Returnable Glass Bottle Market Report Size and Growth

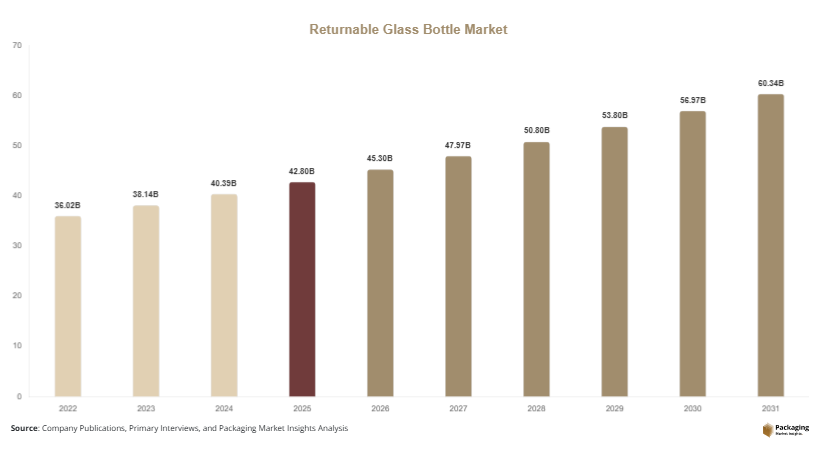

The Returnable Glass Bottle Market was valued at USD 42.80 billion in 2025 and is projected to reach USD 60.20 billion by 2030, registering a compound annual growth rate (CAGR) of 5.9% during 2025–2031. Returnable glass bottles are reusable containers designed for multiple filling cycles, primarily used across beverage industries such as beer, soft drinks, dairy, and bottled water. Their durability, recyclability, and cost efficiency over multiple use cycles make them a preferred sustainable packaging option.

The market growth has been supported by the global transition toward circular packaging systems. Governments and beverage manufacturers are implementing returnable bottle schemes to reduce packaging waste and carbon emissions. Deposit-return systems and refillable packaging programs have gained momentum in several regions, particularly in Europe and Asia Pacific. These initiatives encourage consumers to return used bottles for reuse, reducing the need for single-use packaging.

In addition, beverage manufacturers are adopting returnable glass bottles as part of their sustainability commitments. Companies are investing in durable bottle designs and automated cleaning and refilling systems that improve operational efficiency while extending bottle lifecycles. This shift toward closed-loop packaging ecosystems has strengthened the adoption of returnable glass bottles in both developed and emerging markets.

Key Highlights

- Europe dominated the market with approximately 38.5% share in 2025, while Asia Pacific is projected to grow at the fastest CAGR of 7.1% during the forecast period.

- In the product type segment, standard returnable bottles accounted for the largest share, whereas lightweight returnable bottles are expected to grow at the fastest CAGR of 6.8%.

- In the end-use segment, alcoholic beverages led the market, while non-alcoholic beverages are projected to grow at the fastest CAGR of 6.5%.

- Germany remained the dominant country, with market values estimated at USD 6.10 billion in 2025 and USD 6.40 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Deposit-Return Systems

Deposit-return systems (DRS) are becoming a critical trend shaping the Returnable Glass Bottle Market. Governments across Europe, North America, and parts of Asia Pacific are introducing policies that require consumers to return beverage containers in exchange for deposits. These programs encourage higher return rates and reduce packaging waste.

Retailers and beverage manufacturers are increasingly integrating automated reverse vending machines and bottle collection centers. These technologies streamline the return process and ensure bottles can be cleaned and reused efficiently. As environmental regulations continue to tighten, deposit-return systems are expected to play a growing role in driving returnable glass bottle adoption.

Lightweight and Durable Bottle Design

Another trend influencing the Returnable Glass Bottle Market is the development of lightweight yet durable glass bottles. Manufacturers are focusing on improving bottle strength while reducing material usage. Advanced glass forming technologies allow bottles to maintain durability across multiple reuse cycles while lowering transportation costs.

Lightweight designs also reduce carbon emissions during logistics and handling. Beverage companies increasingly prefer these bottle designs because they lower operational costs and improve sustainability metrics. As technology advances, lightweight returnable bottles are expected to gain wider adoption in global beverage packaging systems.

Market Drivers

Rising Demand for Sustainable Packaging

Growing awareness about environmental sustainability is a key driver of the Returnable Glass Bottle Market. Governments, consumers, and corporations are emphasizing packaging solutions that reduce waste and environmental impact.

Returnable glass bottles align with circular economy principles because they can be reused multiple times before recycling. Compared with single-use plastic bottles, returnable glass bottles significantly reduce packaging waste and raw material consumption. As sustainability commitments become central to corporate strategies, beverage companies are expanding refillable bottle programs globally.

Cost Efficiency in Long-Term Packaging Operations

Returnable glass bottles provide long-term cost advantages for beverage manufacturers. Although the initial production cost of a returnable bottle is higher than that of disposable packaging, the bottle can be reused many times before recycling.

This multi-cycle usage reduces overall packaging costs for companies operating large-scale beverage distribution networks. Automated washing and refilling technologies further enhance operational efficiency. As companies focus on cost optimization while meeting sustainability targets, returnable glass bottle systems continue to gain traction.

Market Restraint

High Logistics and Transportation Costs

Despite its advantages, the Returnable Glass Bottle Market faces challenges related to logistics and transportation. Glass bottles are heavier than plastic or aluminum alternatives, which increases transportation costs and energy consumption.

Additionally, returnable bottle systems require efficient collection, sorting, and cleaning infrastructure. Establishing such infrastructure involves significant investment and operational complexity. In regions lacking organized return networks, companies may hesitate to adopt returnable glass bottle systems, limiting market expansion.

Market Opportunities

Growth in Emerging Beverage Markets

Emerging economies present strong growth opportunities for the Returnable Glass Bottle Market. Rapid urbanization, rising disposable incomes, and expanding beverage consumption are increasing demand for packaged drinks.

Countries in Asia Pacific, Latin America, and Africa are witnessing growth in beer, carbonated beverages, and dairy sectors. As beverage companies expand production facilities in these markets, returnable glass bottle systems can offer cost-effective and sustainable packaging solutions.

Integration with Smart Packaging Systems

The integration of smart packaging technologies offers another opportunity for the Returnable Glass Bottle Market. Technologies such as QR codes, RFID tags, and digital tracking systems can improve bottle lifecycle monitoring and return logistics.

Smart systems help beverage companies track bottle usage, optimize return cycles, and reduce losses in supply chains. As digital technologies become more accessible, their integration into returnable packaging systems may enhance operational efficiency and market adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42.80 Billion |

| Market Size in 2026 | USD 45.30 Billion |

| Market Size in 2031 | USD 60.20 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

The standard returnable glass bottles subsegment dominated the market and accounted for around 61.4% of the market share in 2024. These bottles are widely used by beverage manufacturers due to their durability and compatibility with automated filling systems. Standard bottle formats simplify logistics because they can be reused across multiple beverage brands and distribution networks.

The lightweight returnable bottles subsegment will grow at the fastest CAGR of 6.8% during the forecast period. These bottles are designed using advanced glass manufacturing technologies that reduce material weight while maintaining structural strength. Beverage companies will increasingly adopt lightweight bottles to reduce transportation costs and carbon emissions.

By Capacity

The 500 ml to 1 liter capacity segment dominated the market and held approximately 47.6% share in 2024. This capacity range is widely used for beer, carbonated beverages, and mineral water packaging. Its popularity is linked to consumer preference for single-serving or moderate-size beverage packaging.

The less than 500 ml segment will experience the fastest growth, with a forecast CAGR of 6.4%. Smaller bottle sizes will gain traction due to increasing demand for portion-controlled beverage packaging. Beverage manufacturers will expand product offerings in smaller bottle formats to meet evolving consumer preferences.

By End-Use Industry

The alcoholic beverages segment dominated the Returnable Glass Bottle Market, accounting for approximately 52.3% share in 2024. Beer manufacturers have traditionally relied on returnable glass bottle systems due to their durability and ability to preserve beverage quality. Many breweries operate established bottle return and refill programs that support circular packaging models.

The non-alcoholic beverage segment will grow at the fastest CAGR of 6.5% during the forecast period. Increasing demand for carbonated soft drinks, flavored beverages, and mineral water will drive growth in this segment. Beverage manufacturers will adopt returnable glass bottle systems to meet sustainability targets and reduce packaging costs.

Returnable Glass Bottle Market Segmentations

By Product Type

- Standard Returnable Bottles

- Lightweight Returnable Bottles

By Capacity

- Less than 500 ml

- 500 ml to 1 liter

- More than 1 liter

By End-Use Industry

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Dairy Products

By Distribution Channel

- Direct Supply to Beverage Manufacturers

- Retail Return Systems

- Institutional Distribution

Regional Analysis

North America

North America accounted for approximately 21.5% of the Returnable Glass Bottle Market share in 2025. The regional market will expand at a forecast CAGR of 5.4% during 2025–2033. Market growth in the region has been influenced by sustainability initiatives from beverage manufacturers and regulatory pressure to reduce packaging waste.

The United States represented the dominant country within North America. A key factor supporting growth is the expansion of refillable bottle initiatives among craft beer breweries and carbonated beverage producers. Beverage companies are adopting returnable bottle systems to reduce packaging costs and align with environmental commitments.

Europe

Europe held the largest share of the Returnable Glass Bottle Market at 38.5% in 2025. The market in this region will grow at a CAGR of 5.8% through 2033. Europe’s leadership in the market has been driven by well-established deposit-return systems and strong consumer participation in recycling and reuse programs.

Germany remained the dominant country in the region. The country’s highly organized bottle return infrastructure enables efficient collection and reuse of glass bottles. Beverage companies in Germany widely use standardized bottle formats that can be reused across multiple brands, which improves operational efficiency.

Asia Pacific

Asia Pacific accounted for 26.3% of the global Returnable Glass Bottle Market in 2025. The region will grow at the fastest CAGR of 7.1% during the forecast period. Growth in the region is supported by expanding beverage manufacturing industries and increasing demand for sustainable packaging solutions.

China emerged as the dominant country in Asia Pacific. The country’s large beverage production sector and growing environmental regulations are encouraging the adoption of reusable packaging systems. Beverage manufacturers are investing in returnable glass bottle infrastructure to improve sustainability performance.

Middle East & Africa

The Middle East & Africa represented 7.2% of the Returnable Glass Bottle Market share in 2025. The market in this region will grow at a CAGR of 5.6% through 2033. Growth is supported by expanding beverage production and increasing focus on packaging waste reduction.

South Africa remained the leading country in the region. The growth factor in this market is the expansion of returnable bottle systems within the beer industry. Local beverage producers have adopted refillable glass bottle programs to reduce packaging costs and improve supply chain efficiency.

Latin America

Latin America accounted for 6.5% of the global Returnable Glass Bottle Market in 2025. The region will expand at a CAGR of 6.2% during the forecast period. Beverage companies in the region are implementing returnable bottle programs to address packaging waste challenges and reduce production costs.

Brazil was the dominant country in Latin America. The country’s beverage industry widely uses returnable glass bottles for beer and soft drink distribution. Beverage companies benefit from extensive bottle collection networks that enable efficient reuse cycles.

Competitive Landscape

The Returnable Glass Bottle Market features a moderately consolidated competitive environment with several global glass packaging manufacturers. Companies focus on product innovation, sustainable manufacturing, and partnerships with beverage companies.

O-I Glass, Inc. remained a leading player in the market due to its extensive manufacturing network and advanced glass container technologies. The company has been investing in lightweight returnable glass bottle solutions designed to reduce energy consumption and carbon emissions.

Other key players such as Ardagh Group, Verallia, Vetropack Holding AG, and Vidrala S.A. continue to expand production capacity and improve recycling infrastructure. Strategic collaborations with beverage companies and investments in sustainable packaging solutions remain common competitive strategies.

Key Players in the Returnable Glass Bottle Market

- O-I Glass, Inc.

- Ardagh Group S.A.

- Verallia S.A.

- Vetropack Holding AG

- Vidrala S.A.

- BA Glass

- Toyo Glass Co., Ltd.

- Nihon Yamamura Glass Co., Ltd.

- Amcor Glass Packaging

- Hindusthan National Glass & Industries Limited

- Saverglass Group

- Vitro Packaging

- Gerresheimer AG

- PGP Glass

- Piramal Glass Pvt. Ltd.