Recycle Ready Retort Pouches Market Size and Growth

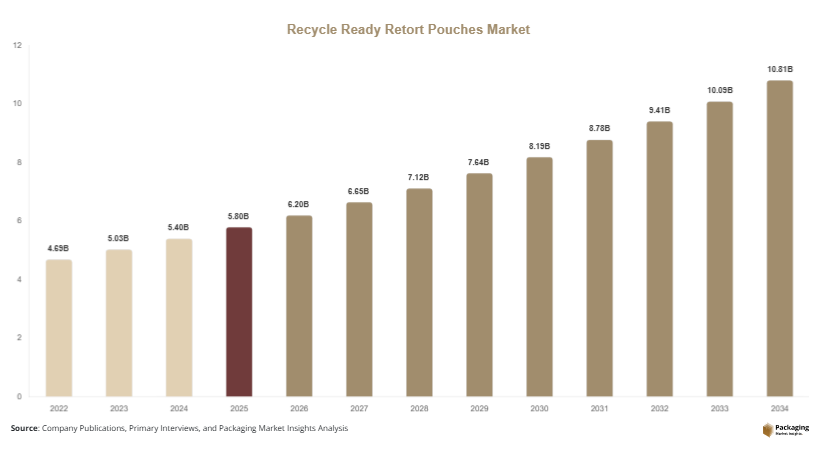

The global recycle ready retort pouches market was valued at USD 5.8 billion in 2025 and is estimated to reach USD 6.2 billion in 2026. The market is projected to further expand to USD 10.9 billion by 2034, growing at a CAGR of 7.2% during the forecast period from 2025 to 2034. The market is witnessing significant growth due to increasing demand for sustainable flexible packaging solutions across food, beverage, pet food, and ready-to-eat meal industries. Recycle-ready retort pouches are designed to withstand high-temperature sterilization processes while maintaining compatibility with existing recycling streams, making them an attractive alternative to conventional multilayer packaging materials.

The market continues to benefit from the growing consumer preference for lightweight and environmentally responsible packaging formats. Food manufacturers are increasingly replacing rigid metal cans and traditional multilayer laminates with recyclable retort pouch structures to reduce transportation costs, improve shelf appeal, and comply with sustainability targets. Rising awareness regarding plastic waste reduction and circular economy initiatives is further encouraging investments in mono-material high-barrier packaging technologies.

Key Market Highlights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.9%.

- Polypropylene-based retort pouches led the type segment with a 34.8% share.

- Plastic-based recyclable structures dominated with a 61.7% share.

- Food & beverage applications led the segment with 48.9% share.

- The US accounted for an estimated market size of USD 0.9 billion in 2025 in the global recycle ready retort pouches market.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Mono-Material Retort Packaging

Packaging manufacturers are increasingly focusing on mono-material recyclable retort pouch structures to improve recycling efficiency and reduce multilayer plastic waste. Traditional retort pouches often contain mixed material laminates including aluminum foil, polyester, and nylon, which are difficult to recycle through standard waste management systems. Companies are now developing polypropylene and polyethylene-based high-barrier pouch structures that maintain thermal resistance while remaining recyclable.

Food brands are using mono-material retort pouches for ready meals, sauces, and seafood packaging to meet sustainability goals and consumer expectations. Several supermarket chains in Europe have introduced recyclable private-label food packaging to reduce landfill waste and improve circular packaging adoption. This trend is expected to reshape material innovation investments across the packaging sector. Over the coming years, improved barrier coatings and advanced resin technologies will further enhance shelf life and retort performance for recyclable pouch formats.

Growth of Sustainable Convenience Food Packaging

The rapid growth of convenience food consumption is significantly increasing demand for recyclable retort pouch packaging solutions. Urban consumers prefer lightweight, portable, and easy-to-store food packaging formats that reduce preparation time while maintaining product freshness. Recycle-ready retort pouches are increasingly used for soups, ready-to-eat rice, baby food, and pet food applications.

Food manufacturers are adopting digital printing and lightweight pouch technologies to improve branding while lowering transportation emissions. In Asia Pacific, convenience food producers are rapidly replacing metal cans with recyclable pouches to reduce packaging costs and improve logistics efficiency. The trend is expected to strengthen as retailers and governments implement sustainability requirements for packaging waste reduction. Future developments in smart packaging integration and bio-based barrier materials may further increase adoption of recyclable retort packaging globally.

Market Drivers

Expansion of Ready-to-Eat Food Consumption

The growing demand for ready-to-eat meals and shelf-stable packaged foods is a major driver supporting the growth of the recycle ready retort pouches market. Consumers increasingly seek convenient food products with longer shelf life, portability, and minimal storage requirements. Retort pouches provide excellent protection against moisture, oxygen, and contamination while enabling high-temperature sterilization processes.

Food manufacturers prefer retort pouches because they reduce packaging weight and transportation expenses compared to rigid packaging alternatives. Large food processing companies are expanding production of packaged soups, seafood products, curries, and instant meals using recyclable pouch formats. This transition is supporting demand for sustainable retort packaging technologies. Rising urbanization, changing dietary habits, and increasing workforce participation rates are expected to further strengthen the market during the forecast period.

Increasing Sustainability Regulations and Corporate Commitments

Government regulations targeting single-use plastic waste reduction are accelerating the transition toward recyclable packaging solutions across the food packaging industry. Several countries are implementing packaging recycling targets and extended producer responsibility regulations that encourage manufacturers to adopt recyclable pouch technologies.

Major food and beverage companies are also committing to recyclable packaging goals to strengthen brand reputation and reduce environmental impact. Packaging suppliers are responding by developing recyclable retort structures compatible with existing recycling infrastructure. For example, European food brands are increasingly adopting aluminum-free retort pouches to improve recyclability. Rising investments in sustainable packaging research and material recovery systems are expected to create favorable conditions for long-term market expansion.

Market Restraint

High Technical Complexity in Recyclable Barrier Packaging

One of the major restraints affecting the recycle ready retort pouches market is the technical difficulty associated with maintaining high barrier performance while ensuring recyclability. Retort packaging must withstand high-temperature sterilization processes and provide protection against oxygen, moisture, and contamination. Traditional multilayer structures achieve this performance using complex combinations of foil, nylon, and polyester materials, but these materials are difficult to recycle.

Developing mono-material recyclable alternatives that deliver similar durability and shelf-life performance remains a major challenge for packaging manufacturers. Some recyclable pouch structures also face limitations in sealing strength and puncture resistance during transportation and storage. Smaller food manufacturers may hesitate to transition due to higher production costs and equipment modification requirements. In emerging economies, inadequate recycling infrastructure and inconsistent waste collection systems further limit large-scale adoption of recyclable retort packaging solutions.

Market Opportunities

Expansion of Sustainable Pet Food Packaging

The rapid expansion of premium pet food products is creating strong opportunities for recyclable retort pouch manufacturers. Pet food companies are increasingly adopting sustainable flexible packaging to improve brand positioning and reduce packaging waste. Retort pouches are widely used for wet pet food products because they maintain freshness and provide convenient handling for consumers.

Manufacturers are introducing recyclable mono-material pouch designs specifically for pet food applications. The growing trend toward human-grade pet food packaging and premium branding is expected to increase demand for advanced recyclable pouch technologies. North America and Europe are expected to remain major markets due to strong pet ownership rates and rising consumer preference for environmentally responsible pet care products.

Development of Advanced Barrier Coating Technologies

Advanced barrier coating technologies present major opportunities for packaging manufacturers operating in the recyclable retort pouch market. Companies are investing in transparent high-barrier coatings and retort-compatible sealant layers that improve recyclability without sacrificing product protection. These innovations can significantly expand the application range of recyclable retort packaging across pharmaceutical, food, and personal care industries.

The adoption of nanocoatings, water-based barrier layers, and bio-based polymers is expected to increase in the coming years. Flexible packaging producers are also collaborating with recycling companies to develop pouch structures optimized for mechanical recycling systems. As global packaging regulations become stricter, advanced recyclable barrier technologies are likely to become a key competitive differentiator in the market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5.8 Billion |

| Market Size in 2026 | USD 6.2 Billion |

| Market Size in 2034 | USD 10.9 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polypropylene-based retort pouches dominated the type segment with a 34.8% market share in 2024. These pouches are widely used because they provide strong heat resistance, sealing performance, and barrier protection during sterilization processes. Food manufacturers prefer polypropylene structures for packaged meals, seafood, sauces, and pet food applications due to their durability and cost efficiency. Packaging companies are increasingly developing recyclable polypropylene retort solutions compatible with existing recycling streams. The segment also benefits from rising demand for lightweight packaging that reduces logistics expenses. In Asia Pacific, polypropylene pouch adoption remains high due to the strong presence of convenience food manufacturing industries. Improved transparency, puncture resistance, and product shelf stability further strengthen the dominance of this segment.

Mono-material polyethylene retort pouches are expected to register the fastest CAGR of 8.1% during the forecast period. These pouches are gaining popularity because they improve recyclability while supporting flexible packaging sustainability goals. Packaging companies are investing heavily in advanced polyethylene barrier films and retort-compatible sealant layers to improve performance under high-temperature sterilization conditions. Food brands are adopting polyethylene recyclable structures to align with circular economy targets and retailer sustainability requirements. The growing focus on mono-material packaging innovation is expected to increase adoption across packaged foods, baby food, and pet food sectors. Future advancements in high-barrier resin technologies and coating systems are likely to accelerate commercial deployment globally.

By Material

Plastic-based recyclable structures dominated the material segment with a 61.7% share in 2024. These materials remain widely used because they provide excellent flexibility, sealing strength, lightweight properties, and compatibility with retort sterilization processes. Polypropylene and polyethylene-based films are commonly used in recyclable pouch manufacturing because they offer improved heat resistance and cost-effective production. Food processing companies continue to prefer plastic-based structures due to their ability to preserve product freshness and reduce transportation costs. Advanced multilayer recyclable plastic films are also supporting demand across convenience food packaging applications. In developed regions, packaging manufacturers are investing in recyclable resin innovation and downgauging technologies to improve environmental performance while maintaining packaging durability.

Paper-laminate recyclable structures are expected to witness the fastest CAGR of 7.4% during the forecast period. Growing consumer preference for sustainable packaging materials is increasing interest in paper-based retort pouch solutions. Packaging companies are developing coated paper structures capable of withstanding moisture exposure and sterilization processes while maintaining recyclability. Food brands are using paper-based packaging to strengthen eco-friendly branding and reduce dependence on conventional plastics. The segment is expected to benefit from growing regulatory pressure regarding single-use plastic reduction across Europe and North America. Improvements in barrier coatings, water resistance technologies, and hybrid fiber structures are likely to enhance commercial adoption over the next decade.

By End-Use

Food & beverage applications dominated the end-use segment with a 48.9% market share in 2024. Recycle-ready retort pouches are widely used for packaged rice, soups, sauces, seafood, dairy products, and ready meals due to their convenience and shelf-life advantages. Food manufacturers prefer retort pouches because they reduce storage space requirements and improve transportation efficiency compared to rigid containers. Rising urbanization and changing dietary preferences are supporting strong demand for packaged convenience foods globally. The segment also benefits from increasing investment in sustainable packaging technologies among large food processing companies. Retailers are encouraging recyclable flexible packaging adoption to improve environmental performance and reduce packaging waste within supply chains.

Pet food packaging is projected to expand at the fastest CAGR of 8.3% during the forecast period. Premium pet food manufacturers are increasingly adopting recyclable retort pouches to improve sustainability and product differentiation. Wet pet food packaging applications require strong barrier protection and sterilization resistance, making recyclable retort pouches an attractive solution. Growing pet ownership rates and rising spending on premium pet nutrition products are contributing to segment growth. Companies are introducing lightweight recyclable packaging formats with improved shelf appeal and convenience features such as resealable closures. Continued innovation in mono-material pet food packaging solutions is expected to create substantial growth opportunities over the forecast period.

Recycle Ready Retort Pouches Market Segmentations

By Type

- Polypropylene-Based Retort Pouches

- Polyethylene-Based Retort Pouches

- Aluminum-Free Retort Pouches

- Paper-Laminate Retort Pouches

By Material

- Plastic

- Paper

- Polymer Films

- Hybrid Laminates

By End-User

- Food & Beverage

- Pet Food

- Healthcare

- Personal Care

- Industrial Products

Regional Analysis

North America

North America accounted for 24.8% of the global recycle ready retort pouches market share in 2025 and is projected to grow at a CAGR of 6.8% during the forecast period. The region continues to benefit from strong demand for sustainable food packaging solutions and increasing adoption of recyclable flexible packaging across retail and e-commerce sectors. Rising consumption of ready-to-eat meals, packaged seafood, and shelf-stable products is driving packaging innovation in the United States and Canada. Large food brands are investing in recyclable pouch formats to comply with corporate sustainability targets and reduce packaging waste. Growth in online grocery delivery services is also supporting demand for lightweight and durable retort pouch solutions.

The United States dominates the regional market due to its advanced food processing industry and growing investment in sustainable packaging technologies. Major packaging companies are collaborating with food manufacturers to develop recyclable high-barrier pouch structures suitable for sterilized food products. Retailers are increasingly encouraging suppliers to transition toward recyclable packaging formats. The expansion of premium pet food products and packaged meal kits is also supporting pouch demand. In addition, recycling infrastructure improvements and extended producer responsibility initiatives are expected to strengthen recyclable pouch adoption across the country.

Europe

Europe represented 22.3% of the global market share in 2025 and is forecasted to expand at a CAGR of 6.9% through 2034. The region is witnessing strong demand for recyclable retort packaging due to strict environmental regulations and ambitious packaging waste reduction goals. European governments continue to implement circular economy policies encouraging recyclable and reusable packaging materials across food and consumer goods industries. Flexible packaging producers are rapidly investing in mono-material retort pouch technologies to meet sustainability requirements and retailer expectations.

Germany remains the dominant country within the European market due to its strong packaging manufacturing industry and advanced recycling systems. Food manufacturers are increasingly replacing conventional multilayer laminates with recyclable pouch formats for soups, sauces, and convenience meals. Several supermarket chains are expanding recyclable private-label packaging programs to improve environmental performance. In addition, increasing investments in high-barrier coating technologies and recyclable polymer research are supporting regional market expansion. Demand for premium sustainable packaging formats is expected to rise steadily across France, Italy, and the United Kingdom.

Asia Pacific

Asia Pacific dominated the global recycle ready retort pouches market with a 39.1% share in 2025 and is expected to maintain strong growth at a CAGR of 7.6% during the forecast period. Rapid urbanization, growing packaged food consumption, and expanding middle-class populations are driving significant demand for flexible retort packaging across the region. Countries including China, India, Japan, and South Korea are major production hubs for packaged foods and convenience meals. Rising investments in sustainable packaging manufacturing and export-oriented food processing industries are further accelerating market growth.

China remains the leading country in the region due to its large-scale food manufacturing sector and increasing focus on recyclable packaging solutions. Domestic food brands are adopting lightweight recyclable pouches to reduce transportation costs and improve sustainability performance. Government initiatives supporting plastic waste reduction are encouraging investments in recyclable packaging technologies. Japan is also contributing to regional growth through advanced material innovation and premium food packaging demand. Meanwhile, India is experiencing rising demand for retort pouch packaging in instant food and dairy applications due to changing consumer lifestyles and retail modernization.

Middle East & Africa

The Middle East & Africa market accounted for 6.8% of global revenue in 2025 and is projected to grow at a CAGR of 6.1% through 2034. The region is gradually adopting recyclable retort pouch packaging as food processing industries expand and sustainability awareness improves. Demand for shelf-stable packaged food products is increasing due to urban population growth and changing consumer purchasing behavior. Flexible pouch packaging is gaining popularity because of its lightweight structure, longer shelf life, and transportation efficiency in hot climatic conditions.

Saudi Arabia dominates the regional market due to strong investments in food manufacturing and retail expansion. Government-led diversification initiatives are supporting domestic food production and packaging modernization. Food companies are increasingly adopting recyclable retort pouches for sauces, seafood, and ready meals to improve operational efficiency and reduce material usage. South Africa is also witnessing rising demand for sustainable packaging formats in packaged food exports. Growth in modern retail chains and packaged convenience food consumption is expected to create additional opportunities across the region.

Latin America

Latin America held 7.0% of the global market share in 2025 and is projected to register the fastest CAGR of 7.9% during the forecast period. Increasing packaged food consumption, retail modernization, and expansion of flexible packaging production are contributing to regional market growth. Food manufacturers are gradually shifting toward recyclable retort packaging to improve sustainability performance and reduce logistics costs. The growing popularity of ready-to-eat meals and packaged meat products is further supporting demand for high-barrier recyclable pouches.

Brazil dominates the Latin American market due to its large food processing industry and expanding flexible packaging sector. Domestic packaging manufacturers are investing in recyclable film production to support rising consumer demand for sustainable packaging solutions. Export-oriented food companies are also adopting recyclable pouch technologies to meet international sustainability requirements. Mexico is emerging as another important market due to rapid growth in packaged food exports and increasing adoption of modern retail distribution channels. Continued investments in recycling infrastructure are expected to support long-term regional market expansion.

Competitive Landscape

The recycle ready retort pouches market remains moderately consolidated, with major packaging companies focusing on sustainable material innovation, barrier technology development, and strategic partnerships with food manufacturers. Companies are investing heavily in recyclable flexible packaging research to improve heat resistance, oxygen barrier performance, and compatibility with recycling systems.

Amcor plc remains one of the leading players in the market due to its extensive recyclable packaging portfolio and strong global manufacturing network. The company continues to expand its mono-material retort pouch offerings for food and pet food applications. Mondi Group and Berry Global are also actively investing in recyclable flexible packaging technologies to strengthen their market position.

Sealed Air Corporation is focusing on lightweight sustainable packaging solutions for convenience food and protein packaging applications. Sonoco Products Company is expanding its recyclable pouch product portfolio to address growing demand from food processing industries. Meanwhile, Huhtamaki is increasing investments in fiber-based flexible packaging innovation to improve circular packaging adoption.

Competition is expected to intensify as companies develop advanced recyclable barrier structures and collaborate with recycling infrastructure providers. Digital printing integration, downgauging technologies, and high-performance mono-material films are expected to remain major strategic priorities across the industry.

Key Players List

- Amcor plc

- Mondi Group

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- ProAmpac LLC

- Constantia Flexibles

- Coveris Holdings S.A.

- Glenroy Inc.

- Winpak Ltd.

- Clondalkin Group

- Bischof + Klein SE & Co. KG

- UFlex Limited

- LC Packaging International BV