Recyclable Shrink Film Market Size and Growth

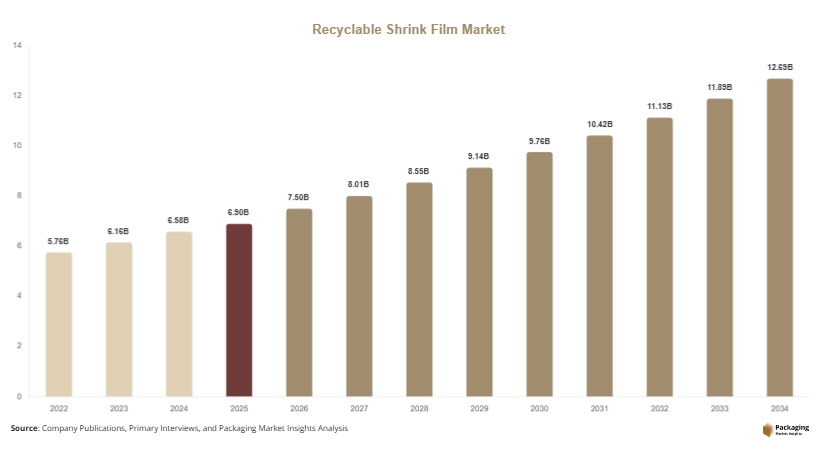

The global recyclable shrink film market size is estimated at USD 6.9 billion in 2025 and is projected to reach approximately USD 7.5 billion in 2026. Over the forecast period, the market is expected to expand significantly to USD 13.6 billion by 2034, registering a CAGR of 6.8% from 2025 to 2034. This growth reflects increasing demand for recyclable materials in packaging applications across food, beverage, consumer goods, and industrial sectors. The recyclable shrink film market is experiencing steady growth as industries transition toward sustainable packaging solutions that reduce environmental impact while maintaining performance efficiency.

One of the primary growth factors driving the market is the rising implementation of sustainability regulations that restrict non-recyclable plastic usage. Governments and regulatory bodies across major regions are encouraging manufacturers to adopt recyclable shrink films as part of broader environmental strategies. Another key factor is the growing demand for lightweight and cost-efficient packaging, as shrink films provide excellent load stability and product protection while reducing material usage. Additionally, the expansion of the e-commerce and logistics sector is contributing to market growth, as shrink films are widely used for bundling and securing products during transportation.

Key Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.1%.

- Polyethylene-based films led the type segment with a 34.2% share, while polyolefin films are expected to grow at a CAGR of 7.3%.

- Flexible packaging dominated the product segment with a 49.1% share, while industrial bundling films are forecasted to grow at a CAGR of 6.9%.

- Food & beverage applications led the segment with 44.8% share, while healthcare packaging is expected to grow at a CAGR of 7.0%.

- China remained the dominant country with a market size of USD 1.9 billion in 2025 and USD 2.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing shift toward mono-material recyclable shrink film solutions

The recyclable shrink film market is witnessing a strong shift toward mono-material structures that enhance recyclability and simplify waste management processes. Traditional multi-layer films often pose recycling challenges due to material incompatibility. Manufacturers are now focusing on developing mono-material polyethylene and polyolefin films that can be easily processed within existing recycling streams. This trend is gaining traction among consumer goods companies seeking to meet sustainability targets. Improved film clarity, strength, and shrink performance are enabling mono-material films to replace conventional options without compromising functionality. As a result, mono-material recyclable shrink films are becoming a key focus area for innovation and product development.

Increasing demand for sustainable packaging in retail and e-commerce

The rapid expansion of retail and e-commerce sectors is driving demand for sustainable packaging solutions, including recyclable shrink films. Retailers and online platforms are increasingly adopting eco-friendly packaging to reduce their environmental footprint and align with consumer expectations. Recyclable shrink films are widely used for bundling products, ensuring stability during transportation while minimizing material usage. The demand is particularly strong in the packaging of beverages, multipacks, and consumer goods. Additionally, brands are leveraging sustainable packaging as a differentiation strategy, which further accelerates the adoption of recyclable shrink films across retail channels.

Market Drivers

Rising regulatory pressure on non-recyclable plastic packaging

The implementation of strict regulations aimed at reducing plastic waste is a major driver for the recyclable shrink film market. Governments across regions are introducing policies that restrict the use of non-recyclable materials and encourage the adoption of sustainable alternatives. Recyclable shrink films offer a viable solution by meeting regulatory requirements while maintaining packaging performance. Companies are investing in research and development to produce films that comply with recycling standards. This regulatory push is accelerating the transition toward recyclable packaging solutions, driving market growth.

Expansion of the food and beverage packaging industry

The growth of the food and beverage industry is significantly contributing to the demand for recyclable shrink films. These films are widely used for packaging beverages, snacks, and other food products due to their ability to provide protection, visibility, and extended shelf life. The increasing demand for packaged food products, driven by urbanization and changing consumer lifestyles, is supporting market expansion. Additionally, the use of shrink films for multipack packaging enhances efficiency and reduces material usage, making them a preferred choice among manufacturers.

Market Restraint

Limited recycling infrastructure in developing regions

Despite the advantages of recyclable shrink films, the lack of adequate recycling infrastructure in many developing regions poses a significant challenge. While these films are designed to be recyclable, their effectiveness depends on the availability of collection, sorting, and recycling facilities. In regions where such infrastructure is limited, recyclable materials may still end up in landfills. This limitation reduces the overall environmental benefits and may discourage adoption. For example, in certain emerging markets, the absence of organized waste management systems can hinder the effective recycling of shrink films. Addressing this issue requires investment in infrastructure and increased awareness about recycling practices.

Market Opportunities

Advancements in high-performance recyclable film technologies

Technological advancements in polymer processing are creating new opportunities in the recyclable shrink film market. Manufacturers are developing high-performance films that combine recyclability with enhanced mechanical properties, such as tensile strength and shrink consistency. These innovations are enabling recyclable films to compete with traditional packaging materials in terms of performance. The development of advanced coatings and additives is also improving barrier properties, making these films suitable for a wider range of applications. As technology continues to evolve, the adoption of high-performance recyclable films is expected to increase.

Increasing adoption of circular economy practices by global brands

The growing emphasis on circular economy principles is creating significant opportunities for the market. Companies are focusing on designing packaging solutions that can be reused, recycled, or repurposed. Recyclable shrink films align with these goals by supporting material recovery and reducing waste. Global brands are committing to sustainability targets, such as using a higher percentage of recyclable materials in packaging. This shift is driving demand for recyclable shrink films across various industries. As businesses continue to prioritize sustainability, the market is expected to benefit from increased adoption of circular packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.9 Billion |

| Market Size in 2026 | USD 7.5 Billion |

| Market Size in 2034 | USD 13.6 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Polyethylene-based shrink films dominated the recyclable shrink film market in 2024, accounting for approximately 34.2% of the total share. These films are widely used due to their flexibility, durability, and cost-effectiveness. Polyethylene offers excellent shrink properties and is compatible with existing recycling streams, making it a preferred choice among manufacturers. Its ability to provide clarity and strength makes it suitable for packaging applications in food, beverages, and consumer goods. The widespread availability of polyethylene further supports its dominance in the market.

Polyolefin-based shrink films are expected to grow at the fastest CAGR of 7.3% during the forecast period. These films offer superior clarity, strength, and shrink performance compared to traditional materials. Polyolefin films are also recyclable and can be used in various applications, including retail packaging and industrial bundling. The increasing demand for high-performance packaging solutions is driving the growth of this segment.

By Product Type

Flexible shrink films accounted for the largest market share in 2024, representing 49.1% of the total market. These films are widely used due to their versatility and ease of application. Flexible shrink films are suitable for packaging a wide range of products, including food items, beverages, and consumer goods. Their lightweight nature and cost efficiency make them a preferred choice among manufacturers.

Industrial bundling films are expected to grow at the fastest CAGR of 6.9%. These films are used for securing and stabilizing products during transportation and storage. The increasing demand for efficient logistics and supply chain solutions is driving the growth of this segment.

By Application

The food and beverage segment dominated the market in 2024, accounting for 44.8% of the total share. The increasing demand for packaged food products is a key factor driving this segment. Recyclable shrink films are widely used for packaging beverages, snacks, and other food items due to their protective properties and ability to enhance product visibility.

Healthcare packaging is expected to grow at the fastest CAGR of 7.0%. The increasing demand for safe and hygienic packaging solutions in the healthcare sector is driving growth. Recyclable shrink films are used for packaging medical products, ensuring product safety and reducing environmental impact.

Recyclable Shrink Film Market Segmentations

By Material Type

- Polyethylene

- Polyolefin

- Polypropylene

By Product Type

- Flexible Shrink Films

- Industrial Bundling Films

- Specialty Shrink Films

By Application

- Food & Beverage

- Healthcare

- Consumer Goods

- Industrial

Regional Analysis

North America

North America accounted for approximately 24.2% of the recyclable shrink film market in 2025 and is expected to grow at a CAGR of 6.3% during the forecast period. The region’s strong regulatory framework and increasing focus on sustainability are key factors driving market growth. The demand for recyclable packaging solutions is particularly high in the food and beverage and consumer goods sectors.

The United States dominates the regional market due to its large consumer base and advanced packaging industry. A unique growth factor is the increasing adoption of corporate sustainability commitments, which encourage companies to use recyclable materials in packaging. This trend is expected to support market expansion in the region.

Europe

Europe held a market share of around 22.5% in 2025 and is projected to grow at a CAGR of 6.5%. The region’s strict environmental regulations and focus on circular economy practices are driving the adoption of recyclable shrink films. The demand is particularly strong in the retail and food packaging sectors.

Germany leads the European market due to its advanced manufacturing capabilities and strong emphasis on sustainability. A unique growth factor is the implementation of extended producer responsibility programs, which encourage manufacturers to adopt recyclable packaging solutions.

Asia Pacific

Asia Pacific dominated the recyclable shrink film market in 2025 with a 38.6% share and is expected to grow at a CAGR of 7.0%. Rapid industrialization, population growth, and increasing demand for packaged goods are key factors driving market growth. The expansion of the retail and e-commerce sectors further supports demand.

China is the dominant country in the region, benefiting from a large manufacturing base and growing consumer demand. A unique growth factor is the increasing investment in recycling infrastructure, which supports the adoption of recyclable packaging materials.

Middle East & Africa

The Middle East & Africa region accounted for 7.4% of the market share in 2025 and is expected to grow at a CAGR of 6.2%. The growing demand for sustainable packaging solutions and increasing awareness about environmental issues are driving market growth. Improvements in retail infrastructure are also supporting adoption.

Saudi Arabia is a key market in the region, driven by the expansion of the retail sector. A unique growth factor is the increasing focus on sustainability initiatives, which encourages the adoption of recyclable packaging solutions.

Latin America

Latin America held a market share of 7.3% in 2025 and is projected to grow at the fastest CAGR of 7.1%. The region’s growing middle class and increasing consumption of packaged goods are key drivers of market growth. The expansion of the food and beverage industry further supports demand.

Brazil dominates the regional market due to its large population and strong manufacturing sector. A unique growth factor is the increasing demand for cost-effective and sustainable packaging solutions, which drives the adoption of recyclable shrink films.

Competitive Landscape

The recyclable shrink film market is characterized by the presence of several global and regional players focusing on innovation, sustainability, and product differentiation. Leading companies include Amcor plc, Berry Global Inc., Sealed Air Corporation, Coveris Holdings S.A., and Intertape Polymer Group. Among these, Amcor plc is recognized as a market leader due to its strong global presence and continuous investment in sustainable packaging solutions.

Companies are focusing on developing recyclable and high-performance shrink films to meet regulatory requirements and consumer expectations. Strategic partnerships, mergers, and acquisitions are commonly used to expand market reach. Recent developments include the introduction of mono-material shrink films and expansion of production capacities to meet growing demand.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Coveris Holdings S.A.

- Intertape Polymer Group

- Dow Inc.

- LyondellBasell Industries

- Sigma Plastics Group

- RKW Group

- Polifilm GmbH

- Clondalkin Group

- Clysar LLC

- Bolloré Group

- Innovia Films

- Bemis Company Inc.