Returnable Transit Packaging Market Size and Growth

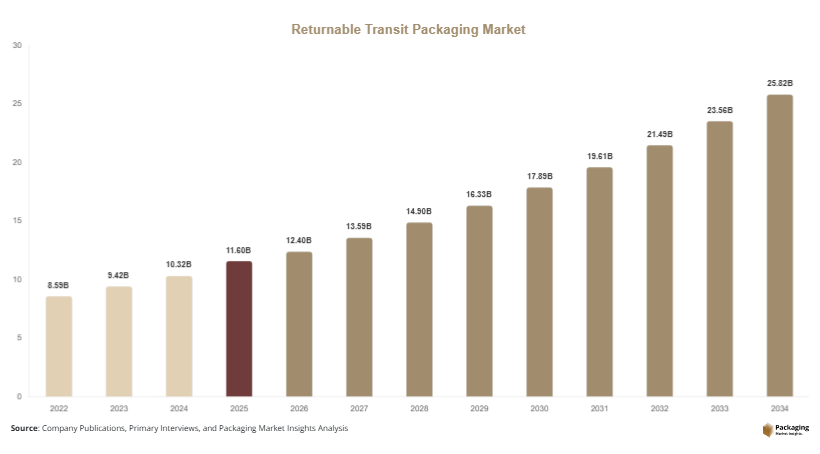

In 2025, the global Returnable Transit Packaging Market size is estimated at USD 11.6 billion, which is expected to reach USD 12.4 billion in 2026. By 2034, the market is projected to reach approximately USD 25.9 billion, growing at a CAGR of 9.6% (2025–2034).The Returnable Transit Packaging (RTP) Market is expanding steadily as industries shift toward sustainable, cost-efficient, and circular logistics solutions. Returnable transit packaging includes reusable containers such as crates, pallets, bins, intermediate bulk containers (IBCs), and totes used across supply chains to reduce single-use packaging waste.

The growth of the RTP market is driven by increasing environmental regulations aimed at reducing plastic waste and carbon emissions. Governments across Europe, North America, and Asia are promoting circular economy models, encouraging industries to adopt reusable packaging systems. Additionally, rising logistics costs and supply chain optimization needs are pushing manufacturers and distributors toward durable packaging solutions that reduce long-term operational expenses.

Key Highlights

- Market size (2025): The Returnable Transit Packaging Market is valued at USD 11.6 Billion in 2025, supported by strong demand from automotive, food & beverage, and industrial logistics sectors. Growth is driven by increasing adoption of reusable logistics systems, rising supply chain optimization needs, and expanding global manufacturing activities.

- Market size (2026): The market is expected to reach USD 12.4 Billion in 2026, reflecting steady expansion in circular packaging systems and increased integration of reusable containers in large-scale distribution networks. Rising investments in automated warehousing and smart logistics infrastructure further support this growth trajectory.

- Forecast value (2034): By 2034, the market is projected to reach USD 25.9 Billion, driven by widespread adoption of circular economy practices, expansion of e-commerce-driven logistics networks, and increasing focus on reducing packaging waste across global supply chains.

- CAGR (2025–2034): The market is expected to grow at a CAGR of 9.6% during 2025–2034, supported by strong demand from automotive, food & beverage, and industrial logistics sectors, along with rising adoption of circular economy and reusable logistics systems.

- Strong demand from automotive, food & beverage, and industrial logistics sectors: These industries are increasingly using durable, reusable packaging solutions to improve supply chain efficiency, reduce product damage, and lower long-term packaging costs across multi-stage distribution networks.

- Rising adoption of circular economy and reusable logistics systems: Companies are shifting toward closed-loop supply chains that prioritize reuse over disposal, helping reduce environmental impact while improving asset utilization and operational efficiency in logistics operations.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Circular Supply Chain Models

One of the most significant trends in the returnable transit packaging market is the increasing adoption of circular supply chain models. Companies are shifting away from traditional single-use packaging systems toward reusable and closed-loop logistics frameworks. This transition is driven by sustainability regulations, rising raw material costs, and corporate ESG commitments. RTP solutions such as collapsible crates, reusable pallets, and modular containers are being widely implemented across industries to minimize waste generation and improve logistics efficiency. Automotive and retail sectors are leading this transformation by establishing return logistics networks that allow packaging to be reused multiple times across distribution cycles. Digital tracking systems further enhance this trend by enabling real-time monitoring and efficient asset recovery.

Integration of Smart Tracking Technologies in RTP Systems

Another key trend shaping the market is the integration of smart technologies such as RFID tags, GPS tracking, and IoT sensors into returnable transit packaging systems. These technologies provide real-time visibility of packaging assets, helping companies optimize utilization rates and reduce losses. Smart RTP systems are particularly useful in large-scale supply chains where containers move across multiple geographies and stakeholders. Industries such as pharmaceuticals and automotive manufacturing are increasingly adopting these technologies to ensure traceability and compliance with regulatory requirements. Additionally, predictive analytics is being used to monitor container lifecycle performance, enabling preventive maintenance and reducing operational downtime.

Market Drivers

Rising Focus on Sustainability and Waste Reduction

The growing global emphasis on sustainability is a major driver of the returnable transit packaging market. Governments and regulatory bodies are implementing strict environmental policies to reduce plastic waste and promote reusable packaging solutions. Industries are under increasing pressure to minimize their environmental footprint, leading to widespread adoption of RTP systems. Companies are transitioning to reusable pallets, crates, and containers to reduce landfill waste and comply with environmental standards. For example, European Union directives on packaging waste reduction are significantly influencing corporate packaging strategies. This shift is also driven by consumer awareness, as end-users increasingly prefer environmentally responsible brands.

Cost Efficiency and Supply Chain Optimization

Another key driver is the long-term cost efficiency associated with returnable transit packaging systems. Although initial investment costs may be higher than disposable packaging, RTP systems offer significant savings over time due to multiple reuse cycles. Companies benefit from reduced packaging procurement costs, lower waste disposal expenses, and improved logistics efficiency. In industries such as automotive and FMCG, RTP systems help minimize product damage during transit and streamline warehouse operations. The ability to standardize packaging sizes also improves transportation efficiency, reducing empty space and lowering freight costs.

Market Restraint

High Initial Investment and Reverse Logistics Complexity

A key restraint in the returnable transit packaging market is the high initial investment required for deploying reusable packaging systems, along with the complexity of reverse logistics management. Unlike single-use packaging, RTP systems require a structured return flow, cleaning processes, and inventory tracking infrastructure, which increases operational complexity.

For small and medium-sized enterprises, the upfront cost of purchasing reusable pallets, crates, and tracking systems can be a significant barrier. Additionally, managing the return cycle of packaging materials across multiple distribution points requires coordination between suppliers, distributors, and logistics providers. Any inefficiency in reverse logistics can lead to asset loss or underutilization, reducing overall cost benefits. In emerging markets, limited infrastructure further restricts large-scale RTP adoption.

Market Opportunities

Expansion in E-commerce and Retail Logistics

The rapid growth of e-commerce presents a major opportunity for the returnable transit packaging market. Online retail companies require efficient, durable, and reusable packaging solutions to manage high-volume product shipments. RTP systems can significantly reduce packaging waste while improving warehouse efficiency and return logistics. Large e-commerce players are increasingly adopting reusable totes and crates for intra-warehouse transportation and last-mile delivery operations. As online retail continues to expand globally, demand for standardized reusable packaging solutions is expected to increase significantly.

Adoption in Automotive and Industrial Manufacturing

The automotive and industrial manufacturing sectors offer strong growth opportunities for RTP adoption. These industries rely heavily on efficient supply chain systems for transporting components, parts, and finished goods. Returnable containers and pallets help reduce damage rates, improve inventory control, and optimize logistics efficiency. Automotive manufacturers are increasingly implementing closed-loop packaging systems across global production networks. The integration of RFID-enabled tracking and automated return systems is further enhancing efficiency, creating long-term growth potential for RTP solution providers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 11.6 Billion |

| Market Size in 2026 | USD 12.4 Billion |

| Market Size in 2034 | USD 25.9 Billion |

| CAGR | 9.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

Pallets held the dominant share of approximately 38% in 2024, driven by their extensive use in industrial logistics, warehousing, and transportation operations. Pallets are widely preferred due to their durability, compatibility with automated handling systems, and ability to support heavy loads across multiple industries such as automotive, retail, and food & beverage. Their standardized design also improves efficiency in storage and freight movement, making them a core component of returnable transit packaging systems.

Crates and bins are expected to grow at a CAGR of 10.6% (2025–2034), driven by increasing demand for reusable packaging in retail distribution, e-commerce fulfillment, and food logistics. These solutions offer flexibility, stackability, and space optimization benefits, making them suitable for high-frequency transportation cycles. Growth is further supported by rising adoption of closed-loop logistics systems and increasing focus on reducing packaging waste in supply chains.

By Material Type

Plastic-based returnable transit packaging dominated the market with approximately 44% share in 2024, due to its lightweight nature, durability, and resistance to moisture and chemicals. Plastic RTP solutions are widely used in automotive, FMCG, and retail logistics, where repeated usage and cost efficiency are critical. Their ability to withstand multiple reuse cycles makes them a preferred choice across global supply chains.

Metal-based RTP solutions are projected to grow at a CAGR of 9.8% (2025–2034), driven by demand for high-strength, long-life packaging systems in heavy industries. Metal containers and pallets are particularly used in automotive and industrial manufacturing sectors where durability and load-bearing capacity are essential. Increasing focus on long-term cost efficiency and lifecycle optimization is supporting growth in this segment.

By End-Use Industry

The automotive sector accounted for approximately 35% share in 2024, making it the largest end-use segment. Automotive manufacturers rely heavily on returnable transit packaging for transporting components, parts, and assemblies across global production networks. The need for standardized, damage-resistant, and reusable packaging solutions makes RTP systems integral to automotive supply chains.

The e-commerce sector is expected to grow at the fastest CAGR of 11.2% (2025–2034), driven by rapid expansion of online retail and increasing demand for efficient warehouse-to-customer logistics systems. Returnable totes, crates, and bins are being widely adopted for internal logistics and fulfillment center operations. Growth is further supported by rising demand for sustainable packaging solutions in digital retail ecosystems.

Returnable Transit Packaging Market Segmentations

By Product Type

- Pallets

- Crates & Bins

- Intermediate Bulk Containers (IBCs)

By Material Type

- Plastic

- Metal

- Wood

By End-Use Industry

- Automotive

- Food & Beverage

- E-commerce

- Retail & Consumer Goods

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for approximately 30% share of the returnable transit packaging market in 2025, with a projected CAGR of 9.4% (2025–2034). The region is driven by strong adoption of sustainable logistics practices, advanced supply chain infrastructure, and high penetration of automated warehousing systems. Demand is particularly strong across automotive, e-commerce, and food & beverage industries, where efficient material handling and reusable packaging solutions are widely implemented.

The United States dominates the regional market due to its large e-commerce ecosystem and well-established manufacturing base. A key growth factor is the increasing implementation of circular supply chain models by leading retail and industrial companies to reduce packaging waste and optimize logistics costs.

Europe

Europe held around 28% share in 2025, with a projected CAGR of 9.7% (2025–2034). Growth is strongly supported by strict environmental regulations, circular economy initiatives, and high adoption of reusable packaging systems across industrial sectors. The region has been an early adopter of returnable transit packaging due to sustainability mandates and corporate ESG commitments.

Germany leads the European market due to its strong automotive and industrial manufacturing base. A key growth factor is the European Union’s stringent packaging waste reduction policies, which are accelerating the transition from single-use to reusable transit packaging systems.

Asia Pacific

Asia Pacific accounted for approximately 27% share in 2025, and is expected to grow at the fastest CAGR of 10.2% (2025–2034). Growth is driven by rapid industrialization, expanding manufacturing output, and increasing investment in logistics and warehousing infrastructure. Rising exports and supply chain modernization are also boosting demand for standardized reusable packaging systems.

China dominates the regional market due to its large-scale manufacturing ecosystem and export-oriented industries. A key growth factor is the expansion of global supply chain networks and increasing adoption of cost-efficient returnable packaging solutions in industrial logistics.

Middle East & Africa

The Middle East & Africa region held approximately 6% share in 2025, with a projected CAGR of 8.8% (2025–2034). Growth is supported by logistics infrastructure development, rising industrial activity, and increasing adoption of modern supply chain practices in key economies. The region is gradually integrating reusable packaging systems into distribution and retail operations.

The United Arab Emirates leads the regional market due to its role as a global logistics hub. A key growth factor is the expansion of free trade zones and advanced warehousing facilities that support efficient returnable packaging operations.

Latin America

Latin America accounted for approximately 9% share in 2025, with a projected CAGR of 9.1% (2025–2034). Growth is driven by increasing industrial production, expansion of retail and e-commerce sectors, and rising focus on supply chain efficiency. Adoption of reusable packaging systems is gradually increasing across manufacturing and distribution networks.

Brazil dominates the regional market due to its strong industrial base and expanding logistics infrastructure. A key growth factor is the modernization of supply chain operations supported by increasing investments in manufacturing and retail distribution systems.

Competitive Landscape

The returnable transit packaging market is moderately consolidated with strong competition among global packaging and logistics solution providers. Key players focus on product durability, tracking technology integration, and sustainability-driven innovations. Major companies include ORBIS Corporation, CHEP (Brambles Ltd.), SSI Schaefer, Schoeller Allibert, and Greif Inc.

CHEP is a leading player due to its extensive global pallet pooling network. A recent development includes expansion of its circular logistics platform to improve asset tracking and reduce supply chain emissions.

Key Players List

- ORBIS Corporation

- CHEP (Brambles Ltd.)

- SSI Schaefer

- Schoeller Allibert

- Greif Inc.

- DS Smith

- Nefab Group

- Cabka Group

- Myers Industries

- Rehrig Pacific Company

- Georg Utz Holding

- Menasha Corporation

- Polymer Logistics

- UFP Technologies

- RPP Containers