Polyvinyl Chloride Packaging Film Market Size and Growth

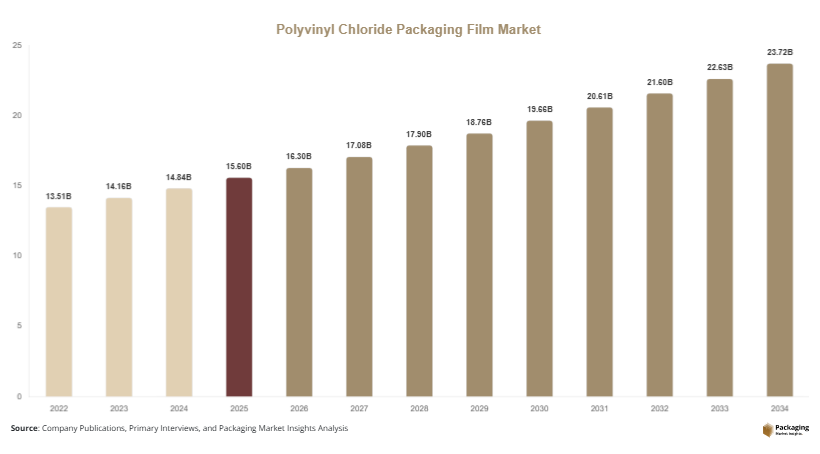

The global polyvinyl chloride packaging film market was valued at USD 15.6 billion in 2025 and is estimated to reach USD 16.3 billion in 2026. The market is projected to reach USD 24.8 billion by 2034, expanding at a CAGR of 4.8% during the forecast period from 2025 to 2034. The market continues to grow steadily due to rising demand for flexible packaging solutions across food, healthcare, consumer goods, and industrial sectors. Polyvinyl chloride packaging films are widely used because of their transparency, durability, moisture resistance, and cost-effectiveness in preserving packaged products.

The increasing demand for packaged and processed food products is one of the primary factors supporting market growth. Food manufacturers continue adopting PVC packaging films for meat, dairy, bakery, fruits, and ready-to-eat meal applications because these films offer strong sealing performance and product visibility. Rising urbanization and changing consumer lifestyles are accelerating the adoption of convenience packaging solutions globally.

Key Market Insights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 5.7%.

- Shrink films led the type segment with a 41.8% share.

- Flexible PVC materials dominated with a 56.2% share.

- Food & beverage applications led the end-use segment with 47.5% share.

- The US remained the dominant country in North America with a market size of USD 3.1 billion in 2025 and USD 3.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Demand for Sustainable and Recyclable PVC Packaging Films

The polyvinyl chloride packaging film market is increasingly witnessing demand for recyclable and sustainable packaging film solutions. Packaging manufacturers and end-use industries are focusing on reducing packaging waste and improving recyclability due to rising environmental concerns and stricter packaging regulations. This trend is encouraging manufacturers to develop advanced PVC film formulations with reduced environmental impact and improved material recovery capabilities.

Several companies are introducing lightweight PVC films that reduce raw material usage while maintaining packaging durability and product protection. Food and pharmaceutical packaging companies are also exploring recyclable multilayer film technologies to improve sustainability performance. For example, packaging manufacturers in Europe and North America are investing in closed-loop recycling systems for flexible packaging materials.

Future market growth is expected to benefit from technological advancements in recyclable film processing and eco-compatible additives. Regulatory support for sustainable packaging practices and increasing consumer awareness regarding environmentally responsible packaging are likely to accelerate the adoption of recyclable PVC packaging films across multiple industries.

Expansion of High-Barrier Multilayer Packaging Films

The growing adoption of high-barrier multilayer packaging films is becoming a significant trend within the polyvinyl chloride packaging film market. Manufacturers are increasingly developing multilayer PVC films designed to improve moisture resistance, oxygen barrier protection, and product shelf life. These films are widely used for food preservation, pharmaceutical packaging, and industrial applications requiring strong protective performance.

Food processing companies are adopting multilayer PVC films for vacuum packaging, meat preservation, and dairy packaging applications where extended shelf life is important. Pharmaceutical manufacturers are also using multilayer blister packaging films to improve product safety and prevent contamination. Several packaging suppliers are integrating advanced coating technologies into PVC film production to enhance transparency and sealing efficiency.

This trend is expected to continue as global demand for packaged food, healthcare products, and export-oriented packaging solutions increases. The development of lightweight high-barrier films compatible with automated packaging systems is likely to create additional growth opportunities for packaging film manufacturers.

Market Drivers

Growth in Packaged Food and Convenience Product Consumption

Rising demand for packaged food and convenience products is one of the primary drivers supporting the polyvinyl chloride packaging film market. Increasing urbanization, changing consumer lifestyles, and rising disposable incomes are encouraging higher consumption of ready-to-eat meals, frozen food products, bakery items, and packaged fresh produce.

PVC packaging films provide moisture resistance, transparency, and flexibility, making them suitable for food preservation and retail display applications. Food manufacturers increasingly rely on shrink and stretch PVC films for packaging meat products, fruits, vegetables, and processed foods. Retail supermarkets and food delivery businesses are additionally driving packaging demand due to increasing product transportation and storage requirements.

Countries such as China, India, Brazil, and Indonesia are witnessing strong growth in packaged food consumption due to expanding middle-class populations and rapid retail sector development. Several food processing companies are investing in automated packaging systems compatible with advanced PVC films to improve production efficiency and packaging quality. These factors continue to create strong long-term growth opportunities for market participants.

Increasing Pharmaceutical and Healthcare Packaging Demand

The expansion of pharmaceutical manufacturing and healthcare packaging industries is significantly supporting the growth of the polyvinyl chloride packaging film market. PVC films are extensively used in pharmaceutical blister packaging, medical device packaging, and healthcare product wrapping because they offer lightweight protection, product visibility, and strong barrier performance.

Growing healthcare expenditure, rising medicine consumption, and increasing demand for over-the-counter drugs are accelerating packaging film demand globally. Pharmaceutical manufacturers continue investing in high-quality blister packaging materials to improve dosage protection and extend product shelf life. PVC films are widely preferred for tablet and capsule packaging applications because they provide effective sealing and compatibility with automated blister packaging machinery.

For example, pharmaceutical manufacturing expansion across India, China, Germany, and the United States is supporting higher consumption of medical-grade PVC packaging films. The increasing focus on product traceability, tamper resistance, and contamination prevention is expected to strengthen future demand for advanced pharmaceutical packaging films worldwide.

Market Restraint

Environmental Concerns and Regulatory Restrictions on PVC Usage

Environmental concerns related to plastic waste generation and PVC disposal remain major restraints for the polyvinyl chloride packaging film market. Governments and environmental organizations across several countries are implementing stricter regulations regarding single-use plastics and non-recyclable packaging materials. These regulations are creating challenges for manufacturers relying heavily on conventional PVC packaging products.

PVC films can face recycling limitations due to mixed-material compositions and additive usage. Concerns regarding chlorine content and emissions during disposal processes have also increased scrutiny around PVC packaging applications. Several food and consumer goods companies are shifting toward alternative biodegradable or paper-based packaging materials to meet sustainability targets and improve environmental performance.

For example, packaging regulations in parts of Europe are encouraging reduced usage of conventional plastic packaging materials in retail applications. Consumer preference for sustainable packaging products is additionally pressuring manufacturers to invest in recyclable film technologies and alternative materials. These factors may increase production costs and slow adoption of traditional PVC packaging films across environmentally sensitive markets.

Despite these challenges, manufacturers continue investing in recyclable PVC formulations and lightweight film technologies to improve sustainability and maintain market competitiveness. Long-term market growth will depend on balancing packaging performance requirements with evolving environmental compliance standards.

Market Opportunities

Expansion of E-Commerce and Retail Packaging Applications

The rapid expansion of e-commerce and organized retail sectors is creating substantial opportunities for the polyvinyl chloride packaging film market. Online retail companies require durable and lightweight packaging materials capable of protecting products during transportation and storage operations. PVC shrink and stretch films are increasingly used for product bundling, tamper resistance, and secondary packaging applications in logistics and retail distribution.

Retail supermarkets and e-commerce companies are adopting advanced packaging films to improve product presentation, handling efficiency, and inventory management. Packaging manufacturers are responding by developing stronger and more flexible PVC films suitable for automated high-speed packaging systems. Several logistics and retail packaging providers across Asia Pacific and Latin America are increasing investments in protective packaging solutions due to rising online shopping activities.

Future opportunities are expected in temperature-sensitive packaging, warehouse automation systems, and retail-ready packaging formats. Growing demand for cost-efficient and lightweight packaging materials across global supply chains is likely to strengthen market demand over the forecast period.

Growth in Medical and Pharmaceutical Export Packaging

Increasing pharmaceutical exports and rising medical product manufacturing activities are creating new growth opportunities for the polyvinyl chloride packaging film market. Pharmaceutical companies require secure and moisture-resistant packaging materials capable of protecting medicines during international transportation and long-term storage.

PVC films are widely used in pharmaceutical blister packs, medical device wrapping, and sterile packaging applications due to their strong barrier properties and compatibility with automated packaging machinery. Several pharmaceutical manufacturers across India, China, and Europe are expanding production capacities for export-oriented healthcare products, increasing demand for advanced packaging materials.

Future growth opportunities are expected in biologics packaging, temperature-controlled healthcare packaging, and high-barrier medical packaging films. Packaging companies investing in medical-grade recyclable PVC films and anti-contamination packaging technologies are likely to benefit from increasing global pharmaceutical trade and healthcare infrastructure expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.6 Billion |

| Market Size in 2026 | USD 16.3 Billion |

| Market Size in 2034 | USD 24.8 Billion |

| CAGR | 4.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Shrink films dominated the polyvinyl chloride packaging film market in 2024 with a market share of 41.8%. Shrink films are widely used in food packaging, beverage bundling, retail packaging, and industrial product protection because they provide strong sealing performance, transparency, and tamper resistance. Manufacturers prefer shrink films for packaging applications requiring improved shelf display and transportation stability. Food and beverage companies extensively use PVC shrink films for bottled drinks, packaged meat products, bakery items, and frozen foods due to their cost efficiency and flexibility. Several retail packaging companies are also adopting automated shrink wrapping systems to improve packaging productivity and reduce packaging waste. Increasing supermarket expansion and growing demand for retail-ready packaging solutions continue supporting the dominance of shrink films across global packaging operations.

Stretch films are expected to witness the fastest CAGR of 5.9% during the forecast period due to rising logistics and industrial packaging requirements. Stretch films are increasingly used for pallet wrapping, warehouse storage, and transportation packaging because they improve load stability and reduce product damage during shipping operations. The growth of e-commerce and global trade activities is significantly increasing demand for lightweight and flexible protective packaging materials. Packaging companies are developing advanced stretch films with higher puncture resistance and improved elasticity to support automated logistics systems. Several manufacturers in Asia Pacific and North America are investing in recyclable stretch film technologies to address sustainability concerns. Future growth is expected to benefit from warehouse automation expansion and increasing demand for secure secondary packaging solutions across industrial sectors.

By Material

Flexible PVC materials accounted for the largest market share of 56.2% in 2024 due to their versatility, transparency, and strong sealing properties. Flexible PVC films are widely used across food packaging, pharmaceutical blister packaging, consumer goods wrapping, and industrial packaging applications. Their lightweight characteristics and moisture resistance make them suitable for both retail and transportation packaging operations. Food processing companies extensively use flexible PVC materials for fresh produce packaging, meat wrapping, and bakery applications where product visibility and shelf life are important. Pharmaceutical manufacturers additionally rely on flexible PVC films for blister packaging due to their compatibility with automated packaging machinery. The growing demand for convenience packaging and lightweight flexible packaging solutions continues supporting segment dominance across global packaging industries.

Recyclable PVC formulations are projected to grow at the fastest CAGR of 6.1% during the forecast period due to increasing environmental awareness and packaging sustainability initiatives. Packaging manufacturers are investing in recyclable film technologies to comply with changing environmental regulations and reduce plastic waste generation. Several companies are introducing recyclable multilayer films and eco-compatible additives designed to improve packaging recyclability without reducing product protection performance. Food, pharmaceutical, and consumer goods companies across Europe and North America are increasingly adopting recyclable packaging materials to support sustainability goals. Future growth opportunities are expected in bio-based additives, lightweight recyclable films, and circular economy packaging systems. Technological advancements in recycling infrastructure and sustainable packaging innovation are likely to accelerate demand for recyclable PVC formulations worldwide.

By End-Use

Food & beverage applications dominated the polyvinyl chloride packaging film market in 2024 with a market share of 47.5%. PVC packaging films are extensively used in food preservation, retail display packaging, beverage bundling, and frozen food packaging because they offer strong sealing performance and product visibility. Food manufacturers continue adopting PVC films for fresh produce, dairy products, bakery goods, and processed foods due to increasing consumer demand for convenience and packaged food products. Retail supermarkets and food distribution companies additionally rely on PVC shrink films for transportation stability and shelf-ready packaging applications. The rapid expansion of food processing industries across Asia Pacific and Latin America continues supporting segment dominance. Increasing investments in automated food packaging systems and high-barrier packaging technologies are also strengthening long-term demand for PVC packaging films.

Pharmaceutical packaging is expected to witness the fastest CAGR of 6.3% during the forecast period due to rising medicine production and healthcare packaging requirements. PVC films are widely used in pharmaceutical blister packaging because they provide moisture resistance, dosage protection, and compatibility with automated packaging systems. Pharmaceutical companies are increasingly investing in advanced blister packaging technologies to improve product safety and regulatory compliance. Several healthcare packaging manufacturers are introducing medical-grade recyclable PVC films designed for improved sustainability and contamination prevention. Future demand is expected to increase due to expanding pharmaceutical exports, rising healthcare expenditure, and growing over-the-counter medicine consumption. Technological advancements in smart pharmaceutical packaging and anti-counterfeiting solutions are likely to create additional opportunities for packaging film manufacturers.

Polyvinyl Chloride Packaging Film Market Segmentations

By Type

- Shrink Films

- Stretch Films

- Cling Films

- Barrier Films

By Material

- Flexible PVC Materials

- Rigid PVC Materials

- Recyclable PVC Formulations

By End-User

- Food & Beverage Packaging

- Pharmaceutical Packaging

- Consumer Goods Packaging

- Industrial Packaging

- Retail Packaging

Regional Analysis

North America

North America accounted for 26.8% of the global polyvinyl chloride packaging film market share in 2025 and is projected to grow at a CAGR of 4.6% during the forecast period. The region benefits from strong demand for packaged food products, pharmaceutical packaging expansion, and advanced retail infrastructure. Food processing companies across the United States and Canada continue investing in high-performance packaging films designed to improve shelf life and transportation efficiency. Increasing demand for shrink films and protective packaging solutions in logistics and consumer goods sectors also contributes to regional market growth. The presence of advanced packaging technology providers and large-scale retail distribution networks supports consistent consumption of PVC packaging films across industrial and commercial applications.

The United States remained the dominant country within North America due to strong pharmaceutical manufacturing activities and increasing demand for convenience food packaging. One major growth driver is the rapid expansion of e-commerce packaging applications requiring lightweight and flexible protective packaging materials. Retailers and logistics companies are increasingly using shrink and stretch PVC films for product bundling and shipment protection. Several packaging manufacturers in the country are additionally investing in recyclable film technologies to address sustainability concerns. Canada is also witnessing rising adoption of advanced food-grade packaging films across dairy and frozen food applications.

Europe

Europe represented 23.7% of the global polyvinyl chloride packaging film market share in 2025 and is expected to expand at a CAGR of 4.5% through 2034. The region is characterized by strong regulatory oversight, rising sustainable packaging initiatives, and advanced pharmaceutical packaging industries. Food packaging manufacturers across Germany, France, Italy, and the United Kingdom are increasingly adopting high-barrier PVC films for processed food and healthcare packaging applications.

Germany emerged as the dominant market in Europe because of its strong industrial packaging sector and advanced packaging machinery manufacturing capabilities. One unique growth driver is the increasing development of recyclable flexible packaging materials compatible with circular economy goals. German packaging companies are investing in multilayer recyclable PVC film technologies for food and pharmaceutical applications. France is also witnessing growing demand for retail-ready packaging solutions in the cosmetics and personal care sectors. The region’s focus on packaging innovation and material efficiency continues supporting stable market expansion despite increasing environmental regulations.

Asia Pacific

Asia Pacific dominated the polyvinyl chloride packaging film market with a 38.6% share in 2025 and is projected to grow at a CAGR of 5.4% during the forecast period. Rising industrialization, increasing packaged food consumption, and rapid pharmaceutical manufacturing expansion are key growth factors supporting regional market development. Countries such as China, India, Japan, and South Korea continue witnessing strong investments in flexible packaging production and food processing industries.

China remained the dominant country in the region due to its large manufacturing base and strong demand for consumer packaging materials. One important growth driver is the expansion of organized retail and food delivery services requiring cost-efficient packaging films. Chinese packaging manufacturers are increasing production capacities for shrink films and multilayer packaging materials to support domestic and export demand. India is additionally emerging as a major market because of growing pharmaceutical exports and rising packaged food consumption. Southeast Asian countries continue investing in retail modernization and industrial packaging infrastructure, further strengthening regional demand.

Middle East & Africa

The Middle East & Africa accounted for 5.1% of the global polyvinyl chloride packaging film market share in 2025 and is forecast to grow at a CAGR of 4.9% through 2034. Increasing food imports, healthcare investments, and retail sector development are contributing to regional market growth. Packaging demand is rising steadily due to expanding supermarket chains, pharmaceutical distribution activities, and industrial product packaging requirements across Gulf countries and South Africa.

Saudi Arabia remained the dominant market within the region because of increasing investments in food processing and pharmaceutical manufacturing industries. One major growth driver is the growing adoption of temperature-resistant packaging films for food preservation and healthcare logistics applications. Retailers and packaging suppliers are increasingly using advanced PVC shrink films for product display and transportation efficiency. The United Arab Emirates is additionally witnessing growth in luxury consumer goods packaging and retail packaging automation. South Africa continues experiencing steady demand for protective packaging films used in agricultural exports and industrial applications.

Latin America

Latin America held 5.8% of the global polyvinyl chloride packaging film market share in 2025 and is projected to register the fastest CAGR of 5.7% through 2034. Rising urbanization, increasing packaged food demand, and expanding retail distribution networks are supporting regional market growth. Countries such as Brazil, Mexico, Argentina, and Colombia are witnessing increased investments in food processing, pharmaceutical production, and flexible packaging manufacturing activities.

Brazil emerged as the dominant market within Latin America due to strong packaged food consumption and retail sector expansion. One important growth driver is the increasing use of shrink packaging films in beverage and consumer goods distribution. Brazilian food and beverage manufacturers are adopting advanced PVC packaging films to improve product visibility and transportation efficiency. Mexico is also experiencing rising pharmaceutical packaging demand due to expanding medicine production and export activities. Government support for industrial manufacturing and retail modernization programs continues supporting long-term regional market growth.

Competitive Landscape

The polyvinyl chloride packaging film market is moderately competitive with the presence of global packaging film manufacturers focusing on sustainable packaging technologies, high-barrier film development, and regional production expansion. Companies continue investing in recyclable packaging solutions, multilayer film technologies, and automated packaging compatibility to strengthen market competitiveness.

Berry Global Inc. is considered one of the leading companies in the market due to its broad flexible packaging portfolio and strong global manufacturing presence. The company continues investing in recyclable PVC film technologies and lightweight packaging innovations.

Amcor plc focuses on sustainable packaging solutions for food and pharmaceutical applications. Sealed Air Corporation continues expanding protective packaging film production capacities for retail and logistics applications. Mondi plc is increasing investments in recyclable flexible packaging technologies. Winpak Ltd. continues strengthening pharmaceutical and food packaging film capabilities through material innovation and advanced barrier technologies.

Manufacturers are increasingly collaborating with food processing companies, pharmaceutical producers, and retail packaging providers to develop customized packaging film solutions designed for high-speed automated packaging environments.

Key Players List

- Berry Global Inc.

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Winpak Ltd.

- Coveris Holdings

- Klockner Pentaplast

- Toray Industries

- Bemis Company

- Constantia Flexibles

- Cosmo Films

- Inteplast Group

- Polyplex Corporation

- RKW Group

- Taghleef Industries