Post Consumer Recycled Plastics Food Packaging Market Size and Growth

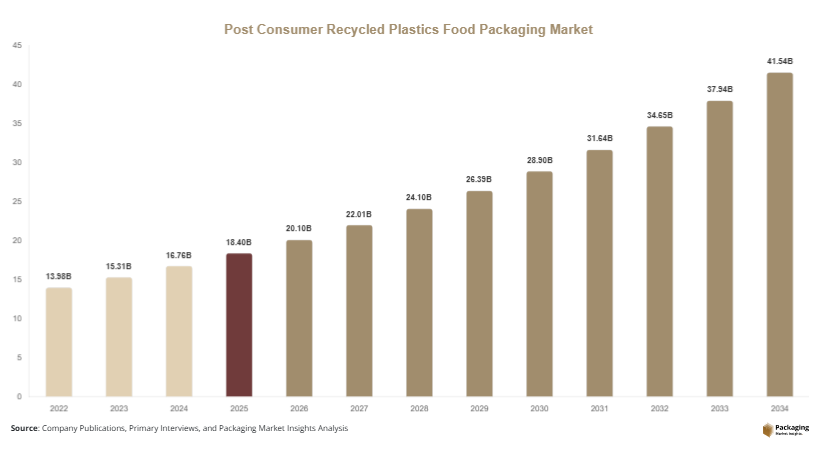

The global post consumer recycled plastics food packaging market is projected to reach USD 18.4 billion in 2025 and USD 20.1 billion in 2026, and is expected to hit USD 41.6 billion by 2034, growing at a CAGR of 9.5% (2025–2034). The post consumer recycled plastics food packaging market is gaining strong momentum as global packaging manufacturers transition toward circular economy models and sustainable material sourcing. Post-consumer recycled (PCR) plastics are derived from discarded plastic waste collected after consumer use, processed, and reintroduced into packaging applications. In food packaging, PCR plastics are increasingly used in rigid containers, trays, bottles, films, and flexible packaging formats due to their ability to reduce virgin plastic consumption while maintaining cost efficiency.

Between 2025 and 2034, the market is expected to expand steadily as regulatory frameworks tighten around single-use plastics and as food brands adopt sustainability commitments. Rising consumer awareness regarding plastic pollution and carbon footprint reduction is further accelerating demand. Retailers and packaged food manufacturers are also integrating recycled content targets into procurement strategies, which is significantly boosting adoption.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of Food-Grade Recycling Technologies

One of the most significant trends in the post consumer recycled plastics food packaging market is the rapid advancement of food-grade recycling technologies. Mechanical recycling systems are being upgraded with enhanced sorting, washing, and decontamination processes to ensure compliance with strict food safety standards. For instance, PET bottle-to-bottle recycling systems are widely deployed in Europe, enabling recycled content to be safely reused in beverage packaging. Chemical recycling is also emerging as a complementary technology, breaking down plastics into monomers for high-quality reuse. This trend is expected to improve material purity, expand application scope in direct food contact packaging, and reduce dependency on virgin polymers, thereby supporting long-term sustainability goals.

Brand-Led Sustainability Commitments

Global food and beverage brands are increasingly adopting sustainability commitments that mandate the use of PCR plastics in packaging. Major FMCG companies are redesigning packaging portfolios to include 25%–100% recycled content targets. For example, several beverage manufacturers in North America have introduced bottles made entirely from recycled PET. Retailers are also pushing suppliers to comply with sustainability labeling requirements. This trend is influencing procurement strategies and driving large-scale demand for PCR materials. In the long term, brand-driven sustainability initiatives will continue to accelerate innovation in recyclable packaging designs and strengthen closed-loop supply chains.

Market Drivers

Regulatory Push for Plastic Waste Reduction

Governments worldwide are implementing strict regulations aimed at reducing plastic waste and increasing recycled content usage in packaging. Policies such as extended producer responsibility (EPR), recycled content mandates, and plastic taxation are encouraging manufacturers to adopt PCR plastics. For example, the European Union’s packaging waste directives require increasing percentages of recycled content in plastic packaging. This regulatory pressure is directly influencing food packaging companies to transition toward sustainable alternatives, thereby accelerating market growth and boosting investments in recycling infrastructure.

Rising Demand for Sustainable Food Packaging

Consumers are increasingly prioritizing environmentally friendly packaging, leading food manufacturers to adopt PCR plastics in their product lines. The shift is particularly strong in urban retail markets, where sustainability labeling influences purchase decisions. For example, ready-to-eat meal packaging and bottled beverages are now widely produced using recycled PET and polypropylene. This demand is creating a strong pull effect across the supply chain, encouraging converters and resin producers to scale up PCR production capacity.

Market Restraint

Limited Availability of High-Quality Feedstock

One of the major restraints in the market is the inconsistent availability of high-quality post-consumer plastic waste suitable for food-grade applications. Contamination, mixed polymer streams, and inefficient collection systems reduce the yield of usable recycled material. This creates supply constraints for manufacturers aiming to meet strict food safety requirements. In regions with underdeveloped waste management infrastructure, such as parts of Africa and Southeast Asia, the challenge is more pronounced. As a result, manufacturers often face higher processing costs and dependency on imported recycled resins, limiting scalability.

Market Opportunities

Expansion of Chemical Recycling Technologies

Chemical recycling presents a major opportunity for the post consumer recycled plastics food packaging market. Unlike mechanical recycling, chemical processes can break down complex plastic waste into virgin-quality raw materials, making them suitable for high-end food packaging applications. Companies are investing in depolymerization and pyrolysis technologies to convert mixed plastic waste into usable feedstock. This opens opportunities for circular supply chains in regions with low-quality waste streams and supports broader adoption of PCR plastics in sensitive applications like dairy and baby food packaging.

Growth in Emerging Economies

Emerging economies in Asia Pacific, Latin America, and Africa offer significant growth opportunities due to increasing urbanization, rising packaged food consumption, and expanding retail infrastructure. Governments in these regions are also introducing recycling initiatives and plastic reduction policies. For instance, India and Brazil are investing in municipal recycling systems and encouraging private sector participation. As organized retail expands, demand for sustainable packaging solutions will increase, creating new market opportunities for PCR plastic suppliers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.4 Billion |

| Market Size in 2026 | USD 20.1 Billion |

| Market Size in 2034 | USD 41.6 Billion |

| CAGR | 9.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Rigid packaging dominates with a 2024 share of 42%, primarily used in bottles, containers, and trays for dairy, beverages, and ready meals. Its dominance is driven by structural strength, recyclability, and compatibility with PET and polypropylene recycling streams. Food brands prefer rigid PCR packaging due to its durability and ease of branding.

Flexible packaging is the fastest-growing subsegment with a CAGR of 10.6%. Demand is increasing due to lightweight benefits and reduced material usage. Innovations in multilayer recyclable films are expanding its use in snack foods and frozen products, supporting sustainability goals.

By Material

PET leads with a 2024 share of 38%, widely used in beverage bottles and food containers due to high recyclability and food safety compliance. Its dominance is supported by established recycling infrastructure and strong collection systems.

Recycled polypropylene is the fastest-growing material segment with a CAGR of 10.2%, driven by increasing use in microwaveable food packaging and dairy containers. Advancements in odor removal and polymer purification technologies are expanding its applications.

By End-Use

Food & beverage dominates with a 45% share in 2024, driven by bottled drinks, dairy packaging, and processed foods. Strong retail consumption and sustainability commitments from global brands support its leadership.

Healthcare packaging is the fastest-growing segment with a CAGR of 9.8%, driven by demand for sterile, recyclable packaging for medical food supplements and nutraceuticals.

Post Consumer Recycled Plastics Food Packaging Market Segmentations

By Type

- Rigid Packaging

- Flexible Packaging

- Films

- Containers

By Material

- PET (Polyethylene Terephthalate)

- Polypropylene (PP)

- Polyethylene (PE)

- Polystyrene (PS)

By End-Use

- Food & Beverage

- Healthcare Packaging

- Retail Packaging

- Household Products

Regional Analysis

North America

North America accounted for approximately 24% market share in 2025 and is projected to grow at a CAGR of 8.7% through 2034. The region benefits from advanced recycling infrastructure, strong regulatory frameworks, and high consumer awareness regarding sustainability. The market is driven by widespread adoption of recycled PET in beverage and ready-to-eat food packaging. Retailers and food brands are increasingly integrating recycled content targets into procurement strategies.

The United States dominates the regional market due to large-scale investments in chemical recycling facilities and strong corporate sustainability commitments. A key growth driver is the rapid expansion of closed-loop recycling systems, particularly in the beverage industry, where companies are introducing fully recycled bottle packaging across national distribution networks.

Europe

Europe holds around 28% market share in 2025, with a CAGR of 9.2%. The region leads in regulatory enforcement, particularly under EU circular economy policies. Strong emphasis on extended producer responsibility is pushing manufacturers to increase recycled content usage in food packaging.

Germany leads the region, driven by advanced waste segregation systems and strong collaboration between packaging companies and recyclers. A notable trend is the widespread adoption of reusable and recyclable packaging formats in supermarkets, supported by strict environmental labeling regulations.

Asia Pacific

Asia Pacific dominates with a 37.4% share in 2025 and is growing at a CAGR of 10.3%. Rapid urbanization, expanding food delivery services, and increasing packaged food consumption are driving demand. Recycling infrastructure is improving significantly, especially in China, India, and Japan.

China remains the dominant country due to large-scale recycling capacity expansion and government-led sustainability programs. A key driver is the integration of digital waste tracking systems that improve collection efficiency and increase availability of PCR feedstock for food packaging applications.

Middle East & Africa

The region accounts for 6% market share in 2025 and is projected to grow at a CAGR of 8.1%. Growth is supported by increasing urban population and rising packaged food imports. Recycling infrastructure is still developing but gradually improving through public-private partnerships.

The UAE leads the region, driven by sustainability initiatives linked to national circular economy goals. Retail expansion in urban centers is increasing demand for eco-friendly packaging solutions.

Latin America

Latin America holds 4.6% share in 2025 but is expected to grow at the fastest CAGR of 10.8%. Growth is driven by rising environmental awareness and increasing adoption of recycling regulations.

Brazil dominates the region due to strong beverage packaging demand and expanding recycling initiatives. A key driver is the growing participation of informal waste collection networks, which are being integrated into formal recycling systems to improve PCR supply chains.

Competitive Landscape

The market is moderately consolidated with key players focusing on recycling technology integration and strategic partnerships. Leading companies include Amcor plc, Berry Global Inc., Sealed Air Corporation, Sabic, and Plastipak Holdings. Amcor plc is considered the market leader due to its extensive global footprint and strong investment in recyclable packaging solutions.

Companies are adopting strategies such as capacity expansion, joint ventures with recyclers, and development of advanced food-grade PCR materials. Recent developments include new chemical recycling plants in Europe and partnerships with FMCG brands to increase recycled content usage in packaging portfolios.