Recyclable Plastic Market Report Size and Growth

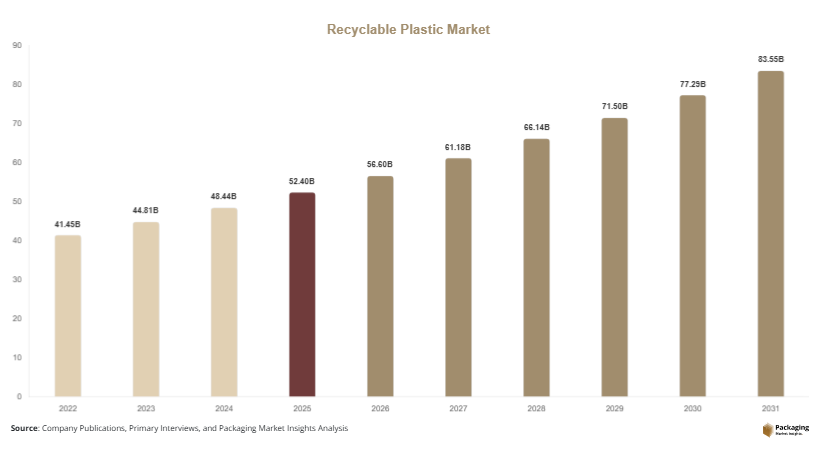

The Recyclable Plastic Market was valued at USD 52.4 billion in 2025 and is projected to reach USD 83.7 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2025–2031). The market has experienced notable expansion as governments, manufacturers, and consumers increasingly prioritize sustainable materials and circular economy practices. Recyclable plastics—including polyethylene terephthalate (PET), polyethylene (PE), polypropylene (PP), and polystyrene (PS)—are widely used across packaging, automotive, construction, electronics, and consumer goods industries.

A major global factor supporting market growth has been the implementation of regulatory policies promoting plastic recycling and waste management infrastructure. Governments across North America, Europe, and Asia Pacific have introduced recycling mandates, extended producer responsibility (EPR) frameworks, and landfill diversion targets, encouraging companies to incorporate recycled materials into product manufacturing. These policies have significantly increased investments in recycling technologies, sorting facilities, and chemical recycling processes.

In addition, rising consumer awareness regarding environmental sustainability has encouraged brand owners to adopt recyclable packaging solutions. Large multinational companies are setting targets to achieve 100% recyclable packaging in the coming years, which is expected to strengthen demand for recyclable plastics.

Key Highlights

- Asia Pacific dominated the Recyclable Plastic Market with a 41.3% share in 2025, while Latin America is projected to record the fastest CAGR of 9.4% during the forecast period.

- By material, PET accounted for the largest share of 32.8% in 2025, while polypropylene (PP) is expected to grow at a CAGR of 8.9%.

- By application, packaging represented the dominant segment with 46.5% share, whereas automotive applications are projected to grow at a CAGR of 8.7%.

- China led the global market, with the recyclable plastic market valued at USD 9.3 billion in 2025 and expected to reach USD 10.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growth of Circular Economy Initiatives

Circular economy strategies have emerged as a key trend shaping the Recyclable Plastic Market. Governments and private organizations are shifting from traditional linear consumption models toward systems that prioritize reuse, recycling, and resource efficiency. Many global brands have pledged to incorporate recycled plastic content into their packaging and products. Retail and consumer goods companies are also collaborating with recycling technology providers to ensure a stable supply of recycled polymers. These initiatives are encouraging large-scale investments in recycling infrastructure, including automated sorting technologies and advanced polymer recovery systems.

Expansion of Chemical Recycling Technologies

Chemical recycling technologies are increasingly gaining traction as they enable the recycling of complex and contaminated plastic waste streams that are difficult to process through conventional mechanical recycling. Technologies such as pyrolysis, depolymerization, and solvent-based recycling can convert plastic waste into raw materials or monomers suitable for new plastic production. As companies continue to scale these technologies, they are expected to enhance recycling efficiency and improve the quality of recycled plastics. The expansion of chemical recycling capacity is anticipated to significantly influence the growth outlook of the Recyclable Plastic Market in the coming years.

Market Drivers

Government Regulations Supporting Plastic Recycling

One of the primary drivers of the Recyclable Plastic Market is the introduction of regulatory policies aimed at reducing plastic waste and promoting recycling. Governments across multiple regions have implemented strict waste management regulations, plastic taxes, and recycling targets for manufacturers and municipalities. Extended producer responsibility policies require companies to manage the lifecycle of their products, including collection and recycling processes. These regulations encourage businesses to adopt recyclable materials and invest in recycling infrastructure, contributing to market growth.

Rising Demand for Sustainable Packaging Solution

The growing demand for sustainable packaging solutions has significantly boosted the adoption of recyclable plastics. Packaging manufacturers are increasingly shifting toward recyclable materials in response to consumer demand for environmentally responsible products. Industries such as food and beverage, personal care, and pharmaceuticals are transitioning toward recyclable plastic packaging to meet sustainability commitments. In addition, retailers and e-commerce companies are adopting recyclable plastic packaging to reduce environmental impact, which is expected to strengthen the growth trajectory of the Recyclable Plastic Market.

Market Restraint

Limited Recycling Infrastructure in Developing Economies

Despite steady growth, the Recyclable Plastic Market faces challenges related to insufficient recycling infrastructure in several developing economies. Many countries lack advanced waste collection systems, sorting technologies, and recycling facilities necessary for efficient plastic recycling. As a result, a large portion of recyclable plastic waste continues to be disposed of in landfills or incinerated.

In addition, the cost of collecting, sorting, and processing plastic waste can be relatively high compared with producing virgin plastic materials. Fluctuating oil prices also influence the competitiveness of recycled plastics. When virgin plastic becomes cheaper, manufacturers may reduce the use of recycled materials, affecting demand.

Another issue involves contamination in plastic waste streams. Improper waste segregation can reduce the quality of recycled plastics and limit their usability in certain applications, particularly food-grade packaging. These factors collectively restrict the growth potential of the Recyclable Plastic Market, particularly in regions where recycling infrastructure and waste management policies are still evolving.

Market Opportunities

Advancements in Recycling Technologies

Technological advancements in recycling processes are expected to create significant opportunities within the Recyclable Plastic Market. Innovations such as AI-powered sorting systems, improved polymer separation technologies, and enhanced recycling processes are increasing the efficiency and quality of recycled plastics. These technologies enable recyclers to process complex plastic waste streams and recover higher-value materials, which can be reused in various industrial applications.

Rising Investments in Recycling Infrastructure

Increasing investments in recycling infrastructure present another major opportunity for market expansion. Governments, private investors, and multinational corporations are investing in recycling facilities, waste management systems, and material recovery plants. Many companies are forming partnerships to expand recycling capacity and ensure a reliable supply of recycled plastic materials. Such investments are expected to strengthen supply chains, reduce reliance on virgin plastic production, and support the long-term growth of the Recyclable Plastic Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 52.4 Billion |

| Market Size in 2026 | USD 56.6 Billion |

| Market Size in 2031 | USD 83.7 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polyethylene Terephthalate (PET)

PET accounted for the largest share of 32.8% in 2024 within the Recyclable Plastic Market. PET is widely used in beverage bottles, food containers, and packaging films due to its durability, lightweight properties, and recyclability. The widespread adoption of PET recycling programs across multiple regions contributed to its dominant position. Additionally, the growing demand for recycled PET in the packaging industry supported segment growth.

Polypropylene (PP)

Polypropylene is expected to grow at a CAGR of 8.9% during the forecast period. The segment will expand as industries increasingly adopt recycled PP in automotive components, packaging products, and consumer goods. The growing use of recycled polypropylene in lightweight automotive applications will serve as a key growth factor for this segment.

By Application

Packaging

Packaging represented the largest share of 46.5% in 2024. The widespread use of recyclable plastics in food and beverage packaging, consumer goods packaging, and e-commerce packaging contributed to segment dominance. Companies across industries increasingly adopted recyclable plastic packaging solutions to meet sustainability targets and regulatory requirements.

Automotive

The automotive segment is expected to grow at a CAGR of 8.7% during the forecast period. Automotive manufacturers will increasingly use recycled plastics to reduce vehicle weight and improve sustainability. The integration of recyclable plastic materials in vehicle interiors and components will support the expansion of this segment.

By End-Use Industry

Consumer Goods

The consumer goods segment accounted for 38.2% share in 2024 within the Recyclable Plastic Market. The segment’s growth was supported by the widespread use of recyclable plastics in packaging, household products, and electronics components.

Construction

The construction industry is projected to grow at a CAGR of 8.5% during the forecast period. Recyclable plastics will be increasingly used in pipes, insulation materials, and construction components due to their durability and environmental benefits.

Recyclable Plastic Market Segmentations

By Material

- Polyethylene Terephthalate (PET)

- Polyethylene (PE)

- Polypropylene (PP)

- Polystyrene (PS)

- Others

By Application

- Packaging

- Automotive

- Construction

- Electronics

- Consumer Goods

By End-Use Industry

- Consumer Goods

- Construction

- Automotive

- Packaging

- Electronics

Regional Analysis

North America

North America accounted for 21.4% of the global Recyclable Plastic Market share in 2025. The region benefited from established recycling infrastructure, strong regulatory frameworks, and growing consumer awareness regarding environmental sustainability. The market in North America is expected to grow at a CAGR of 7.6% during the forecast period (2025–2033). Increasing corporate commitments to sustainable packaging and rising investments in recycling facilities are anticipated to support regional market expansion.

The United States dominated the regional market due to its large packaging industry and growing investments in recycling technologies. Several major consumer goods companies have introduced sustainability goals aimed at increasing the use of recycled plastic in packaging. Additionally, collaborations between municipalities and recycling companies have improved waste collection and sorting systems, supporting market growth.

Europe

Europe represented 27.8% of the global Recyclable Plastic Market in 2025. The region’s strong policy framework for plastic waste reduction and recycling initiatives significantly supported market development. The regional market will expand at a CAGR of 7.8% during the forecast period as governments continue to enforce recycling targets and circular economy policies.

Germany emerged as the leading country in the European market, supported by advanced waste management systems and high recycling rates. The country’s deposit return schemes and plastic recycling regulations have encouraged efficient collection and recycling processes. These factors have enabled Germany to maintain a steady supply of recyclable plastic materials for industrial applications.

Asia Pacific

Asia Pacific held the largest share of 41.3% in the Recyclable Plastic Market in 2025. Rapid industrialization, expanding manufacturing sectors, and growing plastic consumption contributed to the region’s market dominance. The regional market is projected to grow at a CAGR of 8.6% during the forecast period.

China led the Asia Pacific market, supported by its large-scale plastic production and recycling industry. The country’s policies aimed at reducing plastic waste and promoting recycling have accelerated investments in recycling facilities and advanced plastic processing technologies. These initiatives have strengthened China’s position as a major hub for recyclable plastic processing and production.

Middle East & Africa

The Middle East & Africa accounted for 5.9% of the global Recyclable Plastic Market share in 2025. The regional market is still developing but is expected to experience steady growth due to increasing awareness regarding environmental sustainability. The market is projected to grow at a CAGR of 7.2% through 2033.

The United Arab Emirates emerged as a key country in the region, driven by government initiatives aimed at reducing plastic waste and promoting recycling practices. Investments in waste management infrastructure and recycling facilities have improved plastic waste processing capabilities in the country.

Latin America

Latin America held 3.6% of the global Recyclable Plastic Market share in 2025. Growing environmental awareness and expanding recycling initiatives supported market development in the region. The market is forecast to grow at a CAGR of 9.4% through 2033, making it the fastest-growing region.

Brazil dominated the Latin American market, supported by the presence of a large packaging industry and expanding recycling initiatives. The country’s recycling programs and partnerships between waste management companies and packaging manufacturers have improved recycling rates, contributing to market growth.

Competitive Landscape

The Recyclable Plastic Market features the presence of global chemical manufacturers, recycling companies, and packaging material providers. Market participants focus on expanding recycling capacity, developing advanced recycling technologies, and forming strategic partnerships to strengthen their market positions.

Veolia Environment S.A. emerged as a leading player in the global market due to its extensive recycling infrastructure and waste management capabilities. The company has recently expanded its plastic recycling operations in Europe to increase the production of recycled polymers for packaging applications.

Other companies are investing in advanced recycling technologies and forming partnerships with packaging manufacturers to ensure a stable supply of recycled plastic materials. These strategies are expected to enhance competitive dynamics in the global market.

Key Players in the Recyclable Plastic Market

- Veolia Environment S.A.

- Waste Management Inc.

- Republic Services Inc.

- SUEZ Group

- Biffa plc

- Plastipak Holdings Inc.

- Loop Industries Inc.

- Indorama Ventures Public Company Limited

- KW Plastics

- MBA Polymers Inc.

- Jayplas Ltd

- DS Smith plc

- Berry Global Inc.

- LyondellBasell Industries

- BASF SE