Recycled Aluminum Cans Market Size and Growth

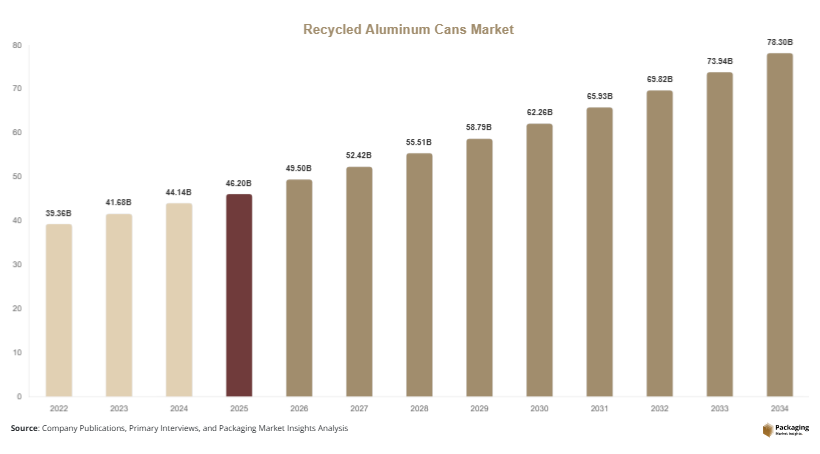

The global recycled aluminum cans market size was valued at USD 46.2 billion in 2025 and is projected to reach USD 49.5 billion in 2026. By 2034, the market is expected to grow to USD 82.8 billion, registering a CAGR of 5.9% during the forecast period from 2025 to 2034. This growth is supported by the increasing emphasis on recycling efficiency, resource conservation, and environmental sustainability. The recycled aluminum cans market is expanding steadily as industries and governments focus on circular economy practices and sustainable packaging solutions.

One of the primary growth factors is the rising demand for sustainable packaging in the beverage industry. Aluminum cans are widely used for soft drinks, beer, and energy drinks due to their recyclability and durability. Recycled aluminum requires significantly less energy compared to primary aluminum production, making it an attractive option for manufacturers aiming to reduce carbon emissions. Another important factor is the implementation of strict government regulations promoting recycling and waste reduction. Policies such as deposit return schemes and extended producer responsibility programs are encouraging higher recycling rates and boosting market growth.

Key Highlights

- Asia Pacific dominated the market with a 35.9% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Used beverage cans (UBC) led the type segment with a 61.7% share, while post-industrial recycled aluminum is expected to grow at a CAGR of 6.1%.

- Beverage packaging dominated with a 72.5% share, while food packaging is forecasted to grow at a CAGR of 5.8%.

- Soft drinks applications led the segment with 39.8% share, while energy drinks are expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 9.6 billion in 2025 and USD 10.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of closed-loop recycling systems

The recycled aluminum cans market is witnessing a growing adoption of closed-loop recycling systems, where used aluminum cans are collected, processed, and reused to produce new cans. This system reduces waste and conserves natural resources by minimizing the need for virgin aluminum production. Beverage companies and recycling firms are collaborating to establish efficient collection and processing networks. Closed-loop systems also help reduce carbon emissions and energy consumption, making them an essential part of sustainability strategies. As awareness about circular economy practices increases, more companies are expected to adopt closed-loop recycling models to improve environmental performance and meet regulatory requirements.

Growing demand for lightweight and sustainable packaging

The demand for lightweight and sustainable packaging is influencing the recycled aluminum cans market. Aluminum cans are preferred due to their ability to preserve product quality while being easy to transport and recycle. Manufacturers are focusing on reducing the weight of cans without compromising strength, which helps lower material usage and transportation costs. This trend aligns with sustainability goals and cost optimization strategies. Additionally, brands are emphasizing the use of recycled content in packaging to enhance their environmental credentials. As consumers become more environmentally conscious, the demand for lightweight and recyclable packaging solutions is expected to grow steadily.

Market Drivers

Increasing environmental regulations and recycling mandates

Government regulations promoting recycling and waste reduction are a major driver of the recycled aluminum cans market. Many countries have implemented policies such as deposit return systems and recycling targets to encourage the collection and reuse of aluminum cans. These regulations aim to reduce landfill waste and conserve natural resources. Compliance with these policies requires companies to adopt recycling practices and use recycled materials in production. This has led to increased demand for recycled aluminum. As governments continue to strengthen environmental regulations, the market is expected to benefit from higher recycling rates and increased adoption of sustainable packaging.

Rising consumption of packaged beverages globally

The growing consumption of packaged beverages is driving demand for recycled aluminum cans. Urbanization, changing lifestyles, and increasing disposable incomes are contributing to higher consumption of soft drinks, beer, and energy drinks. Aluminum cans are widely used in the beverage industry due to their convenience, durability, and recyclability. The expansion of beverage production in emerging markets is further supporting market growth. Additionally, the trend toward on-the-go consumption is increasing demand for portable and lightweight packaging solutions. As beverage consumption continues to rise, the demand for recycled aluminum cans is expected to grow significantly.

Market Restraint

Fluctuating raw material prices and supply chain challenges

The recycled aluminum cans market faces challenges due to fluctuations in raw material prices and supply chain constraints. The availability of scrap aluminum depends on collection rates and recycling efficiency, which can vary across regions. Changes in global aluminum prices also impact the cost of recycled materials. For example, disruptions in supply chains can lead to shortages of scrap aluminum, affecting production levels. Additionally, the cost of collecting and processing recycled materials can be high, particularly in regions with limited infrastructure. These factors can create uncertainty for manufacturers and impact profitability. Addressing these challenges requires investment in efficient recycling systems and stable supply chains.

Market Opportunities

Expansion of recycling infrastructure in emerging economies

The development of recycling infrastructure in emerging economies presents significant opportunities for the recycled aluminum cans market. Governments and private organizations are investing in collection and processing facilities to improve recycling rates. These investments are helping to increase the availability of recycled aluminum and reduce dependence on virgin materials. As infrastructure improves, manufacturers can access a more stable supply of recycled materials. Additionally, public awareness campaigns are encouraging consumers to participate in recycling programs. This trend is expected to drive market growth in regions with previously low recycling rates.

Increasing corporate sustainability initiatives

Corporate sustainability initiatives are creating new opportunities in the recycled aluminum cans market. Many companies are setting targets to reduce carbon emissions and increase the use of recycled materials. Beverage manufacturers, in particular, are committing to using higher percentages of recycled aluminum in their packaging. These initiatives are driving demand for high-quality recycled materials and encouraging innovation in recycling technologies. Companies are also collaborating with recycling firms to develop efficient systems for material recovery. As sustainability becomes a key business priority, the demand for recycled aluminum cans is expected to increase.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46.2 Billion |

| Market Size in 2026 | USD 49.5 Billion |

| Market Size in 2034 | USD 82.8 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Used beverage cans (UBC) held the largest share of the recycled aluminum cans market in 2024, accounting for approximately 61.7%. This segment is driven by the high volume of aluminum cans used in the beverage industry. UBCs are widely collected and recycled due to their economic value and ease of processing. Recycling these cans requires less energy compared to producing new aluminum, making them a preferred choice for manufacturers. The established collection systems in many regions further support the dominance of this segment.

Post-industrial recycled aluminum is expected to grow at a CAGR of 6.1%. This segment includes aluminum waste generated during manufacturing processes. The growth is driven by the increasing focus on reducing industrial waste and improving resource efficiency. Companies are adopting recycling practices to minimize material loss and reduce costs. Advances in processing technologies are also improving the quality of recycled aluminum, supporting its use in various applications.

By Application

Beverage packaging accounted for the largest share of the market in 2024, with approximately 72.5%. Aluminum cans are widely used in the beverage industry due to their ability to preserve product quality and extend shelf life. The demand for canned beverages is increasing, driven by convenience and portability. This supports the growth of the recycled aluminum cans market.

Food packaging is expected to grow at a CAGR of 5.8%. The use of aluminum cans in food packaging is increasing due to their durability and recyclability. Advances in packaging technology are improving the performance of aluminum cans for food products. This segment is expected to grow as demand for sustainable packaging solutions increases.

By End-Use

Soft drinks dominated the market in 2024, accounting for approximately 39.8% of the total share. The high consumption of soft drinks globally drives demand for aluminum cans. Manufacturers prefer recycled aluminum due to its cost efficiency and environmental benefits. The growth of the soft drinks industry continues to support this segment.

Energy drinks are expected to grow at a CAGR of 6.3%. The increasing popularity of energy drinks among younger consumers is driving demand for aluminum cans. These products require packaging that preserves quality and supports branding. Recycled aluminum cans provide an effective solution, supporting growth in this segment.

Recycled Aluminum Cans Market Segmentations

By Type

- Used Beverage Cans (UBC)

- Post-Industrial Recycled Aluminum

By Application

- Beverage Packaging

- Food Packaging

By End-Use

- Soft Drinks

- Alcoholic Beverages

- Energy Drinks

- Food Products

Regional Analysis

North America

North America accounted for approximately 28.7% of the recycled aluminum cans market share in 2025 and is projected to grow at a CAGR of 5.6%. The region benefits from established recycling infrastructure and strong regulatory support. High consumer awareness and participation in recycling programs contribute to market growth. The presence of major beverage companies also drives demand for recycled aluminum cans.

The United States dominates the regional market due to its extensive beverage industry and advanced recycling systems. A key growth factor is the widespread implementation of deposit return schemes, which encourage consumers to return used cans for recycling. This system improves collection rates and supports the availability of recycled materials.

Europe

Europe held around 27.3% of the market share in 2025 and is expected to grow at a CAGR of 5.7%. The region is known for its strong environmental regulations and high recycling rates. Policies promoting circular economy practices are driving demand for recycled aluminum cans.

Germany leads the European market due to its well-developed recycling infrastructure. A unique growth factor is the region’s focus on achieving high recycling efficiency through advanced sorting and processing technologies. This approach ensures a consistent supply of high-quality recycled materials.

Asia Pacific

Asia Pacific dominated the market with a 35.9% share in 2025 and is projected to grow at a CAGR of 6.2%. Rapid urbanization, increasing beverage consumption, and growing environmental awareness are driving market growth. The region’s large population base supports high demand for packaged beverages.

China is the dominant country in this region due to its strong manufacturing capabilities. Government initiatives promoting recycling and waste reduction are a key growth factor. These initiatives are encouraging investment in recycling infrastructure and improving material recovery rates.

Middle East & Africa

The Middle East & Africa region held a market share of approximately 4.5% in 2025 and is expected to grow at a CAGR of 5.8%. Increasing awareness about sustainability and improving waste management systems are supporting market growth. The beverage industry is a key contributor to demand.

South Africa is a leading market due to its growing recycling initiatives. A unique growth factor is the increasing involvement of private organizations in waste collection and recycling programs. These efforts are improving recycling rates and supporting market expansion.

Latin America

Latin America accounted for around 3.6% of the market in 2025 and is projected to grow at a CAGR of 6.4%. The region is witnessing increasing demand for sustainable packaging solutions due to environmental concerns and regulatory support.

Brazil dominates the regional market due to its high recycling rates and strong beverage industry. A unique growth factor is the presence of informal recycling networks, which contribute significantly to the collection of used aluminum cans and support market growth.

Competitive Landscape

The recycled aluminum cans market is moderately competitive, with several global and regional players focusing on improving recycling efficiency and expanding production capacity. Companies are investing in advanced technologies to enhance material recovery and reduce costs. Strategic partnerships with beverage companies and recycling organizations are common.

Novelis Inc. is a leading player in the market, known for its strong focus on sustainability and recycling. The company recently expanded its recycling capacity to meet growing demand for recycled aluminum. Other major players are also investing in infrastructure and innovation to strengthen their market positions.

Key Players List

- Novelis Inc.

- Ball Corporation

- Crown Holdings, Inc.

- Ardagh Group S.A.

- Constellium SE

- Kaiser Aluminum Corporation

- Hydro Aluminium

- Hindalco Industries Limited

- Rio Tinto Aluminum

- Alcoa Corporation

- China Hongqiao Group Limited

- Norsk Hydro ASA

- UACJ Corporation

- Metal Packaging Europe

- Amcor plc