Post Consumer Recycled Pouch Market Size and Growth

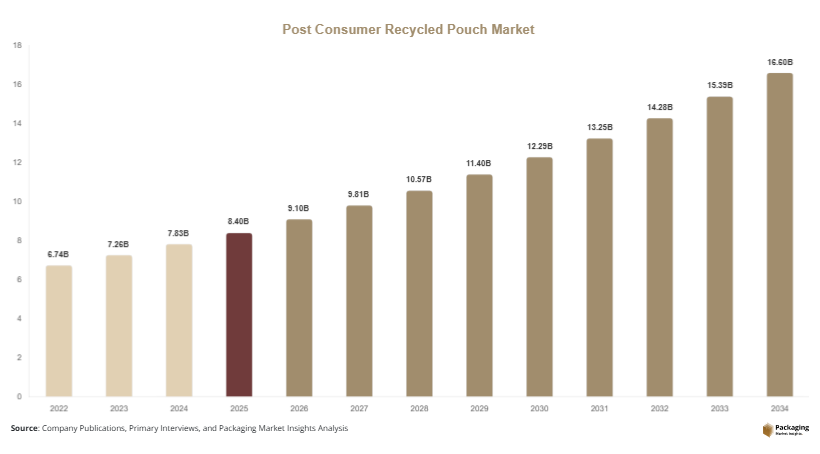

In 2025, the post consumer recycled pouch market size is estimated at USD 8.4 billion, and it is projected to reach USD 9.1 billion in 2026. By 2034, the market is expected to attain approximately USD 16.8 billion, registering a CAGR of 7.8% from 2025 to 2034. This growth reflects strong demand across food & beverage, personal care, healthcare, and industrial packaging sectors where sustainable flexible packaging is becoming a strategic priority. The post consumer recycled pouch market is witnessing steady expansion as global industries increasingly transition toward circular packaging systems and low-carbon material solutions.

Several structural factors are supporting market expansion. The first major factor is the tightening global regulatory framework around plastic waste management. Governments are introducing mandatory recycled content requirements, extended producer responsibility (EPR) systems, and bans on single-use plastics, which are directly increasing demand for post consumer recycled (PCR) pouch formats. The second factor is the rapid shift in consumer behavior, where environmentally conscious purchasing decisions are influencing brand packaging strategies. Consumers are increasingly favoring products packaged in recyclable and sustainable materials, forcing manufacturers to adopt PCR-based solutions. The third factor is technological advancement in recycling systems, including improved sorting technologies and chemical recycling innovations, which are enhancing the quality and availability of PCR resins for flexible pouch manufacturing.

Key Market Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

- Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led with a 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained dominant with USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growth of Mono-Material Recyclable Pouch Structures

The packaging industry is increasingly shifting toward mono-material recyclable pouch structures designed to improve recyclability and reduce environmental impact. Traditional multilayer laminates, which combine plastics and adhesives, are being replaced with single-polymer structures such as polyethylene and polypropylene integrated with post consumer recycled content. This transformation is driven by regulatory requirements and recyclability targets set by global brands. Mono-material pouches also allow easier integration into existing recycling streams, reducing contamination issues. Advancements in barrier coatings and extrusion technologies have enabled these structures to maintain high resistance to moisture, oxygen, and contaminants, making them suitable for food and personal care applications. This trend is reshaping flexible packaging design standards across global supply chains.

Expansion of Smart and Digitally Enhanced Sustainable Packaging

Another important trend is the integration of smart packaging technologies into post consumer recycled pouch formats. Brands are increasingly adopting digital printing techniques to reduce material waste and improve customization capabilities across regional markets. QR codes, NFC tags, and product traceability systems are being embedded into recyclable pouches to enhance consumer engagement and transparency. These features allow end users to track recycled content usage and verify sustainability claims, strengthening brand credibility. Additionally, smart packaging enables better inventory management and supply chain optimization. The combination of digital innovation and recycled materials is creating a new competitive landscape in the flexible packaging industry, where functionality and sustainability are equally important.

Market Drivers

Rising Global Regulations Supporting Circular Packaging Systems

Strict global regulations aimed at reducing plastic pollution are significantly driving the adoption of post consumer recycled pouch solutions. Governments across Europe, North America, and Asia Pacific are implementing mandatory recycled content targets and extended producer responsibility frameworks. These policies require manufacturers to increase the share of recycled materials in packaging formats, including flexible pouches. Additionally, taxes on virgin plastics and restrictions on non-recyclable packaging are increasing production costs for traditional materials, making PCR-based alternatives more attractive. Regulatory pressure is particularly strong in the European Union, where circular economy policies are shaping packaging innovation across industries. These evolving regulatory frameworks are accelerating large-scale adoption of sustainable pouch solutions.

Corporate Sustainability and ESG-Led Packaging Transformation

Corporate sustainability commitments are playing a major role in driving market growth. Global FMCG brands, retail companies, and personal care manufacturers are increasingly setting ambitious ESG targets aimed at achieving fully recyclable or reusable packaging portfolios. These commitments are encouraging procurement of post consumer recycled materials for flexible pouch manufacturing. Companies are also forming strategic partnerships with recycling firms to ensure stable supply of high-quality PCR resins. Sustainability reporting requirements are further pushing organizations to demonstrate measurable reductions in carbon emissions and plastic waste. As a result, PCR-based pouch adoption is becoming a central element of corporate sustainability strategies across global supply chains.

Market Restraint

Limited Availability and Quality Variability of Recycled Feedstock

One of the major challenges in the post consumer recycled pouch market is the inconsistent availability and quality of post consumer recycled materials. PCR feedstock often varies significantly depending on regional waste collection systems, recycling infrastructure, and sorting efficiency. This leads to fluctuations in material purity, mechanical strength, and color consistency, which directly impact pouch manufacturing quality. High-performance applications, particularly in food and healthcare packaging, require strict material standards that are difficult to maintain with inconsistent PCR supply. Additionally, developing regions often lack efficient recycling systems, further limiting the availability of high-grade recycled resins. These constraints create operational challenges for manufacturers and increase production costs.

Market Opportunities

Advancements in Chemical Recycling and High-Quality PCR Production

Chemical recycling technologies present a significant opportunity for the post consumer recycled pouch market. Unlike mechanical recycling, chemical processes break down plastics into their molecular components, enabling the production of high-purity recycled polymers that closely match virgin material performance. This advancement allows PCR materials to be used in high-barrier and sensitive applications such as pharmaceuticals and premium food packaging. As global investments in chemical recycling infrastructure increase, the availability of high-quality recycled resins is expected to improve significantly. This development will expand the application scope of PCR-based pouches and support broader industry adoption across regulated sectors.

Rapid Expansion of E-Commerce and Sustainable Packaging Demand

The growth of e-commerce platforms is creating strong demand for durable and sustainable flexible packaging solutions. Post consumer recycled pouches are increasingly being used for product shipping, food delivery, and retail packaging due to their lightweight and eco-friendly properties. Online retail companies are under pressure to reduce environmental impact while maintaining cost efficiency and product protection. Emerging economies are also witnessing rapid growth in digital commerce, increasing demand for sustainable packaging formats. This shift is encouraging manufacturers to develop innovative PCR-based pouch designs that meet both performance and environmental requirements across global supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.4 Billion |

| Market Size in 2026 | USD 9.1 Billion |

| Market Size in 2034 | USD 16.8 Billion |

| CAGR | 7.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Type

The Type segment is primarily dominated by polyethylene-based recycled materials, which accounted for approximately 34.6% share in 2024. These materials are widely used due to their flexibility, cost efficiency, and compatibility with existing pouch manufacturing systems. They are extensively used in food and personal care packaging due to their strong moisture resistance and durability. Manufacturers continue to prioritize polyethylene-based PCR materials because they allow seamless integration into high-volume production systems without major process modifications.

Polypropylene-based recycled materials represent the fastest-growing subsegment, projected to expand at a CAGR of 8.1%. Growth is driven by increasing demand for high-barrier packaging solutions that offer heat resistance and structural stability. These materials are gaining popularity in pharmaceutical and premium food packaging applications. Continuous innovation in recycling and polymer processing technologies is further enhancing material quality and expanding application scope.

Application

Food & beverage packaging dominated the application segment with a 43.1% share in 2024. This dominance is driven by high consumption of packaged foods and increasing demand for sustainable packaging alternatives. Flexible recycled pouches are widely used for snacks, beverages, dairy products, and ready-to-eat meals. The segment benefits from strong branding initiatives focused on reducing environmental impact while maintaining product quality and shelf stability.

Healthcare packaging is the fastest-growing application segment, projected to grow at a CAGR of 6.3%. Growth is supported by increasing demand for sustainable pharmaceutical packaging solutions and advancements in sterile packaging materials. Companies are gradually adopting PCR-based pouches for secondary packaging applications, ensuring compliance with environmental targets while maintaining safety standards.

End-Use

The FMCG sector dominated the end-use segment with a 48.2% share in 2024 due to large-scale consumption of packaged consumer goods. FMCG companies are leading the transition toward recycled packaging as part of their sustainability commitments. The segment benefits from high-volume demand and global distribution networks that require efficient packaging solutions.

The e-commerce segment is the fastest-growing end-use category, expanding at a CAGR of 8.6%. Growth is driven by rising online retail activity and increasing demand for sustainable shipping solutions. Companies are adopting recycled pouches to reduce packaging waste and align with environmental expectations.

Post Consumer Recycled Pouch Market Segmentations

By Material Type

- Polyethylene (PE) Recycled Pouches

- Polypropylene (PP) Recycled Pouches

- PET-Based Recycled Pouches

- Bio-Enhanced Recycled Pouches

By Application

- Food & Beverage Packaging

- Personal Care & Cosmetics Packaging

- Pharmaceutical Packaging

- Household & Cleaning Products Packaging

- Industrial Packaging

By End-User Industry

- FMCG Industry

- E-commerce Industry

- Healthcare Industry

- Retail Industry

- Industrial Sector

Regional Analysis

North America

North America accounted for approximately 26.8% of the global market share in 2025 and is projected to grow at a CAGR of 7.2% through 2034. The region’s growth is driven by strong regulatory frameworks and increasing adoption of sustainable packaging across FMCG and retail industries. Companies are actively integrating recycled content into flexible packaging to meet evolving compliance requirements.

The United States dominates the regional market due to its advanced recycling infrastructure and strong presence of packaging manufacturers. A key growth factor is the increasing implementation of state-level recycled content mandates, which are encouraging widespread adoption of PCR-based pouch formats across consumer goods industries.

Europe

Europe held around 28.5% market share in 2025, with a CAGR of 7.6% projected through 2034. The region benefits from strict environmental regulations and well-established circular economy frameworks that promote sustainable packaging adoption across industries.

Germany leads the European market due to its advanced waste management systems and strong packaging manufacturing base. A major growth factor is the European Union’s Packaging and Packaging Waste Regulation, which mandates higher recycled content integration across packaging materials.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025 and is projected to grow at a CAGR of 8.4%. The region benefits from large-scale manufacturing activity, rising consumer demand, and increasing sustainability awareness.

China remains the dominant country in the region due to strong government support for recycling infrastructure expansion. A key growth factor is the integration of circular economy principles into national industrial development strategies.

Middle East & Africa

The Middle East & Africa region accounted for 4.9% market share in 2025 and is projected to grow at a CAGR of 6.5%. The market is gradually developing with increasing awareness of sustainable packaging practices.

South Africa leads the region due to growing environmental initiatives and private sector participation in recycling programs. A key growth factor is the expansion of FMCG distribution networks requiring eco-friendly packaging solutions.

Latin America

Latin America held 2.4% market share in 2025 and is expected to grow at the fastest CAGR of 6.2%. The region is witnessing increasing adoption of sustainable packaging solutions supported by regulatory improvements.

Brazil dominates the regional market due to strong food export activity and growing packaging demand. A key growth factor is the expansion of sustainability-focused retail and packaging regulations in urban markets.

Competitive Landscape

The post consumer recycled pouch market is moderately competitive, with global packaging leaders focusing on sustainability-driven innovation, capacity expansion, and recycling integration. Key players include Amcor Plc, Berry Global Inc., Mondi Group, Sealed Air Corporation, and Huhtamaki Oyj. Among these, Amcor Plc holds a leading position due to its extensive recyclable packaging portfolio and strong global manufacturing network.

Recent strategies include expansion of mono-material pouch production, investment in advanced recycling infrastructure, and development of high-barrier sustainable packaging solutions. Companies are also forming partnerships with recycling firms to secure stable PCR material supply chains and improve production efficiency.

Key Players List

- Amcor Plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Sonoco Products Company

- Smurfit Kappa Group

- Constantia Flexibles

- ProAmpac LLC

- Winpak Ltd.

- Clondalkin Group

- Transcontinental Inc.

- Uflex Ltd.

- Glenroy Inc.