Rigid Chilled Food Packaging Market Size and Growth

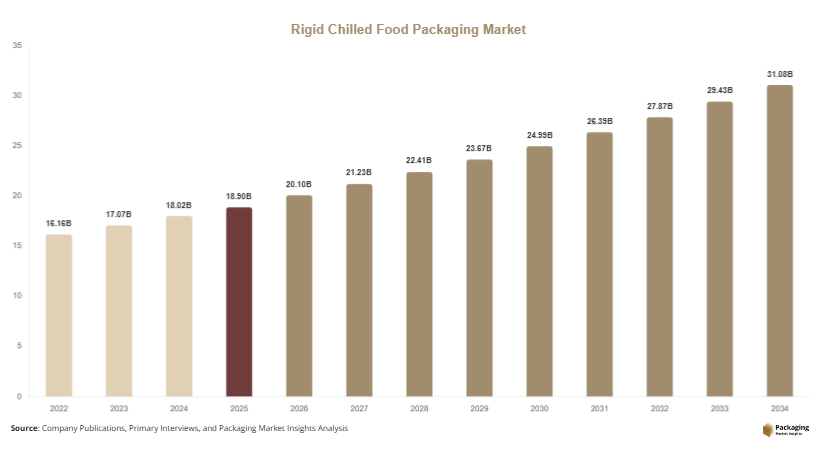

The global rigid chilled food packaging market size is estimated at USD 18.9 billion in 2025 and is expected to reach USD 20.1 billion in 2026. With the increasing need for extended shelf life and product safety, the market is projected to grow to USD 32.8 billion by 2034, registering a CAGR of 5.6% during the forecast period (2025–2034). Rigid chilled food packaging includes trays, containers, clamshells, and tubs designed to maintain product integrity under refrigerated conditions. The rigid chilled food packaging market is expanding steadily as consumer demand for fresh, ready-to-eat, and convenience food products continues to rise globally.

A major growth factor is the rising consumption of chilled and convenience foods driven by busy lifestyles and urbanization. Consumers are increasingly opting for ready meals, dairy products, and fresh produce that require reliable packaging to maintain freshness and prevent contamination. Another important factor is the growth of organized retail and e-commerce grocery platforms, which demand durable and protective packaging solutions that can withstand handling and transportation. Additionally, advancements in packaging materials such as modified atmosphere packaging (MAP) and barrier-enhanced plastics are improving product shelf life, further driving market growth.

Key Highlights:

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.3%.

- Plastic-based rigid packaging led the type segment with a 51.4% share, while paper-based rigid packaging is expected to grow at a CAGR of 6.1%.

- Trays and containers dominated with a 47.6% share, while clamshell packaging is forecasted to grow at a CAGR of 6.4%.

- Dairy and ready meals applications led the segment with 44.2% share, while fresh produce packaging is expected to grow at a CAGR of 6.2%.

- China remained the dominant country with a market size of USD 6.7 billion in 2025 and USD 7.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing demand for sustainable and recyclable rigid packaging

Sustainability is becoming a central focus in the rigid chilled food packaging market as both consumers and regulatory bodies emphasize environmentally responsible packaging solutions. Manufacturers are shifting toward recyclable materials such as PET and paper-based composites to reduce environmental impact. The adoption of mono-material packaging designs is increasing, making recycling processes more efficient. Companies are also investing in biodegradable alternatives and reducing material usage through lightweight designs. This shift is particularly evident in developed regions where environmental regulations are more stringent, encouraging innovation in sustainable rigid packaging solutions.

Advancements in barrier technologies and modified atmosphere packaging

Technological advancements in barrier materials and modified atmosphere packaging are enhancing the performance of rigid chilled food packaging. Improved barrier properties help extend the shelf life of perishable products by controlling oxygen and moisture levels. Modified atmosphere packaging allows manufacturers to maintain optimal conditions within the packaging, preserving freshness and quality. These innovations are enabling the packaging of a wider range of chilled food products, including ready meals and fresh produce. The integration of advanced sealing technologies further enhances product safety and reduces spoilage.

Market Drivers

Growth in consumption of ready-to-eat and chilled food products

The increasing demand for convenience foods is a major driver of the rigid chilled food packaging market. Consumers are seeking quick and easy meal options that require minimal preparation. This trend is driving the demand for packaging solutions that can maintain product quality and extend shelf life. Rigid packaging formats provide the necessary protection and structural integrity required for chilled food products. The expansion of food delivery services and online grocery platforms is further supporting market growth by increasing the demand for reliable packaging solutions.

Expansion of cold chain logistics and retail infrastructure

The development of cold chain logistics is playing a significant role in the growth of the rigid chilled food packaging market. Efficient cold storage and transportation systems are essential for maintaining the quality of chilled food products. As investments in cold chain infrastructure increase, the demand for compatible packaging solutions is also rising. Rigid packaging offers durability and protection during transportation, making it suitable for cold chain applications. The expansion of organized retail and supermarkets is further driving the demand for chilled food packaging.

Market Restraint

High material and production costs compared to flexible packaging

One of the challenges in the rigid chilled food packaging market is the relatively higher cost of materials and production compared to flexible packaging solutions. Rigid packaging requires more raw materials and energy-intensive manufacturing processes, which can increase overall costs. For example, plastic trays and containers used for chilled foods often involve complex molding processes and additional features such as sealing and labeling. These factors can limit adoption among cost-sensitive manufacturers, particularly in emerging markets. Additionally, fluctuations in raw material prices can impact profit margins and create uncertainty for manufacturers.

Market Opportunities

Development of bio-based and recyclable packaging materials

The growing emphasis on sustainability is creating opportunities for the development of bio-based and recyclable rigid packaging materials. Manufacturers are exploring alternatives such as biodegradable plastics and paper-based composites that offer similar performance characteristics. These innovations can help reduce environmental impact while meeting consumer demand for eco-friendly packaging. Companies investing in sustainable material development can gain a competitive advantage and expand their market presence.

Rising demand in emerging markets and urban areas

Emerging markets present significant growth opportunities for the rigid chilled food packaging market. Rapid urbanization, increasing disposable incomes, and changing consumer preferences are driving the demand for chilled and convenience foods. The expansion of retail infrastructure and cold chain logistics in these regions is further supporting market growth. Manufacturers can capitalize on these opportunities by offering cost-effective and adaptable packaging solutions tailored to local market needs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.9 Billion |

| Market Size in 2026 | USD 20.1 Billion |

| Market Size in 2034 | USD 32.8 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic-based rigid packaging dominated the market in 2024, accounting for 51.4% of the total share. This dominance is attributed to its durability, lightweight nature, and excellent barrier properties. Plastic materials such as PET and polypropylene are widely used in chilled food packaging due to their ability to maintain product freshness and resist moisture. The versatility of plastic packaging allows for various designs, including trays and containers, making it suitable for a wide range of applications.

Paper-based rigid packaging is expected to grow at the fastest CAGR of 6.1% during the forecast period. This growth is driven by increasing demand for sustainable packaging solutions. Paper-based materials are biodegradable and recyclable, making them an attractive alternative to plastic. Advancements in coating technologies are improving their barrier properties, enabling their use in chilled food applications.

By Product Type

Trays and containers accounted for the largest share of 47.6% in 2024. These packaging formats are widely used for ready meals, dairy products, and fresh produce due to their structural strength and ease of handling. Trays and containers provide effective protection during transportation and storage, making them a preferred choice for manufacturers.

Clamshell packaging is projected to grow at a CAGR of 6.4%, driven by its convenience and visibility features. Clamshells allow consumers to view the product without opening the package, enhancing product appeal. The growing demand for fresh produce and ready-to-eat meals is supporting the growth of this segment.

By Application

Dairy and ready meals segment held the largest share of 44.2% in 2024. The demand for packaged dairy products and ready meals is increasing due to changing consumer lifestyles. Rigid packaging provides the necessary protection and extends shelf life, making it suitable for these applications.

Fresh produce packaging is expected to grow at a CAGR of 6.2% during the forecast period. This growth is driven by increasing demand for packaged fruits and vegetables. Rigid packaging helps maintain product quality and reduces spoilage, supporting its adoption in this segment.

Rigid Chilled Food Packaging Market Segmentations

By Product Type

- Trays and Containers

- Clamshell Packaging

By Material Type

- Plastic-Based Rigid Packaging

- Paper-Based Rigid Packaging

By Application

- Dairy Products

- Ready Meals

- Fresh Produce

Regional Analysis

North America

North America accounted for 22.7% of the rigid chilled food packaging market share in 2025 and is expected to grow at a CAGR of 5.1% during the forecast period. The region benefits from a well-established food processing industry and advanced cold chain infrastructure. The demand for convenience foods and ready meals is high, driving the need for reliable packaging solutions. Additionally, increasing focus on food safety and sustainability is encouraging the adoption of advanced rigid packaging materials.

The United States dominates the regional market due to its large consumer base and developed retail sector. A unique growth factor is the increasing demand for premium packaging that enhances product presentation and shelf appeal. This trend is driving innovation in packaging design and materials.

Europe

Europe held a market share of 25.1% in 2025 and is projected to grow at a CAGR of 5.4%. The region is characterized by strict food safety regulations and a strong emphasis on sustainability. The adoption of recyclable and biodegradable packaging materials is increasing, supported by government policies and consumer awareness. The presence of leading food manufacturers further supports market growth.

Germany is the leading country in the European market, driven by its advanced food processing industry. A unique growth factor is the focus on reducing food waste through improved packaging solutions, which is driving the adoption of advanced rigid packaging technologies.

Asia Pacific

Asia Pacific dominated the market with a 36.8% share in 2025 and is expected to grow at a CAGR of 6.1%. The region’s growth is driven by rapid urbanization and increasing demand for packaged and convenience foods. The expansion of retail and e-commerce sectors is further supporting market growth. The availability of cost-effective manufacturing and raw materials also contributes to the region’s dominance.

China remains the dominant country in the region due to its large population and growing food industry. A unique growth factor is the increasing investment in cold chain infrastructure, which is enhancing the distribution of chilled food products.

Middle East & Africa

The Middle East & Africa region accounted for 7.3% of the market share in 2025 and is projected to grow at a CAGR of 5.8%. Growth is supported by increasing urbanization and rising demand for packaged foods. The development of retail infrastructure and cold storage facilities is further contributing to market expansion.

South Africa is a key market in the region, supported by its growing food industry. A unique growth factor is the expansion of supermarket chains, which is increasing the demand for chilled food packaging solutions.

Latin America

Latin America held an 8.1% share in 2025 and is expected to grow at the fastest CAGR of 6.3%. The region’s growth is driven by increasing consumer demand for convenience foods and expanding retail networks. The adoption of sustainable packaging solutions is also gaining momentum.

Brazil dominates the regional market due to its large population and strong food industry. A unique growth factor is the growth of local food processing industries, which is increasing the demand for rigid chilled food packaging solutions.

Competitive Landscape

The rigid chilled food packaging market is moderately competitive, with several global and regional players focusing on innovation and sustainability. Companies are investing in advanced materials and technologies to enhance packaging performance and meet evolving consumer demands. Strategic collaborations and product development initiatives are common strategies used to strengthen market presence.

Amcor plc is a leading player in the market, known for its extensive portfolio of packaging solutions. The company recently introduced recyclable rigid packaging products designed for chilled food applications, reflecting its focus on sustainability. Other players are also focusing on expanding their product offerings and improving manufacturing capabilities.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Pactiv Evergreen Inc.

- Genpak LLC

- Sabert Corporation

- Silgan Holdings Inc.

- DS Smith Plc

- Mondi Group

- WestRock Company

- Smurfit Kappa Group

- UFP Technologies Inc.