Retort Packaging Market Size and Growth

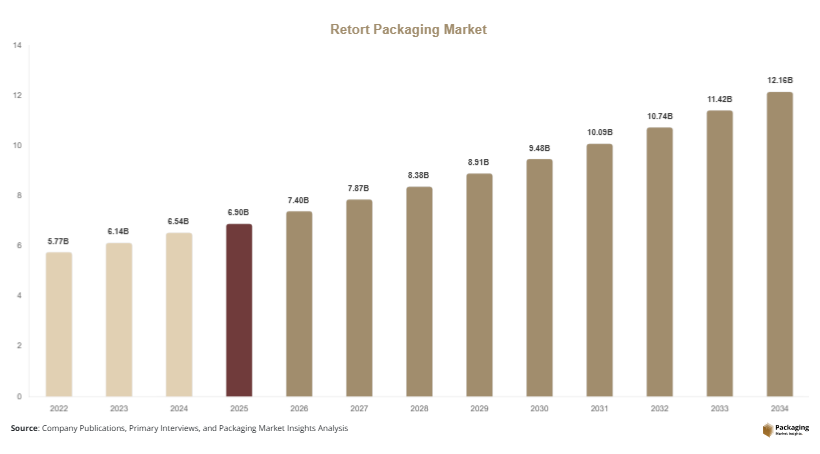

In 2025, the global retort packaging market size is estimated at USD 6.9 billion and is projected to reach USD 7.4 billion in 2026. The industry is expected to expand to approximately USD 12.8 billion by 2034, registering a compound annual growth rate (CAGR) of 6.4% during 2025–2034. This growth is largely supported by the increasing consumption of packaged ready-to-eat meals, advancements in multilayer packaging materials, and growing urbanization worldwide. Flexible retort pouches are gradually replacing traditional metal cans due to their lighter weight, lower transportation costs, and improved storage efficiency.

The retort packaging market is experiencing steady expansion as food manufacturers increasingly adopt packaging solutions that extend shelf life while maintaining product quality and safety. Retort packaging refers to heat-resistant flexible packaging used for sterilizing food and beverages after sealing. This packaging technology allows ready-to-eat meals, sauces, seafood, and pet food to remain shelf-stable without refrigeration. As global demand for convenient and long-lasting food products rises, the market continues to gain momentum across developed and emerging economies.

Key Highlights

- Global market size estimated at USD 6.9 billion in 2025

- Expected to reach USD 12.8 billion by 2034

- Projected CAGR of 6.4% from 2025 to 2034

- Flexible retort pouches gaining strong adoption across food applications

- Rising demand for convenience foods and shelf-stable meals driving growth

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Lightweight Flexible Retort Pouches

One of the most prominent retort packaging market trends is the increasing transition from rigid metal cans to lightweight flexible retort pouches. Food manufacturers are adopting multilayer pouch structures made from materials such as polyester, aluminum foil, and polypropylene. These structures offer strong heat resistance while maintaining barrier protection against oxygen and moisture. Compared with traditional cans, retort pouches reduce packaging weight significantly, which lowers transportation costs and carbon emissions. Retailers also benefit from improved shelf utilization because pouches occupy less storage space. As sustainability and logistics efficiency become critical priorities for food brands, flexible retort packaging formats are becoming a preferred option across ready meals, sauces, and seafood segments.

Integration of Sustainable and Recyclable Packaging Materials

Sustainability initiatives are reshaping the retort packaging market as manufacturers explore recyclable and environmentally responsible materials. Traditional multilayer structures can be difficult to recycle due to mixed material layers. In response, packaging companies are developing mono-material retort films and recyclable laminate technologies that maintain barrier performance while improving recyclability. These innovations align with global regulatory pressure and consumer awareness around packaging waste. Food brands are increasingly promoting eco-friendly packaging as part of their sustainability commitments. As governments introduce stricter packaging regulations and retailers prioritize environmentally responsible suppliers, sustainable retort packaging solutions are expected to gain wider adoption during the forecast period.

Market Drivers

Rising Global Demand for Ready-to-Eat and Convenience Foods

The growing consumption of convenience food products is a major factor driving the retort packaging market growth. Urbanization, busy lifestyles, and an expanding working population are influencing consumer food preferences worldwide. Ready-to-eat meals, instant soups, and pre-cooked rice products are increasingly popular because they require minimal preparation. Retort packaging enables manufacturers to sterilize these foods at high temperatures, ensuring microbial safety and long shelf life without refrigeration. This capability is particularly valuable for distribution through supermarkets, online grocery platforms, and export markets. As convenience foods continue to gain popularity across both developed and emerging economies, the demand for retort packaging solutions is expected to rise steadily.

Expansion of the Global Packaged Food Industry

The continued expansion of the packaged food industry is another important driver supporting the retort packaging market size. Food processing companies are investing heavily in advanced packaging technologies to extend shelf life and maintain product quality. Retort packaging provides superior barrier properties against oxygen, moisture, and light, helping preserve flavor, color, and nutritional value. These characteristics make it suitable for a wide range of applications including baby food, seafood, meat products, and pet food. Additionally, improvements in packaging machinery and high-speed filling systems are enabling efficient production of retort pouches at scale. As packaged food consumption grows globally, retort packaging demand is expected to increase across multiple product categories.

Market Restraint

Limited Recycling Infrastructure for Multilayer Retort Packaging

Despite its advantages, the retort packaging market faces challenges related to recycling and environmental sustainability. Most retort packaging structures are composed of multiple layers of materials such as plastic films, aluminum foil, and adhesives. While these layers provide excellent heat resistance and barrier properties, they complicate recycling processes. Many recycling facilities are not equipped to separate and process multilayer packaging materials efficiently, leading to increased landfill waste.

This limitation is creating concerns among regulators, environmental organizations, and consumers. Governments in several regions are implementing stricter packaging waste regulations that encourage the use of recyclable or compostable materials. Food manufacturers using conventional retort packaging may face pressure to transition toward more sustainable alternatives. For example, certain European countries are introducing extended producer responsibility programs that require packaging producers to manage recycling and waste collection.

As sustainability expectations continue to rise, companies operating in the retort packaging industry must invest in research and development to create recyclable multilayer films or mono-material retort solutions. Failure to address these environmental challenges could slow the adoption of traditional retort packaging formats in the long term.

Market Opportunities

Expansion of Shelf-Stable Food Products in Emerging Economies

Emerging economies present significant growth potential for the retort packaging market due to the rapid expansion of shelf-stable food categories. Countries across Asia Pacific, Latin America, and parts of Africa are experiencing rising disposable incomes and changing dietary habits. Consumers are increasingly purchasing packaged foods such as ready meals, soups, and sauces from supermarkets and convenience stores. Retort packaging offers an efficient solution for preserving these products without refrigeration, making it suitable for regions with limited cold-chain infrastructure. Food manufacturers entering these markets are adopting retort pouches to ensure product safety and longer shelf life. As retail networks expand and urbanization continues, demand for shelf-stable packaged foods is expected to grow.

Technological Innovation in High-Barrier Packaging Materials

Technological advancements in packaging materials represent another promising opportunity for the retort packaging market growth. Packaging manufacturers are investing in advanced barrier films that improve heat resistance, durability, and oxygen protection while reducing overall material usage. Innovations such as nano-coated films, high-performance polymer blends, and recyclable retort laminates are enhancing packaging functionality. These technologies enable food producers to maintain product quality while meeting sustainability and regulatory requirements. Furthermore, improved printing capabilities and flexible packaging designs are enhancing brand visibility on retail shelves. As research and development efforts continue to deliver innovative material solutions, the retort packaging industry is likely to witness new product launches and expanded application areas.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.9 Billion |

| Market Size in 2026 | USD 7.4 Billion |

| Market Size in 2034 | USD 12.8 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The pouches segment dominated the retort packaging market in 2024, accounting for approximately 46% of the total market share. Retort pouches have gained widespread adoption due to their lightweight structure and excellent barrier properties. These pouches typically consist of multilayer laminates that include polyester, aluminum foil, and polypropylene. The design allows food products to be sterilized at high temperatures while maintaining product integrity and taste. Compared with metal cans or rigid containers, retort pouches require less material and occupy less storage space during transportation and retail display. These advantages help food manufacturers reduce logistics costs while improving operational efficiency. As a result, many ready-meal and seafood brands prefer retort pouches as their primary packaging format.

The trays segment is projected to be the fastest-growing subsegment, registering a CAGR of around 7.1% during the forecast period. Retort trays are gaining popularity in premium ready-meal packaging because they offer a more convenient and attractive presentation. These trays are typically made from high-temperature resistant polymers that allow microwave heating without transferring the food to another container. This convenience appeals to consumers seeking quick meal solutions. Additionally, food service providers and airline catering companies are increasingly adopting retort trays for packaged meal solutions. The growing demand for microwaveable ready meals is expected to drive the expansion of this segment.

By Material

The polypropylene segment accounted for the largest share of the retort packaging market in 2024, representing approximately 38% of the total material usage. Polypropylene is widely used in retort packaging because of its strong heat resistance and excellent sealing properties. The material can withstand high sterilization temperatures while maintaining structural stability and product safety. Polypropylene is also compatible with multilayer film structures that provide additional barrier protection against moisture and oxygen. These characteristics make it suitable for packaging ready-to-eat meals, sauces, and processed meats. Food manufacturers often prefer polypropylene because it supports efficient high-speed packaging operations and ensures reliable sealing during retort processing.

The polyester segment is expected to register the fastest growth with a CAGR of about 7.3% through 2034. Polyester films offer high tensile strength and dimensional stability, which are essential for maintaining packaging integrity during thermal sterilization processes. These materials also support high-quality printing and branding on packaging surfaces, improving product visibility on retail shelves. As food brands increasingly focus on product presentation and shelf appeal, polyester-based retort laminates are gaining traction. Additionally, advancements in recyclable polyester films are encouraging manufacturers to adopt these materials in sustainable packaging initiatives.

By End-Use

The food segment held the dominant position in the retort packaging market , accounting for approximately 62% of the total demand in 2024. Retort packaging is widely used for packaging ready-to-eat meals, seafood, vegetables, sauces, soups, and rice products. The technology allows food products to be sterilized at high temperatures after sealing, eliminating harmful microorganisms and extending shelf life. This process ensures that food remains safe and fresh for long periods without refrigeration. Food manufacturers rely on retort packaging to distribute products across global markets and maintain consistent product quality during transportation and storage.

The pet food segment is expected to be the fastest-growing end-use category, with a CAGR of approximately 7.6% during the forecast period. Rising pet ownership and increasing spending on premium pet nutrition are driving demand for high-quality packaged pet food. Retort packaging is particularly suitable for wet pet food products because it preserves flavor and nutritional value while ensuring long shelf life. Pet food manufacturers are also adopting retort pouches with convenient features such as easy-tear openings and portion control packaging. As the global pet care industry expands, the demand for retort packaging in this segment is expected to increase steadily.

Retort Packaging Market Segmentations

Type

- Pouches

- Trays

- Cartons

- Others

Material

- Polypropylene

- Polyester

- Aluminum Foil

- Polyamide

- Others

End-Use

- Food

- Beverage

- Pet Food

- Others

Regional Analysis

North America

North America accounted for approximately 27% of the global retort packaging market share in 2025. The region is expected to grow at a CAGR of around 5.8% during the forecast period. Growth is driven by high consumption of packaged foods and well-established food processing industries. Retail chains and online grocery platforms in the United States and Canada are expanding their offerings of ready-to-eat meals, soups, and sauces, which rely heavily on retort packaging technologies to maintain shelf stability.

The United States represents the dominant country within the North American market. One unique growth factor in the region is the strong presence of large food manufacturers investing in advanced packaging innovations. Companies are adopting lightweight retort pouches and improved barrier materials to reduce logistics costs and enhance product shelf appeal. Continuous investments in packaging automation and food safety regulations also contribute to market growth.

Europe

Europe held nearly 24% of the retort packaging market share in 2025 and is projected to grow at a CAGR of approximately 5.5% through 2034. Demand for retort packaging in the region is driven by increasing consumption of convenience meals and shelf-stable packaged foods. European consumers prefer products that offer both convenience and high food safety standards, encouraging manufacturers to adopt advanced sterilization and packaging technologies.

Germany remains a key contributor to the European market. A unique growth factor in the region is the strong regulatory focus on sustainable packaging solutions. European packaging companies are actively developing recyclable retort films and environmentally responsible materials. This shift toward sustainable packaging innovation is expected to shape the regional market during the forecast period.

Asia Pacific

Asia Pacific dominated the retort packaging market in 2025 with an estimated 36% global market share and is forecast to expand at a CAGR of about 7.4% through 2034. Rapid urbanization, population growth, and increasing demand for ready-to-eat meals are major factors driving regional growth. Countries across the region are experiencing strong expansion in retail food chains and packaged food production.

China is the largest market in the region. A unique growth factor is the rapid expansion of domestic food processing companies producing shelf-stable meals for urban consumers. Additionally, the rise of online grocery platforms and modern retail formats is supporting demand for convenient packaged foods, further increasing the adoption of retort packaging technologies.

Middle East & Africa

The Middle East & Africa accounted for approximately 7% of the global retort packaging market share in 2025 and is expected to grow at a CAGR of around 6.2% over the forecast period. The market is gaining traction as packaged food imports and local food manufacturing industries expand. Retort packaging is particularly valuable in regions with high temperatures, where shelf-stable food products require durable packaging.

Saudi Arabia represents one of the dominant markets in the region. A key growth factor is the expansion of food security initiatives and local food processing investments. Governments are encouraging domestic food production to reduce reliance on imports, which is creating demand for reliable packaging technologies such as retort pouches.

Latin America

Latin America held around 6% of the retort packaging market share in 2025 and is anticipated to grow at a CAGR of approximately 6.6% through 2034. Increasing urban populations and rising consumption of packaged food products are supporting market expansion. Supermarkets and convenience stores across major cities are expanding shelf-stable food product offerings.

Brazil leads the regional market. A unique growth factor is the growing popularity of ready-to-eat traditional meals packaged in retort pouches. Local food producers are adopting retort packaging to deliver authentic regional dishes with extended shelf life, enabling distribution across broader geographic areas.

Competitive Landscape

The retort packaging market is moderately competitive and consists of global packaging manufacturers along with regional flexible packaging providers. Leading companies focus on product innovation, sustainable material development, and expansion of production capacities to strengthen their market presence. Strategic collaborations with food manufacturers are also common as packaging companies aim to develop customized solutions tailored to specific product requirements.

Among industry participants, Amcor plc is widely recognized as a market leader due to its extensive portfolio of flexible packaging solutions and strong global distribution network. The company continues to invest in recyclable retort packaging materials designed to meet evolving sustainability regulations. Several competitors are also focusing on technological innovations such as high-barrier multilayer films and lightweight packaging structures.

Companies are increasingly investing in research and development to improve heat resistance, barrier performance, and recyclability of retort packaging materials. In addition, mergers, acquisitions, and partnerships are helping manufacturers expand their geographic footprint and strengthen supply chains. As food manufacturers demand advanced packaging technologies, competition in the retort packaging industry is expected to remain dynamic throughout the forecast period.

Key Players List

- Amcor plc

- Berry Global Group

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Coveris Holdings

- Huhtamaki Oyj

- Winpak Ltd.

- ProAmpac

- Constantia Flexibles

- Glenroy Inc.

- Clondalkin Group

- Toppan Holdings

- Dai Nippon Printing

- Uflex Limited