Release Liners Market Size and Growth

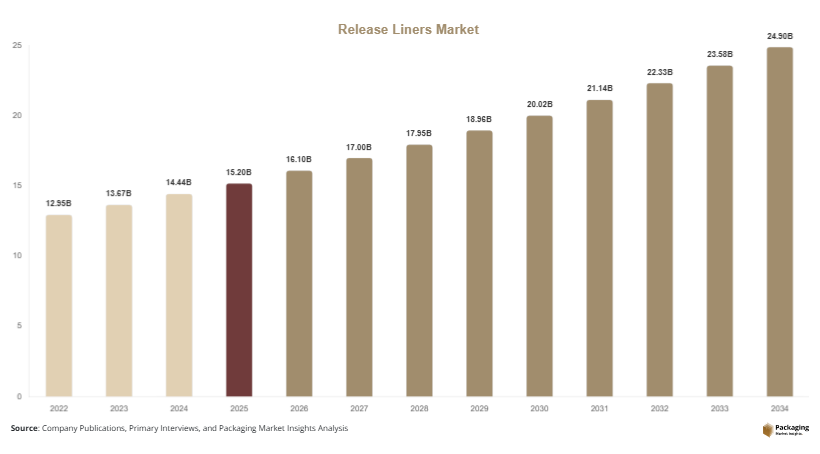

The global release liners market size was valued at approximately USD 15.2 billion in 2025 and is projected to reach USD 16.1 billion in 2026. Over the forecast period, the market is expected to attain a value of USD 24.9 billion by 2034, registering a CAGR of 5.6% from 2025 to 2034. Release liners are widely used as backing materials coated with release agents, enabling easy separation from adhesive products such as tapes, labels, and medical patches. The release liners market is experiencing consistent growth driven by the expanding use of pressure-sensitive adhesives across packaging, hygiene, healthcare, and industrial applications.

A key growth factor is the increasing demand for pressure-sensitive labels in the packaging industry. The expansion of e-commerce, retail, and logistics sectors has significantly increased the need for labeling solutions, thereby driving the demand for release liners. Another important factor is the rising consumption of hygiene and medical products. Release liners are extensively used in diapers, sanitary products, and wound care applications, which are witnessing strong demand due to population growth and increasing healthcare awareness.

Key Highlights

- Asia Pacific dominated the market with a 38.9% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Paper-based liners led the type segment with a 41.2% share, while film-based liners are expected to grow at a CAGR of 6.1%.

- Plastic packaging dominated with a 51.8% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Label applications led the segment with 44.7% share, while hygiene products are expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 3.1 billion in 2025 and USD 3.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Release Liners

Sustainability is becoming a central focus in the release liners market. Manufacturers are developing recyclable and reusable liner materials to reduce environmental impact. The growing awareness of plastic waste and regulatory pressures are encouraging companies to adopt eco-friendly solutions. Paper-based release liners and silicone-free coatings are gaining traction as alternatives to conventional materials. Additionally, liner recycling programs are being implemented to recover and reuse materials, reducing waste generation. These initiatives are not only addressing environmental concerns but also creating cost-saving opportunities for end-users. The trend toward sustainable solutions is expected to shape the future of the market.

Advancements in Coating Technologies and Digital Printing Compatibility

Technological advancements in coating processes are driving innovation in the release liners market. Improved silicone and non-silicone coatings are enhancing release properties and durability. These advancements are enabling the production of high-performance liners suitable for various applications. Additionally, the increasing adoption of digital printing technologies is influencing the demand for release liners. High-quality liners that support advanced printing techniques are becoming essential for labeling applications. The ability to customize labels and improve print quality is driving the adoption of advanced release liners. This trend is expected to contribute to market growth.

Market Drivers

Growth in Pressure-Sensitive Labels and Packaging Industry

The expansion of the packaging industry is a major driver of the release liners market. Pressure-sensitive labels are widely used in packaging applications due to their convenience and versatility. The growth of e-commerce and retail sectors is increasing the demand for labeling solutions, thereby driving the need for release liners. These liners play a crucial role in protecting adhesive surfaces until application. Additionally, the demand for branded and customized packaging is supporting the adoption of high-quality release liners. As packaging requirements continue to evolve, the demand for release liners is expected to grow.

Rising Demand from Hygiene and Medical Applications

The increasing demand for hygiene and medical products is another key driver of the release liners market. Products such as diapers, sanitary napkins, and wound care items rely on release liners for adhesive protection. The growing population and rising healthcare awareness are driving the demand for these products. Additionally, the aging population is increasing the need for medical and hygiene products, further supporting market growth. Release liners are essential in ensuring product functionality and safety, making them a critical component in these applications.

Market Restraint

Environmental Concerns and Disposal Challenges

Environmental concerns related to the disposal of release liners are a significant restraint for the market. Many release liners are coated with silicone, which makes recycling difficult. The accumulation of non-recyclable waste is creating challenges for manufacturers and end-users. Regulatory pressures aimed at reducing waste and promoting sustainability are also impacting the market. For example, restrictions on landfill disposal are encouraging companies to seek alternative solutions. These challenges require investment in recycling technologies and sustainable materials, which can increase costs and affect profitability.

Market Opportunities

Development of Silicone-Free and Recyclable Liner Solutions

The development of silicone-free release liners presents significant opportunities for the market. These liners are easier to recycle and have a lower environmental impact compared to traditional silicone-coated liners. Manufacturers are investing in research and development to create innovative solutions that meet sustainability requirements. The adoption of these materials is expected to increase as companies focus on reducing their environmental footprint. Additionally, the development of recyclable liners is creating opportunities for new business models, such as liner recycling programs.

Expansion in Emerging Markets and Industrial Applications

Emerging markets offer substantial growth opportunities for the release liners market. Rapid industrialization and urbanization in regions such as Asia Pacific and Latin America are driving demand for packaging and industrial materials. The expansion of manufacturing sectors in these regions is creating opportunities for release liners in applications such as composites, electronics, and automotive components. Additionally, the increasing adoption of modern retail formats is supporting the demand for labeling solutions. As emerging economies continue to develop, the market for release liners is expected to expand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.2 Billion |

| Market Size in 2026 | USD 16.1 Billion |

| Market Size in 2034 | USD 24.9 Billion |

| CAGR | 5.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Paper-based liners accounted for the largest market share in 2024, contributing 41.2% to the overall market. These liners are widely used due to their cost-effectiveness and recyclability. The demand for paper-based liners is driven by the increasing focus on sustainable packaging solutions. Additionally, these liners provide good strength and compatibility with various adhesive applications, making them suitable for labeling and packaging industries.

Film-based liners are expected to grow at the fastest CAGR of 6.1%. These liners offer superior strength, flexibility, and moisture resistance. The increasing demand for high-performance materials in industrial and medical applications is driving the growth of this segment. Film-based liners are also used in applications where durability and precision are required.

By Application

Label applications accounted for the largest market share in 2024, contributing 44.7% to the overall market. Release liners are widely used in pressure-sensitive labels for packaging and logistics. The growth of e-commerce and retail sectors is driving the demand for labeling solutions. Additionally, the need for product identification and branding is supporting the adoption of release liners in this segment.

Hygiene applications are expected to grow at the fastest CAGR of 6.3%. The increasing demand for diapers, sanitary products, and medical items is driving the growth of this segment. Release liners are essential in protecting adhesive components in these products, ensuring functionality and safety.

By End-Use

Packaging industry accounted for the largest market share in 2024. Release liners are widely used in packaging applications for labeling and adhesive protection. The increasing demand for packaging materials is driving the growth of this segment. Additionally, the rise of e-commerce is supporting the adoption of release liners in packaging.

Healthcare sector is expected to grow at the fastest CAGR of 6.2%. The increasing demand for medical and hygiene products is driving the growth of this segment. Release liners are used in various healthcare applications, including wound care and medical tapes.

Release Liners Market Segmentations

By Type

- Paper-Based Liners

- Film-Based Liners

- Others

By Application

- Labels

- Hygiene Products

- Industrial Applications

By End-Use

- Packaging Industry

- Healthcare Sector

- Industrial Sector

Regional Analysis

North America

North America accounted for approximately 22.4% of the global market share in 2025 and is expected to grow at a CAGR of 5.2% during the forecast period. The region benefits from a well-established packaging and healthcare industry. The demand for release liners is driven by the growth of pressure-sensitive labels and hygiene products. Additionally, the focus on sustainability is influencing market trends.

The United States dominates the regional market due to its large consumer base and advanced manufacturing capabilities. A key growth factor is the increasing adoption of automation in packaging processes, which is driving demand for high-performance release liners.

Europe

Europe held a market share of 23.7% in 2025 and is projected to grow at a CAGR of 5.4%. The region is characterized by stringent environmental regulations and a strong focus on sustainability. The demand for release liners is supported by the need for eco-friendly packaging solutions. Additionally, the growth of the healthcare industry is contributing to market expansion.

Germany is the leading country in the European market, supported by its strong industrial base. A unique growth factor is the increasing investment in sustainable materials and recycling technologies.

Asia Pacific

Asia Pacific dominated the market with a 38.9% share in 2025 and is expected to grow at a CAGR of 6.1%. The region’s growth is driven by rapid industrialization and increasing consumer demand for packaged goods. The expansion of e-commerce is also supporting market growth.

China leads the regional market due to its large manufacturing base and growing demand for packaging materials. A key growth factor is the increasing production of consumer goods, which is driving the demand for release liners.

Middle East & Africa

The Middle East & Africa region accounted for 6.1% of the market share in 2025 and is expected to grow at a CAGR of 5.5%. The region is witnessing growth in industrial and healthcare sectors, which is driving demand for release liners. Additionally, infrastructure development is supporting market expansion.

The United Arab Emirates is the dominant country in the region. A unique growth factor is the increasing development of logistics hubs, which is boosting demand for packaging materials.

Latin America

Latin America held a market share of 8.9% in 2025 and is projected to grow at the fastest CAGR of 6.4%. The region is experiencing growth in the consumer goods and retail sectors. The demand for release liners is supported by the increasing adoption of modern retail formats.

Brazil dominates the regional market due to its expanding consumer base. A key growth factor is the increasing demand for hygiene products, which is driving the adoption of release liners.

Competitive Landscape

The release liners market is moderately competitive, with several global and regional players focusing on innovation and expansion strategies. Companies are investing in advanced coating technologies and sustainable materials to enhance product performance and meet environmental requirements. Strategic partnerships and acquisitions are common approaches adopted by market players.

Ahlstrom is recognized as a leading player in the market, known for its innovative product offerings and strong market presence. The company recently introduced recyclable release liners to support sustainability initiatives. Other players are also focusing on product innovation and capacity expansion to strengthen their market position.

Key Players List

- Ahlstrom

- Mondi Group

- UPM-Kymmene Corporation

- Sappi Limited

- Loparex LLC

- Lintec Corporation

- 3M Company

- Avery Dennison Corporation

- Siliconature S.p.A.

- Polyplex Corporation Ltd.

- Felix Schoeller Group

- Delfort Group

- Rayven Inc.

- Infiana Group

- Itasa S.A.