Produce Packaging Market Size and Growth

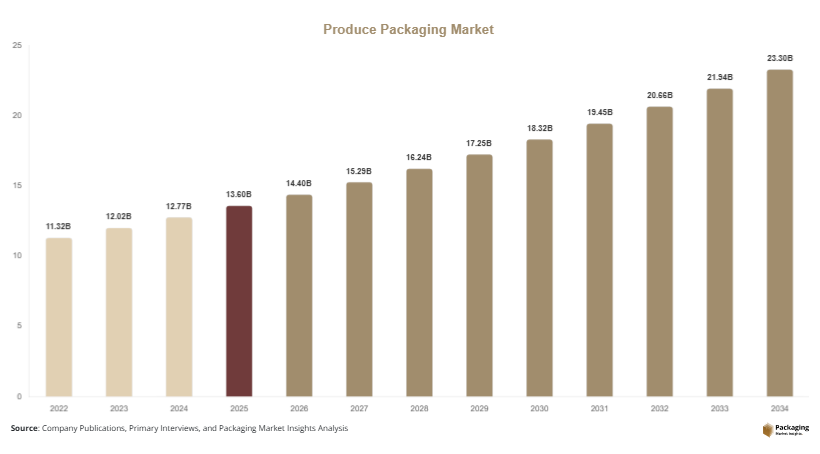

The global produce packaging market size is estimated at USD 13.6 billion in 2025, and it is projected to reach USD 14.4 billion in 2026. By 2034, the market is expected to attain approximately USD 23.9 billion, registering a CAGR of 6.2% during 2025–2034. Growth is being driven by rising consumption of fresh produce, expansion of organized retail, and the increasing need to reduce food wastage across global supply chains. The Global produce packaging market is witnessing steady expansion as global demand for fresh fruits and vegetables increases alongside the modernization of agricultural supply chains and retail distribution systems.

One of the major growth factors is the rapid expansion of organized food retail and supermarket chains. These retailers require advanced packaging solutions such as ventilated crates, clamshell containers, corrugated trays, and modified atmosphere packaging to maintain freshness and extend shelf life. Another key driver is the globalization of agricultural trade, where fruits and vegetables are transported across long distances, requiring durable, moisture-resistant, and temperature-stable packaging systems. Additionally, rising consumer preference for convenience foods and pre-packaged fresh produce is accelerating demand for innovative packaging formats.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Plastic crates led the type segment with a 30.8% share.

- Plastic-based packaging dominated with a 52.3% share.

- Retail & supermarket distribution led the segment with 43.7% share.

- The US remained the dominant country with a market size of USD 3.9 billion in 2025 and USD 4.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Compostable Packaging Solutions

A major trend in the produce packaging market is the growing shift toward sustainable and compostable packaging materials. Consumers and regulatory bodies are increasingly concerned about plastic waste generated from single-use packaging. As a result, manufacturers are adopting biodegradable films, molded fiber trays, and compostable clamshell containers. For example, supermarkets in Europe are replacing plastic fruit trays with pulp-based alternatives to meet environmental targets. This trend is also supported by government bans on non-recyclable plastics in several regions. Over the forecast period, sustainability-driven innovation is expected to reshape packaging material preferences across global produce supply chains.

Expansion of Smart Packaging and Traceability Technologies

Another significant trend is the integration of smart packaging technologies such as QR codes, freshness indicators, and IoT-based tracking systems. These technologies help monitor produce quality, temperature exposure, and shelf-life conditions throughout the supply chain. For instance, large grocery retailers in North America use smart labels on packaged salads and fruits to track freshness and reduce waste. This enhances consumer trust and improves inventory management. In the future, digital traceability solutions are expected to become standard in produce packaging, especially for export-oriented agricultural products.

Market Drivers

Growth in Global Fresh Produce Consumption

Rising global consumption of fruits and vegetables is a primary driver of the produce packaging market. Increasing awareness of healthy diets and nutrition has significantly boosted demand for fresh produce across both developed and emerging economies. This has led to higher requirements for protective packaging that preserves freshness during transportation and storage. For example, supermarkets in Asia Pacific are expanding their fresh produce sections, requiring large volumes of ventilated crates and protective packaging solutions. This growing consumption pattern directly increases demand for advanced packaging systems.

Expansion of Organized Retail and Export Agriculture

The expansion of organized retail chains and global agricultural exports is another key driver. Large retailers require standardized packaging systems to ensure consistent product quality and efficient logistics operations. Additionally, countries exporting fruits and vegetables need durable packaging to withstand long transit times. For example, Latin American countries exporting bananas and avocados use reinforced corrugated boxes and plastic crates to maintain quality during international shipping. This increasing reliance on structured supply chains is driving steady demand for produce packaging solutions.

Market Restraint

High Cost of Sustainable Packaging Materials

One of the major restraints in the produce packaging market is the relatively high cost of sustainable and advanced packaging materials. Biodegradable films, molded fiber packaging, and smart packaging systems are more expensive compared to conventional plastic alternatives. This creates challenges for small and medium-scale producers, particularly in developing economies. For example, small fruit exporters often rely on low-cost plastic crates due to budget constraints, even when sustainable options are available. Additionally, fluctuating raw material prices for paper and biopolymers further increase cost uncertainty, limiting widespread adoption of eco-friendly packaging solutions.

Market Opportunities

Rising Demand for E-commerce Grocery Delivery

The rapid growth of online grocery platforms presents a significant opportunity for the produce packaging market. E-commerce retailers require packaging solutions that maintain freshness during last-mile delivery while preventing damage during transit. This has led to increased demand for insulated boxes, ventilated crates, and tamper-proof packaging systems. For example, online grocery platforms in urban India and the United States are investing in specialized packaging to ensure fresh delivery of fruits and vegetables. This trend is expected to continue as digital grocery shopping expands globally.

Innovation in Reusable Packaging Systems

Reusable packaging systems are creating new growth opportunities in the market. Plastic crates, foldable containers, and returnable transport packaging systems are increasingly being adopted across supply chains to reduce waste and logistics costs. For example, large retail chains in Europe use standardized reusable crates that circulate between farms, distribution centers, and stores. This reduces dependency on single-use packaging and improves operational efficiency. As sustainability becomes a key priority, reusable packaging systems are expected to gain further traction across global agricultural supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 13.6 Billion |

| Market Size in 2026 | USD 14.4 Billion |

| Market Size in 2034 | USD 23.9 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic crates dominated the market in 2024 with a 31.2% share due to their durability, reusability, and ventilation properties. These crates are widely used in agricultural supply chains for transporting fruits and vegetables from farms to retail outlets. Their ability to reduce spoilage and withstand stacking during transportation makes them highly preferred in bulk logistics systems. For example, banana and apple supply chains rely heavily on plastic crates for export operations.

Biodegradable packaging is the fastest-growing subsegment with a CAGR of 6.9%. This growth is driven by increasing environmental regulations and consumer preference for sustainable packaging. Molded pulp trays and compostable films are gaining traction across supermarkets and food delivery platforms. Future adoption is expected to increase significantly as governments enforce stricter plastic reduction policies.

By Material

Plastic-based packaging dominated with a 52.1% share in 2024 due to its cost efficiency and versatility. It is widely used for crates, trays, and wraps in agricultural logistics.

Paper-based packaging is the fastest-growing segment with a CAGR of 5.9%, driven by sustainability trends and increasing adoption in supermarkets. Corrugated trays and fiber-based containers are gaining popularity in retail applications.

By End-Use

Retail & supermarkets dominated the market in 2024 with a 44.3% share due to high demand for packaged fresh produce. Large retail chains require standardized packaging for display and transportation.

E-commerce grocery delivery is the fastest-growing segment with a CAGR of 6.4%, driven by increasing online food purchases and demand for doorstep delivery of fresh fruits and vegetables.

Produce Packaging Market Segmentations

By Product Type

- Plastic Crates

- Corrugated Boxes

- Wooden Crates

- Biodegradable Packaging

By Material

- Plastic Packaging

- Paper-Based Packaging

- Wood-Based Packaging

- Hybrid Materials

By End-Use

- Retail & Supermarkets

- Food Service Industry

- E-commerce Grocery Delivery

- Export Agriculture

Regional Analysis

North America

North America accounted for approximately 28.3% of the market share in 2025 and is projected to grow at a CAGR of 5.8%. The region benefits from advanced cold chain infrastructure and strong demand for fresh produce in supermarkets and food service industries. Growth is supported by increasing adoption of sustainable packaging materials and automation in food distribution systems.

The United States dominates the region due to its large retail grocery sector. A key growth driver is the expansion of organic food consumption, which requires specialized breathable and protective packaging solutions to maintain product quality during distribution.

Europe

Europe held a 24.6% share in 2025 and is expected to grow at a CAGR of 5.7%. The region is heavily influenced by environmental regulations promoting recyclable and compostable packaging materials. Retailers are actively replacing plastic packaging with fiber-based alternatives.

Germany leads the European market due to its strong retail infrastructure. A key driver is the implementation of strict packaging waste reduction laws, encouraging adoption of biodegradable fruit and vegetable packaging solutions across supermarkets.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is projected to grow at a CAGR of 6.8%. Rapid urbanization, rising disposable income, and expanding supermarket chains are key growth factors. The region also benefits from large-scale agricultural production and export activities.

China is the dominant country due to its massive agricultural output. A key driver is the expansion of cold chain logistics networks, which support long-distance transportation of fresh produce across domestic and international markets.

Middle East & Africa

The region accounted for 5.1% of the market in 2025 and is projected to grow at a CAGR of 6.1%. Growth is driven by increasing import of fresh fruits and vegetables and rising investment in retail infrastructure.

The UAE leads the region due to its strong import-dependent food supply chain. A key driver is the growth of luxury retail supermarkets requiring premium packaging solutions for imported fresh produce.

Latin America

Latin America held a 4.6% share in 2025 and is expected to grow at the fastest CAGR of 7.0%. The region benefits from strong agricultural exports and expanding trade relationships with North America and Europe.

Brazil dominates the region due to its large fruit export industry. A key driver is the increasing demand for durable export packaging for bananas, mangoes, and avocados shipped to global markets.

Competitive Landscape

The produce packaging market is moderately competitive, with key players focusing on sustainability, material innovation, and supply chain efficiency. Amcor plc is a leading player due to its strong portfolio of flexible and sustainable packaging solutions. The company continues to invest in recyclable and compostable packaging technologies.

Other major players include Sealed Air Corporation, Smurfit Kappa, Mondi Group, and DS Smith. These companies are focusing on expanding eco-friendly product lines and improving packaging durability. Strategic collaborations with retail chains and agricultural exporters are also shaping competitive dynamics.

Key Players List

- Amcor plc

- Sealed Air Corporation

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- WestRock Company

- International Paper Company

- Packaging Corporation of America

- Sonoco Products Company

- Rengo Co. Ltd.

- Oji Holdings Corporation

- Huhtamaki Oyj

- Uflex Ltd.

- Placon Corporation

- Pactiv Evergreen Inc.