Rigid Box Market Size and Growth

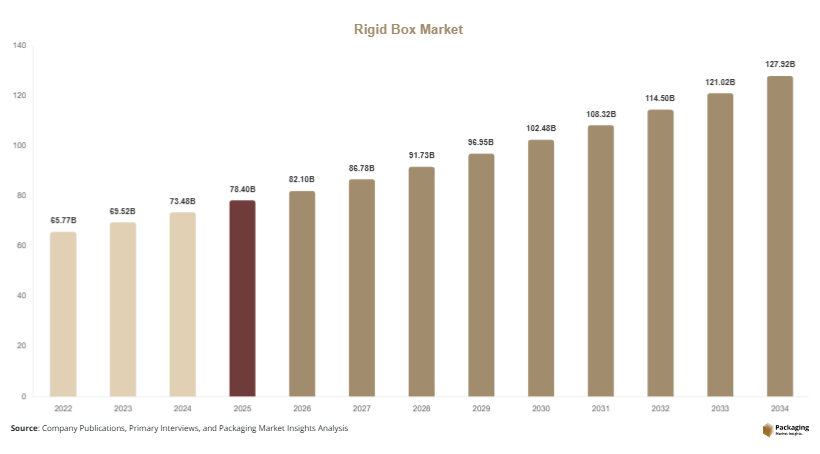

In 2025, the global rigid box market size is estimated at approximately USD 78.4 billion, and it is projected to reach USD 82.1 billion in 2026. By 2034, the market is expected to attain around USD 129.6 billion, registering a CAGR of 5.7% during the forecast period (2025–2034). The growth reflects the rising importance of brand differentiation, unboxing experience, and product protection in premium consumer markets. The rigid box market is witnessing steady expansion as demand for premium packaging solutions increases across luxury goods, electronics, cosmetics, and high-end retail sectors.

Several key factors are driving market expansion. First, the rapid growth of the luxury goods sector, particularly in cosmetics, perfumes, and jewelry, is increasing demand for high-quality rigid packaging solutions. Second, the expansion of e-commerce platforms has amplified the need for visually appealing yet durable packaging that enhances customer experience and reduces product damage during transit. Third, increasing corporate branding investments are encouraging companies to adopt customized rigid boxes with advanced printing, embossing, and magnetic closure features.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

- Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for Luxury and Premium Packaging Experiences

The rigid box market is experiencing a strong shift toward luxury-oriented packaging solutions driven by evolving consumer expectations. Brands in cosmetics, fashion, jewelry, and premium electronics are increasingly using rigid boxes to enhance perceived product value and create a strong unboxing experience. The use of magnetic closures, velvet linings, foil stamping, and embossed finishes is becoming more common. This trend is strongly influenced by social media unboxing culture, where packaging presentation directly impacts brand visibility. Companies are investing in creative structural designs that differentiate products on retail shelves and digital marketplaces, leading to higher adoption of customized rigid packaging formats globally.

Integration of Sustainable and Smart Packaging Solutions

Sustainability is becoming a core trend in the rigid box market as manufacturers shift toward recyclable and biodegradable materials. Paperboard-based rigid boxes with water-based coatings are gaining traction as brands aim to reduce environmental impact. Regulatory pressure in Europe and North America is accelerating this transition. At the same time, smart packaging features such as QR codes and NFC tags are being integrated into rigid boxes to provide product authentication, traceability, and interactive consumer engagement. This combination of sustainability and digital integration is reshaping packaging innovation strategies across industries, especially in luxury retail and electronics sectors.

Market Drivers

Expansion of Luxury Goods and Premium Consumer Markets

The growing global demand for luxury goods is a major driver of the rigid box market. Increasing disposable income, especially in emerging economies, is fueling consumption of high-end products such as perfumes, watches, cosmetics, and premium electronics. Rigid boxes are widely used in these segments due to their superior strength, aesthetic appeal, and customization capabilities. Luxury brands rely on rigid packaging to reinforce brand identity and enhance customer perception. The rise of premium gifting culture and seasonal retail demand further supports market growth. As luxury consumption expands across Asia Pacific and the Middle East, rigid box adoption continues to rise steadily.

Growth of E-commerce and Retail Branding Strategies

The rapid expansion of e-commerce platforms is another key driver of the rigid box market. Online retailers increasingly use rigid packaging to improve product presentation and reduce damage during shipping. Unlike traditional packaging, rigid boxes offer structural durability combined with premium visual appeal, making them ideal for direct-to-consumer shipments. Brands are also using packaging as a marketing tool, integrating storytelling elements, brand logos, and personalized designs. The competitive nature of online retail is pushing companies to invest in enhanced packaging solutions that improve customer retention and unboxing experiences, further accelerating demand for rigid boxes.

Market Restraint

High Production Costs and Material Limitations

A key restraint in the rigid box market is the relatively high production cost compared to flexible packaging alternatives. Rigid boxes require multiple manufacturing steps, including cutting, lamination, and finishing, which increases overall production expenses. The use of premium materials such as high-density paperboard, specialty coatings, and decorative elements further adds to cost pressure. Small and medium-sized enterprises often face challenges in adopting rigid packaging due to budget limitations. Additionally, fluctuations in raw material prices, particularly paper pulp and adhesives, create supply chain uncertainties. These cost factors can limit widespread adoption in price-sensitive markets, especially in developing regions.

Market Opportunities

Expansion in Emerging Retail and Luxury Markets

Emerging economies present significant opportunities for the rigid box market due to rising urbanization and increasing consumer spending on luxury products. Countries in Asia Pacific, Latin America, and the Middle East are witnessing rapid growth in organized retail and premium brand penetration. This is driving demand for high-quality packaging solutions that enhance product differentiation. Local manufacturers are also investing in advanced printing technologies to meet growing customization needs. The expansion of beauty, fashion, and electronics industries in these regions creates long-term opportunities for rigid box suppliers to establish strong market presence.

Innovation in Eco-Friendly and Lightweight Rigid Packaging

Innovation in eco-friendly rigid packaging materials presents another major opportunity. Manufacturers are developing lightweight rigid boxes using recycled fibers, molded pulp, and biodegradable coatings to reduce environmental impact. These innovations not only comply with sustainability regulations but also reduce transportation costs due to lighter packaging weight. Additionally, advancements in structural engineering are enabling stronger yet thinner box designs. Brands are increasingly adopting sustainable rigid packaging as part of their ESG commitments, creating a strong growth avenue for manufacturers focusing on green packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 78.4 Billion |

| Market Size in 2026 | USD 82.1 Billion |

| Market Size in 2034 | USD 129.6 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Paperboard rigid boxes dominated the market with a 44.8% share in 2024, driven by their balance of durability, cost efficiency, and printability. These boxes are widely used in cosmetics, electronics, and retail gifting due to their ability to support high-end customization such as embossing and foil stamping. Paperboard remains the preferred material due to its recyclability and compatibility with sustainable packaging initiatives. Its versatility in design applications also allows brands to create premium unboxing experiences that enhance consumer engagement and brand recall.

Luxury laminated rigid boxes are the fastest-growing subsegment, projected to expand at a CAGR of 6.4%, driven by increasing demand for premium aesthetics in cosmetics and electronics. These boxes often feature specialty coatings, textured finishes, and magnetic closures, making them highly attractive for high-value products. Growth is further supported by rising consumer preference for visually appealing packaging and the increasing influence of social media-driven product presentation. Manufacturers are investing in advanced finishing technologies to enhance visual appeal and structural durability.

By Application

Cosmetics packaging led the application segment with a 38.5% share in 2024, driven by strong demand from skincare, perfume, and beauty brands. Rigid boxes are widely used in this segment due to their ability to enhance product perception and support premium branding strategies. The cosmetic industry heavily relies on visually appealing packaging to influence purchasing decisions, making rigid boxes a preferred choice across global markets.

Electronics packaging is the fastest-growing application segment, projected to grow at a CAGR of 6.1%, supported by increasing demand for smartphones, wearable devices, and premium gadgets. Rigid boxes provide superior protection for delicate electronic components while maintaining premium presentation standards. The growth of e-commerce electronics sales is further driving adoption of durable and aesthetically enhanced packaging solutions.

By End-Use Industry

Retail and luxury goods dominated the end-use segment with a 41.2% share in 2024, driven by strong demand from fashion, jewelry, and premium gifting industries. Rigid boxes are widely used in this segment to enhance brand identity and improve customer experience. Retailers prioritize packaging that adds value to the product while reinforcing brand recognition.

E-commerce is the fastest-growing end-use segment, projected to expand at a CAGR of 6.5%, driven by the rise of online shopping platforms. Brands are increasingly using rigid boxes to reduce product damage during transit while enhancing unboxing experiences. Growth in direct-to-consumer sales models is further accelerating adoption of premium packaging solutions.

Rigid Box Market Segmentations

By Material Type

- Paperboard Rigid Boxes

- Chipboard Rigid Boxes

- Laminated Luxury Boxes

- Specialty Coated Boxes

By Application

- Cosmetics & Personal Care

- Electronics

- Luxury Goods & Fashion

- Food & Beverage Packaging

By End-Use Industry

- Retail & Luxury Brands

- E-commerce Platforms

- Electronics Industry

- Corporate Gifting

Regional Analysis

North America

North America accounted for approximately 24.6% of the rigid box market in 2025, with a projected CAGR of 5.3% through 2034. The region’s growth is supported by strong demand from cosmetics, luxury goods, and premium electronics sectors. High consumer preference for branded and aesthetically appealing packaging is further driving market adoption across retail channels.

The United States dominates the regional market due to its well-established luxury goods industry and strong e-commerce ecosystem. Increasing focus on premium branding strategies and sustainable packaging initiatives is further boosting demand for customized rigid boxes across multiple industries.

Europe

Europe held around 22.9% market share in 2025, with a CAGR of 5.1% during the forecast period. The region is characterized by strong demand for eco-friendly packaging solutions and premium retail packaging formats. Strict environmental regulations are encouraging manufacturers to adopt recyclable materials.

Germany leads the European market due to its advanced packaging manufacturing industry and strong luxury goods sector. The country’s emphasis on sustainable design innovation and high-quality printing technologies supports consistent market growth.

Asia Pacific

Asia Pacific dominated the market with 37.4% share in 2025, expanding at a CAGR of 6.0% through 2034. Rapid urbanization, rising disposable incomes, and expansion of luxury retail are key growth drivers. The region also benefits from strong manufacturing capabilities and cost-efficient production.

China remains the dominant country due to its large consumer base and growing luxury goods consumption. Expansion of e-commerce platforms and domestic premium brands is significantly boosting rigid box demand.

Middle East & Africa

The Middle East & Africa region accounted for 8.3% market share in 2025, with a CAGR of 5.8% through 2034. Growth is driven by rising luxury retail penetration and increasing demand for premium packaging in cosmetics and gifting sectors.

The United Arab Emirates leads the region due to its strong luxury retail industry and high tourist spending. Expansion of high-end shopping destinations and branding investments supports market growth.

Latin America

Latin America held around 7.0% market share in 2025, with the fastest CAGR of 6.2% through 2034. Growth is driven by increasing demand for premium consumer goods and expansion of organized retail networks.

Brazil dominates the regional market due to its growing cosmetics and fashion industries. Rising consumer preference for branded packaging in urban centers is further supporting rigid box adoption.

Competitive Landscape

The rigid box market is moderately fragmented, with several global and regional players competing on design innovation, material quality, and customization capabilities. Key companies include WestRock Company, International Paper Company, Smurfit Kappa Group, DS Smith Plc, and HH Deluxe Packaging. These players focus on expanding sustainable packaging portfolios and investing in advanced printing technologies. WestRock Company is a leading player, known for its strong presence in premium packaging solutions and continuous innovation in eco-friendly rigid box designs. Recent developments include expansion of luxury packaging production facilities and integration of digital printing technologies to enhance customization and reduce lead times.

Key Players List

- WestRock Company

- International Paper Company

- Smurfit Kappa Group

- DS Smith Plc

- HH Deluxe Packaging

- Lacerta Group

- Robinson Plc

- Pendragon Presentation Packaging Ltd

- JohnsByrne Company

- Mw Luxury Packaging

- United Packaging Industries

- PakFactory

- Red Paper Plane

- All Packaging Company

- Cardboard Box Company