Primary Packaging Labels Market Size and Growth

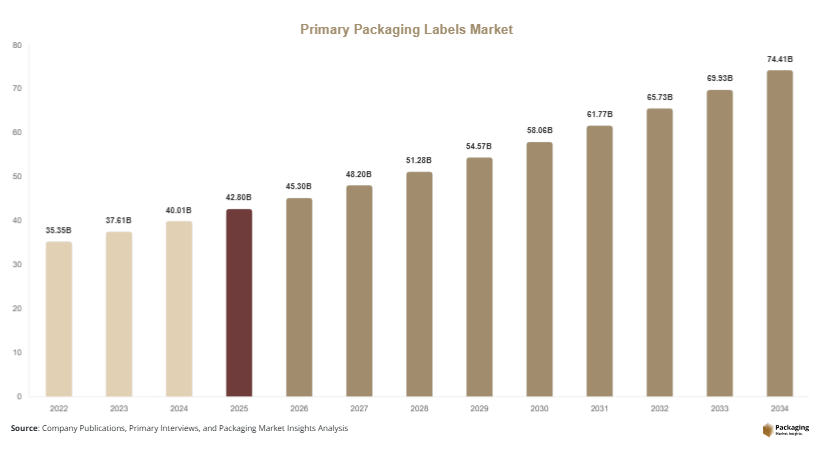

The global primary packaging labels market size was valued at approximately USD 42.8 billion in 2025 and is projected to reach USD 45.3 billion in 2026. With growing adoption of advanced labeling technologies and expanding end-use industries, the market is expected to reach USD 74.6 billion by 2034, registering a CAGR of 6.4% during the forecast period (2025–2034). Labels serve as a critical component of primary packaging, providing essential product information while enhancing shelf appeal and consumer engagement. The primary packaging labels market is witnessing steady growth driven by increasing demand for product identification, branding, and regulatory compliance across industries such as food & beverage, pharmaceuticals, and personal care.

One of the key growth factors is the rapid expansion of the global food and beverage sector, which relies heavily on labeling for branding, nutritional information, and traceability. Another major factor is the increasing regulatory requirements for product labeling, particularly in pharmaceuticals and chemicals, where compliance with safety standards is essential. In addition, the rising demand for sustainable and eco-friendly labeling materials is driving innovation in the market, with manufacturers focusing on recyclable and biodegradable label solutions.

Key Highlights:

Asia Pacific dominated the market with a 37.6% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.7%.

Pressure-sensitive labels led the type segment with a 41.8% share, while shrink sleeve labels are expected to grow at a CAGR of 6.9%.

Plastic-based labels dominated with a 53.1% share, while paper-based labels are forecasted to grow at a CAGR of 6.2%.

Food & beverage applications led the segment with 46.5% share, while pharmaceutical labeling is expected to grow at a CAGR of 6.8%.

China remained the dominant country with a market size of USD 9.6 billion in 2025 and USD 10.2 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of smart and interactive labeling solutions

The primary packaging labels market is experiencing a shift toward smart and interactive labeling solutions that enhance consumer engagement and supply chain transparency. Technologies such as QR codes, NFC tags, and RFID-enabled labels are being integrated into packaging to provide detailed product information, authentication, and traceability. These smart labels enable brands to connect directly with consumers through digital platforms, offering features such as product origin details, usage instructions, and promotional content. This trend is particularly prominent in the food and pharmaceutical sectors, where traceability and authenticity are critical. As companies continue to invest in digital transformation, the adoption of smart labeling solutions is expected to increase significantly.

Growing demand for sustainable labeling materials

Another important trend is the rising demand for sustainable and eco-friendly labeling materials. With increasing environmental awareness and regulatory pressure, companies are focusing on reducing their environmental footprint by adopting recyclable, biodegradable, and compostable label materials. Paper-based labels and water-based adhesives are gaining popularity as alternatives to traditional plastic-based labels. Manufacturers are also exploring innovative solutions such as linerless labels and recyclable films to minimize waste. This trend is supported by consumer preferences for environmentally responsible products and is driving continuous innovation in label design and production processes.

Market Drivers

Expansion of the food and beverage industry

The rapid growth of the global food and beverage industry is a major driver for the primary packaging labels market. Increasing demand for packaged and processed foods is boosting the need for effective labeling solutions that provide product information, branding, and compliance with regulatory standards. Labels play a crucial role in enhancing product visibility and influencing consumer purchasing decisions. The rise of convenience foods and ready-to-eat products is further increasing the demand for high-quality labels. Additionally, the expansion of retail channels, including supermarkets and online platforms, is contributing to market growth by increasing the need for visually appealing and durable labeling solutions.

Stringent regulatory requirements for labeling

The implementation of strict regulations regarding product labeling is another key factor driving market growth. Governments and regulatory bodies require detailed labeling for products, particularly in industries such as pharmaceuticals, chemicals, and food. These regulations ensure consumer safety by providing essential information such as ingredients, usage instructions, and safety warnings. Compliance with these requirements necessitates the use of high-quality labeling solutions. As regulations continue to evolve, manufacturers are investing in advanced labeling technologies to meet compliance standards and avoid penalties. This regulatory environment is encouraging innovation and driving demand for primary packaging labels.

Market Restraint

Fluctuating raw material prices and environmental concerns

The primary packaging labels market faces challenges due to fluctuations in raw material prices and environmental concerns associated with certain label materials. The cost of raw materials such as plastics, adhesives, and inks can vary significantly, affecting production costs and profit margins. Additionally, increasing scrutiny on plastic-based labels due to environmental impact is creating pressure on manufacturers to adopt sustainable alternatives. Transitioning to eco-friendly materials often involves higher costs and technical challenges, particularly in maintaining label performance and durability. These factors can limit market growth, especially for small and medium-sized manufacturers with limited resources.

Market Opportunities

Rising adoption of digital printing technologies

The increasing adoption of digital printing technologies presents significant opportunities for the primary packaging labels market. Digital printing allows for high-quality, customizable labels with shorter production times and reduced waste. This technology is particularly beneficial for small and medium-sized production runs, enabling manufacturers to offer personalized and variable data printing. The ability to quickly adapt to changing consumer preferences and market trends is driving the adoption of digital printing solutions. As technology continues to advance, it is expected to play a crucial role in enhancing efficiency and expanding market opportunities.

Growth of e-commerce and retail sectors

The rapid growth of e-commerce and retail sectors is creating new opportunities for the primary packaging labels market. The increasing volume of packaged goods being transported and delivered requires durable and high-quality labels that can withstand handling and environmental conditions. Labels are also essential for logistics, providing information such as barcodes, tracking details, and product identification. The rise of online shopping is encouraging companies to invest in innovative labeling solutions that enhance brand visibility and improve customer experience. This trend is expected to drive demand for primary packaging labels in the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42.8 Billion |

| Market Size in 2026 | USD 45.3 Billion |

| Market Size in 2034 | USD 74.6 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pressure-sensitive labels dominated the market with a 41.8% share in 2024. These labels are widely used due to their ease of application, versatility, and compatibility with various surfaces. They do not require heat or water for application, making them suitable for high-speed production lines. The growing demand for efficient labeling solutions in industries such as food and beverage is driving this segment.

Shrink sleeve labels are expected to grow at the fastest CAGR of 6.9% during the forecast period. These labels provide 360-degree coverage and enhance product aesthetics. The increasing demand for visually appealing packaging is driving the adoption of shrink sleeve labels. Technological advancements are further improving their performance and efficiency.

By Material

Plastic-based labels accounted for the largest share of 53.1% in 2024 due to their durability and resistance to moisture and chemicals. These labels are widely used in industries such as food, beverages, and personal care. The ability to maintain label integrity under various conditions is driving their adoption.

Paper-based labels are projected to grow at a CAGR of 6.2% due to increasing demand for sustainable packaging solutions. These labels are biodegradable and recyclable, making them an environmentally friendly option. The shift toward eco-friendly materials is encouraging manufacturers to adopt paper-based labels.

By Application

Food & beverage applications dominated the market with a 46.5% share in 2024. Labels play a crucial role in providing product information and enhancing brand visibility. The growing demand for packaged foods is driving the adoption of labeling solutions in this segment.

Pharmaceutical labeling is expected to grow at a CAGR of 6.8% due to increasing regulatory requirements and demand for product safety. Labels are essential for providing information such as dosage, ingredients, and safety warnings. The expansion of the pharmaceutical industry is supporting segment growth.

Primary Packaging Labels Market Segmentations

By Type

- Pressure-Sensitive Labels

- Shrink Sleeve Labels

- Glue-Applied Labels

- In-Mold Labels

By Material

- Plastic-Based Labels

- Paper-Based Labels

- Metalized Labels

By Application

- Food & Beverage

- Pharmaceutical

- Personal Care

- Industrial

Regional Analysis

North America

North America accounted for approximately 23.8% of the primary packaging labels market share in 2025 and is projected to grow at a CAGR of 5.7% during the forecast period. The region benefits from advanced packaging technologies and strong demand from the food and pharmaceutical industries. The presence of established manufacturers and increasing adoption of smart labeling solutions are driving market growth.

The United States dominates the regional market due to its large consumer base and well-developed retail sector. A key growth factor is the increasing adoption of digital printing technologies, which enable high-quality and customizable labels. This technological advancement is supporting market expansion and improving production efficiency.

Europe

Europe held a market share of around 22.6% in 2025 and is expected to grow at a CAGR of 5.5%. The region’s growth is driven by strict environmental regulations and high consumer awareness regarding sustainable packaging. Manufacturers are focusing on developing eco-friendly labeling solutions to meet regulatory requirements.

Germany is the leading country in the European market due to its strong manufacturing base and advanced packaging industry. A significant growth factor is the emphasis on sustainable materials, which is encouraging innovation in label production. This trend is supporting market growth across the region.

Asia Pacific

Asia Pacific dominated the global market with a 37.6% share in 2025 and is projected to grow at a CAGR of 6.9%. Rapid urbanization, increasing disposable income, and growing demand for packaged goods are key factors driving growth in this region. The expansion of the food and beverage industry is also contributing significantly.

China is the dominant country in the region, supported by large-scale manufacturing capabilities and government initiatives promoting industrial growth. A unique growth factor is the increasing investment in packaging technologies, which enhances production efficiency and supports market expansion.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.8% of the market share in 2025 and is expected to grow at a CAGR of 6.1%. The market is gradually expanding due to increasing demand for packaged goods and improving industrial infrastructure. Growth is also supported by rising awareness of product labeling.

The United Arab Emirates is a key contributor to regional growth due to its growing retail sector and focus on innovation. A major growth factor is the adoption of advanced labeling technologies, which improve product presentation and compliance with regulations.

Latin America

Latin America held a market share of around 8.2% in 2025 and is projected to grow at the fastest CAGR of 6.7%. Increasing urbanization and changing consumer preferences are driving demand for packaged goods and labeling solutions. The expansion of the food and beverage industry is also contributing to growth.

Brazil dominates the regional market due to its strong manufacturing sector and increasing demand for packaged products. A unique growth factor is the growth of retail distribution networks, which is driving demand for high-quality labeling solutions and supporting market expansion.

Competitive Landscape

The primary packaging labels market is moderately competitive, with key players focusing on innovation, sustainability, and technological advancements. Companies are investing in research and development to improve label quality and expand their product portfolios. Strategic partnerships and acquisitions are also common, enabling companies to strengthen their market presence.

CCL Industries Inc. is a leading player in the market, known for its extensive range of labeling solutions. The company recently introduced new sustainable label materials to meet growing demand for eco-friendly packaging. Other major players are also focusing on developing innovative solutions to remain competitive in the market.

Key Players List

- CCL Industries Inc.

- Avery Dennison Corporation

- UPM Raflatac

- Multi-Color Corporation

- Constantia Flexibles

- Huhtamaki Oyj

- Coveris Holdings S.A.

- 3M Company

- Henkel AG & Co. KGaA

- LINTEC Corporation

- Fuji Seal International, Inc.

- Brady Corporation

- SATO Holdings Corporation

- R.R. Donnelley & Sons Company

- WS Packaging Group