers

- Online B2B Platforms

- Industrial Supply Networks

Regional Analysis

North America

North America accounted for approximately 24.2% of the global rigid IBC market share in 2025 and is expected to grow at a CAGR of 5.2% during the forecast period. The region’s growth is driven by strong demand from chemical, food, and pharmaceutical industries. Advanced logistics infrastructure and strict safety regulations are encouraging the adoption of rigid IBCs. The presence of major packaging manufacturers is also supporting market development.

The United States dominates the North American market due to its large industrial base and advanced supply chain networks. A unique growth factor in this region is the increasing adoption of automated material handling systems, which require standardized bulk containers. This is driving demand for rigid IBCs.

Europe

Europe held a market share of approximately 22.5% in 2025 and is projected to grow at a CAGR of 5.1%. The region is characterized by strict environmental and safety regulations, which are driving the adoption of reusable packaging solutions. Industries such as chemicals and pharmaceuticals are major consumers of rigid IBCs. Technological advancements in packaging materials are also contributing to market growth.

Germany is the leading country in Europe due to its strong industrial base and focus on innovation. A unique growth factor is the increasing emphasis on sustainable packaging solutions to comply with environmental regulations. This is driving demand for rigid IBCs.

Asia Pacific

Asia Pacific dominated the rigid IBC market in 2025 with a share of 39.6% and is expected to grow at a CAGR of 6.2%. Rapid industrialization, urbanization, and expansion of manufacturing sectors are driving market growth. The region is also witnessing increased demand from chemical and food industries. The growth of logistics and supply chain networks is further supporting market expansion.

China is the dominant country in Asia Pacific, supported by its large manufacturing and chemical industries. A key growth factor is the increasing export of industrial goods, which requires efficient bulk packaging solutions. This is driving the adoption of rigid IBCs.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5.8% of the global market share in 2025 and is projected to grow at a CAGR of 5.5%. The market is driven by increasing industrial activities and expansion of the oil and gas sector. Demand for bulk packaging solutions is rising due to growth in export-oriented industries.

Saudi Arabia is a leading market in this region, supported by its strong petrochemical industry. A unique growth factor is the increasing demand for safe transportation of chemicals, which is driving the adoption of rigid IBCs.

Latin America

Latin America held a market share of approximately 7.9% in 2025 and is expected to grow at the fastest CAGR of 6.3%. The region’s growth is driven by rising industrial activities and increasing demand for bulk packaging solutions. The expansion of logistics infrastructure is also supporting market development.

Brazil is the dominant country in Latin America, driven by its large agricultural and industrial sectors. A key growth factor is the increasing demand for efficient packaging solutions for export activities. This is driving the adoption of rigid IBCs.

Competitive Landscape

The rigid IBC market is moderately competitive, with key players focusing on product innovation, sustainability, and strategic partnerships. Companies are investing in research and development to create advanced containers with improved durability and safety features. Expansion into emerging markets and development of customized solutions are common strategies among market participants.

Mauser Packaging Solutions is recognized as a leading player in the market, known for its extensive product portfolio and global presence. The company recently introduced reconditioned rigid IBCs to promote sustainability and reduce environmental impact. Other major players are also focusing on enhancing their product offerings and expanding production capacities to meet growing demand.

Key Players List

- Mauser Packaging Solutions

- SCHÜTZ GmbH & Co. KGaA

- Greif Inc.

- Berry Global Inc.

- Time Technoplast Ltd.

- Snyder Industries Inc.

- Hoover Ferguson Group Inc.

- Thielmann US LLC

- Schäfer Werke GmbH

- Custom Metalcraft Inc.

- Precision IBC Inc.

- Finncont Oy

- Qiming Packaging L.L.C.

- Pensteel Ltd.

- Envirotainer AB