Rigid Bulk Packaging Market Size and Growth

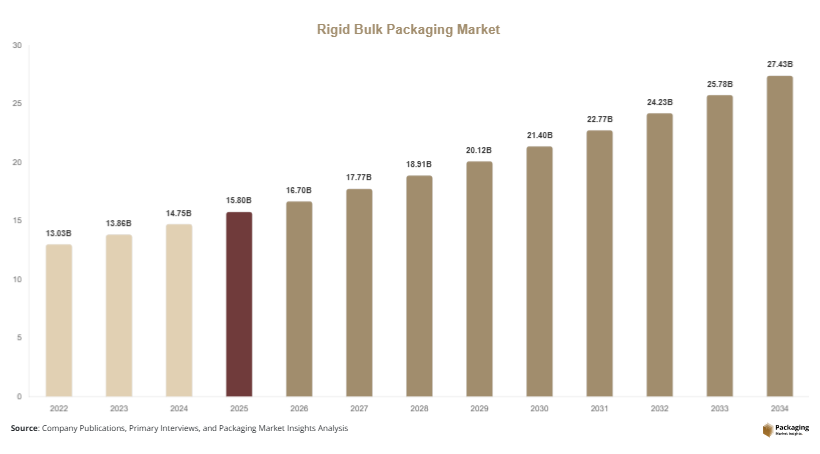

The global rigid bulk packaging market was valued at USD 15.8 billion in 2025 and is estimated to reach USD 16.7 billion in 2026. The market is projected to attain USD 27.4 billion by 2034, registering a CAGR of 6.4% during the forecast period from 2025 to 2034. The global rigid bulk packaging market is witnessing stable expansion due to increasing demand for durable industrial packaging solutions across chemicals, food processing, pharmaceuticals, construction, agriculture, and petrochemical industries. Rigid bulk packaging products, including drums, intermediate bulk containers (IBCs), pails, crates, and rigid plastic containers, are widely used for the safe transportation and storage of hazardous and non-hazardous materials.

Industrialization and increasing cross-border trade are major contributors to market growth. Manufacturers and exporters are increasingly adopting rigid bulk packaging solutions due to their high durability, stackability, and ability to withstand harsh transportation conditions. The expansion of chemical and petrochemical industries in Asia Pacific and the Middle East is creating sustained demand for industrial-grade storage and transport containers. In addition, the growing pharmaceutical and food processing sectors are supporting demand for contamination-resistant packaging solutions that comply with strict quality regulations.

Key Market Insights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.9%.

- Intermediate bulk containers led the type segment with a 34.2% share.

- Plastic material dominated with a 58.4% share.

- Chemicals and petrochemicals led the end-use segment with 39.7% share.

- The US remained the dominant country with a market size of USD 3.1 billion in 2025 and USD 3.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for Reusable Industrial Packaging Systems

The increasing adoption of reusable industrial packaging solutions is becoming a major trend in the rigid bulk packaging market. Companies operating in chemicals, automotive, food processing, and manufacturing industries are replacing single-use transport containers with reusable drums, crates, and intermediate bulk containers to reduce operational costs and improve sustainability performance. Reusable rigid bulk packaging systems offer longer product life cycles, lower replacement frequency, and improved storage efficiency compared to disposable alternatives.

Industrial logistics providers are also introducing closed-loop transportation systems where containers are collected, cleaned, and redeployed multiple times. For example, food ingredient manufacturers are increasingly using reusable plastic IBCs to transport syrups, edible oils, and liquid concentrates. The trend is expected to accelerate as sustainability regulations tighten and industries focus on lowering packaging waste generation. Future investments in lightweight reusable materials and digital tracking technologies are likely to strengthen adoption across industrial supply chains.

Integration of Smart Tracking and IoT-Based Packaging Technologies

Digital transformation in industrial logistics is driving the adoption of smart packaging technologies in the rigid bulk packaging market. Companies are integrating RFID tags, QR codes, GPS-enabled sensors, and IoT monitoring systems into bulk containers to improve supply chain visibility and asset management. Smart rigid packaging solutions allow manufacturers and distributors to track container location, filling levels, temperature conditions, and handling status in real time.

Chemical and pharmaceutical companies are increasingly adopting connected packaging systems to improve inventory management and reduce losses from damaged or misplaced containers. For example, lubricant and industrial fluid suppliers are implementing RFID-enabled drums and IBCs to improve warehouse efficiency and shipment accuracy. Future developments in industrial automation and digital logistics infrastructure are expected to increase demand for intelligent packaging systems that support predictive maintenance, asset utilization monitoring, and regulatory compliance across global trade networks.

Market Drivers

Expansion of Chemical and Petrochemical Industries

The rapid expansion of chemical and petrochemical production is a major factor driving the growth of the rigid bulk packaging market. Industrial chemicals, solvents, lubricants, and specialty liquids require highly durable and leak-resistant packaging solutions for transportation and storage. Rigid bulk packaging products such as steel drums and IBCs provide enhanced safety, product integrity, and compatibility with hazardous materials regulations.

Increasing investments in petrochemical complexes across Asia Pacific and the Middle East are supporting demand for industrial packaging containers capable of handling corrosive and high-value materials. Chemical exporters prefer rigid packaging because it minimizes product contamination and improves handling efficiency during international shipping. In addition, rising production of industrial coatings, adhesives, and specialty chemicals is creating consistent demand for certified packaging systems. As industrial chemical trade continues to grow globally, manufacturers of rigid bulk packaging products are expected to benefit from stable long-term demand.

Growth in Food Processing and Beverage Distribution

The expansion of food processing and beverage industries is significantly contributing to the growth of the rigid bulk packaging market. Manufacturers of edible oils, dairy ingredients, liquid sweeteners, sauces, and beverage concentrates require hygienic and durable packaging solutions for bulk transportation and storage. Rigid containers provide protection against contamination, moisture, and leakage, making them suitable for food-grade applications.

The growth of organized retail and processed food exports is increasing demand for standardized bulk packaging systems that support long-distance transportation. Beverage manufacturers are also using reusable plastic containers and food-grade drums to optimize supply chain efficiency and reduce product losses during handling. In regions such as North America and Europe, stricter food safety regulations are encouraging companies to adopt certified packaging systems with advanced sealing and traceability features. Continued expansion of global food trade is expected to sustain demand for rigid industrial packaging solutions.

Market Restraint

High Manufacturing Costs and Logistics Challenges

High production and transportation costs remain major restraints for the rigid bulk packaging market. Rigid packaging products such as steel drums, heavy-duty plastic containers, and metal intermediate bulk containers require substantial raw material inputs and energy-intensive manufacturing processes. Fluctuations in steel, aluminum, and high-density polyethylene prices can significantly affect manufacturing margins and product pricing.

Transportation and storage costs are also higher for rigid packaging compared to flexible alternatives because rigid containers occupy more space and increase freight weight. Small and medium-sized manufacturers may face operational challenges in maintaining return logistics systems for reusable containers, particularly in fragmented supply chains. For example, companies involved in international chemical exports often incur additional cleaning, inspection, and reverse logistics costs for reusable IBCs and drums. These cost-related challenges can limit adoption among price-sensitive industries and encourage some businesses to continue using lower-cost packaging alternatives.

Market Opportunities

Increasing Demand for Sustainable Packaging Solutions

The growing emphasis on environmental sustainability is creating significant opportunities for the rigid bulk packaging market. Industries are increasingly investing in reusable and recyclable bulk containers to reduce industrial packaging waste and improve compliance with sustainability goals. Plastic and metal rigid packaging systems with extended life cycles are gaining popularity across chemicals, food processing, and automotive sectors.

Manufacturers are introducing containers made from recycled resins and lightweight alloys to improve environmental performance without compromising durability. Companies involved in industrial logistics are also implementing container return and refurbishment programs to support circular economy initiatives. Future opportunities are expected to emerge from regulatory incentives promoting sustainable industrial packaging and rising demand for eco-friendly supply chain solutions among multinational corporations.

Expansion of Pharmaceutical and Specialty Chemical Applications

The rapid expansion of pharmaceutical manufacturing and specialty chemical production is opening new growth opportunities for the rigid bulk packaging market. Pharmaceutical companies require contamination-resistant and chemically stable containers for transporting active pharmaceutical ingredients, sterile liquids, and sensitive compounds. Rigid packaging products with tamper-evident seals and advanced barrier properties are increasingly preferred for high-value pharmaceutical applications.

Specialty chemical manufacturers are also investing in customized rigid containers designed for temperature-sensitive and hazardous materials. Growth in biotechnology production and specialty healthcare chemicals is expected to increase demand for premium industrial packaging solutions. Countries such as India, Germany, and the United States are witnessing rising pharmaceutical exports, creating long-term opportunities for packaging manufacturers capable of meeting strict regulatory and quality standards.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Size in 2026 | USD 16.7 Billion |

| Market Size in 2034 | USD 27.4 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Intermediate bulk containers accounted for the largest share of the rigid bulk packaging market in 2024, representing approximately 34.2% of total revenue. These containers are widely used for transporting chemicals, food ingredients, oils, lubricants, and pharmaceutical liquids due to their high durability and storage efficiency. Intermediate bulk containers provide advantages such as stackability, reusable design, and compatibility with automated handling systems, making them highly preferred across industrial supply chains. Chemical manufacturers rely on stainless steel and high-density polyethylene IBCs for safe handling of hazardous and corrosive materials. Food processing companies are also increasing adoption of food-grade IBCs for transporting syrups, edible oils, and beverage concentrates. The dominance of this segment is supported by rising global trade in industrial liquids and growing investment in warehouse automation.

Reusable crates are projected to emerge as the fastest-growing type segment, registering a CAGR of 7.2% during the forecast period. Retailers, food distributors, and agricultural producers are increasingly using reusable crates for transportation and storage of fruits, vegetables, dairy products, and packaged consumer goods. The growth of organized retail and cold-chain logistics is creating strong demand for durable and stackable crate systems that improve transportation efficiency and reduce packaging waste. Manufacturers are introducing foldable and lightweight crate designs to reduce reverse logistics costs and improve storage optimization. Future growth is expected to be supported by sustainability initiatives encouraging reusable transport packaging across retail and food distribution networks.

By Material

Plastic material dominated the rigid bulk packaging market in 2024 with a revenue share of approximately 58.4%. High-density polyethylene and polypropylene materials are widely preferred due to their durability, lightweight structure, chemical resistance, and cost efficiency. Plastic rigid containers are extensively used in food processing, pharmaceuticals, chemicals, and agriculture because they provide strong protection against moisture, leakage, and contamination. Manufacturers favor plastic materials because they support large-scale production and allow easy customization for different industrial applications. Increasing demand for reusable plastic containers and lightweight industrial packaging solutions is further strengthening segment growth. Plastic-based rigid packaging also offers compatibility with RFID systems and automated filling equipment, supporting adoption across modern logistics networks.

Composite materials are anticipated to witness the fastest growth during the forecast period, expanding at a CAGR of 7.5% through 2034. Composite containers combine the advantages of plastic, metal, and fiber materials to improve durability, insulation, and impact resistance. Industries handling hazardous chemicals and temperature-sensitive products are increasingly adopting composite packaging systems due to their enhanced structural performance. Packaging manufacturers are investing in advanced multilayer designs and reinforced composite structures to meet evolving industrial transportation requirements. Sustainability trends are also encouraging research into recyclable composite materials with lower environmental impact. Continued innovation in lightweight industrial packaging technologies is expected to accelerate adoption of composite rigid bulk containers across global markets.

By End-Use

Chemicals and petrochemicals represented the dominant end-use segment in the rigid bulk packaging market in 2024, accounting for nearly 39.7% of total revenue. The segment relies heavily on drums, IBCs, and rigid containers for safe transportation and storage of solvents, lubricants, industrial oils, coatings, and hazardous chemicals. Stringent safety regulations for chemical handling are encouraging manufacturers to invest in certified packaging systems with leak-resistant and corrosion-resistant properties. Increasing global trade in petrochemical products and industrial chemicals is further supporting demand for high-performance bulk packaging solutions. Major exporters in Asia Pacific and the Middle East are expanding production capacity, which is driving the need for durable industrial storage and transportation systems.

Pharmaceutical applications are expected to register the fastest CAGR of 7.1% during the forecast period. Pharmaceutical manufacturers require high-quality rigid packaging solutions for transporting sterile liquids, active pharmaceutical ingredients, and specialty healthcare chemicals. Growth in biologics production and specialty drug manufacturing is increasing demand for contamination-resistant containers with advanced barrier properties. Packaging suppliers are investing in tamper-evident sealing technologies, cleanroom production processes, and traceability systems to meet strict pharmaceutical safety standards. The rapid expansion of pharmaceutical exports from India, Europe, and North America is expected to create sustained demand for premium rigid packaging products over the next decade.

Rigid Bulk Packaging Market Segmentations

By Type

- Intermediate Bulk Containers

- Drums

- Pails

- Reusable Crates

- Rigid Plastic Containers

By Material

- Plastic

- Metal

- Fiber

- Composite Materials

By End-User

- Chemicals and Petrochemicals

- Food and Beverage

- Pharmaceuticals

- Agriculture

- Construction and Industrial Manufacturing

Regional Analysis

North America

North America accounted for approximately 23.1% of the global rigid bulk packaging market share in 2025 and is projected to expand at a CAGR of 5.7% during the forecast period. The regional market benefits from strong demand across chemical manufacturing, food processing, pharmaceuticals, and industrial logistics sectors. Companies in the United States and Canada are increasingly investing in reusable bulk packaging systems to improve sustainability performance and reduce operational costs. Rising adoption of automated warehousing systems is encouraging the use of standardized rigid containers compatible with robotic handling equipment. Growth in industrial exports and cross-border trade is also supporting demand for durable bulk packaging products across the region.

The United States remains the dominant country in North America due to its extensive industrial manufacturing base and advanced logistics infrastructure. A major growth driver in the country is the increasing transportation of industrial chemicals and lubricants requiring certified leak-resistant containers. Food and beverage manufacturers are also expanding the use of food-grade drums and reusable IBCs to improve storage efficiency and reduce contamination risks. Industrial packaging suppliers are introducing RFID-enabled container tracking systems to improve inventory visibility and reduce container loss. The continued modernization of industrial supply chains is expected to sustain market demand in the United States.

Europe

Europe represented nearly 25.4% of the global rigid bulk packaging market in 2025 and is expected to register a CAGR of 5.9% through 2034. The regional market is supported by strict packaging safety standards and growing emphasis on sustainable industrial packaging systems. Demand for reusable metal and plastic containers is increasing across Germany, France, Italy, and the United Kingdom due to environmental regulations targeting industrial waste reduction. Pharmaceutical and food processing industries are major consumers of rigid packaging solutions because they require high standards of hygiene and product protection.

Germany dominates the European market due to its large chemical manufacturing and industrial export sectors. One unique growth driver is the country’s increasing adoption of circular economy models within industrial packaging operations. Packaging suppliers are collaborating with logistics providers to establish reusable container pooling and refurbishment systems that lower packaging waste and transportation costs. In addition, German automotive and lubricant manufacturers are increasing demand for heavy-duty bulk containers used for industrial fluid transportation. Rising exports of specialty chemicals and pharmaceutical ingredients are expected to support long-term demand for rigid bulk packaging products.

Asia Pacific

Asia Pacific held the largest share of the rigid bulk packaging market at 38.6% in 2025 and is forecasted to expand at a CAGR of 6.8% through 2034. Rapid industrialization, increasing export activities, and strong growth in chemical and food manufacturing industries are major factors driving regional market expansion. Countries such as China, India, Japan, and South Korea are witnessing rising demand for industrial packaging products used in chemicals, edible oils, paints, and industrial liquids. Expanding logistics infrastructure and increasing containerized trade are also supporting market growth.

China remains the leading market in Asia Pacific due to its strong manufacturing ecosystem and large-scale industrial exports. A major growth driver in the country is the expansion of petrochemical and specialty chemical production facilities that require high-capacity storage and transportation containers. Chinese manufacturers are investing in automated production lines and lightweight packaging technologies to improve manufacturing efficiency and export competitiveness. India is also emerging as a significant market due to growth in pharmaceutical production and agricultural processing industries. Rising industrial trade across Southeast Asia is expected to further increase demand for rigid bulk packaging products in the region.

Middle East & Africa

The Middle East & Africa accounted for approximately 7.2% of the global rigid bulk packaging market share in 2025 and is projected to grow at a CAGR of 6.0% during the forecast period. Industrial diversification strategies and infrastructure development projects are contributing to increased demand for industrial packaging solutions across the region. Petrochemical production, mining operations, and food imports are key sectors driving demand for drums, crates, and intermediate bulk containers. Investments in port infrastructure and logistics modernization are also improving regional trade efficiency.

Saudi Arabia dominates the regional market due to the rapid expansion of petrochemical manufacturing and industrial export activities. A unique growth driver is the country’s investment in downstream chemical industries and industrial logistics hubs. Packaging manufacturers are benefiting from rising demand for heavy-duty containers used in lubricant and resin transportation. In Africa, South Africa is witnessing growing use of rigid packaging products in mining and food processing sectors. The expansion of industrial warehousing and cold-chain logistics infrastructure is expected to create additional growth opportunities across the region.

Latin America

Latin America represented nearly 5.7% of the global rigid bulk packaging market in 2025 and is expected to witness the fastest CAGR of 6.9% during the forecast period. The regional market is benefiting from expanding agricultural exports, mining activities, and industrial manufacturing operations. Countries including Brazil, Argentina, and Chile are increasing exports of edible oils, industrial chemicals, and processed food products, which require durable and efficient bulk packaging systems. Improvements in logistics infrastructure and rising trade agreements are supporting the adoption of standardized rigid packaging solutions.

Brazil remains the dominant country in Latin America due to its strong agriculture and industrial processing sectors. One important growth driver is the increasing export volume of edible oils, ethanol, and processed agricultural products requiring food-grade rigid containers. Packaging companies are expanding manufacturing facilities and distribution networks to improve service capabilities for exporters and industrial producers. The mining industries in Chile and Peru are also contributing to demand for industrial drums and high-capacity containers used in mineral transportation. Ongoing investments in industrial modernization are expected to strengthen long-term market growth across Latin America.

Competitive Landscape

The rigid bulk packaging market is moderately consolidated, with major companies competing through product innovation, regional expansion, sustainability initiatives, and strategic partnerships. Leading manufacturers are investing in lightweight materials, reusable packaging technologies, and digital tracking systems to strengthen their market position and improve operational efficiency. Product customization and compliance with industrial safety regulations remain critical competitive factors across chemical, food, and pharmaceutical applications.

Mauser Packaging Solutions is recognized as a leading company in the market due to its extensive global manufacturing footprint and broad industrial packaging portfolio. The company continues to invest in sustainable packaging systems, container reconditioning programs, and recycled material integration to meet evolving customer requirements. Other major players are expanding production capacities in Asia Pacific and Latin America to capitalize on rising industrial trade and manufacturing growth.

Several companies are also focusing on smart packaging technologies that integrate RFID tracking and IoT-based monitoring capabilities for industrial logistics applications. Strategic acquisitions and partnerships with logistics providers are helping companies strengthen distribution networks and improve customer service capabilities. Investments in food-grade and pharmaceutical-grade packaging systems are expected to remain a key focus area as regulatory standards continue to evolve.

Key Players List

- Mauser Packaging Solutions

- Greif Inc.

- SCHÜTZ GmbH & Co. KGaA

- Snyder Industries Inc.

- Hoover Ferguson Group

- Time Technoplast Ltd.

- Schutz Container Systems

- Myers Industries Inc.

- Berry Global Inc.

- DS Smith Plc

- Nefab Group

- IPL Plastics Inc.

- Balmer Lawrie & Co. Ltd.

- Peninsula Drums Pty Ltd.

- Fibrestar Drums Limited

- Sicagen India Limited