Ready To Drink Packaging Market Size and Growth

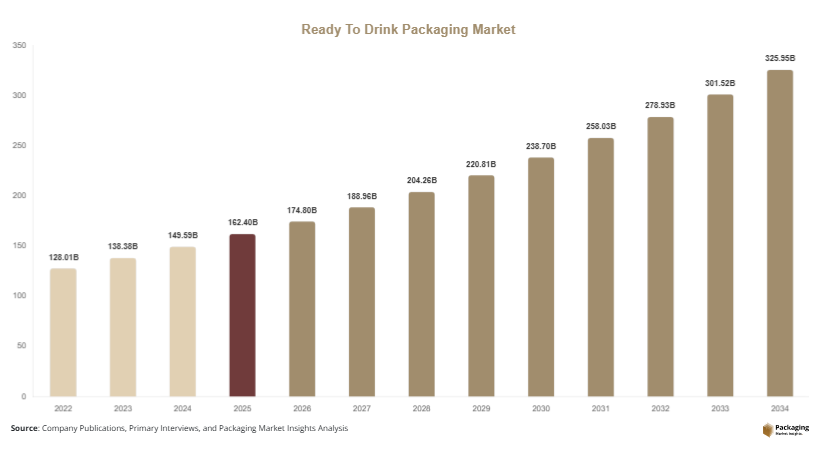

The global ready to drink packaging market size was estimated at USD 162.4 billion in 2025 and is projected to reach USD 174.8 billion in 2026. Over the forecast period, the market is expected to grow steadily and reach USD 326.9 billion by 2034, registering a compound annual growth rate (CAGR) of 8.1% from 2025 to 2034. Growth is driven by rising demand for portable beverage formats, expansion of e-commerce beverage distribution, and the increasing use of sustainable packaging materials across the beverage industry.

The ready to drink packaging market has experienced steady growth as beverage manufacturers expand their product portfolios to meet evolving consumer preferences for convenience and portability. Ready-to-drink (RTD) beverages include coffee, tea, energy drinks, flavored water, dairy beverages, and alcoholic ready mixes that require packaging solutions capable of maintaining freshness, extending shelf life, and supporting efficient distribution. As beverage consumption patterns shift toward on-the-go formats, packaging innovation has become a critical competitive factor for producers and distributors.

Key Highlights

- Market size reached USD 162.4 billion in 2025

- Expected to grow at 8.1% CAGR from 2025–2034

- Forecast market value projected to reach USD 326.9 billion by 2034

- Increasing demand for convenient beverage formats supports packaging innovation

- Sustainability initiatives are shaping material selection and design strategies

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Recyclable Packaging

Sustainability has become a central trend influencing the ready to drink packaging market. Beverage manufacturers and packaging suppliers are transitioning toward recyclable, biodegradable, and lightweight materials to reduce environmental impact. Governments in several regions are introducing regulations that encourage the use of recyclable plastics, aluminum cans, and paper-based cartons. These policies have encouraged companies to redesign packaging formats that minimize waste and improve material recovery.

In addition, consumers increasingly prefer beverages packaged in environmentally responsible containers. This shift has accelerated the adoption of recycled PET bottles, aluminum cans with higher recycled content, and fiber-based cartons. Packaging producers are also exploring plant-based plastics and compostable materials that maintain product safety while reducing carbon emissions. As beverage companies adopt sustainability targets, the use of eco-friendly packaging solutions is expected to expand significantly across RTD beverage categories.

Growth of Smart and Innovative Packaging Technologies

Technological innovation is transforming the ready to drink packaging market as manufacturers introduce intelligent packaging features that enhance product safety and consumer engagement. Smart labels, QR codes, and digital printing technologies allow brands to provide traceability, authenticity verification, and interactive marketing experiences.

Advanced packaging solutions also improve shelf life and product protection. For example, oxygen barrier layers and aseptic filling technologies help maintain beverage freshness for extended periods. These innovations are particularly valuable for ready-to-drink coffee, dairy beverages, and functional drinks that contain sensitive ingredients. As beverage companies compete to differentiate their products on retail shelves, packaging design and technology are expected to play an increasingly strategic role.

Market Drivers

Rising Demand for On-the-Go Beverage Consumption

The increasing preference for convenient consumption formats is a major driver of the ready to drink packaging market. Urbanization, busy work schedules, and mobile lifestyles have led consumers to choose beverages that require minimal preparation. Ready-to-drink products such as iced coffee, bottled tea, flavored water, and energy drinks have gained strong popularity across retail and convenience channels.

Packaging solutions that support portability, durability, and ease of use have therefore become essential. Lightweight bottles, resealable cans, and compact cartons allow consumers to consume beverages while commuting or traveling. In addition, the growth of convenience stores and vending machine distribution has increased demand for packaging formats designed for quick retail access. As convenience continues to influence purchasing decisions, demand for RTD packaging is expected to rise across both developed and emerging markets.

Expansion of the Global Beverage Industry

The rapid growth of the global beverage industry is another significant driver supporting the ready to drink packaging market. Beverage companies are continuously launching new ready-to-drink products across multiple categories, including plant-based drinks, sports beverages, and functional nutrition drinks.

These product launches require specialized packaging solutions that preserve flavor, nutrients, and product integrity. In addition, brand differentiation is increasingly dependent on packaging design, which drives investment in innovative materials, shapes, and labeling technologies. As beverage brands compete to capture consumer attention and expand distribution networks, packaging suppliers benefit from increased production volumes and new design opportunities.

Market Restraint

Environmental Concerns and Regulatory Pressure on Plastic Packaging

Environmental concerns surrounding plastic waste represent a key restraint for the ready to drink packaging market. Plastic packaging has historically been widely used in the beverage industry because of its durability, lightweight structure, and cost efficiency. However, rising awareness about plastic pollution has led to stricter regulations and increasing pressure on manufacturers to adopt sustainable alternatives.

Governments across North America, Europe, and Asia have implemented policies that restrict single-use plastics and promote recycling targets. These regulations often require beverage producers to invest in new packaging materials, recycling systems, and supply chain modifications. Such transitions can increase operational costs and create challenges for smaller beverage companies that rely on traditional plastic packaging.

For example, regulatory mandates encouraging recycled content in beverage bottles require packaging manufacturers to secure stable supplies of recycled PET materials. Limited recycling infrastructure in some regions may restrict material availability, leading to cost fluctuations. While sustainable packaging innovations are progressing, the transition away from conventional plastics remains a complex process that may temporarily slow market expansion in certain regions.

Market Opportunities

Growth of Functional and Health-Focused Beverages

The rapid expansion of functional beverages presents a significant opportunity for the ready to drink packaging market. Consumers increasingly seek beverages that offer health benefits such as energy support, hydration, immune enhancement, and protein supplementation. Ready-to-drink protein shakes, probiotic drinks, and vitamin-infused beverages have gained traction across retail channels.

These beverages often require advanced packaging technologies that protect sensitive ingredients and extend shelf life. For example, aseptic cartons and multi-layer bottles help maintain nutritional integrity while preventing contamination. As the global wellness trend continues to influence beverage consumption, demand for specialized RTD packaging solutions designed for functional drinks is expected to increase steadily.

Expansion of E-Commerce Beverage Distribution

The rapid growth of online retail has created new opportunities for the ready to drink packaging market. Beverage companies are increasingly distributing ready-to-drink products through e-commerce platforms and direct-to-consumer channels. This shift requires packaging solutions that are durable, lightweight, and optimized for shipping logistics.

Packaging formats designed for e-commerce must protect products from leakage, temperature fluctuations, and transportation damage. As a result, beverage brands are investing in improved packaging structures and protective designs that ensure safe delivery. The continued expansion of digital retail channels is expected to create long-term demand for innovative packaging solutions tailored to online distribution.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 162.4 Billion |

| Market Size in 2026 | USD 174.8 Billion |

| Market Size in 2034 | USD 326.9 Billion |

| CAGR | 8.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

The bottles segment held the dominant position in the ready to drink packaging market, accounting for approximately 42% of global revenue in 2024. Bottles remain widely used for packaging ready-to-drink beverages such as flavored water, juices, iced tea, and sports drinks. PET bottles are particularly popular due to their lightweight structure, cost efficiency, and ability to maintain beverage freshness. Manufacturers also prefer bottles because they can be produced in various shapes and sizes, allowing beverage brands to differentiate their products visually on retail shelves.

The cans segment is expected to record the fastest growth during the forecast period, with an estimated CAGR of around 9.1% through 2034. Aluminum cans are increasingly preferred for ready-to-drink coffee, energy drinks, and carbonated beverages due to their high recyclability and excellent barrier properties. Another growth factor is the growing popularity of slim cans that offer convenient portability and modern branding appeal. Beverage companies are also adopting cans for premium beverage lines because the format supports vibrant printing and improved product protection.

By Material

The plastic packaging segment dominated the ready to drink packaging market in 2024 with a share of approximately 48%. Plastic materials such as PET and HDPE remain widely used because they are lightweight, durable, and relatively inexpensive compared with other packaging materials. These materials allow beverage companies to produce bottles in large volumes while maintaining transportation efficiency. Plastic packaging also supports resealable designs, which are preferred by consumers who consume beverages over multiple occasions.

The paperboard and carton segment is projected to grow at the fastest pace, with a CAGR of around 9.5% during the forecast period. Carton packaging is gaining traction due to its strong sustainability profile and increasing recyclability. Many beverage companies are adopting aseptic carton packaging for ready-to-drink coffee, dairy beverages, and plant-based drinks. A major growth factor is the ability of cartons to preserve beverages without refrigeration for extended periods, which supports distribution across emerging markets.

By Beverage Type

The non-alcoholic beverages segment accounted for the largest share of the ready to drink packaging market in 2024, representing nearly 71% of total revenue. This category includes ready-to-drink coffee, tea, energy drinks, juices, flavored water, and dairy beverages. High global consumption levels and continuous product innovation support the dominance of this segment. Beverage companies frequently launch new flavors and functional beverage options, which increases demand for diverse packaging formats and advanced preservation technologies.

The alcoholic ready-to-drink beverages segment is expected to witness the fastest growth, registering a CAGR of around 9.0% through 2034. Ready-to-drink cocktails, hard seltzers, and canned mixed drinks have gained strong popularity among younger consumers. These beverages often use stylish cans or glass bottles designed to enhance brand appeal. A key growth factor is the increasing availability of RTD alcoholic beverages in retail stores and entertainment venues, which supports rising packaging demand.

Ready To Drink Packaging Market Segmentations

Packaging Type

- Bottles

- Cans

- Cartons

- Pouches

Material

- Plastic

- Metal

- Glass

- Paperboard / Carton

Beverage Type

- Non-Alcoholic Beverages

- Alcoholic Ready-To-Drink Beverages

Regional Analysis

North America

North America held a significant share of the ready to drink packaging market in 2025, accounting for approximately 32% of global revenue, supported by strong consumption of ready-to-drink coffee, energy drinks, and flavored beverages. The region is projected to maintain stable growth with a CAGR of around 7.4% through 2034. High consumer demand for convenience beverages, combined with advanced beverage manufacturing infrastructure, supports continued packaging innovation across the region.

The United States represents the dominant market within North America. A key growth factor is the strong popularity of ready-to-drink coffee and functional beverages among young professionals and students. Beverage brands in the country frequently launch new RTD products with unique packaging formats such as slim aluminum cans and resealable bottles, which drives continuous demand for packaging manufacturing and design services.

Europe

Europe accounted for approximately 24% of the global ready to drink packaging market in 2025. The market in this region is expected to expand at a CAGR of 7.6% during the forecast period. Growth is influenced by strong consumption of ready-to-drink teas, flavored sparkling beverages, and dairy-based drinks. European beverage companies are also investing heavily in sustainable packaging technologies to comply with environmental regulations.

Germany remains the dominant market in Europe due to its well-developed beverage manufacturing industry and strong recycling infrastructure. A unique growth factor in the region is the widespread adoption of deposit return systems for beverage containers. These programs encourage consumers to return packaging materials for recycling, supporting circular economy initiatives and driving demand for recyclable packaging solutions.

Asia Pacific

Asia Pacific represented the largest regional share of around 34% in 2025, reflecting the region’s large population and rapidly expanding beverage industry. The ready to drink packaging market in Asia Pacific is projected to grow at a CAGR of approximately 9.3% through 2034, making it the fastest-growing regional market. Rising urbanization and increasing disposable income have significantly boosted demand for convenient beverage options.

China leads the Asia Pacific market due to its massive consumer base and rapidly growing ready-to-drink tea and coffee segments. One unique growth factor is the strong influence of convenience retail stores and automated beverage vending machines in urban areas. These distribution channels rely heavily on standardized packaging formats such as cans and PET bottles, increasing demand for packaging production.

Middle East & Africa

The Middle East & Africa accounted for around 5% of the global ready to drink packaging market in 2025. The region is forecast to expand at a CAGR of about 7.8% between 2025 and 2034. Demand for packaged beverages continues to increase as urban populations grow and retail infrastructure improves across major cities.

Saudi Arabia represents a leading market within the region. A unique growth factor is the rising popularity of ready-to-drink energy drinks and flavored beverages among younger consumers. Beverage companies operating in the country increasingly invest in modern packaging technologies to support product differentiation and maintain beverage quality in hot climate conditions.

Latin America

Latin America accounted for approximately 5% of the ready to drink packaging market in 2025 and is expected to expand at a CAGR of around 7.9% during the forecast period. The region’s beverage industry continues to grow as consumer preferences shift toward convenient beverage options that are easy to transport and consume.

Brazil dominates the Latin American market due to its large population and well-established beverage sector. A unique growth factor is the strong popularity of ready-to-drink fruit beverages and dairy drinks in the country. Beverage companies frequently introduce innovative packaging formats that maintain freshness and appeal to younger consumers, which supports packaging market growth.

Competitive Landscape

The ready to drink packaging market is moderately consolidated, with several global packaging companies competing through innovation, sustainability initiatives, and strategic partnerships with beverage manufacturers. Leading companies focus on expanding production capacity, developing recyclable packaging materials, and introducing advanced packaging technologies that improve shelf life and product safety.

Among the key participants, Ball Corporation is widely recognized as a leading provider of aluminum beverage cans and sustainable packaging solutions. The company has invested heavily in expanding its aluminum can production facilities to meet rising demand for ready-to-drink beverages worldwide.

Other prominent players such as Amcor, Crown Holdings, and Tetra Pak focus on developing lightweight and recyclable packaging formats to address environmental regulations and consumer preferences. In recent years, companies have increased research investments to introduce packaging materials with improved barrier properties and reduced carbon footprints.

Strategic collaborations between beverage manufacturers and packaging suppliers remain a key competitive strategy shaping market development.

Key Players List

- Amcor plc

- Ball Corporation

- Crown Holdings Inc.

- Tetra Pak International S.A.

- Ardagh Group S.A.

- Berry Global Group Inc.

- Mondi Group

- Smurfit Kappa Group

- Silgan Holdings Inc.

- WestRock Company

- AptarGroup Inc.

- Graham Packaging Company

- Krones AG

- Toyo Seikan Group Holdings Ltd.

- Can-Pack S.A.