Recycled Glass Market Size and Growth

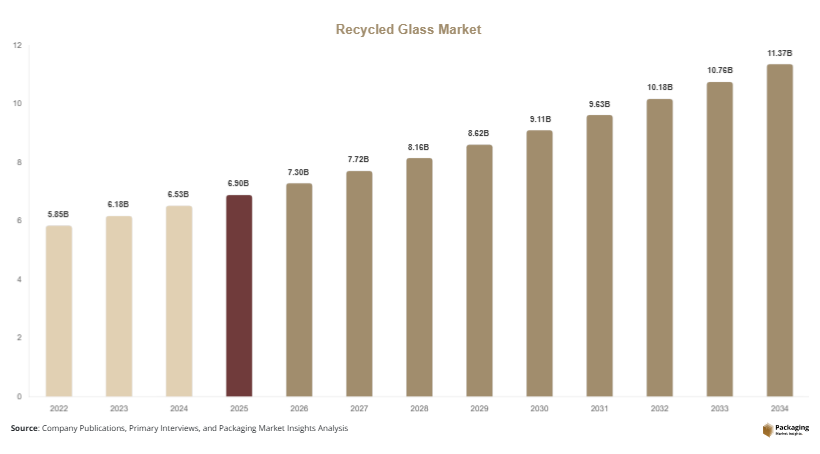

The global recycled glass market was valued at USD 6.9 billion in 2025 and is projected to reach USD 11.4 billion by 2034, expanding at a CAGR of 5.7% during the forecast period from 2025 to 2034. The market reached an estimated value of USD 7.3 billion in 2026. The market is witnessing stable expansion due to increasing demand for sustainable raw materials across packaging, construction, automotive, and fiberglass manufacturing industries. Recycled glass, commonly referred to as cullet, is extensively used to reduce energy consumption, minimize landfill waste, and lower carbon emissions associated with virgin glass production. Governments and manufacturers are increasingly investing in circular economy initiatives, supporting long-term growth of the recycled glass industry.

The rising use of recycled glass in container manufacturing remains one of the primary growth contributors. Beverage companies, food manufacturers, and pharmaceutical packaging producers are adopting high recycled-content glass packaging to comply with sustainability commitments and environmental regulations. Glass manufacturers are also increasing cullet utilization rates to reduce furnace operating temperatures and improve production efficiency. In addition, growing consumer preference for recyclable and reusable packaging materials is strengthening demand for recycled glass across developed and emerging economies.

Key Market Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5%.

- Container glass led the type segment with a 41.3% share.

- Glass bottle recycling dominated the material segment with a 57.4% share.

- Packaging applications led the end-use segment with 46.8% share.

- The US remained the dominant country with a market size of USD 1.5 billion in 2025 and USD 1.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Closed-Loop Glass Recycling Systems

Manufacturers across beverage, pharmaceutical, and food packaging industries are increasingly adopting closed-loop recycling systems to improve sustainability and reduce raw material dependency. Closed-loop recycling allows recovered glass to be reused in the production of new glass containers without quality degradation. Major beverage companies are collaborating with municipal recycling facilities and packaging suppliers to secure stable cullet supplies. For example, several European beverage producers are increasing recycled content in glass bottles beyond 50% to meet environmental commitments and carbon reduction targets.

This trend is expected to strengthen over the coming years as governments introduce stricter packaging waste regulations and recycling targets. Improved collection infrastructure and consumer participation in recycling programs are likely to increase glass recovery rates. Manufacturers using higher recycled content can reduce furnace energy consumption and operational costs, improving long-term profitability. The growing emphasis on circular economy models will continue driving investments in advanced glass recovery technologies.

Rising Use of Recycled Glass in Sustainable Construction Materials

Recycled glass is increasingly being used in sustainable construction products such as decorative tiles, insulation materials, countertops, and concrete aggregates. Construction companies are integrating recycled materials into green building projects to meet environmental certification standards and reduce landfill waste. Crushed recycled glass is also being used in road construction and drainage systems due to its durability and cost efficiency. Several infrastructure projects across Asia Pacific and North America have increased the adoption of recycled glass aggregates in urban development activities.

The future impact of this trend is expected to be significant as governments expand investments in sustainable infrastructure and energy-efficient buildings. Demand for environmentally friendly construction materials is projected to rise steadily due to stricter carbon emission regulations. Manufacturers are likely to introduce improved recycled glass composites with higher durability and thermal insulation performance. Increasing awareness regarding sustainable architecture and green building standards will further accelerate market growth.

Market Drivers

Expansion of Sustainable Packaging Industry

The rapid expansion of sustainable packaging solutions is one of the primary drivers supporting growth in the recycled glass market. Food, beverage, and pharmaceutical manufacturers are increasingly shifting toward recyclable packaging materials to meet environmental goals and improve brand positioning. Recycled glass packaging reduces energy consumption during manufacturing and lowers greenhouse gas emissions compared to virgin glass production. Beverage companies are particularly increasing the use of recycled cullet in bottle manufacturing to comply with circular economy initiatives.

The growing popularity of premium glass packaging in alcoholic beverages, sauces, cosmetics, and healthcare products is creating higher demand for recycled glass inputs. For instance, several global beverage brands have announced plans to increase recycled content in packaging over the next decade. This trend is encouraging glass manufacturers to invest in recycling infrastructure and material recovery technologies. The increasing adoption of sustainable packaging regulations across Europe and North America is expected to strengthen long-term demand.

Government Regulations Supporting Recycling Activities

Government regulations promoting recycling and landfill reduction are significantly contributing to recycled glass market growth. Several countries have implemented mandatory recycling targets, deposit return schemes, and waste segregation programs to improve recycling rates. These initiatives encourage higher collection volumes and increase the availability of recyclable glass materials. Regulations focused on reducing industrial waste and carbon emissions are also pushing manufacturers toward sustainable raw material sourcing.

For example, European countries continue to strengthen packaging waste directives and recycling mandates to reduce environmental impact. Similarly, North American municipalities are expanding curbside recycling infrastructure to improve glass recovery efficiency. These regulatory initiatives are encouraging investments in advanced recycling plants and automated sorting technologies. As governments continue focusing on sustainable waste management practices, the recycled glass market is expected to experience stable long-term growth.

Market Restraint

High Transportation and Processing Costs

High transportation and processing costs remain a major restraint for the recycled glass market. Glass is relatively heavy and fragile compared to alternative recyclable materials, making transportation expensive over long distances. Collection, sorting, cleaning, and color separation processes also require significant operational investments. Smaller recycling facilities often face profitability challenges due to rising fuel prices and labor expenses. In many developing countries, inadequate recycling infrastructure further limits efficient collection and processing activities.

Contamination from ceramics, metals, and plastics can reduce recycled glass quality and increase processing complexity. Mixed-color cullet also creates limitations for manufacturers requiring high-purity recycled materials for packaging applications. For example, food-grade glass manufacturers often require strict contamination control standards, increasing operational costs for recyclers. These factors may restrict market growth in regions lacking advanced recycling systems. However, ongoing investments in automation and sorting technologies are expected to gradually improve operational efficiency and reduce processing challenges over the forecast period.

Market Opportunities

Growth in Fiberglass Insulation Manufacturing

The increasing demand for fiberglass insulation products presents a strong opportunity for recycled glass manufacturers. Recycled glass is widely used as a raw material in fiberglass production due to its thermal stability and energy efficiency benefits. Rising construction activities and growing adoption of energy-efficient buildings are driving demand for fiberglass insulation materials globally. Governments are also promoting insulation products to reduce energy consumption in residential and commercial infrastructure.

Manufacturers are expanding fiberglass production capacity to meet growing demand from construction and industrial sectors. Recycled glass suppliers can benefit from long-term contracts with insulation producers seeking stable cullet supplies. The expansion of sustainable housing projects and green building standards is expected to further increase fiberglass consumption. This opportunity is likely to create additional revenue streams for recycling companies during the forecast period.

Emerging Demand from Automotive Applications

The automotive industry is creating new opportunities for recycled glass applications in lightweight vehicle components and sustainable manufacturing processes. Recycled glass is increasingly used in automotive fiberglass, reflective materials, and interior design components. Electric vehicle manufacturers are particularly focusing on sustainable material sourcing to reduce carbon emissions throughout the supply chain. This trend is increasing interest in recycled raw materials across automotive manufacturing facilities.

Several automotive suppliers are investing in recycled-content materials for insulation, coatings, and lightweight composites. The expansion of electric vehicle production across China, Europe, and North America is expected to support long-term demand for recycled glass products. Technological advancements in glass processing and composite manufacturing may also create innovative automotive applications in the coming years. As sustainability regulations continue strengthening in the automotive industry, recycled glass demand is projected to rise steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.9 Billion |

| Market Size in 2026 | USD 7.3 Billion |

| Market Size in 2034 | USD 11.4 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Container glass dominated the type segment with a 41.3% market share in 2024 due to strong demand from beverage, food, and pharmaceutical packaging industries. Glass bottles and jars remain widely used because of their recyclability, chemical stability, and premium product appeal. Beverage manufacturers are increasingly adopting recycled-content container glass to reduce carbon emissions and comply with sustainability regulations. Several packaging companies are investing in lightweight bottle manufacturing and higher cullet utilization rates to improve production efficiency. Demand from alcoholic beverages, sauces, dairy products, and pharmaceutical containers continues to strengthen the dominance of this segment globally.

Processed cullet is projected to grow at the fastest CAGR of 6.8% during the forecast period. Processed cullet offers improved purity, color separation, and compatibility with advanced manufacturing systems. Rising investments in automated sorting technologies and contamination reduction systems are supporting segment expansion. Manufacturers prefer processed cullet due to lower energy consumption and reduced furnace operating costs. Growing adoption in fiberglass insulation, construction aggregates, and specialty glass manufacturing is expected to drive future demand. The increasing focus on sustainable manufacturing practices will continue creating growth opportunities for processed cullet suppliers.

By Material

Glass bottle recycling dominated the material segment with a 57.4% share in 2024 due to the large-scale consumption of bottled beverages and food packaging products worldwide. Beverage manufacturers generate significant post-consumer glass waste, creating a stable supply stream for recycling companies. Collection programs, deposit return systems, and municipal recycling initiatives continue supporting high recovery rates for glass bottles. Manufacturers also prefer recycled bottle glass because it reduces raw material costs and improves environmental sustainability performance. Strong demand from breweries, wineries, and soft drink manufacturers further contributes to segment dominance.

Industrial glass recycling is expected to register the fastest CAGR of 6.2% through 2034. Industrial glass waste from electronics, automotive, and construction industries is increasingly being recycled into insulation products, decorative materials, and specialty applications. Advancements in material recovery technologies are improving the processing efficiency of industrial glass waste. Growing investments in sustainable industrial manufacturing and waste reduction programs are supporting segment growth. The expansion of renewable energy projects and green infrastructure development is expected to create additional opportunities for industrial glass recycling companies over the forecast period.

By End-Use

Packaging applications led the end-use segment with a 46.8% market share in 2024 due to rising global demand for recyclable and reusable packaging solutions. Food, beverage, pharmaceutical, and cosmetic industries continue increasing the use of recycled-content glass packaging to improve sustainability performance and meet regulatory requirements. Glass packaging offers strong barrier properties, product safety, and premium branding advantages, supporting continued adoption across consumer goods industries. Beverage companies are also investing in lightweight recyclable glass packaging to reduce transportation costs and carbon emissions.

Construction applications are projected to grow at the fastest CAGR of 6.4% during the forecast period. Recycled glass is increasingly used in tiles, countertops, insulation materials, road aggregates, and decorative concrete products. Governments and developers are promoting sustainable building materials to reduce environmental impact and improve energy efficiency. Rising investments in green infrastructure projects across Asia Pacific, Europe, and the Middle East are supporting strong demand for recycled glass construction materials. Technological innovations in recycled glass composites and decorative building products are expected to accelerate future segment growth.

Recycled Glass Market Segmentations

By Type

- Container Glass

- Processed Cullet

- Fiberglass Glass

- Flat Glass

- Specialty Glass

By Material

- Glass Bottle Recycling

- Industrial Glass Recycling

- Flat Glass Recycling

- Mixed Glass Recycling

- Colored Glass Recycling

By End-User

- Packaging

- Construction

- Automotive

- Fiberglass Insulation

- Electronics

- Others

Regional Analysis

North America

North America accounted for 26.8% of the global recycled glass market share in 2025 and is projected to expand at a CAGR of 5.3% during the forecast period. The region benefits from strong recycling infrastructure, growing environmental awareness, and rising adoption of sustainable packaging materials. Beverage manufacturers across the United States and Canada are increasingly using recycled-content glass bottles to reduce carbon emissions and improve sustainability performance. Government initiatives supporting landfill reduction and waste recycling are also contributing to market expansion. Rising investments in automated recycling systems and smart waste management technologies are improving glass collection efficiency across urban areas.

The United States remained the dominant country in North America due to its large beverage packaging industry and strong recycling ecosystem. The country is witnessing increasing investments in municipal recycling facilities and container recovery programs. Several beverage brands are partnering with recycling companies to improve cullet supply chains and increase recycled content usage in packaging. Demand for fiberglass insulation products in construction projects is also supporting recycled glass consumption. Rising consumer preference for sustainable packaging and green building materials is expected to strengthen market growth across the country.

Europe

Europe held 29.4% of the global recycled glass market share in 2025 and is expected to grow at a CAGR of 5.5% through 2034. The region has one of the most developed recycling systems globally, supported by strict environmental regulations and circular economy policies. European countries continue to implement packaging waste reduction targets and deposit return schemes, encouraging higher glass collection rates. Strong demand from beverage, pharmaceutical, and cosmetic packaging industries is driving recycled glass utilization across manufacturing facilities. Investments in low-carbon manufacturing technologies are also contributing to market growth.

Germany dominated the European recycled glass market due to its advanced waste management infrastructure and high recycling participation rates. The country has established efficient glass collection systems and strong government support for sustainable manufacturing practices. German beverage manufacturers are increasingly adopting high recycled-content glass packaging to meet carbon neutrality targets. The expansion of green construction projects and fiberglass insulation manufacturing is also supporting recycled glass demand. Growing investments in sustainable industrial production are expected to maintain Germany’s leadership position during the forecast period.

Asia Pacific

Asia Pacific dominated the recycled glass market with a 38.6% share in 2025 and is projected to grow at a CAGR of 6.1% through 2034. Rapid urbanization, industrialization, and rising consumption of packaged products are supporting strong demand for recycled glass across the region. Governments in China, Japan, South Korea, and India are implementing recycling initiatives and sustainable waste management policies to reduce landfill pressure. Increasing beverage production and growing construction activities are further strengthening market expansion. The region is also witnessing rising investments in recycling infrastructure and material recovery facilities.

China remained the largest market within Asia Pacific due to its large manufacturing base and expanding packaging industry. The country is investing heavily in sustainable industrial practices and circular economy initiatives to reduce environmental impact. Rising consumption of bottled beverages and pharmaceutical packaging products is increasing demand for recycled glass materials. Chinese construction companies are also using recycled glass aggregates and insulation materials in infrastructure projects. The expansion of domestic recycling facilities and advanced sorting technologies is expected to support continued market growth.

Middle East & Africa

The Middle East & Africa recycled glass market accounted for 8.1% of global revenue in 2025 and is projected to expand at a CAGR of 5.8% during the forecast period. Increasing urban development activities and growing investments in waste management infrastructure are supporting market growth across the region. Governments are introducing sustainability programs to reduce landfill waste and encourage recycling initiatives. The hospitality and beverage industries are also increasing demand for recyclable glass packaging solutions. Rising awareness regarding environmental protection is contributing to gradual expansion of recycling activities.

Saudi Arabia emerged as the dominant country within the region due to increasing infrastructure projects and industrial diversification initiatives. The country is investing in sustainable construction materials and recycling technologies as part of long-term economic transformation programs. Demand for recycled glass in insulation materials and decorative construction products is increasing steadily. Beverage and food packaging manufacturers are also adopting recyclable packaging solutions to align with sustainability objectives. Continued expansion of industrial recycling facilities is expected to improve recycled glass utilization across the country.

Latin America

Latin America is projected to register the fastest CAGR of 6.5% during the forecast period due to expanding recycling awareness and growing demand for sustainable packaging solutions. The region is witnessing increasing investments in waste collection infrastructure and recycling facilities, particularly in Brazil, Mexico, and Chile. Rising urbanization and growing packaged food consumption are supporting demand for recyclable glass materials. Beverage manufacturers are also increasing the use of recycled-content bottles to improve environmental performance and reduce packaging costs.

Brazil dominated the Latin American recycled glass market due to its large beverage industry and growing recycling ecosystem. The country is witnessing increasing collaboration between packaging manufacturers and recycling companies to improve cullet recovery rates. Government initiatives promoting waste segregation and circular economy practices are supporting industry expansion. The construction sector is also adopting recycled glass materials for decorative and infrastructure applications. Growing investments in sustainability-focused manufacturing are expected to create long-term market opportunities across Brazil and neighboring economies.

Competitive Landscape

The recycled glass market remains moderately consolidated, with major players focusing on capacity expansion, strategic partnerships, advanced sorting technologies, and regional recycling infrastructure development. Leading companies are investing heavily in automated recovery systems, optical sorting equipment, and sustainable manufacturing practices to improve cullet quality and operational efficiency. Market participants are also collaborating with beverage manufacturers, municipalities, and waste management companies to secure long-term recycled glass supply contracts.

Strategic acquisitions and facility modernization projects are becoming common across North America and Europe. Companies are expanding regional recycling plants to increase processing capacity and improve collection efficiency. Several firms are also investing in low-carbon furnace technologies and closed-loop recycling systems to strengthen sustainability performance. The increasing demand for food-grade recycled glass and fiberglass manufacturing materials is encouraging manufacturers to enhance contamination control capabilities.

Strategic Materials Inc. remained one of the leading companies in the market due to its extensive recycling network, advanced glass processing operations, and strong partnerships with packaging manufacturers. The company continues expanding its recycling infrastructure across North America to support growing demand for high-quality cullet materials. Ardagh Group and O-I Glass are also increasing recycled content usage in glass packaging production to improve carbon reduction performance.

European companies are focusing on circular economy initiatives and high glass recovery rates, while Asian manufacturers are expanding recycling capacity to support rapid industrial growth. Companies operating in emerging economies are investing in municipal recycling programs and waste collection systems to improve raw material availability. Increasing demand for sustainable packaging and construction materials is expected to intensify competition over the forecast period.

Key Players List

- Strategic Materials Inc.

- O-I Glass Inc.

- Ardagh Group S.A.

- Vetropack Holding Ltd.

- Momentum Recycling LLC

- Glass Recycled Surfaces

- Gallo Glass Company

- Encirc Ltd.

- Dlubak Glass Company

- Trivitro Corporation

- Harsco Minerals International

- Binder+Co AG

- Berryman Glass Recycling

- REMONDIS SE & Co. KG

- Pace Glass Inc.