Pouch Packaging Market Size and Growth

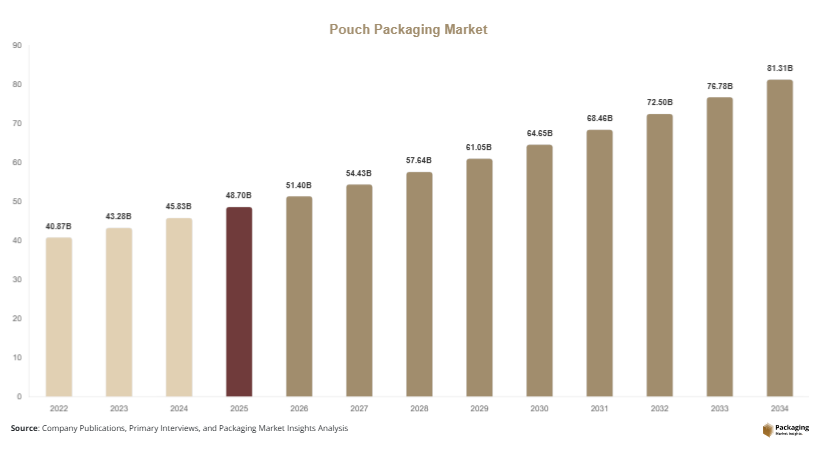

The global pouch packaging market size is estimated at USD 48.7 billion in 2025 and is projected to reach USD 51.4 billion in 2026. By 2034, the market is forecast to reach USD 81.6 billion, registering a CAGR of 5.9% during 2025–2034. Rising consumer demand for lightweight packaging, increasing shelf-life requirements, and growing adoption of convenient resealable packaging formats are supporting market growth globally. The pouch packaging market is witnessing sustained expansion as flexible packaging formats continue to gain preference across food, beverage, healthcare, personal care, and household product industries.

One of the major growth factors is the increasing shift from rigid packaging formats toward flexible pouch-based packaging due to lower transportation costs, reduced material usage, and improved storage efficiency. Compared with glass jars, rigid cans, and thick plastic containers, pouches require less raw material and occupy lower warehouse volume, making them commercially attractive across supply chains. This cost-efficiency benefit is especially valuable in food processing, beverage concentrates, and household cleaning product packaging.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.5%.

- Stand-up pouches led the type segment with a 34.7% share.

- Plastic-based materials dominated with a 61.3% share.

- Food & beverage applications led the end-use segment with 46.8% share.

- The US remained the dominant country with a market size of USD 8.4 billion in 2025 and USD 8.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Recyclable Mono-Material Pouch Structures

Sustainability-driven packaging innovation is significantly influencing the pouch packaging market, particularly through growing adoption of recyclable mono-material pouch formats. Traditional multi-layer flexible pouches often combine incompatible materials, making recycling difficult in conventional waste streams. Packaging manufacturers are now investing in polyethylene-based and polypropylene-based mono-material laminates that deliver barrier protection while improving recyclability. Large food producers are introducing recyclable stand-up pouches for snacks, frozen foods, and dry grocery products, while personal care brands are shifting refill products into recyclable pouch systems. In the coming years, wider collection infrastructure and improved film engineering are expected to accelerate adoption of recyclable mono-material pouch packaging across developed and emerging markets.

Rising Demand for Premium Printed Flexible Packaging

Digital and high-definition flexographic printing technologies are reshaping packaging aesthetics in the pouch packaging market. Brands increasingly view pouch packaging as both protective packaging and marketing media. Premium matte finishes, metallic coatings, transparent windows, tactile surfaces, and digitally personalized graphics are becoming more common in coffee, premium pet food, nutritional products, and cosmetics refill packaging. For example, regional beverage brands are using high-quality printed spouted pouches to differentiate fruit concentrates and sports nutrition products in retail channels. Over time, smart packaging integration such as QR-enabled engagement, traceability printing, and short-run customized designs will strengthen the commercial role of premium printed pouch packaging.

Market Drivers

Expansion of Packaged Food Consumption Across Urban Markets

Urbanization and changing consumer eating patterns are strongly supporting growth in the pouch packaging market. Packaged snacks, instant foods, frozen meals, sauces, condiments, baby food, and nutritional supplements increasingly rely on flexible pouch packaging because of its lightweight structure, storage convenience, and high barrier protection. Rising dual-income households and busy lifestyles continue increasing demand for packaged convenience foods globally. For instance, ready-to-eat meal kits in metropolitan markets increasingly use retort pouches instead of rigid trays because of easier handling and lower logistics cost. This shift is expected to support long-term pouch packaging demand across food supply chains.

Growth in Refill Packaging Models Across Consumer Goods

Refill packaging systems are becoming an important commercial driver for the pouch packaging market. Personal care brands, home cleaning product manufacturers, and premium cosmetics companies increasingly offer refill pouches designed to reduce packaging waste while lowering packaging cost per unit. Liquid soaps, shampoos, detergents, lotions, and cleaning concentrates are widely shifting toward pouch-based refill systems. This trend reduces plastic consumption compared with rigid bottles and supports circular packaging strategies. In coming years, broader adoption of refill stations in organized retail and direct-to-consumer refill subscriptions could significantly expand pouch packaging applications globally.

Market Restraint

Recycling Complexity in Multi-Layer Flexible Packaging

Despite strong growth, recycling limitations remain a major restraint in the pouch packaging market. Many high-performance pouches rely on layered combinations of polymers, foil barriers, inks, and adhesives designed for durability and shelf-life protection. While effective for product preservation, these mixed-material structures remain difficult to recycle using conventional municipal systems. This creates regulatory pressure, particularly in North America and Europe where packaging recovery targets are tightening. For example, snack packaging formats that combine PET, aluminum foil, and PE sealing layers often face end-of-life disposal challenges. Unless recycling infrastructure and material simplification improve rapidly, sustainability-related regulatory pressure may slow adoption in certain premium packaging categories.

Market Opportunities

Expansion of Pharmaceutical Sachet and Medical Flexible Packaging

Healthcare applications present meaningful growth opportunities for the pouch packaging market. Single-dose pharmaceutical sachets, sterile medical packaging pouches, nutraceutical powder pouches, and liquid formulation packs are increasingly being adopted because of dosage precision, portability, and product protection benefits. Healthcare packaging producers are developing high-barrier sterile flexible formats that support compliance, tamper resistance, and efficient storage. As healthcare access expands across developing economies and home-based wellness products gain popularity, pouch packaging demand in regulated medical and wellness applications is expected to rise steadily over the forecast period.

Increasing Penetration in Industrial and Agricultural Packaging

Industrial and agricultural packaging applications are creating new demand channels for flexible pouch solutions. Lubricants, specialty chemicals, water treatment compounds, crop nutrients, seeds, and powdered industrial ingredients increasingly use durable pouch formats for transport efficiency and storage convenience. Heavy-duty laminated pouches with reinforced seals and spout systems are replacing rigid containers in several industrial packaging applications. For example, agricultural micronutrient blends are increasingly sold in moisture-resistant stand-up pouch systems that reduce freight cost while improving shelf presentation. Future packaging engineering focused on puncture resistance and chemical compatibility will further expand industrial pouch adoption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.7 Billion |

| Market Size in 2026 | USD 51.4 Billion |

| Market Size in 2034 | USD 81.6 Billion |

| CAGR | 5.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

By Type

Stand-up pouches accounted for the largest share of the pouch packaging market, representing 34.7% of total revenue in 2024. Their dominance is largely attributed to structural stability, superior shelf presentation, efficient storage design, and broad application compatibility across food, beverages, personal care, pet food, and household products. Unlike flat sachets or rigid packaging formats, stand-up pouches offer enhanced merchandising visibility while maintaining lightweight packaging economics. Their ability to integrate zip-lock closures, tear notches, transparent windows, and high-quality print surfaces further supports widespread commercial adoption. Snack foods, coffee packaging, powdered nutrition products, frozen foods, and confectionery brands increasingly prefer stand-up pouches because they balance branding, preservation, and logistics efficiency. Retailers also favor these formats because of improved stacking efficiency and better shelf utilization. With continued innovation in barrier laminates, recyclable mono-material films, and premium tactile finishes, stand-up pouches are expected to maintain broad commercial leadership across packaging applications.

Spouted pouches are projected to register the fastest CAGR of 6.9% during 2025–2034, supported by rising demand for liquid convenience packaging, refill systems, and portable dispensing formats. These pouches are increasingly used for fruit purees, baby food, liquid detergents, sauces, edible oils, beverage concentrates, and skincare refill packaging because they provide controlled dispensing, leak resistance, and portability advantages. Packaging innovation is further improving spout design, tamper-proof sealing, ergonomic pouring systems, and material durability. Consumer goods brands are also shifting toward refill pouch systems using spouted designs as part of packaging waste reduction strategies. In emerging economies, spouted pouches are becoming attractive for affordable single-use and medium-volume liquid packaging formats. With rising adoption in foodservice concentrates, household cleaning products, and health beverages, spouted pouch demand is expected to expand significantly over the forecast period.

By Material

Plastic-based materials dominated the pouch packaging market, accounting for 61.3% market share in 2024. Polyethylene, polypropylene, PET laminates, nylon layers, and multi-polymer barrier structures remain widely used because they offer flexibility, durability, puncture resistance, moisture protection, and excellent seal integrity. These materials support broad commercial use in food preservation, frozen products, ready meals, pet nutrition, liquid packaging, and healthcare sachets. Plastic films also enable compatibility with high-speed filling systems, retort processing, and premium printing technologies. Their lightweight structure reduces freight cost and supports efficient large-scale packaging operations. Manufacturers continue investing in downgauging technology that reduces material thickness while maintaining performance standards. High-barrier plastic laminates remain commercially important for aroma-sensitive, oxygen-sensitive, and moisture-sensitive products where product protection directly affects shelf life and brand value.

Paper-based pouch packaging is forecast to grow at a CAGR of 6.6% through 2034, supported by sustainability targets, rising consumer preference for natural packaging aesthetics, and growing retail acceptance of fiber-based flexible packaging solutions. Brands across snacks, dry foods, coffee, premium confectionery, and personal care refill products are increasingly adopting paper-laminate pouch structures that improve recyclability while maintaining moderate barrier protection. Packaging converters are developing coated paper systems with moisture resistance, grease barriers, and improved sealing capabilities suitable for automated packaging lines. Premium organic food brands increasingly use paper-based stand-up pouches to reinforce environmentally conscious brand positioning. In the coming years, improved hybrid paper structures, compostable coatings, and stronger fiber engineering are expected to expand paper-based pouch adoption into broader consumer and retail packaging applications.

By End-Use

Food and beverage represented the largest share in the pouch packaging market, accounting for 46.8% of total market revenue in 2024. This dominance reflects broad usage in snacks, sauces, coffee, frozen foods, nutritional powders, dairy alternatives, pet treats, instant meals, and beverage concentrates. Flexible pouch packaging offers strong barrier performance, efficient storage, lower transport weight, and premium print customization, making it commercially attractive across packaged food supply chains. Retort pouches are increasingly replacing cans and rigid trays in ready meals due to easier handling and lower logistics cost. Resealable closures are also improving consumer convenience in snacks, cereals, dried fruits, and powdered beverage products. Food exporters increasingly prefer flexible packaging because reduced volume improves container utilization and lowers shipping expenses. With continued expansion of packaged food demand across emerging economies, food and beverage will remain the core end-use sector supporting long-term pouch packaging growth.

Healthcare is projected to register the fastest CAGR of 6.7% during 2025–2034, driven by rising pharmaceutical packaging demand, increasing nutraceutical consumption, and expansion of home-based wellness products. Sachets, sterile medical pouches, single-dose powder packs, diagnostic packaging, and supplement refill formats are becoming more common because flexible packaging supports portability, dose accuracy, tamper evidence, and efficient storage. Pharmaceutical manufacturers increasingly use high-barrier medical-grade pouch materials that provide contamination protection and strong sealing reliability. Growth in vitamin supplements, sports nutrition, functional wellness powders, and portable liquid healthcare products is further increasing pouch demand. In developing healthcare markets, flexible packaging is also valued for affordability and ease of distribution. Advanced sterile packaging engineering and medical compliance packaging innovation are expected to strengthen healthcare’s role as a fast-growing end-use segment.

Pouch Packaging Market Segmentations

By Type

- Stand-Up Pouches

- Flat Pouches

- Spouted Pouches

- Retort Pouches

- Vacuum Pouches

By Material

- Plastic-Based Materials

- Paper-Based Materials

- Aluminum Foil Laminates

- Bio-Based Materials

- Multi-Layer Composite Materials

By End-User

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Household Products

- Industrial Applications

Regional Analysis

North America

North America accounted for 24.6% of the global pouch packaging market share in 2025 and is projected to grow at a CAGR of 5.2% through 2034. Market growth is supported by strong packaged food consumption, advanced retail packaging standards, and increasing use of flexible refill systems across personal care and household products. Food brands increasingly favor stand-up and resealable pouch formats because they offer better shelf visibility, reduced shipping weight, and improved storage efficiency compared with rigid packaging. E-commerce expansion is also strengthening demand for lightweight durable packaging formats that reduce freight costs while protecting products during distribution.

The United States dominates the North American market. A unique growth driver is the rapid expansion of pouch packaging in meal kits, protein powders, and health-focused packaged foods. Functional nutrition products increasingly use high-barrier resealable pouches with premium printed finishes to improve brand positioning and product freshness. Retailers are also encouraging shelf-ready flexible packaging that improves merchandising efficiency. Growing consumer demand for convenience, portability, and portion-controlled packaged products is expected to maintain strong pouch packaging demand in the U.S. market.

Europe

Europe represented 22.1% market share in 2025 and is forecast to expand at a CAGR of 5.4% during the forecast period. Growth is primarily supported by sustainability regulations, premium food packaging demand, and rapid adoption of recyclable mono-material flexible packaging structures. Consumer brands are increasingly replacing conventional rigid packs with lightweight pouch formats that reduce material consumption and improve transport efficiency. Flexible refill packaging in household cleaning and personal care products is also gaining traction as retailers promote waste-reduction packaging models aligned with circular economy goals.

Germany leads the European market due to its advanced packaging conversion industry and strong adoption of eco-designed flexible packaging. A unique regional driver is the rapid commercialization of refill pouch packaging for detergents, soaps, and skincare products in mass retail and pharmacy chains. European converters are also scaling recyclable pouch film production to meet brand sustainability commitments. As packaging legislation becomes stricter, demand for compliant lightweight pouch solutions is expected to strengthen across European consumer markets.

Asia Pacific

Asia Pacific held the leading 38.2% share in 2025 and is projected to record a CAGR of 6.1% through 2034, supported by rising packaged food consumption, rapid urbanization, strong manufacturing output, and expanding middle-class consumer spending. Flexible packaging demand continues to rise in ready meals, beverages, frozen food, sauces, dairy products, and instant nutrition categories. Cost-efficient lightweight packaging formats remain attractive to manufacturers operating in high-volume consumer markets. Regional converters are also investing in digital pouch printing, retort pouch technology, and sustainable laminate development.

China remains the dominant country in Asia Pacific due to its large food manufacturing base and advanced flexible packaging conversion capacity. A unique growth factor is the rapid rise of pouch packaging in e-commerce grocery and direct-to-consumer packaged foods. Lightweight packaging reduces shipping cost and improves handling efficiency across large domestic logistics networks. In addition, export-focused packaging manufacturers continue scaling premium pouch production for global packaged food, pet food, and wellness product markets.

Middle East & Africa

Middle East & Africa accounted for 6.3% of market share in 2025 and is projected to grow at a CAGR of 5.8% over the forecast period. Demand is rising due to packaged food imports, retail modernization, increasing pharmaceutical distribution, and higher consumption of packaged household products. Flexible pouch packaging is becoming more common in powdered beverages, cooking ingredients, baby nutrition, and liquid refill packaging. Regional manufacturers are also increasing adoption of lightweight packaging to improve logistics efficiency in import-driven supply chains. Growth in organized retail channels is supporting wider penetration of branded pouch packaging across urban consumer markets.

The United Arab Emirates leads the region due to strong retail infrastructure and a growing packaging conversion sector. A unique growth driver is premium packaged food import relabeling and repacking using flexible pouch systems designed for regional consumer preferences. The country’s role as a trade and re-export hub supports demand for short-run pouch customization, multilingual packaging adaptation, and premium shelf-ready flexible packaging formats. This commercial packaging ecosystem is expected to strengthen regional pouch demand further.

Latin America

Latin America accounted for 8.8% share in 2025 and is expected to record the fastest CAGR of 6.5% during 2025–2034, supported by rising processed food demand, improving retail penetration, and increasing adoption of lightweight packaging across household and personal care products. Manufacturers are shifting toward flexible pouch formats because they reduce raw material consumption and lower transportation cost across geographically dispersed markets. Demand for stand-up pouches, refill pouches, and value-size flexible packs is increasing across beverages, sauces, snacks, and dairy alternatives.

Brazil dominates the Latin American market. A unique growth factor is strong adoption of pouch packaging in value-oriented refill products for detergents, soaps, and food condiments. Regional brands increasingly use flexible refill formats to offer cost-effective products while reducing packaging material intensity. Expanding packaged food exports and rising investment in flexible packaging conversion capacity are expected to support long-term market growth across Brazil and neighboring consumer markets.

Competitive Landscape

The pouch packaging market remains moderately consolidated, with global flexible packaging manufacturers competing through material innovation, sustainable film development, advanced barrier technology, geographic expansion, and digital printing capabilities. Amcor plc remains a leading market participant due to its strong global manufacturing footprint, diversified pouch portfolio, and active investment in recyclable flexible packaging technologies. The company recently expanded its mono-material recyclable pouch platform for food and personal care applications, strengthening its position in sustainable flexible packaging conversion.

Berry Global Inc. continues expanding lightweight film engineering and refill packaging pouch solutions aimed at consumer goods brands transitioning away from rigid packaging formats. Mondi Group is investing in paper-based pouch innovation and high-performance recyclable laminates to align with tightening sustainability regulations across Europe and North America. Sealed Air Corporation remains focused on performance packaging, food preservation pouches, and protective flexible packaging systems that improve shelf life and supply chain efficiency. Sonoco Products Company continues strengthening custom pouch manufacturing capabilities, especially in premium food packaging, healthcare flexible packaging, and specialty retail packaging segments.

Competition is increasingly shaped by circular packaging design, downgauged film structures, premium print enhancement, and packaging automation compatibility. Manufacturers with scalable sustainable material platforms and strong regional conversion networks are expected to gain competitive advantage over the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Constantia Flexibles

- Huhtamaki Oyj

- Coveris Holdings S.A.

- ProAmpac LLC

- Winpak Ltd.

- Glenroy Inc.

- Clondalkin Group

- Uflex Ltd.

- Smurfit Westrock

- TC Transcontinental Packaging