Pouch Materials For Pharmaceutical Market Size and Growth

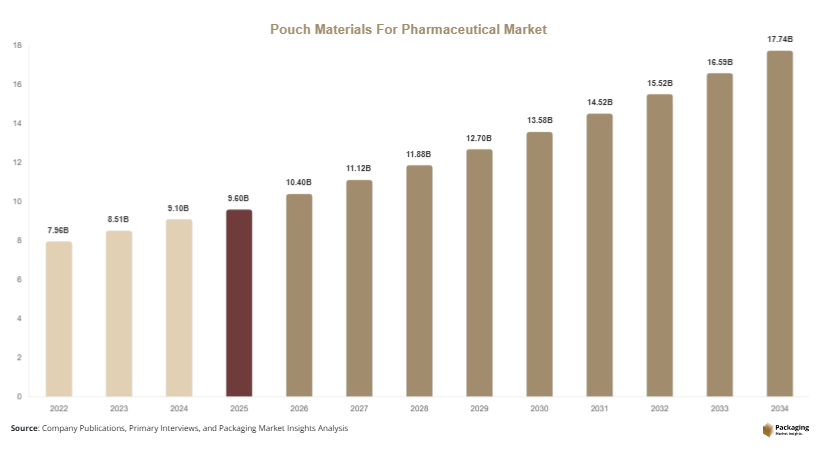

The pouch materials for pharmaceutical market is witnessing steady growth due to the increasing demand for flexible, lightweight, and high-barrier packaging solutions in the pharmaceutical industry. Pouch materials are widely used for packaging tablets, capsules, powders, liquids, and medical devices due to their ability to protect sensitive products from moisture, oxygen, light, and contamination. In 2025, the global market size is estimated at USD 9.6 billion and is projected to reach USD 10.4 billion in 2026. The market is expected to grow to approximately USD 17.8 billion by 2034, registering a compound annual growth rate (CAGR) of 6.9% during the forecast period (2025–2034).

One of the primary growth factors is the rising demand for pharmaceutical products globally, driven by increasing healthcare needs, aging populations, and the prevalence of chronic diseases. Pouch materials provide efficient and cost-effective packaging solutions that ensure product safety and extend shelf life. Another important factor is the shift toward flexible packaging formats, which offer advantages such as reduced material usage, improved portability, and enhanced patient convenience.

Key Highlights:

- Market size projected to grow from USD 9.6 billion (2025) to USD 17.8 billion (2034)

- CAGR of 6.9% during the forecast period

- Rising demand for flexible and high-barrier pharmaceutical packaging

- Growth of generic drugs and contract manufacturing organizations

- Advancements in multi-layer and high-performance pouch materials

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Use of High-Barrier Multi-Layer Films

A key trend in the pouch materials for pharmaceutical market is the growing adoption of high-barrier multi-layer films. These materials are designed to provide superior protection against moisture, oxygen, and light, which are critical factors in preserving the efficacy of pharmaceutical products. Multi-layer films combine different materials such as polyethylene, polypropylene, and aluminum foil to achieve enhanced barrier properties. This trend is particularly important for sensitive drugs, including biologics and specialty medicines, which require strict storage conditions. Manufacturers are investing in advanced film technologies to improve product performance and meet regulatory standards.

Shift Toward Patient-Centric and Convenient Packaging

Another notable trend is the increasing focus on patient-centric packaging solutions. Pharmaceutical companies are adopting pouch materials that enhance ease of use, portability, and convenience for patients. Features such as easy-tear openings, resealable closures, and single-dose packaging are gaining popularity. These innovations are particularly beneficial for elderly patients and those requiring regular medication. The trend toward patient-friendly packaging is also aligned with the growing emphasis on adherence to treatment regimens. As a result, manufacturers are developing pouch materials that combine functionality with user convenience.

Market Drivers

Growth of the Pharmaceutical Industry

The expansion of the pharmaceutical industry is a major driver of the pouch materials for pharmaceutical market. Increasing demand for medicines, driven by population growth and rising healthcare needs, is boosting the need for efficient packaging solutions. Pouch materials offer several advantages, including lightweight design, cost efficiency, and high barrier protection, making them suitable for pharmaceutical applications. The growth of the generic drug market and the increasing production of over-the-counter medicines are further driving demand for pouch materials. Additionally, the rise of global pharmaceutical trade is increasing the need for reliable packaging solutions that ensure product safety during transportation.

Rising Demand for Flexible Packaging Solutions

The shift from rigid to flexible packaging is another key driver of the market. Flexible packaging offers benefits such as reduced material usage, lower transportation costs, and improved storage efficiency. Pouch materials are increasingly being used as an alternative to traditional packaging formats such as bottles and blister packs. This trend is supported by the need for sustainable and cost-effective packaging solutions. Additionally, flexible packaging allows for innovative designs and features, enhancing product appeal and usability. The growing adoption of flexible packaging in the pharmaceutical industry is expected to drive market growth.

Market Restraint

Stringent Regulatory Requirements

Stringent regulatory requirements related to pharmaceutical packaging pose a significant restraint for the pouch materials for pharmaceutical market. Regulatory authorities require packaging materials to meet strict standards for safety, quality, and performance. Compliance with these regulations can be challenging and costly for manufacturers, particularly for those operating in multiple regions with varying standards.

The impact of this restraint is evident in the need for extensive testing and certification processes, which can increase production costs and time-to-market. For example, manufacturers must ensure that pouch materials do not interact with pharmaceutical products and maintain their integrity throughout the product lifecycle. Additionally, any changes in material composition or design may require reapproval from regulatory authorities, further complicating the process. These challenges can limit the adoption of new materials and technologies, affecting market growth.

Market Opportunities

Development of Sustainable and Recyclable Materials

The development of sustainable and recyclable pouch materials presents a significant opportunity for the market. With increasing environmental concerns, pharmaceutical companies are seeking packaging solutions that reduce environmental impact while maintaining product safety. Manufacturers are investing in research and development to create recyclable and biodegradable materials that meet regulatory standards. The adoption of sustainable packaging solutions is expected to increase as companies aim to align with environmental goals and consumer expectations.

Expansion in Emerging Markets

Emerging markets offer substantial growth opportunities for the pouch materials for pharmaceutical market. Rapid economic development, increasing healthcare expenditure, and expanding pharmaceutical industries in regions such as Asia Pacific and Latin America are driving demand for packaging materials. The growth of local manufacturing and the increasing availability of generic medicines are further supporting market expansion. Companies that establish a strong presence in these regions can benefit from rising demand and favorable market conditions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.6 Billion |

| Market Size in 2026 | USD 10.4 Billion |

| Market Size in 2034 | USD 17.8 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic-based pouch materials dominated the pouch materials for pharmaceutical market in 2024, accounting for approximately 54% of the total share. These materials are widely used due to their flexibility, durability, and cost-effectiveness. Plastic films such as polyethylene and polypropylene offer excellent barrier properties and are suitable for a wide range of pharmaceutical products. The availability of different grades and formulations further supports their widespread adoption.

Aluminum-based materials are expected to be the fastest-growing segment, with a CAGR of 7.4% during the forecast period. This growth is driven by increasing demand for high-barrier packaging solutions. Aluminum foil provides superior protection against moisture, oxygen, and light, making it suitable for sensitive pharmaceutical products. The growing demand for specialty medicines is further supporting the growth of this segment.

By Application

The tablets and capsules segment held the largest market share in 2024, accounting for approximately 48%. Pouch materials are widely used for packaging solid dosage forms due to their ability to maintain product integrity and extend shelf life. The increasing demand for over-the-counter medicines is driving the growth of this segment.

The liquid pharmaceuticals segment is expected to grow at the fastest rate, with a CAGR of 7.2%. The rising demand for liquid medicines, particularly in pediatric and geriatric populations, is driving this growth. Pouch materials provide leak-proof and flexible packaging solutions, making them suitable for liquid products.

By End-Use

The pharmaceutical companies segment dominated the market in 2024, accounting for approximately 62% of the total share. These companies rely on high-quality packaging materials to ensure product safety and compliance with regulatory standards. The increasing production of medicines is driving the demand for pouch materials in this segment.

The contract manufacturing organizations segment is expected to grow at a CAGR of 7.1% during the forecast period. The rising trend of outsourcing pharmaceutical manufacturing and packaging operations is driving this growth. CMOs require standardized and efficient packaging solutions, supporting the adoption of pouch materials.

Pouch Materials For Pharmaceutical Market Segmentations

Material Type

- Plastic

- Aluminum

- Paper

Application

- Tablets & Capsules

- Liquid Pharmaceuticals

- Powders

End-Use

- Pharmaceutical Companies

- Contract Manufacturing Organizations

Regional Analysis

North America

North America accounted for approximately 31% of the pouch materials for pharmaceutical market share in 2025 and is expected to grow at a CAGR of 6.3% during the forecast period. The region’s growth is driven by a well-established pharmaceutical industry and high demand for advanced packaging solutions. The presence of leading pharmaceutical companies and strict regulatory standards further supports market expansion.

The United States dominates the North American market due to its large pharmaceutical sector and strong focus on innovation. A unique growth factor is the increasing adoption of unit-dose packaging, which is driving demand for high-quality pouch materials.

Europe

Europe held around 26% of the market share in 2025 and is projected to grow at a CAGR of 6.1%. The region’s growth is influenced by stringent regulatory requirements and a strong emphasis on product safety. Companies are increasingly adopting advanced packaging materials to comply with these standards.

Germany is a leading country in the European market, supported by its robust pharmaceutical industry. A unique growth factor is the implementation of sustainability initiatives, encouraging the use of recyclable packaging materials.

Asia Pacific

Asia Pacific accounted for the largest market share of approximately 30% in 2025 and is expected to grow at a CAGR of 7.6%. Rapid industrialization, population growth, and increasing healthcare expenditure are key factors driving market growth in the region.

China dominates the Asia Pacific market due to its large manufacturing base and expanding pharmaceutical industry. A unique growth factor is the growth of contract manufacturing organizations, which is increasing demand for pouch materials.

Middle East & Africa

The Middle East & Africa region held around 7% of the market share in 2025 and is projected to grow at a CAGR of 6.5%. The growth is driven by increasing healthcare investments and the expansion of pharmaceutical industries.

Saudi Arabia is a key market in the region, supported by government initiatives to improve healthcare infrastructure. A unique growth factor is the increasing demand for imported pharmaceutical products, boosting the need for reliable packaging solutions.

Latin America

Latin America accounted for approximately 6% of the market share in 2025 and is expected to grow at a CAGR of 6.6%. The region’s growth is supported by increasing healthcare expenditure and the expansion of the pharmaceutical sector.

Brazil leads the Latin American market due to its large population and growing healthcare industry. A unique growth factor is the increasing production of generic medicines, which is driving demand for cost-effective packaging solutions.

Competitive Landscape

The pouch materials for pharmaceutical market is characterized by the presence of several global and regional players competing on product quality, innovation, and compliance with regulatory standards. Companies are focusing on developing advanced materials with improved barrier properties and sustainability features. Strategic partnerships and collaborations are common as companies aim to expand their market presence.

Amcor plc is considered a leading player in the market, known for its extensive product portfolio and focus on innovation. The company has recently introduced advanced multi-layer pouch materials designed to enhance product protection and sustainability. Other key players are also investing in research and development to improve material performance and meet evolving market demands. The competitive landscape is expected to remain dynamic, with companies focusing on innovation and regulatory compliance.

Key Players List

- Amcor plc

- Berry Global Group Inc.

- Sealed Air Corporation

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Mondi Group

- Sonoco Products Company

- Coveris Holdings S.A.

- Winpak Ltd.

- UFlex Ltd.

- Glenroy Inc.

- Clondalkin Group

- ProAmpac LLC

- Wipak Group

- Cosmo Films Ltd.