Rigid Food Packaging Market Size and Growth

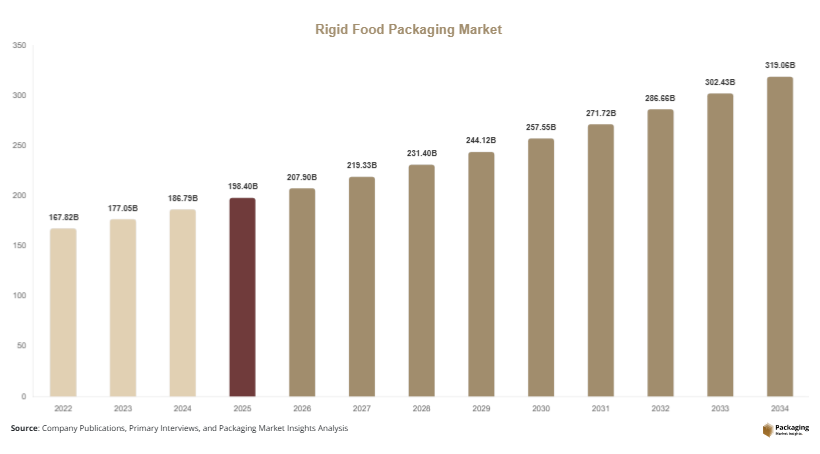

The global rigid food packaging market size was valued at approximately USD 198.4 billion in 2025 and is projected to reach USD 207.9 billion in 2026, further growing to USD 318.6 billion by 2034, at a CAGR of 5.5% during the forecast period from 2025 to 2034. Rigid packaging formats such as bottles, jars, trays, containers, and cans are widely used to preserve food quality, extend shelf life, and ensure product safety during transportation and storage. The rigid food packaging market is expanding steadily as demand rises for durable, protective, and hygienic packaging solutions across the global food industry.

One of the key growth factors is the increasing demand for processed and packaged food products, driven by urbanization, changing lifestyles, and rising disposable incomes. Consumers are seeking convenient and ready-to-eat food options, which require reliable packaging solutions that maintain freshness and quality. Another important factor is the growth of the food delivery and e-commerce sector, which requires sturdy packaging to prevent leakage, contamination, and damage during transit. Rigid packaging materials provide structural integrity, making them suitable for such applications.

Key Market Insights:

- Asia Pacific dominated the market with a 39.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.1%.

- Plastic containers led the type segment with a 42.6% share, while glass packaging is expected to grow at a CAGR of 5.9%.

- Plastic materials dominated with a 51.2% share, while metal packaging is forecasted to grow at a CAGR of 5.7%.

- Food & beverage applications led the segment with 46.3% share, while ready-to-eat meals are expected to grow at a CAGR of 6.2%.

- China remained the dominant country with a market size of USD 36.5 billion in 2025 and USD 38.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Packaging Materials

Sustainability is shaping the rigid food packaging market as manufacturers and consumers focus on reducing environmental impact. Companies are shifting toward recyclable materials such as glass, aluminum, and recyclable plastics to comply with regulatory requirements and meet consumer expectations. The use of post-consumer recycled content in packaging is increasing, which helps reduce waste and lower carbon emissions. Additionally, innovations in biodegradable and compostable materials are gaining attention. Food brands are incorporating eco-friendly packaging solutions to strengthen their sustainability credentials, which is influencing purchasing decisions and driving market demand.

Growth in Smart and Functional Packaging Technologies

The integration of smart and functional packaging technologies is becoming a key trend in the rigid food packaging market. Features such as tamper-evident closures, freshness indicators, and QR codes are being incorporated into packaging to enhance consumer safety and engagement. These technologies help monitor product quality and provide information about storage conditions and shelf life. Additionally, advancements in barrier technologies are improving the protection of food products against moisture, oxygen, and contamination. The adoption of smart packaging is increasing across premium and perishable food segments, contributing to market growth.

Market Drivers

Rising Demand for Processed and Convenience Foods

The increasing demand for processed and convenience foods is a major driver of the rigid food packaging market. Busy lifestyles and urbanization are encouraging consumers to opt for ready-to-eat and easy-to-prepare food products. These products require durable packaging solutions that maintain freshness and prevent contamination. Rigid packaging formats such as containers and trays provide structural strength and protection, making them suitable for these applications. Additionally, the growth of the food service industry is further supporting demand for rigid packaging solutions.

Expansion of Food Delivery and E-commerce Channels

The rapid expansion of food delivery services and e-commerce platforms is driving demand for rigid food packaging. Online food ordering and home delivery require packaging that can withstand handling and transportation without compromising product quality. Rigid packaging materials provide durability and leak resistance, ensuring safe delivery of food products. The increasing popularity of meal kits and online grocery shopping is further contributing to market growth. Companies are focusing on developing packaging solutions that meet the specific requirements of e-commerce and delivery services.

Market Restraint

Environmental Concerns and Regulatory Pressure on Plastic Usage

Environmental concerns related to plastic waste and increasing regulatory pressure are significant restraints for the rigid food packaging market. Many rigid packaging products are made from plastic, which contributes to environmental pollution if not properly managed. Governments are implementing regulations to reduce plastic usage and promote recycling, which is impacting the production and use of plastic packaging. For example, restrictions on single-use plastics are encouraging manufacturers to explore alternative materials. However, transitioning to sustainable materials can be costly and may require significant changes in production processes. This creates challenges for companies in maintaining cost efficiency while complying with regulations.

Market Opportunities

Development of Lightweight and Sustainable Packaging Solutions

The development of lightweight and sustainable packaging solutions presents significant opportunities for the rigid food packaging market. Manufacturers are focusing on reducing material usage while maintaining packaging strength and performance. Lightweight packaging helps reduce transportation costs and environmental impact. Additionally, the use of recyclable and biodegradable materials is gaining traction, providing opportunities for innovation. Companies that invest in sustainable packaging technologies can gain a competitive advantage in the market.

Growth in Emerging Markets and Changing Consumer Preferences

Emerging markets offer substantial growth opportunities for the rigid food packaging industry. Rapid urbanization, rising disposable incomes, and changing consumer preferences are driving demand for packaged food products in regions such as Asia Pacific, Latin America, and Africa. The expansion of retail and e-commerce sectors is further supporting market growth. Additionally, the increasing adoption of modern lifestyles is encouraging the consumption of packaged and processed foods. Companies that expand their presence in these regions can benefit from growing demand and favorable market conditions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 198.4 Billion |

| Market Size in 2026 | USD 207.9 Billion |

| Market Size in 2034 | USD 318.6 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic containers dominated the market in 2024, accounting for approximately 42.6% of the total share. These containers are widely used due to their lightweight nature, durability, and cost-effectiveness. Plastic packaging offers excellent barrier properties and can be molded into various shapes and sizes, making it suitable for a wide range of food products. Additionally, advancements in plastic materials are improving recyclability and reducing environmental impact.

Glass packaging is expected to grow at the fastest CAGR of 5.9% during the forecast period. Glass is considered a safe and sustainable packaging material, as it is fully recyclable and does not react with food products. The increasing demand for premium and organic food products is driving the adoption of glass packaging. Consumers perceive glass as a high-quality material, which is supporting its growth.

By Application

Food and beverage applications dominated the market in 2024, holding a share of 46.3%. Rigid packaging is widely used in this segment to ensure product safety and extend shelf life. The increasing demand for packaged food and beverages is driving growth in this segment. Additionally, the need for convenient and portable packaging solutions is supporting market expansion.

Ready-to-eat meals are expected to grow at a CAGR of 6.2%, driven by changing consumer lifestyles and increasing demand for convenience foods. Rigid packaging provides the necessary protection and durability for these products. The growth of the food service industry and the expansion of retail channels are further supporting this segment.

By End-Use

The food processing industry accounted for the largest share of 44.9% in 2024. Rigid packaging is widely used in this industry to protect food products during storage and transportation. The increasing production of processed foods is driving demand for packaging solutions. Additionally, the need for compliance with food safety regulations is supporting the adoption of rigid packaging.

The retail and e-commerce sector is projected to grow at a CAGR of 6.3%. The increasing popularity of online grocery shopping and food delivery services is driving demand for durable packaging solutions. Rigid packaging helps protect products during transit and ensures quality upon delivery. The growth of modern retail formats is further supporting this segment.

Rigid Food Packaging Market Segmentations

By Product Type

- Plastic Containers

- Glass Containers

- Metal Cans

- Rigid Paperboard Packaging

By Application

- Food & Beverage

- Ready-to-Eat Meals

- Dairy Products

- Frozen Foods

By End-Use

- Food Processing Industry

- Retail & E-commerce

- Food Service Industry

Regional Analysis

North America

North America accounted for approximately 24.1% of the global rigid food packaging market share in 2025 and is expected to grow at a CAGR of 5.2% during the forecast period. The region’s growth is driven by strong demand for processed and convenience foods, as well as the expansion of food delivery services. The presence of established packaging companies and advanced manufacturing technologies supports market development. Increasing focus on sustainability and recycling is also influencing market trends.

The United States is the dominant country in North America, supported by its large food processing industry and high consumer demand for packaged foods. A unique growth factor in this region is the adoption of advanced packaging technologies, including smart packaging solutions that enhance food safety and quality. This is driving the demand for innovative rigid packaging products.

Europe

Europe held a market share of approximately 22.3% in 2025 and is projected to grow at a CAGR of 5.1%. The region is characterized by strict environmental regulations and a strong emphasis on sustainability. Demand for rigid food packaging is driven by the need for safe and hygienic packaging solutions. Technological advancements in packaging materials are also contributing to market growth.

Germany leads the European market due to its strong industrial base and focus on innovation. A unique growth factor is the increasing adoption of recyclable and reusable packaging solutions. Companies are investing in sustainable materials to comply with regulations and reduce environmental impact, which is supporting market expansion.

Asia Pacific

Asia Pacific dominated the rigid food packaging market in 2025 with a share of 39.8% and is expected to grow at a CAGR of 5.9%. Rapid urbanization, rising disposable incomes, and increasing demand for packaged foods are driving market growth. The expansion of retail and e-commerce sectors is also contributing to demand.

China is the dominant country in the Asia Pacific region, supported by its large population and growing food industry. A key growth factor is the increasing consumption of processed and convenience foods, which require reliable packaging solutions. The expansion of modern retail channels is further supporting market growth.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.7% of the global market share in 2025 and is projected to grow at a CAGR of 5.6%. The market is driven by increasing urbanization and the growth of the food and beverage industry. Demand for packaged foods is rising due to changing consumer preferences.

The United Arab Emirates is a leading market in this region, supported by strong retail and tourism sectors. A unique growth factor is the increasing demand for premium packaged food products, which require high-quality packaging solutions. This is driving the adoption of rigid food packaging.

Latin America

Latin America held a market share of approximately 7.1% in 2025 and is expected to grow at the fastest CAGR of 6.1%. The region’s growth is driven by rising urbanization and increasing demand for packaged foods. The expansion of retail and e-commerce sectors is also supporting market development.

Brazil is the dominant country in Latin America, driven by its large consumer base and growing food industry. A key growth factor is the increasing investment in food processing and packaging industries, which is creating demand for rigid food packaging solutions.

Competitive Landscape

The rigid food packaging market is moderately competitive, with several global and regional players focusing on innovation and sustainability. Companies are investing in research and development to create advanced packaging solutions with improved performance and environmental benefits. Strategic partnerships and expansions are common strategies used to strengthen market presence.

Amcor Plc is recognized as a leading player in the market, known for its extensive product portfolio and global presence. The company recently introduced recyclable rigid packaging solutions aimed at reducing environmental impact. Other key players are also focusing on developing sustainable materials and expanding production capacities to meet growing demand.

Key Players List

- Amcor Plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Silgan Holdings Inc.

- Ardagh Group S.A.

- Crown Holdings Inc.

- Ball Corporation

- Tetra Pak International S.A.

- DS Smith Plc

- Smurfit Kappa Group

- Mondi Group

- WestRock Company

- International Paper Company

- Huhtamaki Oyj